|

市場調査レポート

商品コード

1432832

クラウドマイグレーション:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Cloud Migration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| クラウドマイグレーション:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

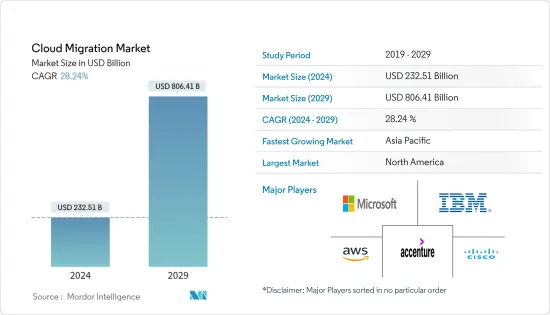

クラウドマイグレーション市場規模は2024年に2,325億1,000万米ドルと推定され、2029年には8,064億1,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは28.24%で成長すると予測されます。

過去10年間で、クラウド・コンピューティングの導入は中小企業の投資の増加により増加しました。世界的には、多くの企業がクラウドプラットフォームに移行し、その利点を活用しています。近年、クラウドの採用はITコスト削減戦略の重要な検討事項となっています。

主なハイライト

- クラウドに移行する主な理由は、拡張性、有効性の向上、迅速な導入、機動性、ディザスタリカバリです。かなりの企業が顧客にクラウドのディザスタリカバリ機能を提供し、ビジネスの拡大を支援しています。クラウドへの移行は、リアルタイムのエクスペリエンス、ビジネス要素、オンプレミスのデータへのアクセシビリティで人気を集めています。この技術はまた、最小限の時間で複数の事業部門を立ち上げるのに役立っています。

- クラウドと産業化サービスの成長と従来のデータセンター・アウトソーシング(DCO)の衰退は、ハイブリッド・インフラ・サービスへの大転換を示しています。従来のDCO市場が縮小する一方で、インフラ・ユーティリティ・サービスとともにコロケーションやホスティングへの支出が急増しています。これにより、クラウドIaaSやホスティングへのシフトが進むと予想されます。PaaS、IaaS、SaaSへの移行が近年最も重要となっています。また、企業はDevOps機能と自動化を採用しているため、クラウド導入の技術的およびビジネス的なメリットを実現する上で、これらの機能が不可欠と見なされるようになっています。

- クラウドマイグレーションサービスに対する需要の高まりは、拡張性、柔軟性、リモート・コラボレーション、タスクの自動化、モビリティの向上、強固なデータ保護が要因となっています。さらに、接続されたデバイスのネットワークが拡大することで、膨大なデータが増加しています。その結果、低コストのデータストレージソリューションに対するニーズが高まり、クラウドマイグレーションサービスの利用が増加すると予測されています。

- ハイブリッド・クラウドへの移行は、他のクラウド・サービスと比較して、ここ数年で全体的に大きく成長しています。ハイブリッド・クラウドを利用することで、企業はコンピューティング・リソースを拡張することができ、短期的な需要の急増に対応するための巨額の資本を必要としなくなります。多くのクラウド・プロバイダーは、世界中のさまざまな場所でインフラを急速に増強する機能を提供しており、ビジネスを新しい地域に迅速に拡大することができます。

- データ・セキュリティの問題とアプリケーションの相互運用性の問題が、クラウドマイグレーション市場の成長を妨げると予想されます。インターネット接続の増加とデジタル化は、クラウドマイグレーションサービスを提供する企業にチャンスを与えます。

- しかし、世界中でCOVID-19の発生が続いているため、オンプレミスのITシステムで運営されている企業には大規模な制限が生じています。そのため、こうした企業の多くが急速にクラウドに移行しています。パンデミック時のリモートワークの増加が、クラウドマイグレーション市場を拡大させました。さらにアクセンチュアは、COVID-19が新たな変曲点を生み出し、エンドツーエンドのデジタルトランスフォーメーションの基盤を構築するために、すべての企業がクラウドマイグレーションを大幅に加速させることを要求しており、すべての企業がクラウドビジネスになることを必要としているとしています。

クラウドマイグレーション市場の動向

著しい成長が期待されるBFSI

- 銀行や金融機関は、柔軟性、俊敏性、新興技術やFinTechエコシステムの統合などの利点により、クラウドソリューションへの移行を加速させています。クラウド・ソリューションは、インフラ・コストを大幅に削減することで、銀行の経費削減に貢献しています。

- このような事例が、BFSI部門だけでなく他のエンドユーザー業界におけるクラウドサービスの採用を後押しし、市場ベンダーは大きな牽引力を獲得しています。例えば、Zscalerのデータによると、2021年には、発見されたインスタンスの総エクスポージャーの50%がAWSパブリッククラウドプラットフォームに起因していました。Microsoft Azureは35%、Google Cloudは13%で2位だった。

