|

市場調査レポート

商品コード

1444184

商用機MRO(メンテナンス・修理・オーバーホール):市場シェア分析、業界動向と統計、成長予測(2024~2029年)Commercial Aircraft Maintenance, Repair, and Overhaul (MRO) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 商用機MRO(メンテナンス・修理・オーバーホール):市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

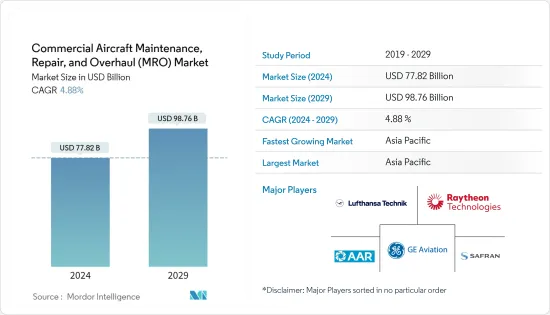

商用機MRO(メンテナンス・修理・オーバーホール)の市場規模は、2024年に778億2,000万米ドルと推定され、2029年までに987億6,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に4.88%のCAGRで成長します。

現在進行中のCOVID-19のパンデミックは、ウイルスの蔓延を阻止する世界の取り組みとして渡航制限や航空便の運航停止を課し、本格的な危機をもたらしました。旅客輸送量の減少と航空機の移動の制限により、2020年はMROの市場が大きな影響を受けました。それにもかかわらず、2021年には渡航制限が減少し、航空機の移動が徐々に増加するため、航空機メンテナンスの需要は今後も増加すると予想されます。今後数年間でプラスの成長が見込まれます。

航空会社は、多額の投資が必要となるため、航空機の最適な状態を維持し、最後の手段としてのみ新しい航空機を調達する傾向があります。COVID-19が航空会社の収入源を深刻に妨げ、利益率を侵食しているため、より多くの航空会社が機材効率を維持するためにMROに頼ると予想されます。さらに、空港が戦略的活動としてMROを支援することを奨励するために、いくつかの政府の取り組みが策定されました。政府は現在、国内のさまざまな空港でMROのために十分なスペースが割り当てられるよう、さまざまな総合的なアプローチに取り組んでおり、これにより予測期間中の商用機MRO活動が強化される可能性があります。

しかし、予知保全の出現により、MRO業界は技術面と人材面の両方に関連した問題が大量に発生しました。デジタルツインなどの革新的なテクノロジーを活用した予知保全の概念はまだ初期段階にあるため、短期間での急速な改善と成長が視覚化されています。これは、機械学習やその他の先進的な概念の真の可能性を活用するために必要なインフラをすべての企業が備えているわけではないことを意味します。これはまた、少数のMRO組織が職員のこれらのスキルを開発するための資本投資に熱心であるため、この概念の到達範囲が限られていることを示しています。しかし、この分野は、業界に焦点を当てた教育やトレーニングのカリキュラムでは十分に反映されていません。さらに、新しい機器やコンポーネントの修理基準に関してMROとOEMの間の協力は限られており、MROプロセスは非常に複雑で要求の厳しいものになっています。このような破壊的な脅威は、予測期間中に焦点を当てている市場の成長を危険にさらす可能性があります。

航空宇宙MRO市場動向

エンジンMROセグメントは、予測期間中に市場を独占する可能性がある

エンジンMROには、現場保守と拠点保守点検が含まれます。デポレベルのメンテナンスには、材料メンテナンス、大規模修理、オーバーホール、またはエンジン、部品、最終品目、アセンブリ、サブアセンブリの完全な再構築が含まれます。これには、部品の製造、技術支援、テストも含まれます。フィールドレベルのメンテナンスは、拠点メンテナンスとは異なるレベルでのショップタイプの作業と機器のメンテナンス活動で構成されます。エンジンメンテナンス分野ではOEMが市場の約半分を支配しており、残りの半分は独立系と航空会社のオーバーホールショップにほぼ分かれています。特に新しい世代の発電所の場合、オペレーターは頻繁にエンジンのメンテナンスを外部委託し、完全なMROサポートプログラムを利用します。たとえば、2021年12月、サウジアラビアの格安航空会社フライナスは、同社のエアバスA320neo航空機80機に動力を供給するLEAP-1Aエンジンについて、CFMインターナショナルと複数年にわたる飛行時間当たり料金(RPFH)契約を締結しました。 RPFH契約は、CFMの柔軟なアフターマーケットサポート製品のポートフォリオの一部です。契約期間中、CFMは航空会社の160基のLEAP-1Aエンジンのメンテナンス費用をエンジン飛行時間ごとに保証します。このような開発は、予測期間中に市場のエンジンMROセグメントを推進すると予想されます。

