|

|

市場調査レポート

商品コード

1641860

産業用エアコンプレッサ:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Industrial Air Compressors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 産業用エアコンプレッサ:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

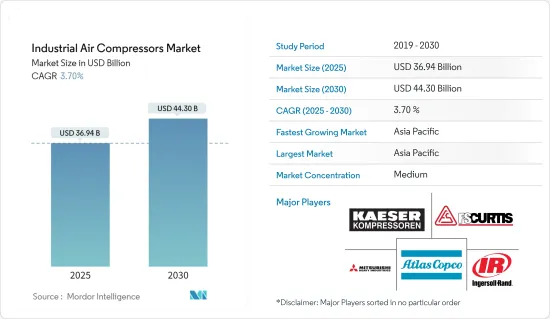

産業用エアコンプレッサの市場規模は、2025年に369億4,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは3.7%で、2030年には443億米ドルに達すると予測されています。

世界の石油・ガス、石油化学、運輸、農業、自動車産業の増加や、産業用コンプレッサ技術開発に対する政府支援の増加は、市場拡大を大きく加速させる重要な理由です。

主要ハイライト

- 世界中の様々な企業が、複雑な産業プロセスに動力を供給するために、圧縮空気を供給するエアコンプレッサを使用しています。ヘビーデューティー産業用エアコンプレッサは、高馬力モーターとヘビーデューティーコンポーネントに依存しているため、より高い圧力レベルを供給するために開発されています。農業施設では、作物の散布やサイロの換気、製造業では空気圧機械の動力、石油・ガス事業などに使用されます。

- エアコンプレッサは、その柔軟性、安全性、低メンテナンスコストの能力により、電力や油圧よりも優れています。エアコンプレッサは、電気や油圧の動力システムよりも可動部品が少ないです。しかし、エアコンプレッサは、供給される空気に特別な治療が必要です。空気に汚れがあると、供給パイプが損傷し、漏れの腐食につながり、最終的に出力が低下します。

- 市場の各社は、エネルギー効率の高いエアコンプレッサの開発にも継続的に投資しています。例えば、アトラスコプコは、インテリジェントな制御・モニタリングシステムを統合して省エネコンプレッサソリューションを提供するため、給油技術の開発に注力していると述べています。

- さらに、これらのコンプレッサは、コンプレッサの用途と設置場所に基づいて使用されます。例えば、レシプロタイプのコンプレッサは、壁側にフライホイールを設置し、密閉式のベルトガードを設置する必要があり、側面にはメンテナンス用のスペースが必要です。ロータリー式コンプレッサの場合は、吸込グリッドと換気扇がコンプレッサに冷却空気を再循環させないように設置する必要があります。

- 産業で使用されるこれらのエアコンプレッサは、発生する熱を逃がすための特別な冷却ユニットを必要とし、企業の初期設定コストを増加させています。そのため、企業はエネルギーとメンテナンスのコストを削減するため、より高性能のコンプレッサに期待しています。

- これらの用途以外にも、エアコンプレッサは石油精製、石油化学合成、パイプライン輸送、ガス注入にも使用されています。石油・ガス探査の拡大と産業への投資の増加が、市場成長の主要要因です。

- ngersoll Randによると、圧縮空気システムに投入されるエネルギーのうち、使用ポイントに到達するのはわずか10%から20%に過ぎず、残りのエネルギーは熱や漏れのために浪費されます。残りのエネルギーは、熱や漏れに浪費されます。大規模な事業を展開する組織では、これは数十0万米ドルに相当する可能性があります。

- エアコンプレッサの設置とメンテナンスのコストは非常に高いです。様々なエアコンプレッサの複雑なモニタリング・制御システムを維持するため、価格は上昇の一途をたどっています。このため、近い将来、市場の拡大が鈍化すると予想されます。

- しかし、COVID-19の発生により、中国のベンダーは工場を閉鎖し、生産設備を一時停止しました。中国ではCOVID-19の患者数が減少しているため、同地域に製造工場を持つベンダーは、工場閉鎖による供給不足のため、部品価格を2~3%近く引き上げています。このため、中国からのサプライチェーン全体に影響が出ています。COVID-19の普及もコンプレッサセグメントの技術革新を促し、ベンダーは急激な需要増に対応するために生産を拡大しています。

