空港荷物ハンドリングシステム:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Airport Baggage Handling Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1939085

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

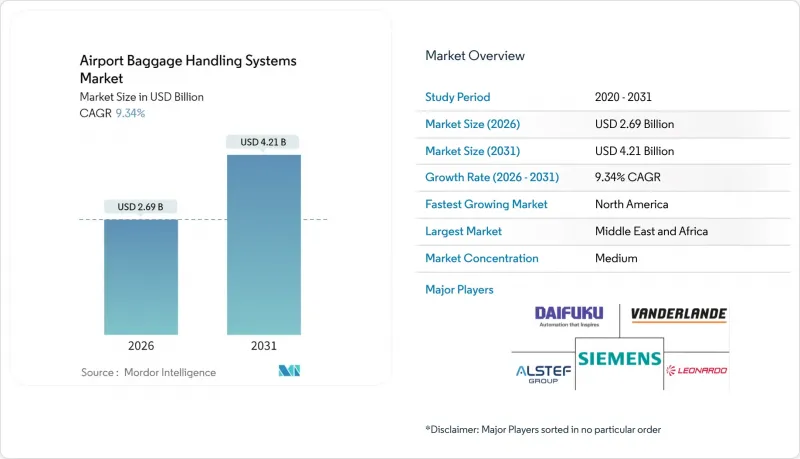

空港荷物ハンドリングシステム市場は、2025年に24億6,000万米ドルと評価され、2026年の26億9,000万米ドルから2031年までに42億1,000万米ドルに達すると予測されています。

予測期間(2026年~2031年)におけるCAGRは9.34%と見込まれています。

この成長は、航空業界における旅客数の回復、着実な容量拡張計画、そして労働力不足や高まるセキュリティ・コンプライアンスコストへの対策として自動化へ移行する空港の動向に支えられています。システムの中間改修、デジタルツインを活用した予知保全、コンピュータビジョンベースの追跡技術が、空港荷物ハンドリングシステム市場のあらゆる層において調達優先順位を再構築しています。コンベアの信頼性とAIを活用した分析機能を組み合わせられるベンダーは現在、価格プレミアムを獲得しています。一方、サイバーセキュリティ対策は、規制当局によるインシデント報告期限の厳格化を受け、バックオフィス上の懸念事項から取締役会レベルの調達基準へと移行しました。資本プロジェクトでは、持続可能性目標と公衆衛生ガイドラインを満たすため、ハイブリッドシステム、省エネモーター、UV-C消毒モジュールを組み合わせるケースが増加しています。

世界の空港荷物ハンドリングシステム市場の動向と洞察

世界の旅客数の急増

旅客数は既にパンデミック前の予測値を上回り、空港荷物ハンドリングシステム市場を牽引するハブ空港の手荷物インフラに深刻な負荷がかかっております。国際空港評議会(ACI)は2040年までに旅客数が倍増すると予測しており、この見通しにより設備更新サイクルが加速し、拡張可能なモジュール式レイアウトへの関心が高まっております。年間4,000万人以上の旅客を処理するメガハブ空港では、ピーク時の処理能力維持のため、事前手荷物保管モジュールやトートベースの仕分け機を導入しております。2023年における手荷物誤処理率は1,000人当たり6.9件まで低下したもの、誤配送された手荷物1件あたり航空会社には100~200米ドルの補償金と再配送費用が発生しており、空港側ではAIを活用した根本原因分析への投資を推進しております。北米の空港運営会社は今後5年間で、パンデミック前の支出の75%に相当するアップグレード予算を確保しており、空港荷物ハンドリングシステム市場における長期的な需要の下支え要因となっています。

空港容量拡張計画

年間2億6,000万人の旅客処理を想定した総額350億米ドルのアル・マクトゥーム国際空港拡張計画など、画期的なプロジェクトは次世代手荷物システムの規模感を示しています。欧州の空港もこれに追随し、スキポール空港では総額60億ユーロ(81億3,000万米ドル)の計画により手荷物地下施設を近代化するとともに、作業環境の改善につながる空調設備のアップグレードを組み込んでいます。北米の空港では、ソルトレイクシティからシアトル・タコマに至るまで、LEED基準に準拠したモーター技術を新規ラインに導入し、軽負荷サイクル時の電力消費を最大25%削減しています。これらのプロジェクトは、空港荷物ハンドリングシステム市場において、改造用センサー、制御ソフトウェアライセンス、サイバーセキュリティ監査といった長期的なアフターマーケット収益源を生み出しています。

