|

市場調査レポート

商品コード

1403971

インターベンショナル神経学機器:市場シェア分析、産業動向と統計、2024年~2029年の成長予測Interventional Neurology Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| インターベンショナル神経学機器:市場シェア分析、産業動向と統計、2024年~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

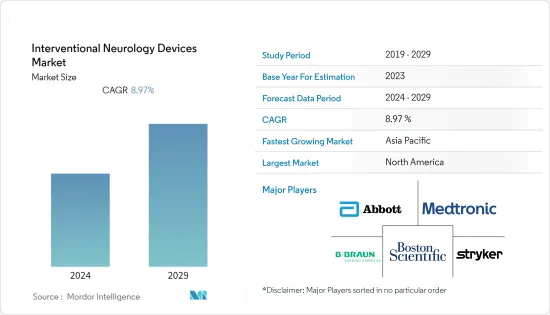

インターベンショナル神経学機器市場は、予測期間中にCAGR 8.97%を記録すると予測されています。

COVID-19は、現在進行中の研究活動に影響を与えた診断および治療プロセスの制限により、脳関連障害を持つ人々に大きな影響を与えました。例えば、2021年2月にPubMedで発表された研究によると、重度のCOVID-19患者は高いDダイマー値を示し、凝固系状態の変化を示唆しました。さらに、ICUに入院したCOVID-19患者は、急性肺塞栓症、虚血性脳卒中、深部静脈血栓症、全身性動脈塞栓症などの重大な血栓性合併症を示しました。したがって、パンデミック期間中はインターベンショナル神経学機器に対する需要が高く、市場成長に大きな影響を与えました。COVID-19関連の規制が緩和されたため、介入型神経学機器の需要に関してはパンデミック前の状態に戻った。さらに、COVID後の神経学的合併症や新製品の承認・発売により、市場は今後数年間で大きな成長を記録すると考えられています。

神経疾患の罹患率の増加や低侵襲治療の採用増加といった要因が、市場の成長を後押しする可能性が高いです。例えば、2022年に発表された英国てんかん協会のデータによると、英国に住むてんかん患者は約60万人で、約100人に1人の割合です。毎日87人がてんかんと診断されると予想されます。同国ではてんかん患者数が多いため、インターベンショナル神経学機器に対する需要が増加しており、市場成長に寄与しています。同様に、パーキンソン財団の2022年最新情報によると、米国では約100万人がパーキンソン病(PD)を患っています。この数は2030年までに120万人に増加すると予想されています。パーキンソン病は、アルツハイマー病に次いで2番目に多い神経変性疾患です。したがって、神経疾患の有病率の高さが市場の成長を後押しすると考えられます。

加えて、製品償還などの最近の市場開拓が大きな成長につながると思われます。例えば、2021年6月、Terumo France/EuropeとMicroVention Europeは、Roadsaver頸動脈ステントシステムの償還を受けました。これは、フランス国家衛生局(HAS)からの肯定的な評価によるもので、同デバイスの治療上の有益性が強調されています。このようなイニシアチブは市場を押し上げると思われます。同様に、2022年9月、革新的な治療に焦点を当てた世界のヘルスケア企業であるPenumbra, Inc.は、同社のRED再灌流カテーテルがCEマーク(Conformite Europeenne)を取得し、欧州で販売されていることを公表しました。このカテーテルは同社のPenumbraシステムの一部です。同システムは、急性虚血性脳卒中(AIS)患者の血流を回復させるための完全に統合された機械的吸引式血栓除去システムです。また、2021年3月、イノベーティブ・カーディオキュラー・ソリューションズ(ICS)は、経カテーテル大動脈弁置換術(TAVR)を受ける患者を対象に、次世代型EMBLOK塞栓防止システムを使用した欧州の臨床例から良好な結果を報告しました。

このため、神経疾患の増加や製品の上市・承認の急増により、調査対象市場は予測期間中に大きな成長が見込まれます。しかし、新技術を採用するための規制機関の厳しい規則やデバイスの高コストが市場成長の妨げになると予想されます。

インターベンショナル神経機器市場の動向

神経血栓摘出装置セグメントは予測期間中に大幅な成長が見込まれる

神経血栓除去装置は、機械的技術、レーザー技術、超音波技術、またはこれらの技術の組み合わせによって、脳微小血管系内の血栓を回収または破壊することを目的としています。虚血性急性脳卒中は、副作用と高い健康負担を伴う。神経血栓除去装置は、機能制限を含む治療を受ける患者に推奨されます。現在利用可能な神経血栓摘出装置は、急性虚血性脳卒中患者に興味深い治療選択肢を提供します。神経血栓摘出装置セグメントは、予測期間中に大きな成長を示す可能性が高いです。これは、神経疾患の増加や研究開発と相まって神経血栓摘出装置の発売が増加するなどの要因によるものです。