- 多くのベンダーがIaaSやPaaSアプリケーションを提供し、BFSI部門をターゲットとしたサービス運用の管理、ホスト、保守、更新、拡張の必要性を排除しています。銀行は、クラウドインフラストラクチャが、AI、ブロックチェーン、ソフトウェアコンテナによってサポートされる運用プログラムや顧客対応プログラムなど、抜本的な近代化イニシアチブの推進に役立つことを広く認識しています。

- 銀行はまた、クラウド・サービス提供企業との戦略的パートナーシップを通じて、クラウドマイグレーション技術を採用しています。例えば、2022年5月、ジェフリーズ・ファイナンシャル・グループはアマゾンと提携し、情報技術サービスをクラウドに移行します。これは、クラウドベースのソフトウェアとデータ分析に成長し始めたばかりの金融ビジネスによる最新のステップです。ジェフリーズは、4年間の契約に基づいて、同社の重要なビジネスプロセス、社内および顧客向けアプリケーション、ITリソース、データをアマゾン・ウェブ・サービスに移行します。

- 顧客にデジタルバンキング体験を提供するため、銀行組織はクラウドマイグレーション技術を採用しています。例えば、2021年5月、アマゾンウェブサービス(AWS)は、フィリピンユニオン銀行が2022年までにITインフラをオンプレミスからクラウドに移行すると発表しました。この移行は、同行のデジタルトランスフォーメーションを加速し、顧客のデジタルバンキング体験を向上させ、フィリピンの遠隔地にも金融サービスを提供することで、フィリピンにおける金融包摂を拡大することを目的としています。

北米が最大の市場シェアを占める見込み

- 北米はクラウドマイグレーションにおける主要なイノベーターでありパイオニアであり、市場で大きなシェアを占めています。同地域はまた、クラウドマイグレーションベンダーの足場も強固であり、これが同市場の成長に拍車をかけています。IBM Corporation、Microsoft Corporation、Amazon Web Services Inc.、Cisco Systems Inc.、Cognizant Technology Solutions Corporation、Google Inc.などです。

- データやアプリケーションなどの情報をクラウドに移行することで得られるメリットが、この地域の多くの組織にクラウドマイグレーションサービスの導入を促し、市場の成長にプラスの影響を与えています。

- 2021年12月、ナスダックは北米の資本市場を移行するためにアマゾン・ウェブ・サービスとの提携を発表しました。このハイブリッド・アーキテクチャにより、ナスダックはオンプレミス・システムへの低遅延アクセスを提供し、高頻度取引機能を実現するとともに、顧客は仮想接続サービス、市場分析、機械学習などのクラウドベースの機能にアクセスできるようになります。

- さらに2022年8月、トロントの自動クラウドマイグレーション企業であるネクスト・パスウェイ社は、レガシー・データウェアハウスやデータレイクからマイクロソフト・アジュールへの移行を加速するため、マイクロソフトとの協業を発表しました。Shift Analyzerは、ソースとなるレガシー・アプリケーションのワークロードを包括的にレビューし、存在するコードタイプやオブジェクトを確認します。Shift Translatorは、SQL、ストアドプロシージャ、ETLパイプライン/ワークフロー、その他さまざまなコードタイプなどの複雑なワークロードの翻訳、テスト、移行を加速します。さらに、Next Pathwayのテクノロジーは、他のクラウドプラットフォームやクラウドデータウェアハウスからAzureへのワークロードの移行を簡単かつ効率的に行うことができます。

クラウドマイグレーション業界の概要

クラウドマイグレーション市場は適度に統合されており、複数の主要企業で構成されています。市場シェアの面では、現在数社の大手企業が市場を独占しています。市場で高いシェアを誇るこれらの大手企業は、海外における顧客基盤の拡大に注力しています。これらの企業は、市場シェアと収益性を高めるために、戦略的な協業イニシアティブを活用しています。

- 2023年1月デジタル・ソリューション企業のLTIMindtreeは、インテリジェント・ソリューション・プロバイダーのDuck Creek Technologiesおよびマイクロソフトと提携し、保険会社がオンプレミスの基幹システムを迅速かつ効率的にクラウドに移行できるソリューションを構築したと発表しました。

- 2022年2月:IBM Corporationは、SAPとの協業を発表し、ハイブリッド・クラウド戦略を採用し、SAPソリューションからミッション・クリティカルなワークロードをクラウドに移行することを支援するテクノロジーとコンサルティング・スキルを提供します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- バリューチェーン分析

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- 組織におけるクラウドの利点の増加

- BYOD利用の増加

- 市場の課題

- データセキュリティとアプリケーションの相互運用性の問題

第6章 市場セグメンテーション

- 導入タイプ

- パブリッククラウド

- プライベートクラウド

- ハイブリッドクラウド

- 企業規模

- 中小企業(SMEs)

- 大企業

- サービスの種類

- PaaS

- IaaS

- SaaS

- エンドユーザー業界別

- BFSI

- ヘルスケア

- 小売

- 政府機関

- IT・通信

- 製造業

- その他エンドユーザー業界別

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Accenture PLC

- Amazon Inc.

