パワーマネジメントIC(PMIC):市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Power Management Integrated Circuit (PMIC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1910438

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

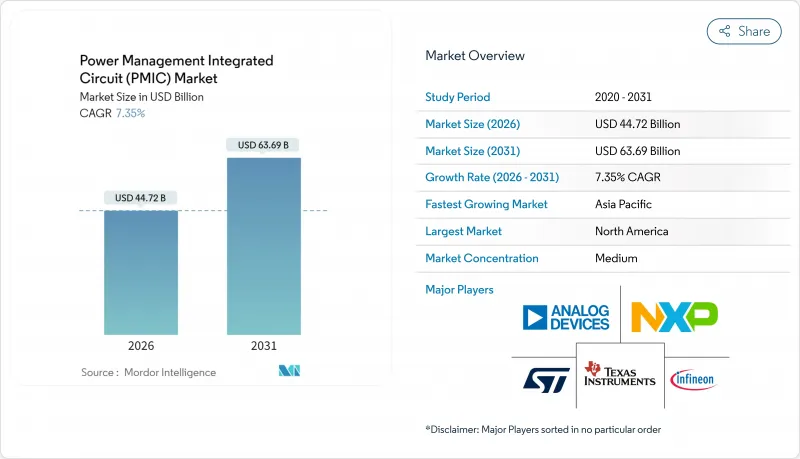

2026年のパワーマネジメントIC(PMIC)市場規模は447億2,000万米ドルと推定され、2025年の416億6,000万米ドルから成長を遂げ、2031年には636億9,000万米ドルに達すると予測されています。

2026年から2031年にかけてはCAGR7.35%で拡大が見込まれます。

電気自動車、フラッグシップスマートフォン、超低消費電力IoTデバイスの拡大により、高効率変換トポロジー、厳密な電圧許容差、先進プロセスノードへの需要が高まっています。バッテリー管理ICは引き続きパワーマネジメントIC(PMIC)市場の基盤であり、ワイヤレス充電用PMIC、ワイドバンドギャップ電源ステージ、20nm以下の設計が成長の重要な触媒として台頭しています。競合情勢は、独自の知的財産(IP)でシェアを守るアナログ分野の老舗企業と、垂直統合に向けた自社専用ソリューションを開発するプロセッサベンダーによって形成されています。ファウンダリ容量、超薄型デバイスにおける熱的制約、偽造部品の流入は、市場全体の勢いに対する具体的なリスクとして引き続き存在しています。

世界のパワーマネジメントIC(PMIC)市場の動向と洞察

EVおよびxEVの急速な普及が、高電流・高効率PMICの需要を押し上げています

電気自動車のアーキテクチャは、パワーマネジメントIC(PMIC)市場の仕様を再構築しています。テスラの4680バッテリーセルは、125°C以下の接合部温度を維持しながら最大500Aの連続電流を処理できるPMICを要求しており、これにより炭化ケイ素(SiC)パワーステージと先進的な熱パッケージングが促進されています。BYDの分散型バッテリー管理設計は10Cの急速充電能力を実現し、セル単位のPMIC制御の必要性を示しています。インフィニオンのCoolSiCモジュールは800V車載充電器で98.5%の効率を達成し、フリートオペレーターは予知保全を可能にするPMIC診断機能を優先しています。これらの要求はセンサーインターフェースや無線リンクの統合を促進し、PMICを単体のレギュレーターからスマートサブシステムへと変革しています。

微細化プロセスノードによるオンチップ電力密度の向上

20nm以下のプロセス移行により、単一ダイ上に複数の電源レールと制御ロジックを配置可能となり、基板面積の縮小と寄生要素の抑制を実現します。TSMCの16nm FinFETプラットフォームは、設計基板による熱プロファイルの保護を維持しつつ、65nm時の0.3W/mm2に対し1W/mm2を超える電力密度を達成しています。MediaTekのDimensity 9400は、AIワークロード向けにサブマイクロ秒単位の電圧スケーリングを実行するオンダイPMICによって管理される12の独立した電源ドメインを統合しています。しかしながら、量子効果によるリーク電流のばらつき増大により、補償アルゴリズムの採用が迫られており、現行の3nmプロセスと比較して30%の消費電力削減を目指す2nmプロセスノードでは、ゲートオールアラウンド構造の導入が示唆されています。

アナログおよびミックスドシグナルノード向けファウンダリ容量の供給チェーン循環性

アナログ生産はデジタル容量拡大に遅れ、2024年末にはTSMCの専門ラインで95%の稼働率に達し、PMICのリードタイムは従来の8週間から16週間に延長されます。世界のファウンドリーズの成熟ノードへの戦略転換により、自動車向け認定ロットのサプライヤーが減少、地政学的リスクへの曝露が高まっています。自動車プログラムが5年間の契約を締結する中、民生電子機器は縮小するスロットを争い、割り当てリスクが激化しています。

セグメント分析

2025年におけるパワーマネジメントIC(PMIC)市場規模の33.15%をバッテリー管理ICが占め、電気自動車用パックや定置型蓄電システムにおけるその不可欠性が浮き彫りとなりました。しかしながら、ワイヤレス充電用PMICは、Qi2の磁気アライメント技術により15W伝送効率が85%に向上し、MagSafe類似のエコシステムが拡大するにつれ、2031年までにCAGR8.32%を記録すると予測されます。

