|

市場調査レポート

商品コード

1437875

除細動器:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Defibrillator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 除細動器:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

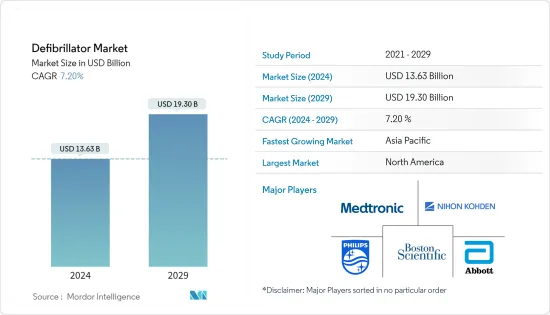

除細動器市場規模は2024年に136億3,000万米ドルと推定され、2029年までに193億米ドルに達すると予測されており、予測期間(2024年から2029年)中に7.20%のCAGRで成長します。

新型コロナウイルス感染症(COVID-19)の流行は、病院外と病院内での心停止に対する人々の治療方法など、ヘルスケア制度のいくつかの側面を変えました。パンデミック期間中、世界中のさまざまな政府による厳しい規制により、心臓手術は減少しました。たとえば、2021年3月に発表されたEHRAの記事では、英国ではパンデミック期間中、除細動装置を使用した心臓再同期療法処置が45%減少し、植込み型除細動器を使用した処置が45%になったと述べています。パンデミック期間中の除細動器を伴う心臓血管処置のこのような減少は、市場の成長に顕著な影響を与えました。ただし、パンデミック後の厳しい規制が緩和された後のすべての心臓外科手術の再開は、予測期間中の市場の成長に貢献すると予想されます。

心血管疾患の有病率の増加と除細動器分野の技術進歩が市場の主な促進要因となっています。たとえば、2022年 1月に発表された英国心臓財団(BHF)のデータによると、世界中で影響を受ける最も一般的な心臓病は、冠状動脈(虚血性)心疾患(世界有病率は2億人と推定)、末梢動脈(血管)疾患(1億1,000万人)でした。、脳卒中(1億人)、心房細動(6,000万人)。この報告書はまた、北米での心臓および循環器疾患の有病者数が4,600万人、欧州で9,900万人、アフリカで5,800万人、南米で3,200万人、アジアとオーストラリアで3億1,000万人であると述べた。したがって、心血管疾患による負担の高さは、除細動器の需要の増加に寄与すると予想されます。除細動器は、突然のショックによって必要な臓器に十分な酸素と血液を供給することにより、突然の心停止から患者を蘇生させるために広く使用されており、それによって医療機器の成長を促進するからです。市場。

さらに、さまざまな政府やさまざまな市場関係者による製品発売の増加も市場の成長に貢献すると予想されます。たとえば、2022年 2月、ニコラ・マロンインフラ大臣は、北アイルランドの公共交通網全体に設置される初の救命用除細動器の1つを発表しました。さらに、2021年 7月、Jeevtronics Pvt Ltdは、手回し式のデュアルパワー除細動器であるSanMitra 100 HCTを開発しました。この装置は手頃な価格で軽量であり、電気が利用できない地域でも使用できるため、専門家の間では従来の除細動器よりも信頼性が高いと考えられています。

ただし、厳格な規制の枠組みは、予測期間中の市場の成長を妨げる可能性があります。

除細動器の市場動向

完全自動体外式除細動器は予測期間中に成長すると予想される

全自動体外式除細動器(AED)は、救助者がショックを与えるためにボタンを押す必要がなく、必要なときに自動的にショックを与えるように設計されています。このデバイスは段階的な指示を伝達し、被害者がショックを受ける時期を救助者に知らせます。完全自動モデルは、心停止の緊急事態において対応者を支援するように設計されています。多くの研究により、全自動AEDは安全かつ効果的であり、救助中にショックボタンを押すことをためらうことに伴う長時間の遅延を軽減できることが示されています。

完全自動体外式除細動器の重要性を促進するためのさまざまなプログラム、意識向上キャンペーン、製品の発売、およびAED管理プラットフォームの開始が、この部門の成長を推進する主な要因です。たとえば、2022年 8月、ポーテージ健康財団(PHF)は、より安全なコミュニティを構築するという財団の長期持続可能性目標に取り組むため、1回限りの自動体外式除細動器(AED)助成プログラムを発表しました。さらに、2021年 3月、オーストラリア政府はオーストラリア政府庁舎に自動体外式除細動器を導入しました。 AEDは、セントジョンアンビュランスオーストラリアとゾールメディカルオーストラリアの合弁事業でした。

また、2022年 8月に、グレートウェスタン航空救急車慈善チームは、米国で心肺蘇生中の自動体外式除細動器(AED)の使用キャンペーンを開始しました。同様に、WhaleTeqは2021年 6月に、AEDのテストと管理のギャップを埋めるために、最新の除細動器テスト DSF2000を備えた初の自動体外式除細動器管理プラットフォームを発売しました。したがって、AEDの意識向上プログラムとさまざまな政府機関による製品発売の増加は、市場の成長に貢献すると予想されます。

