|

|

市場調査レポート

商品コード

1444448

自動車用ECU(電子制御ユニット):市場シェア分析、業界動向と統計、成長予測(2024~2029年)Automotive Electronic Control Unit - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動車用ECU(電子制御ユニット):市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

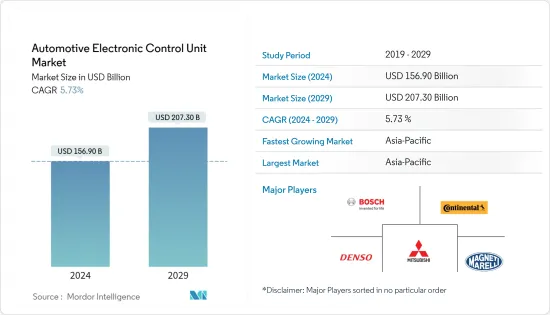

自動車用ECU(電子制御ユニット)の市場規模は、2024年に1,569億米ドルと推定され、2029年までに2,073億米ドルに達すると予測されており、予測期間(2024年から2029年)中に5.73%のCAGRで成長します。

自動車製造部門の閉鎖とロックダウンにより、COVID-19感染症のパンデミックが自動車用ECU(電子制御ユニット)市場に悪影響を与えることは避けられませんでした。しかし、世界中で電気自動車の導入率が前年比で急速に高まっているため、市場は勢いを取り戻すと予想されています。

市場は主に技術の進歩とシステムの革新によって動かされています。先進国では、運転の利便性と安全性に対する消費者の嗜好の高まりが市場の成長を推進しています。ナビゲーションおよびインフォテインメントシステムは世界中のほとんどの自動車に標準機能として採用されており、その導入が進んでいます。これらのシステムを相互に接続するには、中央電子制御ユニットの自動車用コネクタが必要です。

燃料使用量を削減するための政府の規制と、車両の燃費を向上させたいという一般大衆からの需要の高まりも、自動車分野におけるECU市場の高成長につながる大きな要因です。

先進国におけるハイブリッド車や純電気自動車などの代替車両の選択肢の着実な成長は、これらの車両が従来の車両に比べて非常に複雑であるため、ECU市場に大きく貢献してきました。 促進要因の安全性、セキュリティ上の懸念、運転のしやすさ、顧客が求めるメンテナンスの負担の軽減なども、ECU市場の成長を促進する要因の一部です。

スマートフォンを車両に接続し、車両の状態に関するリアルタイムの情報を 促進要因に提供することが、最近の大きな動向となっています。これらの先進的なECUシステムは、スマートフォンと簡単に接続できる機能を備えており、ECUシステムの成長の向上につながります。

アジア太平洋地域、それに北米、欧州が続き、この地域での電気自動車の需要の高まりにより、予測期間中に大幅な成長が見込まれると予想されます。さらに、先進国および新興諸国におけるハイブリッド車などの技術的に先進的な車両に対する需要の増加が、ECU市場の成長を促進すると予想されます。

自動車用ECU(電子制御ユニット)市場動向

電気自動車の販売増加によりECUの需要が拡大

電気自動車の需要は世界中で急速に成長しており、これによりこれらの自動車におけるECUの需要が増大すると予想されます。さらに、政府の有利な補助金や取り組みがECU市場の成長を促進する触媒として機能します。 2040年までに、新車販売のほぼ54%、世界の自動車保有台数の33%が電気自動車になるでしょう。

欧州政府は電気自動車の販売目標を達成するために、地域全体で充電インフラを構築するためのさまざまなプロジェクトをすでに開始しています。自動車分野におけるこの変革は、自動車メーカー、電子部品メーカー、アフターマーケット、およびこの分野のサプライチェーンに影響を与えると予想されます。

電気自動車の需要と販売の増加に伴い、ICエンジン車のみに関連する部品メーカーが電気自動車の分野にも事業を拡大しています。自動車診断市場では、エンジン制御やトランスミッション用のECUなどのコンポーネントが、電気アーキテクチャやバッテリー管理システム用のECUに置き換えられるでしょう。

さらに、従来の診断システムは、車両のすべての電気および機械コンポーネントの状態を継続的に監視する車載診断システムに完全に置き換えられることが予想されます。

アジア太平洋がECU市場を独占すると予想される

アジア太平洋は、乗用車における車載インフォテインメントおよび通信アプリケーションの需要の増加、可処分所得の増加、この地域での自動車生産の増加により、自動車用ECU(電子制御ユニット)市場を独占しています。

アジア太平洋地域における電動化は、中国と日本の存在により高い普及率を示しています。中国は電気自動車の主要市場であり、電気自動車技術を進歩させているほとんどの自動車メーカーは日本のものです。この電気自動車の発展は、現在収益と販売量の両方の点で最高の市場シェアを保持しているこの地域のECU市場における需要の増加と相関している可能性があります。

北米でも、高級車の需要の増加、エネルギー効率の高い車両の需要の増大、この地域での二酸化炭素排出量を削減するための厳しい政府規制により、自動車用電子制御ユニット市場の成長が見込まれています。