電源管理集積回路市場における需要は、バッテリー管理ICにおいては安全診断、セルバランス精度、熱制御を中心に展開しています。一方、異物検知と適応共振制御がワイヤレス充電用PMICの差別化要因となります。DC-DCコンバータPMICはデータセンターやノートPCの電源レール向けに引き続き需要があり、リニアレギュレータは10μV未満のノイズフロアを必要とするニッチ市場を維持しています。また、モータードライバーPMICは工場自動化の成長に支えられています。電圧リファレンスおよびスーパーバイザICは、自動車の機能安全基準により必須とされる安定した収益基盤であり続けております。

2025年のパワーマネジメントIC(PMIC)市場シェアにおいて、民生用電子機器は42.25%の収益を生み出しました。これはスマートフォン、ノートブック、タブレットが1台あたり15本以上の安定化レールを統合していることを反映しています。800V駆動システムとADASコンピューティングクラスターに支えられた自動車・eモビリティ分野は、8.55%のCAGRを記録すると予測され、他の全分野を上回る成長が見込まれます。

産業用およびロボット工学の使用事例ではトルク精度に優れたモーター駆動が求められ、5Gインフラでは48V直結電源を扱う高電圧PMICが不可欠です。医療機器、特にインプラントは1マイクロアンペア未満の待機電流を優先し、IoTエンドポイントは380mVから起動可能なエネルギーハーベスティング対応PMICを採用します。各業界は信頼性、安定化電圧、テレメトリーの高精度化を基準にPMIC仕様を調整するため、パワーマネジメントIC(PMIC)市場全体でサプライヤーのロードマップが細分化されています。

地域別分析

北米は2025年に世界収益の36.85%を占め、テスラのバッテリー管理システム受注とAppleのカスタムPMICシリコンへの注力が牽引しました。同地域は設計サービスエコシステムの深化と堅調なEVインフラ整備の恩恵を受けています。

主要ファウンダリと民生電子機器組立拠点であるアジア太平洋地域は、2031年までCAGR10.21%で推移すると予測されます。中国のEV拡大と韓国のメモリ生産ラインがPMICの数量を牽引し、ファブへの近接性が開発サイクルを短縮しています。

欧州では、ドイツの自動車メーカーが800Vシステムを採用する電動化と厳格なエコデザイン規制が相まって、安定した需要が持続しています。北欧の再生可能エネルギー分野では、最大電力点追従(MPPT)を最適化する系統連系インバーター向けPMICが導入されています。中東・アフリカ地域では太陽光ミニグリッドが成長の牽引役となり、南米ではブラジルのEV優遇政策とアルゼンチンのリチウム資源を活用した地域密着型バッテリー供給網が成長の要因となっています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 電気自動車(EV)およびハイブリッド車(xEV)の急速な普及により、高電流・高効率PMICの需要が高まっています

- 微細化プロセスノード(20nm未満)による高密度チップ内電力集積の実現

- フラッグシップスマートフォンにおける先進的なバッテリーヘルス管理PMICの採用

- 民生用・産業用電子機器に対する政府の省エネルギー規制

- エッジAI/IoTの普及により、超低待機電流PMICが必要とされています

- 急速充電器におけるワイドバンドギャップ(GaN/SiC)パワーステージの採用

- 市場抑制要因

- アナログおよびミックスドシグナルノード向けファウンダリ容量のサプライチェーン循環性

- 設計の複雑化が進み、NREコストが中小OEMメーカーの手の届かない水準に上昇

- 超薄型民生機器における熱管理の限界

- 増加する偽造PMICの流入が信頼性への認識に影響を与えています

- 業界サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- マクロ経済要因の影響

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- ICタイプ別

- リニアレギュレータPMIC

- DC-DCコンバータPMIC

- バッテリー管理IC

- 電圧リファレンスおよびスーパーバイザIC

- モーター制御およびドライバー向けPMIC

- ワイヤレス充電用PMIC

- 用途別

- 民生用電子機器

- 自動車およびeモビリティ

- 産業用ロボット

- 電気通信およびネットワーク

- 医療・医療機器

- IoTおよびエッジデバイス

- ウエハーノード別

- 65 nm以上

- 40~65 nm

- 20~40 nm

- 20 nm未満

- 電力範囲別

- 低電力PMIC

- 中電力PMIC

- 高電力PMIC

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- 東南アジア

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Texas Instruments Inc.

- Analog Devices, Inc.

- Infineon Technologies AG

- NXP Semiconductors N.V.

- STMicroelectronics N.V.

- ON Semiconductor Corporation

- Renesas Electronics Corporation

- Qualcomm Incorporated

- Broadcom Inc.

- Skyworks Solutions, Inc.

- Dialog Semiconductor(Renesas)

- Rohm Co., Ltd.

- Maxim Integrated(ADI)

- Toshiba Electronic Devices and Storage Corp.

- MediaTek Inc.

- Power Integrations, Inc.

- Silicon Laboratories Inc.

- Monolithic Power Systems, Inc.

- Vishay Intertechnology, Inc.

- Littelfuse, Inc.

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日