高額な設備投資と長期的な投資回収期間

包括的な手荷物プロジェクトは当初予算を大幅に超過する傾向があります。シアトル・タコマ空港の最適化プロジェクトは稼働前に3億2,000万米ドルから5億4,000万米ドルへ膨れ上がり、同様の規模を検討する中規模空港にとって教訓となっています。10~15年という長い回収期間は民営化ターミナルのコンセッション期間と衝突し、運営者は利用料収入の証券化やグリーンボンド構造の活用を余儀なくされています。国際空港評議会(ACI)は現在、財務委員会に対し、ROIをソブリン利回りを150ベーシスポイント上回るハードルレートでストレステストするよう推奨していますが、小規模運営者にとっては依然として債務返済能力の確保が課題となっています。

セグメント分析

年間旅客数4,000万人超のハブ空港は、2025年時点で空港荷物ハンドリングシステム市場の39.88%を占めました。これらの巨大施設は10.25%のCAGRを記録し、2026年から2031年にかけての市場規模拡大を牽引しています。これらの空港の予算規模は、個別航空会社向けシステム、ロボティクス、AI搭載制御システム群を可能にしており、小規模空港では通常、技術サイクルが2回経過してからようやく導入されるものです。ドバイのアル・マクトゥーム空港の設計図は、組み込み型スマートコンベアと予知保全ダッシュボードが、デジタルツインのマスタープランと統合され、将来の需要急増に備える手法を示しています。

2,500万~4,000万人の旅客規模を持つ中規模空港では、ピーク負荷を軽減する事前手荷物保管ゾーンから段階的にアップグレードを実施し、技術革新の格差を縮めています。1,500万~2,500万人規模の施設では、地下構造の全面改修を伴わずに精度向上を図るため、モジュール式コンベアとRFIDゲートウェイの標準化が進められています。1,500万人未満の小規模空港では、資本支出を削減し自動化範囲を段階的に拡大するため、共用セルフサービス端末に依存しています。ベンダー価格の低下に伴い、従来メガハブ空港に限定されていた技術が下流へ普及し、空港荷物ハンドリングシステム市場のあらゆる拠点における基本水準の期待値を引き上げています。

2025年時点で、空港荷物ハンドリングシステム市場の31.12%を搭乗手続き・発券ソリューションが占めており、各ターミナル入口段階での普及度を反映しています。しかしながら、追跡・トレーサビリティソリューションは10.98%というより高いCAGRを示しており、管理部門が取引自動化からデータ中心の意思決定支援へ軸足を移しつつあることを裏付けています。航空会社は、エンドツーエンドの可視化が標準化されれば、手荷物誤処理によるコスト削減効果を乗客1人あたり最大3米ドルと試算しており、これにより空港は手荷物受取ベルトや引渡しポイントの下にRFIDマットを設置するインセンティブを得ています。

保安検査モジュールは、規制当局が検知閾値を見直すたびに調達優先度を維持します。TSA(米国運輸保安庁)だけでも、次世代爆発物検知器に年間2億5,000万米ドルを割り当てており、これらはコンベア制御システムや監視制御ソフトウェアとシームレスに連携する必要があります。初期段階の荷物保管プラットフォームは、航空会社に数時間前の荷物受付の柔軟性を提供し、非航空収入源となる小売受取サービスさえ創出することで、滞留時間を収益化します。この収束効果は、旅客数の増加だけでなく、複数の収益源を通じて空港荷物ハンドリングシステム市場規模の拡大を継続的に推進しています。

空港荷物ハンドリングシステム報告書は、空港容量(1,500万人以下、1,500万~2,500万人、2,500万~4,000万人、4,000万人超)、ソリューション(チェックイン・発券システム、保安検査システムなど)、技術(バーコード、RFIDなど)、システムタイプ(コンベアベルトシステムなど)、地域(北米、欧州など)別に分析しております。市場予測は金額ベース(米ドル)で提示されます。