インフォテインメントおよび通信アプリケーションが高級車や乗用車に実装する需要が高まっているため、欧州の自動車ECU市場は成長しています。ドイツ、イタリアなどの欧州諸国に存在する大手自動車メーカーによる高級感と快適性の機能の提供への注目の高まりにより、市場成長の機会がさらに創出されています。

自動車用ECU(電子制御ユニット)業界の概要

自動車用電子制御ユニット市場は、Lear Corporation、Robert Bosch GmbH、Nidec Corporation、Continental AG、Delphi Technologiesなどの企業によって独占されています。世界中の企業がさまざまな革新的なテクノロジーを採用し、研究開発プロジェクトに投資しています。さらに、メーカーは利益を獲得し、業界での存在感を強化するために、世界中に販売店と流通ネットワークを展開することでネットワークを拡大しています。例えば、

2021年10月、マザーソンはインドの新しいツールルームのためにマレリ・オートモーティブ・ライティング(マレリ)との協力を拡大しました。これは、特定の照明用途に特化したインド初のこの種のツールルームとなります。このツールルームは、既存の合弁会社であるマレリ・マザーソン・オートモーティブ・ライティング・インディア・プライベート・リミテッドを拡張したものとなります。この50/50合弁会社は、インドの屋外照明市場に対応するために2008年に設立され、現在インドに4つの工場を持っています。

2020年3月、ロバート・ボッシュGmBHとニコラ・モーター・カンパニーは、積載量40トンの燃料電池トラックを開発するためのパートナーシップを締結しました。先進的なトラックシステムの重要な要素はボッシュ車両制御ユニットであり、独立したユニットの数を減らしながら、高度な機能のためにより高い計算能力を提供します。 VCUは、ニコラのトラックの高度な機能をサポートするために不可欠な、複雑なe/eアーキテクチャに拡張可能なプラットフォームを提供することで、将来のイノベーションをサポートします。

2021年 10月、ZFは、アクティブリアアクスルステアリングシステムAKC(アクティブキネマティクスコントロール)が2013年の発売以来100万台生産されたと発表しました。AKCは、さまざまな運転状況で機敏性、安全性、快適性を実現します。

上記の事例と発展により、自動車用電子制御ユニット市場のプレーヤーは、市場シェアの大部分を獲得することに注力すると予想され、予測期間中に地理的なプレゼンスを拡大する可能性があります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 推進別

- 内燃エンジン

- ハイブリッド

- バッテリー電気自動車

- 用途別

- ADASと安全システム

- ボディコントロールとコンフォートシステム

- インフォテイメントおよび通信システム

- パワートレインシステム

- ECU別

- 16ビットECU

- 32ビットECU

- 64ビットECU

- 自律性別

- 従来車両

- 半自動運転車

- 自動運転車

- 車両別

- 乗用車

- 商用車

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 世界のその他の地域

- 南米

- 中東とアフリカ

- 北米

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- Lear Corporation

- Robert Bosch GmbH

- Nidec Corporation

- Continental AG

- Aptiv PLC

- Leopold Kostal GmbH &Co. KG

- ZF Friedrichshafen AG

- Autoliv Inc.

- Magneti Marelli

第7章 市場機会と将来の動向

The Automotive Electronic Control Unit Market size is estimated at USD 156.90 billion in 2024, and is expected to reach USD 207.30 billion by 2029, growing at a CAGR of 5.73% during the forecast period (2024-2029).

The negative impact of the COVID-19 pandemic on the automotive electronic control unit market was inevitable due to shut down of automotive manufacturing units and lockdowns. However, the market is expected to regain momentum due to the swiftly escalating year-on-year adoption rate of electric vehicles worldwide.

The market is primarily driven by technological advancements and innovation in systems. In developed nations, increasing consumer preference for driving convenience and safety is driving the market's growth. The adoption of navigation and infotainment systems is growing as they have become standard features in most cars across the world. Central electronic control unit automotive connectors are required to connect these systems to one another.

Government regulations to reduce fuel usage and increasing demand for better mileage of vehicles from the general public are other major factors leading to the high growth of the ECU market in the automotive sector.

The steady growth of alternative vehicle choices, such as hybrid and pure electric cars, in developed nations has contributed significantly to the ECU market due to the high complexities of these vehicles over conventional vehicles. Driver safety, security concerns, ease of driving, and low maintenance demanded by the customers are also some of the factors driving the growth of the ECU market.

Connecting smartphones to the vehicle and providing the driver with real-time information about the vehicle's state is a major trend in recent times. These advanced ECU systems, with the provision to connect with smartphones easily, can lead to an improvement in the growth of ECU systems.

The Asia-Pacific region, followed by North America and Europe, is anticipated to witness significant growth during the forecast period owing to the growing demand for electric vehicles in the region. Moreover, increased demand for technologically advanced vehicles like hybrid vehicles in developed and developing countries is expected to drive the growth of the ECU market.