産業用エアコンプレッサ市場の動向

ロータリーエアコンプレッサが大きなシェアを占める

- ロータリーエアコンプレッサは、ロータリースクリューエアコンプレッサとしても知られ、容積式圧縮システムであり、大幅な軽量化とメンテナンスの容易さ(簡素化されたメンテナンス手順が利用可能なため)、少ないオイル消費量、過酷な環境での実証済みの信頼性、発熱の少なさなど、いくつかの利点があるため、他のコンプレッサよりも多く採用されています。

- ロータリーエアコンプレッサは主に、長時間一定の圧力を必要とするユーザーに好まれています。マテリアルハンドリング、スプレー塗装、工作機械での使用など、様々な産業環境で使用されています。さらに、製造、飲食品、製薬など複数の産業が、プロセスを最適化し生産コストを削減するため、オイルフリーエアコンプレッサを導入しています。

- さらに、給油式エアコンプレッサは一般的に、大量の中圧空気を必要とするユーザーに使用されています。例えば、世界のBICグループのメキシコ子会社であるNo Sabe Fallar, SA de CVは、安全で信頼性の高いBIC製品を製造しており、GA型コンプレッサ群、省エネES制御システム、AirConnect可視化システムを使用しています。オイル潤滑式エアコンプレッサは、同等レベルの信頼性を提供し、エネルギーのスマートな使用によりコストを大幅に削減します。

- オイルフリーロータリスクリュモデルは、食品包装や医療用酸素のように、オイルが気流に混入しないようにするため、生産、産業、または医療用途で使用されます。オイルフリーロータリーエアコンプレッサは、給油式ロータリーシステムと同じ圧力に達するために2つの圧縮段が必要なため、高価です。

- 産業用エアコンプレッサは、現代の石油・ガス産業において、大小さまざまな業務で重要な役割を果たしています。例えば、Q Air-Californiaによると、石油ガスの95%は、パイプラインで輸送する前に圧縮処理されます。

- 石油・ガス産業では、持続可能で信頼性の高い圧縮空気装置が求められています。石油・ガスの様々な下流企業は、COVID-19の大流行による石油化学製品や精製製品の需要鈍化の影響を受けています。精製マージンの低下は、BPCL、HPCL、IOCL、RILなどの石油下流企業の利益低下につながります。これとは対照的に、Oil IndiaやONGCなどの上流企業は、旅行や産業活動の減少による石油・ガス需要の伸びの減少により、石油・ガス産業の産業用エアコンプレッサに影響を及ぼしています。

アジア太平洋が大きな市場シェアを占める

- 中国は、産業用エアコンプレッサの生産と消費の面で、アジア太平洋と世界最大の市場の1つになると予想されます。同国が優位に立つ主要要因は、浙江開山圧縮機、VMAC Company、DHH Compressor Jiangsu、DENAIR Energy Saving Technology(Shanghai)PLCなど、複数のエアコンプレッサメーカーが同国に存在することです。

- 同地域の成長に大きく貢献しているその他の要因としては、政府の規制と施策が市場をさらに押し上げ、エネルギー効率のためにエアコンプレッサの採用を増加させることが期待されています。例えば、エネルギー施策保全法(The Energy Policy and Conservation Act)は、エアコンプレッサを含む様々な消費者製品と商業・産業機器の省エネルギー基準を規定しています。

- さらに、中国は自国産業の開発とそれに続く輸出の加速、厳しい基準の導入、急速な都市化によって魅力的な国になっています。中国は産業生産率が非常に高く、最も急速に成長している28カ国にランクインしています。これらの要因は、同国の製造施設で産業用エアコンプレッサを採用する推進力となっています。

- さらに、この地域の成長の質を高め、環境問題に対処し、過剰生産能力を削減するために、いくつかの投資が計画されています。飲食品、エレクトロニクス、建設、鉱業など、いくつかのエンドユーザー産業で主導的な存在感を示しています。

- 代替エネルギー源の開発にもかかわらず、石油と石油ベースの製品の需要は、主に中国、インド、日本における世界人口の増加に伴って増加しています。その結果、この需要に対応するため、産業用エアコンプレッサとガスコンプレッサは、これらの作業に適切な圧力レベルを確保するために非常に貴重なものとなっており、競合優位性を維持するため、より低いエネルギー要件、高速化、過酷な掘削環境に耐えるより顕著な能力に焦点を当てた技術革新が行われています。