アジア太平洋は予測期間中に最高の成長を遂げると予想される

アジア太平洋地域の民間航空産業は、新しいナローボディ機に対する強い需要を受けて、今後10年間で急速に成長すると予想されており、これによりMROオペレーションの必要性が高まります。アジア太平洋地域は現在、世界の商用機保有数の3分の1を運航しており、この地域の保有数は2031年までに1万3,000機以上に達すると予想されており、中国の航空保有数は地域全体の45%以上を占めます。業界の専門家によると、航空会社のリース契約の延長により、アジア太平洋地域の航空機保有機の平均使用年数は18~24年に増加しました。COVID-19が流行する以前は、フリートの平均使用年数は6~12年でした。この地域では大規模な航空機が存在し、航空産業の潜在力が高まっているため、多くの大手MROプレーヤーが市場での存在感を急速に高めています。たとえば、2020年に、プラット&ホイットニーは、中国の2つの新しいMROプロバイダーと提携して、世界のプラット&ホイットニーGTFエンジンメンテナンスネットワークを拡大しました。 Aircraft Maintain and Engineering Corporation(Ameco)(中国国際航空とルフトハンザ航空の合弁会社)とMTUメンテナンス珠海(MTU Aeroエンジンと中国南方航空会社の合弁会社)は、GTF MROネットワークの一部として新しい施設となりました。エアバスA320neoファミリーの航空機用PW1100G-JMエンジンのエンジンメンテナンスを提供します。さらに、ベトナムやタイなどの低コストの労働市場は、OEMやMROにとって、地域全体での需要の高まりに対応するために新しい施設を設立する上でますます魅力的になってきています。このような発展は、この地域で注目を集めている市場の成長を促進すると予想されます。

航空宇宙MRO業界の概要

商用機MRO市場は非常に細分化されており、さまざまなMRO機能を備えた多くのプレーヤーが世界規模および地域規模でサービスを提供しています。 GE Aviation、AAR Corp.、Safran SA、Raytheon Technologies Corporation、Lufthansa Technik AGは、商用機MRO市場における著名なプレーヤーの一部です。現在、MRO市場の前向きな市場見通しにより、新規プレーヤーが市場に参入し、既存プレーヤーが新しい地理的場所で存在感を拡大しています。たとえば、2021年 2月、SIA Engineering Company Limitedは、エンジンメンテナンス、部品修理、翼上サービス、保管および保存、材料管理、エンジンテストなどのエンジンサービスを開発および提供するために、新しいエンジンサービス部門(ESD)を設立しました。新しい事業部門は、シンガポールにおけるSIAECのエンジン合弁事業のネットワークを補完することが期待されています。さらに、両社は、MRO活動をサポートするために、人工知能、ロボット工学、ドローン、ビッグデータ、ブロックチェーン技術に投資しています。新世代航空機の出現により、航空機のTBO(Time Between Overhole)が増加しており、今後数年間で小規模なプレーヤーの存在が困難になる可能性があります。しかし、航空機の定期的なメンテナンスと修理から得られる収益は、保有機材の増加に伴い増加し続けるでしょう。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

- USDの通貨換算レート

第2章 調査手法

第3章 エグゼクティブサマリー

- 市場規模と予測、世界、2018~2027年

- MROタイプ別の市場シェア、2021年

- 地域別の市場シェア、2021年

- 市場の構造と主要参加企業

- 商用機MRO市場に関する専門家の意見

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション(金額別の市場規模と予測、2018~2027年)

- MROタイプ

- 機体

- エンジン

- コンポーネント

- ライン

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- AAR Corp.

- Delta TechOps(Delta Air Lines Inc.)

- GE Aviation

- Hong Kong Aircraft Engineering Co. Ltd

- Lufthansa Technik AG

- Raytheon Technologies Corporation

- SIA Engineering Company Ltd

- TAP Maintenance &Engineering

- Singapore Technologies Engineering Ltd

- MTU Aero Engines AG

- Rolls-Royce Holding PLC

- Safran SA

- Air India Engineering Services Ltd

- Emirates Engineering

- StandardAero

- AFI KLM E&M

- Avia Solutions Group PLC

- Garuda Indonesia(GMF AeroAsia)

第7章 市場機会と将来の動向

The Commercial Aircraft Maintenance, Repair, and Overhaul Market size is estimated at USD 77.82 billion in 2024, and is expected to reach USD 98.76 billion by 2029, growing at a CAGR of 4.88% during the forecast period (2024-2029).

The ongoing COVID-19 pandemic resulted in a full-scale crisis, with the imposition of travel restrictions and suspension of flights in a global effort to contain the spread of the virus. Due to decreased passenger traffic and limited aircraft movements, the market for maintenance, repair, and overhaul was affected significantly in 2020. Nevertheless, as travel restrictions decreased in 2021 and as aircraft movements are gradually increased, the demand for aircraft maintenance is expected to witness positive growth in the coming years.

Airlines are inclined toward maintaining the optimum health of their fleet and procuring new aircraft only as a last resort, owing to the high investment required for it. With COVID-19 severely hampering the revenue sources and eroding the profit margins of airlines, more airlines are expected to resort to MRO to maintain fleet efficiency. Furthermore, several government initiatives were formulated to encourage airports to support MRO as a strategic activity. The governments are now undertaking various holistic approaches to ensure that adequate space is allocated at different airports within the country for MRO, which may enhance commercial aircraft MRO activities during the forecast period.