地域別分析

北米は空港荷物ハンドリングシステム市場において31.85%のシェアで首位を維持しております。これは、TSA(運輸保安庁)による年間2億5,000万米ドルのスクリーニング設備更新プログラムなど近代化義務付けが背景にあり、コンベアメーカーの受注を促進しております。しかしながら、既存インフラの改修は、混雑した地下施設への統合を運用中断なく行い、設置スケジュールを遅らせず、追加の統合コストを発生させない必要があるため、拡張を複雑にしております。カナダとメキシコは漸増的な成長に寄与していますが、ハブ・アンド・スポーク型ネットワークにおける優位性と持続可能性に関する法整備の成熟度から、米国が依然として市場の要となっています。

中東・アフリカ地域は12.09%のCAGRで最速の成長を記録しました。これは、多くの欧州諸国を合わせた旅客処理量を超える規模を目指す湾岸諸国のメガプロジェクトが牽引しています。ドバイのアル・マクトゥーム拡張計画は、地域計画担当者が中間技術段階を飛び越え、第一期工事段階でロボット技術、AIダッシュボード、非接触型消毒モジュールを導入している実例を示しています。ケープタウンなどのアフリカのゲートウェイ空港では、10億米ドルを超える近代化予算が計上されていますが、資金調達サイクルにより実施スケジュールがずれる可能性があります。貨物量の急増は、手荷物と貨物の統合処理ソリューションの需要増加にもつながり、空港荷物ハンドリングシステムの市場範囲が旅客専用から拡大しています。

欧州とアジア太平洋地域は、既存施設の制約と厳しい炭素排出目標が交錯する技術の最先端を形成しています。スキポール空港の60億ユーロ(70億7,000万米ドル)計画では、手荷物地下施設全体を再構築し、人間工学に基づいた作業空間と気候安定型のコンベアホールを実現。これにより熱によるモーター故障を最小限に抑えます。ハイデラバードからジャカルタに至るアジアのハブ空港は、世界のサプライヤーの製造拠点として機能しています。ダイフクの新インド工場は生産能力を4倍に拡大し、地域顧客へのリードタイム短縮を実現しました。南米は絶対規模では依然として小規模ながら、航空会社のネットワーク再開や空港の多国間銀行融資を活用したグリーンフィールドアップグレードのリスク低減により、追い上げの勢いを見せています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3か月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 世界の旅客数の急増

- 空港容量拡張計画

- 統合型RFID追跡システムへの移行

- エンドツーエンド自動化への需要

- 収益拡大の手段としての手荷物事前預かりサービス(EBS)

- パンデミックによる消毒設備の改修

- 市場抑制要因

- 高い設備投資と長い投資回収期間

- レガシーITと相互運用性のギャップ

- 空港労働組合による自動化への反発

- サイバーセキュリティコンプライアンスコスト(EU NIS2/FAA AD)

- バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 空港容量別

- 1,500万人未満

- 1500万~2500万人

- 2500万~4000万人

- 4,000万人以上

- ソリューション別

- チェックインおよび発券システム

- セキュリティスクリーニングシステム

- 搬送・仕分けシステム

- 手荷物の一時預かりサービス

- 手荷物受取所/荷降ろし

- 追跡およびトレーシング

- 技術別

- バーコード

- RFID

- IoTセンサーおよびエッジデバイス

- ロボティクスおよび自律走行車両

- AI/機械学習ソフトウェア

- システムタイプ別

- コンベアベルトシステム

- ティルトトレイ式およびクロスベルト式選別機

- 目的地コード車両(DCV)

- トートベース/個別搬送システム

- ハイブリッドおよびその他の新興システム

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Daifuku Co. Ltd.

- Vanderlande Industries BV

- Siemens AG

- BEUMER Group GmbH & Co. KG

- Alstef Group SAS

- CIMC TianDa Holdings Co. Ltd.

- SITA N.V.

- Ansir Systems

- G&S Airport Conveyer

- Leonardo S.p.A

- Pteris Global Limited

- RBS Global Media Ltd.

- Amadeus IT Group, S.A.

- Lyngsoe Systems A/S

- Brock Solutions

- FIVES SAS

- Robson Handling Technology Ltd.

- ULMA Group

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日