さらに、インドのような国々では交通事故の件数が年々増加しており、交通事故によるTBIの課題に直面しています。例えば、2022年8月に発表された国家犯罪記録局のデータによると、インドにおける交通事故件数は2020年の36万8,828件から2021年には42万2,659件に増加しています。さらに、インド頭部外傷財団(Indian Head Injury Foundation)が2021年に発表した報告書によると、全国で毎年100万人以上が重度の頭部外傷に苦しんでおり、インドにおけるTBIの約60%は交通事故が原因です。したがって、与えられた統計を観察すると、インドでTBIを引き起こす交通事故が増加し、予測期間中に神経血栓摘出装置の成長に大きく貢献すると考えられています。

さらに、神経血栓除去装置は、迅速な再建の成功、太い血管の治療効率の向上、出血イベントのリスクの低下など、薬理学的血栓溶解療法を超える多くの潜在的な利点を提供します。神経血栓摘出装置の導入は市場シェアの拡大につながり、市場を牽引します。例えば、2021年1月、Vesalioは、神経血管血栓除去術の段階を拡大する近傍の血管から血栓を除去するためのFDA 510k承認と4番目のCE承認を取得しました。同様に、2022年2月、MicroPort NeuroTech Limitedは、自社開発のNeurohawk Stent Thrombectomy Device(Neurohawk)について、中国国家医薬品監督管理局(NMPA)から販売承認を取得しました。ニューロホークは、血管内の大きな血栓を除去する血管内侵襲的血栓除去術に使用される、回収可能で自己拡張可能な血栓ステント回収器です。

したがって、神経疾患の増加、製品の上市、いくつかの製品の承認により、研究セグメントは予測期間中に大きく成長すると予想されます。

北米が予測期間中に大きな市場シェアを占めると予測される

北米は、アルツハイマー病、パーキンソン病などの神経変性疾患の負担の増加、製品の上市、低侵襲治療に対する需要の増加などの要因により、調査市場において大きな成長が見込まれています。例えば、北米における神経疾患の増加は、市場の主要促進要因の一つです。米国脳損傷協会が2021年3月に発表した報告書によると、年間約350万人の米国人が外傷性脳損傷に苦しんでいます。また、年間約280万人が外傷性脳損傷を負い、約28万人が入院を余儀なくされていることも報告されています。さらに2022年、Heart &Stroke誌はCanadian Journal of Neurological Sciences誌に新たな研究結果を発表し、カナダにおける脳卒中の年間発生率が10万8,707人、つまり約5分に1人に増加したことを明らかにしました。

さらに、2022年1月にCDCが発表した報告書によると、2021年には0~17歳の子供の約0.6%が活動性てんかんでした。また、同出典によると、2021年には米国で約47万人の小児が活動性てんかんを、約300万人の成人が活動性てんかんを有していました。さらに、米国における高齢者のてんかん発症率は、年間10万人当たり240人に上ります。したがって、てんかんの有病率の上昇は、介入型神経学機器に対する需要を促進し、市場成長を増加させる。

さらに、製品発売の増加、主要企業による戦略的活動、政府のイニシアティブや啓発キャンペーンが市場成長を促進すると予想されます。例えば、2022年10月、血管・介入神経学会は40秒間の脳卒中啓発課題を公表しました。この課題では、各自が安全にできる範囲で腕立て伏せをする40秒間の動画を作成することが求められました。このような課題によって、人々は自分の健康についてより慎重になり、それによって市場の成長が促進されます。

従って、神経疾患や啓発プログラムの増加に伴い、北米は予測期間中に大きな成長を遂げることが予想されます。

インターベンショナル神経学機器産業の概要

インターベンショナル神経学機器市場は細分化されています。世界の主要企業が介入神経学機器の大半を製造しています。より多くの研究資金と優れた流通システムを持つ市場リーダーが、市場での地位を確立しています。市場の主要企業は、アボット、BブラウンSE、メドトロニック、ボストン・サイエンティフィック・コーポレーション、ストライカー・コーポレーションです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 神経疾患の発生率の増加

- 低侵襲治療に対する需要の高まり

- 市場抑制要因

- デバイスの高コスト

- 厳しい規制シナリオ

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-米ドル)

- 製品タイプ別

- 脳バルーン血管形成術およびステント留置システム

- 頸動脈ステント

- 塞栓防止システム

- 神経血栓除去装置

- 動脈瘤コイリングおよび塞栓装置

- マイクロカテーテル

- ガイドワイヤー

- 脳バルーン血管形成術およびステント留置システム

- 用途別

- 動脈狭窄

- 虚血性脳卒中

- 脳動脈瘤

- 静脈狭窄

- その他

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Abbott

- B. Braun SE

- Boston Scientific Corporation

- Johnson & Johnson

- Medtronic

- Merit Medical Systems.

