|

市場調査レポート

商品コード

1850189

がん診断:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Cancer Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| がん診断:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月24日

発行: Mordor Intelligence

ページ情報: 英文 114 Pages

納期: 2~3営業日

|

概要

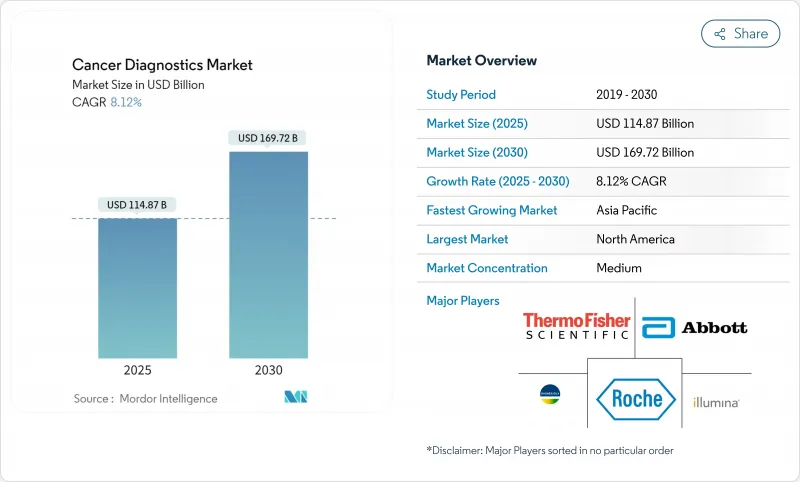

がん診断市場は、2025年に1,148億7,000万米ドルと評価され、2030年には1,697億2,000万米ドルに達し、CAGR 8.12%で拡大すると予測されています。

人工知能ツールの承認加速、血液ベースのスクリーニングに対するメディケアの適用範囲拡大、リキッドバイオプシー・プラットフォームの急速な採用により、早期発見の経路が再構築されつつあります。マルチがん血液検査とポイント・オブ・ケア画像診断装置に対するFDAの画期的な指定は、競争力を高めつつイノベーションに有利な規制環境を示しています。バイデン・キャンサー・ムーンショット(Biden Cancer Moonshot)やオーストラリアの新しい肺検診プログラムを通じて、各国政府は集団検診を最も目に見える形で拡大しており、制約のある公衆衛生予算内に収まる分散型ソリューションへの需要を生み出しています。画像診断大手とAIスペシャリストの戦略的パートナーシップは、生産性の向上と診断所要時間の短縮を推進し、高齢者人口動態のシフトは長期的な検査件数の伸びを維持します。

世界のがん診断市場動向と洞察

政府資金による検診プログラムの増加

世界の保健機関は、乳がんや大腸がん以外の集団検診を拡大しています。ARPA-HのPOSEIDONイニシアチブは、家庭での複数がん検査に資金を提供し、オーストラリアの肺スクリーニングの展開は、十分なサービスを受けていないグループに診断法を近づけています。欧州では現在、肺、前立腺、胃の検診が推奨されており、ベンダーは国家プログラムに適した高スループットでコスト効率の高いプラットフォームの構築を促しています。米国の地域がんプロジェクトに対する6億5,000万米ドルの配分は、三次病院以外でも実施可能な利用しやすい診断法を優先しています。

世界的ながん罹患率の上昇と人口の高齢化

インドでは2040年までに年間200万人のがん患者が発生すると予測されており、欧州では1995年の210万人から2022年には320万人に増加すると見られています。こうしたシフトは、高齢者コホートにおける精密治療のための高複雑度ゲノミクスと、人口の多い市場向けの低コストの迅速検査の両方を医療システムに導入するよう迫るものです。異種インフラ間で検査メニューを拡張できるベンダーは、大きな利益を獲得するのに有利な立場にあります。

高度な分子診断の高コスト

AI放射線検査の自己負担額の中央値は1,000米ドルを超えており、保険導入が遅れている地域では導入が妨げられています。AMAはAI CPTコードを起草したが、エビデンスのハードルにより広範な適用が遅れています。新興国は輸入関税と為替の逆風に直面し、機器価格が現地の手の届く範囲をはるかに超えて上昇し、臨床的価値があるにもかかわらずゲノミクスの普及を妨げています。

セグメント分析

ゲノム/リキッドバイオプシー検査は、汎腫瘍コンパニオン診断薬のFDA認可取得に伴い、がん診断市場内で最も高いCAGR 18.4%を記録すると予測されます。FDAは2024年にイルミナのTruSight Oncology Comprehensiveアッセイを認可し、固形がんの幅広いゲノムプロファイリングをサポートします。一方、画像診断検査は、解釈時間を短縮し放射線科医不足を緩和するAIオーバーレイにより、2024年に46.2%の足場を保っています。生検と細胞診は組織学的確認に不可欠であることに変わりはないが、非侵襲的血液検査は、特にマルチオミクス解析と組み合わせた場合に、組織の精度に近づいています。腫瘍バイオマーカーパネルは、治療選択における役割を通じて安定した需要があります。体外診断用医薬品のイムノアッセイは、検査室のインフラが乏しい分散型施設で成長し、中所得環境における基本的な腫瘍学サービスの拡大を後押ししています。大規模コホートで94.75%の精度を持つ表面増強ラマン分光法のような他のプラットフォームは、将来の競合の脅威を示唆するものです。