北米は予測期間中に除細動器市場で大きなシェアを保持すると予想される

北米は、心血管疾患の罹患率の高さ、技術的に先進的な除細動器製品の採用の増加、および主要な市場企業の存在により、予測期間にわたって市場のかなりのシェアを保持すると予想されます。たとえば、2022年 5月に発行されたACCの記事では、米国では毎年約377,000人の成人と23,000人の子供が院外で心停止を経験していると述べています。

また、カナダ心臓脳卒中財団の2022年 2月の報告書によると、カナダでは75万人が心不全を抱えて暮らしており、毎年 10万人がこの難病と診断されており、2030年までに心不全が起こると予測されています。カナダにおける心不全に関連するヘルスケア費は年間最大28億米ドルに達すると予想されます。したがって、この国の心臓病患者の数の多さと心不全による経済的負担の増加により、この地域の市場は予測期間中に高い成長を遂げると予想されます。

この地域における重要な市場の存在と、除細動器の需要の高まりに応える高度な製品の開発が市場の成長に貢献すると予想されます。たとえば、ボストンサイエンティフィックは2021年 12月に、mCRMモジュラー療法システムの安全性、性能、有効性を評価するMODULAR ATP臨床試験を開始しました。 mCRMシステムは、EMBLEM MRI皮下植込み型除細動器(S-ICD)システムとその他の2つの心調律管理デバイスで構成されます。

したがって、心血管疾患の負担の高さなどの前述の要因により、革新的な製品の発売は、北米地域の調査対象市場の成長に貢献すると予想されます。

除細動器業界の概要

除細動器市場は、世界的および地域的に事業を展開している複数の企業が存在するため、本質的に細分化されています。競合情勢には、 Boston Scientific Corporation、Koninklijke Philips NV、Medtronic PLC、Nihon Kohden Corporation、Abbott Laboratoriesなど、市場シェアを保持し、よく知られているいくつかの国際企業と地元企業の分析が含まれています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 心血管疾患の有病率の増加

- 除細動器分野における技術の進歩

- 市場抑制要因

- 厳格な規制の枠組み

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品別

- 植込み型除細動器(ICD)

- 経静脈植込み型除細動器(T-ICD)

- 皮下植込み型除細動器(S-ICD)

- ペースメーカー・ICD機能付きCRT(CRT-D)

- 体外式除細動器(ED)

- 自動体外式除細動器(AED)

- 半自動体外式除細動器

- 全自動体外式除細動器

- 手動体外式除細動器

- ウェアラブル除細動器(WCD)

- 植込み型除細動器(ICD)

- エンドユーザー別

- 病院

- 救急医療

- ホームケア

- その他のエンドユーザー

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Abbott Laboratories

- Boston Scientific Corporation

- Cardiac Science Corporation

- Defibtech LLC

- Koninklijke Philips NV

- LivaNova PLC

- Medtronic PLC

- Nihon Kohden Corporation

- Physio-Control Inc.

- ZOLL Medical Corporation

- Bexen Cardio

- Mindray Medical International Ltd.

第7章 市場機会と将来の動向

The Defibrillator Market size is estimated at USD 13.63 billion in 2024, and is expected to reach USD 19.30 billion by 2029, growing at a CAGR of 7.20% during the forecast period (2024-2029).

The COVID-19 epidemic has altered several facets of the healthcare system, including how people are treated for cardiac arrests both outside and within hospitals. There was a reduction in cardiac procedures during the pandemic period due to the strict regulation by various governments across the world. For instance, the EHRA article published in March 2021 mentioned that during the pandemic period, cardiac resynchronization therapy procedures with defibrillation devices decreased by 45%, and procedures involving implantable cardioverter defibrillators were 45% in England. Such reductions in the cardiovascular procedures involving defibrillator devices during the pandemic period had a notable impact on the growth of the market. However, the resumption of all cardiac surgical procedures after the relaxation of strict regulations during the post-pandemic period is expected to contribute to the growth of the market over the forecast period.

The increasing prevalence of cardiovascular diseases and technological advancements in the field of defibrillators are the major drivers for the market. For instance, the British Heart Foundation (BHF) data published in January 2022 reported that the most common heart conditions affected globally were coronary (ischemic) heart disease (global prevalence estimated at 200 million), peripheral arterial (vascular) disease (110 million), stroke (100 million) and atrial fibrillation (60 million). The report also mentioned that the prevalence of heart and circulatory diseases in North America was 46 million, in Europe 99 million, in Africa 58 million, in South America 32 million, in Asia and Australia 310 million. Therefore, the high burden of cardiovascular diseases is expected to contribute to the growing demand for defibrillators as they are widely used in reviving patients from sudden cardiac arrest by providing sufficient oxygen and blood to the required organs via a sudden shock, thereby fueling the growth of the market.

Additionally, the increasing product launches by various governments and various market players are also expected to contribute to the growth of the market. For instance, in February 2022, Infrastructure Minister Nichola Mallon unveiled one of the first life-saving defibrillators that will be installed across the public transport network in Northern Ireland. Additionally, in July 2021, Jeevtronics Pvt Ltd developed SanMitra 100 HCT, the hand-cranked dual-powered defibrillator. The device is affordable, low-weight, and considered more reliable than traditional defibrillators by experts as it can be used even in areas where electricity is unavailable.