Automotive Electronic Control Unit Market Trends

Rising Electric Vehicle Sales to Boost Demand for ECUs

The demand for electric vehicles is growing rapidly across the world, and this is expected to augment the demand for ECU in these vehicles. In addition, favorable government subsidies and initiatives act as catalysts for boosting the growth of the ECU market. By 2040, nearly 54% of new car sales and 33% of the global car fleet will be electric.

The European government has already started various projects for building charging infrastructure across the regions to meet the electric vehicle sales target. This transformation in the automotive sector is expected to impact the automakers, electronic component manufacturers, aftermarkets, and the sector's supply chain.

Manufacturers of parts and components only pertaining to IC engine vehicles are now expanding their business into the electric vehicle domain as the demand for and sale of electric vehicles increases. In the automotive diagnostics market, components, such as ECU for engine control and transmission would be replaced by ECUs for electrical architecture and battery management systems.

Moreover, the conventional diagnostic systems are anticipated to be replaced entirely by onboard diagnostic systems that would continually monitor the health of all the electric and mechanical components of the vehicle.

Asia-Pacific Anticipated to Dominate the ECU Market

Asia-Pacific dominates the automotive electronic control unit market due to a rise in the demand for in-vehicle infotainment and communication applications in passenger vehicles, increased disposable income, and a rise in automobile production in this region.

Electrification in the Asia-Pacific region has witnessed a high penetration rate due to the presence of China and Japan, as China is the leading market for electric vehicles, and most automakers advancing in electric vehicle technology are from Japan. This development in electric vehicles can be correlated to the increased demand in the market for ECU in the region, which currently holds the highest market share in terms of both revenue and volume.

North America is also expected to witness growth in the automotive electronic control unit market due to increased demand for luxury cars, growing demand for energy-efficient vehicles, and strict government regulations to reduce carbon emissions in this region.

The European automotive ECU market is growing as infotainment & communication applications are experiencing high demand for their implementation in luxury & passenger vehicles. The growing focus on providing luxury and comfort features by leading automotive manufacturers present in European countries, including Germany, Italy, etc., is further creating opportunities for the market's growth.

Automotive Electronic Control Unit Industry Overview

The automotive electronic control unit market is dominated by players such as Lear Corporation, Robert Bosch GmbH, Nidec Corporation, Continental AG, and Delphi Technologies, among others. Companies worldwide are adopting various innovative technologies and investing in R&D projects. Moreover, manufacturers are expanding their networks by developing dealership and distribution networks globally to gain profits and strengthen their industry presence. For instance,

In October 2021, Motherson extended its cooperation with Marelli Automotive Lighting (Marelli) for a new tool room in India. This will be the first of its kind tool room in India dedicated to specific lighting applications. The toolroom will be an extension of the existing joint venture company Marelli Motherson Automotive Lighting India Private Limited. The 50/50 JV was established in 2008 to address the Indian exterior lighting market, and now it has four plants in India.

In March 2020, Robert Bosch GmBH and Nikola Motor Company formed a partnership to develop a fuel cell truck with a capacity of 40 ton. The key element of the advanced truck system is the Bosch vehicle control unit, which provides higher computing power for advanced functions while reducing the number of independent units. The VCU supports future innovations by providing a scalable platform for the complex e/e architecture, which is essential to support the advanced features of Nikola's trucks.

In October 2021, ZF announced that one million units of its active rear-axle steering system AKC (Active Kinematics Control) had been produced since its launch in 2013. AKC enables agility, safety, and comfort in numerous driving situations.

Owing to the abovementioned instances and developments, players in the automotive electronic control unit market are anticipated to focus on capturing the majority of the market share and are likely to expand their geographical presence during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Force Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Propulsion

- 5.1.1 Internal Combustion Engine

- 5.1.2 Hybrid

- 5.1.3 Battery Electric Vehicle

- 5.2 By Application

- 5.2.1 ADAS and Safety System

- 5.2.2 Body Control and Comfort System

- 5.2.3 Infotainment and Communication System

- 5.2.4 Powertrain System

- 5.3 By ECU

- 5.3.1 16-bit ECU

- 5.3.2 32-bit ECU

- 5.3.3 64-bit ECU

- 5.4 By Autonomy

- 5.4.1 Conventional Vehicle

- 5.4.2 Semi-autonomous Vehicle

- 5.4.3 Autonomous Vehicle

- 5.5 By Vehicle

- 5.5.1 Passenger Car

- 5.5.2 Commercial Vehicle

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 US

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 UK

- 5.6.2.2 France

- 5.6.2.3 Germany

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Rest of the World

- 5.6.4.1 South America

- 5.6.4.2 Middle-East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Lear Corporation

- 6.2.2 Robert Bosch GmbH

- 6.2.3 Nidec Corporation

- 6.2.4 Continental AG

- 6.2.5 Aptiv PLC

- 6.2.6 Leopold Kostal GmbH & Co. KG

- 6.2.7 ZF Friedrichshafen AG

- 6.2.8 Autoliv Inc.

- 6.2.9 Magneti Marelli