地域分析

北米は2024年に38.9%のシェアで売上をリードしたが、これはメディケアによる血液ベースの大腸検査が2025年の診療報酬体系に組み込まれたことと、FDAによる画期的医療機器の頻繁な指定に支えられています。成熟した支払者システムと電子カルテの広範な導入はAIアナリティクスの統合を容易にし、この地域を早期導入のハブとして位置づけています。米国の学術ネットワークは、複数のがん検出プラットフォームを検証する複数州での臨床試験を実施しており、分析の妥当性が証明されれば、償還までの時間を短縮できます。カナダは、治療ガイダンスのためのシークエンシングを引き受ける汎州ゲノム構想の恩恵を受けており、検査件数はさらに増加しています。

欧州は2番目に大きな収益源です。EUの検診ガイドラインが更新され、肺がん、前立腺がん、胃がんが含まれるようになったため、低線量CTとリキッドバイオプシーの両方に対する需要が生じています。欧州リキッドバイオプシー学会はサンプル取り扱いの標準化を進めており、これにより加盟国間での臨床導入の調和が図られるはずです。しかし、保険償還は大きく異なる:ドイツのDRGシステムはNGSパネルを迅速にカバーしているが、南欧州は遅れており、2つのスピードで取り込まれる環境となっています。GDPRに基づくデータプライバシー規制は、クラウドベースのAIベンダーにとってコンプライアンスコストを引き上げるが、国内データセンターへの投資によって導入は緩和されつつあります。

アジア太平洋地域はCAGR 10.9%と最も急速に拡大しています。中国のNMPAは2023年に61の革新的なデバイスを承認したが、これは規制の現実主義を反映したもので、現地のイノベーターの市場投入までの時間を早めています。官民パートナーシップにより、ティア2都市に分子病理ラボが建設され、サンプル処理能力が拡大しています。インドのNational Cancer Gridは、デジタル病理学と遠隔腫瘍学を展開し、農村部の施設が都市部の専門知識を利用できるようにしています。日本における汎肺PCRパネルの迅速承認は、この地域の成熟市場がいかに精密診断を受け入れ続けているかを例証しています。

ラテンアメリカでは、地方分権政策はまだ始まったばかりであるが、シークエンスコストは低下しており、胃がんや胆嚢がんなど発生率の高いがんの標的スクリーニングに道を開いています。中東とアフリカは、依然として保険償還の格差と限られた腫瘍学の労働力によって妨げられています。サハラ以南のがん専門医の90%以上が、診断のために患者が海外に渡航していると報告しています。国際機関はこのような不公平を解消するため、ポータブル画像診断やポイント・オブ・ケア検査法を試験的に導入しているが、その導入には持続可能な資金モデルが必要です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 政府資金によるスクリーニングプログラムの増加

- 世界のがん罹患率の上昇と人口の高齢化

- 液体生検とctDNA検査の急速な導入

- ポイントオブケア画像診断の拡大

- AI駆動型マルチオミクス早期検出プラットフォーム

- 価値に基づくコンパニオン診断の償還

- 市場抑制要因

- 高度な分子診断の高コスト

- 低所得国における限定的な償還

- 訓練を受けた分子病理学者の不足

- AIクラウドワークフローにおけるデータプライバシーの懸念

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 診断タイプ別

- 診断画像検査

- 生検および細胞診検査

- 腫瘍バイオマーカー

- ゲノム/液体生検検査

- IVD免疫測定

- その他の診断タイプ

- がんタイプ別

- 乳がん

- 肺がん

- 大腸がん

- 子宮頸がん

- 前立腺がん

- 腎臓がん

- 肝臓がん

- 膵臓がん

- 卵巣がん

- その他のがんタイプ

- エンドユーザー別

- 病院

- 診断検査室

- 学術研究機関

- POC/外来センター

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Abbott Laboratories

- F. Hoffmann-La Roche Ltd

- Siemens Healthineers

- Thermo Fisher Scientific

- GE HealthCare

- Hologic Inc.

- Illumina Inc.

- Bio-Rad Laboratories

- Agilent Technologies

- bioMerieux SA

- Qiagen

- Guardant Health

- Exact Sciences Corporation

- Becton, Dickinson and Company

- Danaher Corporation(Cepheid)

- PerkinElmer

- Myriad Genetics

- Sysmex Corporation

- Foundation Medicine

- NanoString Technologies