- さらに、インドは2021年末までに世界第5位の製造国になると予想されています。Siemens、GE、Boeingなどの製造大手は、拡大戦略の一環として、インドに新たな製造工場を設立、または設立中です。こうした動向は、同国における産業用エアコンプレッサの採用が拡大していることを示しています。

- OPECの最近の予測によると、現在の予測で初めて、インドが将来のエネルギー需要に最も大きく貢献する唯一の国になると予想され、次いで中国、その他の国々が続き、22~23mboe/dの石油製品範囲になると予想されています。これらの精製所や貯蔵所を海辺や気候条件の厳しい地域に設置することが、国内の産業用エアコンプレッサ需要を押し上げると予想されます。

産業用エアコンプレッサ産業概要

産業用エアコンプレッサ市場は競争が激しく、複数の参入企業が参入しています。Atlas Copco Group、Ingersoll Rand Inc.(Gardner Denver Inc.)、Kaeser Kompressoren, Inc.、Mitsubishi Heavy Industries Compressor Corp.などの市場競合企業は、市場での競合を維持することに取り組んでいます。このため市場競争企業間の敵対関係は激化しており、市場集中度は低いです。

2022年5月、ELGiは、オイルフリースクリューエアコンプレッサのABシリーズの最新製品であるELGi AB 11-22kWの2つの新シリーズを発表しました。このユニットは、特に飲食品、小型製薬、酪農産業の圧縮空気要件に対応します。また、LDシリーズ2.2~11kWの潤滑式ダイレクトドライブ往復動エアコンプレッサもあります。新しいLDシリーズは、ピストンエアコンプレッサ技術の革新です。

2022年6月、Ingersoll Randは、遠心式コンプレッサポートフォリオの最新の革新である新型MSGターボエアNX 1500(NX 1500)コンプレッサを発表しました。NX 1500は、実績のある技術と機能により、ビジネスの収益に大きな違いをもたらしながら、エネルギー集約型サイトの要求を満たすことができます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターファイブフォース

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- COVID-19の市場への影響

第5章 市場力学

- 市場促進要因

- 石油・ガスへの世界的投資の増加

- エネルギー効率の高いコンプレッサへの需要

- 市場抑制要因

- 環境と安全使用への懸念

第6章 市場セグメンテーション

- タイプ別

- ロータリーエアコンプレッサ

- 往復動エアコンプレッサ

- 遠心式エアコンプレッサ

- エンドユーザー別

- 石油・ガス

- 飲食品

- 製造

- 医療

- 発電

- 建設・鉱業

- その他

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Atlas Copco Group

- Ingersoll Rand Inc.

- FS-Curtis

- Howden Group Ltd.

- Gardner Denver Inc.

- Mitsubishi Heavy Industries Compressor Corp.

- Kaeser Kompressoren

- Zhejiang Kaishan Compressor Co. Ltd(Kaishan Group)

- Sullair, LLC(Hitachi Group)

- Bauer Kompressoren GmbH

- Aerzener Maschinenfabrik GmbH

- Hanwha Power Systems

第8章 投資分析

第9章 市場機会と今後の動向

The Industrial Air Compressors Market size is estimated at USD 36.94 billion in 2025, and is expected to reach USD 44.30 billion by 2030, at a CAGR of 3.7% during the forecast period (2025-2030).

Increases in the oil and gas, petrochemical, transportation, agricultural, and automotive industries globally, as well as increased government support for developing industrial compressor technology, are some important reasons that significantly speed up market expansion.

Key Highlights

- A wide range of businesses worldwide generally uses air compressors to deliver compressed air to power complex industrial processes. Heavy-duty industrial air compressors are developed to provide higher pressure levels, as they rely on high horsepower motors and heavy-duty components. In agricultural facilities, these are used to spray crops and ventilate silos, power pneumatic machinery in the manufacturing industries, and oil and gas operations, among others.

- Air compressors have an advantage over electric power and hydraulic power due to their capability to offer flexibility, safety, and low-maintenance cost. Air compressors require fewer moving parts than electrical and hydraulic power systems. However, air compressors need special treatment for the supplied air, as any contamination in the air can damage the supply pipes, leading to corrosion in leakages, ultimately resulting in power output.

- The companies in the market are also continuously investing in developing energy-efficient air compressors. For instance, Atlas Copco mentioned that it is focusing on developing oil-injected technology for offering energy-saving compressor solutions by integrating intelligent control and monitoring systems.