However, the stringent regulatory framework is likely to hinder market growth over the forecast period.

Defibrillator Market Trends

Fully Automated External Defibrillator is Expected to Witness Growth Over the Forecast Period

A fully automated external defibrillator (AED) is designed to automatically deliver a shock when needed without the rescuer having to press a button to deliver the shock. The device communicates step-by-step instructions to let rescuers know when the victim is about to receive a shock. Fully automatic models are designed to assist responders in cardiac arrest emergencies. Many studies have shown that fully automatic AEDs are safe, and effective, and can reduce extended delays associated with hesitating to press the shock button during a rescue.

The launch of various programs, awareness campaigns, product launches, and AED management platforms to promote the importance of fully automated external defibrillators are the major factors driving the segment's growth. For instance, in August 2022, Portage Health Foundation (PHF) announced a one-time automated external defibrillator (AED) grant program to address the foundation's long-term sustainability goal of building safer communities. Additionally, in March 2021, the government of Australia launched an automated external defibrillator at the Government house of Australia. The AED was a joint venture between St. John Ambulance Australia and Zoll Medical Australia.

Also, in August 2022, the Great Western Air Ambulance Charity team launched an automated external defibrillator (AED) usage campaign during CPR in the United States. Likewise, in June 2021, WhaleTeq launched the first automated external defibrillator management platform with their latest defibrillator test, DSF2000 to fill in the AED testing and management gap. Thus, the rising awareness programs for AED and increasing product launches by various government organizations are expected to contribute to the growth of the market.

North America is Expected to Hold Significant Share in the Defibrillator Market Over the Forecast Period

North America is expected to hold a significant share of the market over the forecast period owing to the high prevalence of cardiovascular diseases, increasing adoption of technologically advanced defibrillator products, and the presence of major market players. For instance, the ACC article published in May 2022 mentioned that about 377,000 adults and 23,000 children experience out-of-hospital cardiac arrest each year in the United States.

Also, as per the February 2022 report from the Heart and Stroke Foundation of Canada, 750,000 people are living with heart failure, and 100,000 people are diagnosed with this incurable condition each year in the country and it is projected that by the year 2030, the healthcare costs associated with heart failure in Canada will reach up to USD 2.8 billion per year. Hence, with this high number of heart patients along with the increasing economic burden due to heart failure in the country, the market is expected to witness high growth over the forecast period in this region.

The presence of a key market in this region and the development of advanced products to meet the growing demand for defibrillators is expected to contribute to the growth of the market. For instance, in December 2021, Boston Scientific launched the MODULAR ATP clinical trial to evaluate the safety, performance, and effectiveness of the mCRM Modular Therapy System. The mCRM system consists of two cardiac rhythm management devices, the EMBLEM MRI subcutaneous implantable defibrillator (S-ICD) system and the other.

Therefore, owing to the aforesaid factors, such as the high burden of cardiovascular diseases, innovative product launches, are expected to contribute to the growth of the studied market in the North America Region.

Defibrillator Industry Overview

The defibrillator market is fragmented in nature due to the presence of several companies operating globally as well as regionally. The competitive landscape includes an analysis of a few international as well as local companies which hold the market shares and are well known including Boston Scientific Corporation, Koninklijke Philips NV, Medtronic PLC, Nihon Kohden Corporation, and Abbott Laboratories among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Defination

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Cardiovascular Diseases

- 4.2.2 Technological Advancements in the Field of Defibrillators

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Framework

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Million)

- 5.1 By Product

- 5.1.1 Implantable Cardioverter Defibrillator (ICD)

- 5.1.1.1 Transvenous Implantable Cardioverter Defibrillator (T-ICDs)

- 5.1.1.2 Subcutaneous Implantable Cardioverter Defibrillator (S-ICDs)

- 5.1.1.3 CRT with Pacemaker and ICD Function (CRT-D)

- 5.1.2 External Defibrillator (ED)

- 5.1.2.1 Automated External Defibrillator (AEDs)

- 5.1.2.1.1 Semi-automated External Defibrillators

- 5.1.2.1.2 Fully-automated External Defibrillators

- 5.1.3 Manual External Defibrillator

- 5.1.3.1 Wearable Cardioverter Defibrillators (WCDs)

- 5.1.1 Implantable Cardioverter Defibrillator (ICD)

- 5.2 By End User

- 5.2.1 Hospitals

- 5.2.2 Emergency Care

- 5.2.3 Home Care

- 5.2.4 Other End Users

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Boston Scientific Corporation

- 6.1.3 Cardiac Science Corporation

- 6.1.4 Defibtech LLC

- 6.1.5 Koninklijke Philips NV

- 6.1.6 LivaNova PLC

- 6.1.7 Medtronic PLC

- 6.1.8 Nihon Kohden Corporation

- 6.1.9 Physio-Control Inc.

- 6.1.10 ZOLL Medical Corporation

- 6.1.11 Bexen Cardio

- 6.1.12 Mindray Medical International Ltd.