- Cisco Systems Inc.

- Cognizant Technology Solutions Corp

- DXC Technology

- Evolve IP LLC

- Google LLC

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- Rackspace Hosting Inc.

- Rightscale Inc.(Flexera)

- Tech Mahindra Ltd

- VMware Inc.

- WSM International LLC

第8章 投資分析

第9章 市場の将来

The Cloud Migration Market size is estimated at USD 232.51 billion in 2024, and is expected to reach USD 806.41 billion by 2029, growing at a CAGR of 28.24% during the forecast period (2024-2029).

Over the past decade, cloud computing adoption has risen owing to increasing investments from small and medium enterprises. Globally, many organizations have already switched to cloud platforms to take advantage of its benefits. In recent years, cloud adoption stands to be a significant consideration for IT cost reduction strategies.

Key Highlights

- The significant reasons for migrating to the cloud are scalability, increased effectiveness, faster implementation, mobility, and disaster recovery. Considerable companies are offering cloud disaster recovery features to their customers, aiding them in expanding their businesses. Cloud migration is gaining traction for its real-time experience, business elements, and accessibility to on-premise data. This technology also aids in setting up several business units in minimal time.

- The growth of cloud and industrialized services and the decline of traditional data center outsourcing (DCO) indicate a massive shift toward hybrid infrastructure services. While the conventional DCO market is shrinking, spending on colocation and hosting, along with infrastructure utility services, is increasing rapidly. This is expected to drive the shift toward cloud IaaS and hosting. Migration for PaaS, IaaS, and SaaS has been most important in recent years. Companies are also embracing DevOps capabilities and automation; hence, they are increasingly seen as critical to realizing cloud adoption's technical and business benefits.

- The growing demand for cloud migration services is attributed to increased scalability, flexibility, remote collaboration, task automation, improved mobility, and robust data protection. Furthermore, the growing network of connected devices has resulted in massive data growth. As a result, the growing need for a low-cost data storage solution is projected to increase the use of cloud migration services.

- The migration to the hybrid cloud has experienced significant overall growth in the past few years compared to other cloud services. Using a hybrid cloud allows companies to scale computing resources and helps eliminate the need for massive capital to handle short-term spikes in demand. Many cloud providers offer the ability to rapidly increase infrastructure in various worldwide locations, enabling a business to expand to new territories quickly.

- Data security issues and application interoperability issues are expected to hamper the growth of the cloud migration market. Increased internet connectivity and digitization provide opportunities to the cloud migration service offering companies.

- However, the ongoing outbreak of COVID-19 across the world has created massive restrictions on businesses operating with on-premise IT systems. Hence, many of these organizations have rapidly migrated to the cloud. The increase in remote working during the pandemic peopled the cloud migration market. Further, Accenture also states that COVID-19 has created a new inflection point that demands every company to significantly accelerate their cloud migration in order to create a foundation for end-to-end digital transformation, requiring that every business becomes a cloud business

Cloud Migration Market Trends

BFSI Expected to Witness Significant Growth

- Banking and financial organizations are accelerating the migration toward cloud solutions owing to benefits such as flexibility, agility, and integration of emerging technologies and the FinTech ecosystems. Cloud solutions are helping banks cut down expenses by significantly reducing infrastructure costs.

- Such instances have boosted the adoption of cloud services among the BFSI sector as well as other end-user industries, and market vendors are gaining significant traction. For instance, according to the data from Zscaler, In 2021, 50% of total found instance exposure was attributed to the AWS public cloud platform. Microsoft Azure took second place with 35% and Google Cloud 13%, respectively.

- Many vendors are providing IaaS and PaaS applications to eliminate the need to manage, host, maintain, update, and scale service operations targeted toward the BFSI sectors. Banks widely recognize that a cloud infrastructure can help them pursue sweeping modernization initiatives, including operational and customer-facing programs supported by AI, blockchain, and software containers.