- Moreover, these compressors are used based on the application and location of the compressor to be installed. For instance, reciprocating-type compressors must be installed with flywheels on the side of the wall and an enclosed belt guard, and they need spaces on the sides for maintenance. In the case of the rotary type, the compressors need to be installed so that their inlet grids and ventilation fan may not recirculate the cooling air to the compressor.

- These air compressors used in industries require special cooling units to dispense the heat generated, adding to the companies' initial setup cost. Hence, the companies are looking forward to better-performance compressors to cut down on energy and maintenance costs.

- Apart from these applications, air compressors are also used for petroleum refining, petrochemical synthesis, pipeline transportation, and gas injection. The increasing expansion of oil and gas exploration and investment in the industry are the major factors driving the market growth.

- According to Ingersoll Rand, only 10% to 20% of the energy input to the compressed air systems reaches the point of use, whereas the rest of the energy gets wasted in heat or leaks. This may account for millions of dollars for organizations having large operations.

- Air compressor installation and maintenance costs are very high. Due to the upkeep of intricate monitoring and control systems for various air compressors, the price keeps increasing. This is anticipated to slow market expansion in the near future.

- However, due to the outbreak of COVID-19, Chinese vendors closed their factories, temporarily suspending production facilities. Since the number of COVID-19 cases has reduced in China, the vendors having manufacturing plants based in the region have increased component prices by nearly 2-3%, owing to a shortage of supplies due to factory shutdown. Therefore, this has impacted the entire supply chain from China. The COVID-19 spread has also driven innovations in the compressors segment, with vendors ramping up their production to meet the sudden demand increase.

Industrial Air Compressor Market Trends

Rotary Air compressors to Hold Significant Share

- Rotary air compressors, also known as rotary screw air compressors, are a positive displacement compression system and are adopted above other compressors due to several advantages it offers, like a significant reduction in weight and easier maintenance (owing to the availability of simplified maintenance procedures), lesser overall oil consumption, proven reliability in harsh environments, and less heat generation.

- Rotary air compressors are mainly preferred by users requiring constant pressure for usually extended periods. It is used in various industrial settings for applications such as material handling, spray painting, and use with machine tools. In addition, multiple industries, such as manufacturing, food, beverage, and pharmaceutical, are deploying oil-free air compressors to optimize their processes and reduce costs in production.

- Moreover, Oil-injected air compressors are generally used by users requiring large volumes of medium-pressure air. For instance, No Sabe Fallar, SA de CV, the Mexican subsidiary of the global BIC Group, manufactures safe, reliable BIC products and uses a group of GA-type compressors, an energy-saving ES control system, and the AirConnect Visualization System. The oil-lubricated air compressor provides equal levels of reliability and substantially drives down costs through the smart use of energy.

- Oil-free rotary screw models are used in production, industrial, or medical applications to disable oil from entering the airflow, like food packaging or medical oxygen. Oil-free rotary air compressors are expensive as they require two compression stages to reach the same pressures as an oil-injected rotary system.

- Industrial air compressors play a significant role in the modern oil and gas industry for large and small operations. For instance, according to Q Air-California, 95% of petroleum gas is processed through compression before transporting in a pipeline.

- The oil and gas industry demands sustainable and reliable compressed air equipment. Various downstream oil & gas companies are impacted due to a slowdown in demand for petrochemical and refined products due to the COVID-19 pandemic. Lower refining margins lead to lower profits for downstream oil companies such as BPCL, HPCL, IOCL, and RIL. In contrast, upstream companies such as Oil India and ONGC are impacted due to less gas and oil demand growth due to a reduction in travel and industrial activities, thereby affecting industrial air compressors in the oil and gas industry.

Asia-Pacific to Account for a Significant Market Share

- China is expected to be one of the largest markets in the Asia-Pacific region and globally for industrial air compressors in terms of production and consumption. The primary factor for the country's dominance is the presence of several air compressor manufacturers in the country, such as Zhejiang Kaishan Compressor Co. Ltd, VMAC Company, DHH Compressor Jiangsu Co. Ltd, and DENAIR Energy Saving Technology (Shanghai) PLC, among others.