- Penumbra, Inc.

- Stryker Corporation

- Terumo Corporation

- Integer Holdings Corporation

- Canon Inc.

- MicroPort Scientific Corporation

第7章 市場機会と今後の動向

The interventional neurology devices market is anticipated to register a CAGR of 8.97% over the forecast period.

COVID-19 significantly impacted people with brain-related disorders due to limitations in the diagnostic and therapeutic processes that influenced ongoing research activities. For example, according to a study published in February 2021 in PubMed, patients with severe COVID-19 demonstrated a higher D-dimer level, suggesting an altered coagulation system state. Furthermore, the ICU-admitted COVID-19 patients showed significant thrombotic complications, including acute pulmonary embolism, ischemic stroke, deep-vein thrombosis, and systemic arterial embolism. Hence, the demand for interventional neurology devices was high during the pandemic, significantly impacting the market growth. The studied market reached its pre-pandemic nature regarding demand for interventional neurology devices as COVID-19-related restrictions were eased. Moreover, the market is believed to be registering significant growth in the coming years due to post-COVID neurological complications and new product approvals and launches.

Factors such as an increase in the incidence of neurological diseases and a rise in the adoption of minimally invasive treatment will likely fuel the market growth. For instance, as per the British Epilepsy Association data published in 2022, there were about 600,000 people with epilepsy living in the UK, around one in every 100 people. Every day, 87 people are expected to be diagnosed with epilepsy. With the high number of people living with epilepsy in the country, the demand for interventional neurology devices is increasing, contributing to market growth. Similarly, according to the 2022 update from the Parkinson's Foundation, nearly one million people in the United States were living with Parkinson's disease (PD). This number is expected to rise to 1.2 million by 2030. Parkinson's is the second-most common neurodegenerative disease after Alzheimer's disease. Hence, the high prevalence of neurological disease is likely to boost the market growth.

Additionally, the recent developments in the market, such as product reimbursement, will lead to significant growth. For instance, in June 2021, Terumo France/Europe and MicroVention Europe received reimbursement for the Roadsaver carotid stent system due to the positive assessment from the French National Authority for Health (HAS), highlighting the device's therapeutic benefit. Such initiatives will boost the market. Similarly, in September 2022, Penumbra, Inc., a global healthcare company focused on innovative therapies, publicized that its RED Reperfusion Catheters secured CE Mark (Conformite Europeenne) and are available in Europe. The catheters are part of the company's Penumbra System. It is a fully integrated mechanical aspiration thrombectomy system to restore blood flow in acute ischemic stroke (AIS) patients. Also, in March 2021, Innovative Cardiovascular Solutions (ICS) reported positive results from European clinical cases using the next generation of the EMBLOK Embolic Protection System in patients undergoing transcatheter aortic valve replacement (TAVR).

Therefore, due to the increase in neurology diseases and a surge in product launches and approvals, the studied market is expected to witness significant growth over the forecast period. However, the strict rules of regulatory bodies for adopting new technologies and the high cost of devices are expected to hinder the market's growth.

Interventional Neurology Devices Market Trends

Neuro Thrombectomy Devices Segment is Expected to Show Significant Growth Over the Forecast Period

A neurothrombectomy device is intended to retrieve or destroy blood clots in the cerebral microvasculature by mechanical, laser, ultrasound technologies, or a combination of technologies. Ischemic acute stroke is associated with side effects and higher health burdens. Neurothrombectomy equipment is recommended for patients receiving treatment that may include limited functionality. The currently available neuro-thrombectomy machines offer interesting treatment options to patients with acute ischemic stroke. The neuro-thrombectomy device segment will likely witness significant growth over the forecast period. It is due to factors such as an increase in neurological diseases and a rise in neuro-thrombectomy device launches coupled with research and development.

Moreover, countries like India are facing the challenge of TBI caused by road accidents, as the number of road accidents in these countries is increasing yearly. For instance, as per the data by National Crime Records Bureau published in August 2022, the number of road accidents in India increased from 3,68,828 in 2020 to 4,22,659 in 2021. Furthermore, other data from the Indian Head Injury Foundation published in its 2021 report stated that over one million people across the country suffer from severe head injuries every year, and around 60% of TBI in India are caused by road accidents. Hence, observing the given statistics, it is believed that increasing road accidents in India causing TBIs will contribute significantly to the growth of neuro-thrombectomy devices over the forecast period.