- Banks are also adopting Cloud migration technology through strategic partnerships with cloud service-providing companies. For instance, in May 2022, Jefferies Financial Group Inc. is partnering with Amazon to move its information-technology services to the cloud. This is the latest step by a financial business that has just begun to grow into cloud-based software and data analytics. Jefferies is transferring its essential business processes, internal and customer-facing apps, IT resources, and data to Amazon Web Services under a four-year arrangement.

- To provide a digital banking experience to customers, banking organizations are adopting cloud migration technology. For instance, in May 2021, Amazon Web Services (AWS) announced that the Union Bank of the Philippines would transition its IT infrastructure from on-premises to the cloud by 2022. The move is designed to speed the bank's digital transformation, improve customers' digital banking experiences, and increase financial inclusion in the Philippines by providing financial services to distant areas of the nation.

North America Expected to Hold the Largest Market Share

- North America is among the leading innovators and pioneers in cloud migration and holds a significant share of the market. The region also has a strong foothold on cloud migration vendors, which adds to its growth. Some companies include IBM Corporation, Microsoft Corporation, Amazon Web Services Inc., Cisco Systems Inc., Cognizant Technology Solutions Corporation, and Google Inc.

- The benefits offered by moving data and applications, among other information, to the cloud are pushing many organizations in the region to adopt cloud migration services, thereby impacting the market's growth positively, and also the companies in the North American region are making strategic collaborations, business expansion to propel the cloud migration.

- In December 2021, Nasdaq announced a partnership with Amazon Web Services to transfer its North American capital market. This hybrid architecture would offer Nasdaq low-latency access to its on-premises systems, enabling high-frequency trading capabilities and allowing its customers access to cloud-based features such as virtual connection services, market analytics, and machine learning.

- Furthermore, in August 2022, Next Pathway Inc., the Automated Cloud Migration company in Toronto, announced a collaboration with Microsoft to accelerate the migration from legacy data warehouses and data lakes to Microsoft Azure. Shift Analyzer provides a comprehensive review of source legacy application workloads to review the code types and objects present. Shift Translator accelerates the translation, testing, and migration of complex workloads such as SQL, Stored Procedures, ETL pipelines/workflows, and various other code types. Furthermore, Next Pathway's technology can easily and efficiently transfer workloads from other cloud platforms and cloud data warehouses to Azure.

Cloud Migration Industry Overview

The cloud migration market is moderately consolidated and consists of several major players. In terms of market share, few major players currently dominate the market. These major players with prominent shares in the market are focusing on expanding their customer base across foreign countries. These companies leverage strategic collaborative initiatives to increase their market shares and profitability.

- January 2023: Digital solutions firm LTIMindtree announced that it had partnered with Duck Creek Technologies, the intelligent solutions provider, and Microsoft to build a solution enabling insurers to migrate their on-premises core systems to the cloud quickly and efficiently.

- February 2022: IBM Corporation announced a collaboration with SAP to deliver technology and consulting skills to help clients embrace a hybrid cloud strategy and migrate mission-critical workloads from SAP solutions to the cloud in regulated and non-regulated sectors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain Analysis

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Benefits Of Cloud To Organizations

- 5.1.2 Increasing Use of BYOD

- 5.2 Market Challenges

- 5.2.1 Data Security And Application Interoperability Issues

6 MARKET SEGMENTATION

- 6.1 Type of Deployment

- 6.1.1 Public Cloud

- 6.1.2 Private Cloud

- 6.1.3 Hybrid Cloud

- 6.2 Enterprise Size

- 6.2.1 Small and Medium Enterprises (SMEs)

- 6.2.2 Large Enterprises

- 6.3 Type of Service

- 6.3.1 PaaS

- 6.3.2 IaaS

- 6.3.3 SaaS

- 6.4 End-user Vertical

- 6.4.1 BFSI

- 6.4.2 Healthcare

- 6.4.3 Retail

- 6.4.4 Government

- 6.4.5 IT and Telecommunication

- 6.4.6 Manufacturing

- 6.4.7 Other End-user Verticals

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia Pacific

- 6.5.4 Latin America

- 6.5.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Accenture PLC

- 7.1.2 Amazon Inc.

- 7.1.3 Cisco Systems Inc.

- 7.1.4 Cognizant Technology Solutions Corp

- 7.1.5 DXC Technology

- 7.1.6 Evolve IP LLC

- 7.1.7 Google LLC

- 7.1.8 IBM Corporation

- 7.1.9 Microsoft Corporation

- 7.1.10 Oracle Corporation

- 7.1.11 Rackspace Hosting Inc.

- 7.1.12 Rightscale Inc. (Flexera)

- 7.1.13 Tech Mahindra Ltd

- 7.1.14 VMware Inc.

- 7.1.15 WSM International LLC