- The other factors that are highly responsible for the growth in the region are the Government regulations and policies expected to boost the market further, increasing air compressors' adoption for energy efficiency. For instance, The Energy Policy and Conservation Act prescribed energy conservation standards for various consumer products and commercial and industrial equipment, including air compressors.

- Moreover, China has become attractive by developing indigenous industries and subsequent acceleration in exports, the introduction of stringent standards, and rapid urbanization. China has a very high industrial production rate and ranks among the 28 fastest-growing nations. These factors act as drivers for adopting industrial air compressors in manufacturing facilities in the county.

- In addition, Several investments are being planned to aid the quality of growth in the region, address environmental concerns, and reduce overcapacity, for the same. It has a leading presence in several end-user industries, such as food and beverage, electronics, construction, and mining.

- Despite enormous development in alternative energy sources, oil and oil-based products' demand increases with the rising global population, predominantly in China, India, and Japan. Consequently, to keep up with the demand, industrial air and gas compressors have become invaluable for ensuring the appropriate pressure levels for these operations, with innovations focused on lower energy requirements, increased speed, and a more remarkable ability to withstand harsh drilling environments to maintain a competitive edge.

- Furthermore, India is expected to become the fifth-largest manufacturing country globally by the end of 2021. Manufacturing giants, such as Siemens, GE, and Boeing, have either set up or are setting up new manufacturing plants in India as part of their expansion strategy. These trends indicate the growth in the country's adoption of industrial air compressors.

- According to the recent forecast of OPEC, for the first time in current projections, India is expected to stand as the single most significant contributor to future energy demand, followed by China and other countries, standing in the product range of oil from 22 to 23 mboe/d. Establishing these refineries and storage in seashore areas and areas of harsh climatic conditions is expected to push industrial air compressor demand in the country.

Industrial Air Compressor Industry Overview

The Industrial Air Compressors Market is competitive, with several players in the market. The players in the market, such as Atlas Copco Group, Ingersoll Rand Inc.(Gardner Denver Inc.), Kaeser Kompressoren, Inc., and Mitsubishi Heavy Industries Compressor Corp, are engaged in maintaining a competitive edge in the market. This has intensified the competitive rivalry in the market, and therefore, the market concentration is low.

In May 2022, ELGi introduced two new ranges of Air Compressors, ELGi AB 11 - 22kW, the latest addition to the AB-Series range of oil-free screw air compressors. The units specifically address the compressed air requirements of the food and beverage, small pharmaceutical, and dairy industry, and LD Series 2.2 - 11kW lubricated direct drive range of reciprocating air compressors. The new LD Series is an innovation in piston air compressor technology.

In June 2022, Ingersoll Rand unveiled the latest innovation in its centrifugal portfolio, the new MSG Turbo-Air NX 1500 (NX 1500) compressor, engineered to deliver the lowest total cost of ownership for sites seeking a long-lasting, low-maintenance and 100 percent oil-free solution. The NX 1500 can meet the demands of energy-intensive sites while making a substantial difference to a business's bottom line through a range of proven technologies and features.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter Five Forces

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitutes

- 4.4 Impact of COVID-19 on the market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Global Investment in Oil and Gas

- 5.1.2 Demand for Energy Efficient Compressors

- 5.2 Market Restraints

- 5.2.1 Environmental and Safe Use Concerns

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Rotary Air Compressors

- 6.1.2 Reciprocating Air Compressors

- 6.1.3 Centrifugal Air Compressors

- 6.2 By End-user

- 6.2.1 Oil and Gas

- 6.2.2 Food and Beverages

- 6.2.3 Manufacturing

- 6.2.4 Healthcare

- 6.2.5 Power Generation

- 6.2.6 Construction and Mining

- 6.2.7 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia- Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 South Korea

- 6.3.3.5 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Atlas Copco Group

- 7.1.2 Ingersoll Rand Inc.

- 7.1.3 FS-Curtis

- 7.1.4 Howden Group Ltd.

- 7.1.5 Gardner Denver Inc.

- 7.1.6 Mitsubishi Heavy Industries Compressor Corp.

- 7.1.7 Kaeser Kompressoren

- 7.1.8 Zhejiang Kaishan Compressor Co. Ltd (Kaishan Group)

- 7.1.9 Sullair, LLC (Hitachi Group)

- 7.1.10 Bauer Kompressoren GmbH

- 7.1.11 Aerzener Maschinenfabrik GmbH

- 7.1.12 Hanwha Power Systems