Furthermore, neurothrombectomy machines offer many potential benefits beyond pharmacologic thrombolysis, including the success of rapid reconstruction, improved efficiency in treating large vessels, and a lower risk of bleeding events. Introducing neurothrombectomy devices will lead to an increase in market share, thus driving the market. For example, in January 2021, Vesalio received the FDA 510k approval and its 4th CE approval to remove a thrombus from nearby blood vessels that expand the stage of neuro-vascular thrombectomy. Similarly, in February 2022, MicroPort NeuroTech Limited received marketing approval from China's National Medical Products Administration (NMPA) for its self-developed Neurohawk Stent Thrombectomy Device (Neurohawk). Neurohawk is a retrievable, self-expandable clot stent retriever used in endovascular invasive thrombectomy procedures to remove large clots in blood vessels.

Hence, with increased neurology diseases, product launches, and several product approvals, the studied segment is expected to grow significantly over the forecast period.

North America Anticipated to Hold a Significant Market Share Over the Forecast Period

North America is expected to witness significant growth in the studied market owing to factors such as the increasing burden of neurodegenerative diseases like Alzheimer's, Parkinson's disease, etc., product launches, and increasing demand for minimally invasive treatment. For instance, the increasing number of neurological disorders in North America is one of the major drivers for the market. According to the report published by the Brain Injury Association of America in March 2021, around 3.5 million Americans yearly suffer from traumatic brain injuries. The same source also reported that about 2.8 million people sustain traumatic brain injuries annually, with some 280,000 resulting in hospitalizations. Furthermore, in 2022, Heart & Stroke published a new study in the Canadian Journal of Neurological Sciences, which revealed that annual stroke occurrence rates in Canada increased to 108,707, or approximately one every five minutes.

Furthermore, as per the report published by the CDC in January 2022, about 0.6% of children aged 0-17 years had active epilepsy in 2021. The same source also stated that around 470,000 children had active epilepsy and around 3.0 million adults in the United States had active epilepsy in 2021. In addition, the incidence of epilepsy in the United States in seniors is up to 240 per 100,000 per year. Thus, the rising prevalence of epilepsy propels the demand for interventional neurology devices, which will increase market growth.

Additionally, a rise in product launches, strategic activities by the key players, and government initiatives and awareness campaigns are expected to drive market growth. For instance, in October 2022, the Society of Vascular and Interventional Neurology publicized a 40-second stroke awareness challenge. During the challenge, each person was required to create a 40-second video doing as many push-ups as they could safely do. Such awareness challenges make people more cautious about their health and, thereby, driving the market growth.

Therefore, with increased neurology diseases and awareness programs, North America is expected to witness significant growth over the forecast period.

Interventional Neurology Devices Industry Overview

The interventional neurology devices market is fragmented in nature. The global key players are manufacturing the majority of interventional neurology devices. Market leaders with more funds for research and a better distribution system established their position in the market. The key players in the market are Abbott, B Braun SE, Medtronic, Boston Scientific Corporation, and Stryker Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incidence of Neurological Disorders

- 4.2.2 Risng Demand for Minimally Invasive Treatment

- 4.3 Market Restraints

- 4.3.1 High Cost of Devices

- 4.3.2 Stringent Regulatory Scenario

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Product Type

- 5.1.1 Cerebral Balloon Angioplasty and Stenting Systems

- 5.1.1.1 Carotid Artery Stents

- 5.1.1.2 Embolic Protection Systems

- 5.1.2 Neurothrombectomy Devices

- 5.1.3 Aneurysm Coiling and Embolization Devices

- 5.1.4 Micro-catheters

- 5.1.5 Guidewires

- 5.1.1 Cerebral Balloon Angioplasty and Stenting Systems

- 5.2 By Application

- 5.2.1 Artery Stenosis

- 5.2.2 Ischemic Strokes

- 5.2.3 Brain Aneurysm

- 5.2.4 Vein Stenosis

- 5.2.5 Others

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott

- 6.1.2 B. Braun SE

- 6.1.3 Boston Scientific Corporation

- 6.1.4 Johnson & Johnson

- 6.1.5 Medtronic

- 6.1.6 Merit Medical Systems.

- 6.1.7 Penumbra, Inc.

- 6.1.8 Stryker Corporation

- 6.1.9 Terumo Corporation

- 6.1.10 Integer Holdings Corporation

- 6.1.11 Canon Inc.

- 6.1.12 MicroPort Scientific Corporation