However, the advent of predictive maintenance flooded the MRO industry with a flurry of problems, both technological and manpower-related. As the concept of predictive maintenance powered by innovative technologies, such as digital twins, is still in its infancy, rapid improvements and growth are visualized within a short period. This implies that not all firms are equipped with the required infrastructure to harness the true potential of machine learning and other advanced emerging concepts. This also indicates the limited reach of the concept, as a few MRO organizations are keen on investing in capital to develop these skills among their personnel. However, the domain is not well-represented in industry-focused education and training curricula. Moreover, there is limited cooperation between MROs and OEMs about the repair standards for new equipment and components, making the MRO process highly complex and demanding. Such disruptive threats may endanger the growth of the market in focus during the forecast period.

Aerospace MRO Market Trends

The Engine MRO Segment is Likely to Dominate the Market During the Forecast Period

Engine MRO includes field maintenance and depot maintenance checks. Depot-level maintenance entails material maintenance, major repair, overhaul, or complete rebuilding of engines, parts, end items, assemblies, and subassemblies. It also includes the manufacturing of parts, technical assistance, and testing. Field-level maintenance comprises shop-type work and on-equipment maintenance activities at levels different than depot maintenance. Intermediate or shop-type work includes limited repair of commodity-oriented assemblies and end-items, job shop, bay, and production line operations as per requirement, software maintenance, and repair of subassemblies, such as fabrication or the manufacturing of repair parts, assemblies, and components. OEMs control approximately half of the market in the engine maintenance sector, with the other half roughly split between independent and airline overhaul shops. For new powerplant generations specifically, operators frequently outsource engine maintenance and use full MRO-support programs. For instance, in December 2021, the low-cost airline of Saudi Arabia, flynas, finalized a multi-year Rate Per Flight Hour (RPFH) agreement with CFM International for the LEAP-1A engines powering the airline's fleet of 80 Airbus A320neo aircraft. The RPFH agreement is a part of CFM's portfolio of flexible aftermarket support offerings. Throughout the term of the agreement, CFM will guarantee maintenance costs for the airline's 160 LEAP-1A engines on per engine flight hour basis. Such developments are anticipated to drive the engine MRO segment of the market during the forecast period.

Asia-Pacific is Expected to Witness the Highest Growth During the Forecast Period

The commercial aviation industry in the Asia-Pacific region is expected to grow rapidly over the next decade, in the wake of the strong demand for new narrow-body aircraft, which will enhance the need for MRO operations. The Asia-Pacific region currently operates 1/3rd of the global commercial aircraft fleet, and the fleet in the region is expected to reach over 13,000 aircraft by 2031, with China's airline fleet accounting for over 45% of the region's total. According to industry experts, with the extension of lease contracts of airlines, the average age of the aircraft fleet in the Asia-Pacific region increased to 18 to 24 years. Earlier, in pre-COVID-19 years, the average age of the fleet was 6 to 12 years. With a large fleet and growing potential for the aviation industry in the region, many major MRO players are rapidly enhancing their presence in the market. For instance, in 2020, Pratt & Whitney expanded its global Pratt & Whitney GTF engine maintenance network with two new MRO providers in China. Aircraft Maintenance and Engineering Corporation (Ameco) (a joint venture of Air China Limited and Lufthansa Airlines) and MTU Maintenance Zhuhai Co. Ltd (a joint venture of MTU Aero Engines and China Southern Airline Company Limited) became new facilities as part of the GTF MRO network to provide engine maintenance for PW1100G-JM engines for the Airbus A320neo family of aircraft. Moreover, low-cost labor markets, such as Vietnam and Thailand, are becoming increasingly attractive to OEMs and MROs for setting up new facilities to cater to the growing demand across the region. Such developments are expected to drive the growth of the market in focus in the region.

Aerospace MRO Industry Overview

The market for commercial aircraft MRO is highly fragmented, with many players with different MRO capabilities offering services both globally and regionally. GE Aviation, AAR Corp., Safran SA, Raytheon Technologies Corporation, and Lufthansa Technik AG are some of the prominent players in the commercial aircraft MRO market. Currently, the positive market outlook of the MRO market led to new players entering the market and existing players expanding their presence in new geographical locations. For instance, in February 2021, SIA Engineering Company Limited established a new Engine Services Division (ESD) to develop and provide engine services like engine maintenance, parts repair, on-wing services, storage and preservation, material management, and engine testing. The new business unit is expected to complement SIAEC's network of engine joint ventures in Singapore. Furthermore, the companies are investing in artificial intelligence, robotics, drones, big data, and blockchain technologies to support maintenance, repair, and overhaul activities. With the advent of newer generation aircraft, the TBO (Time Between Overhaul) of aircraft is increasing, which may challenge the existence of smaller players in the coming years. However, the revenue generated from regular maintenance and repair of aircraft will continue to increase with the growing fleet.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Currency Conversion Rates for USD

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

- 3.1 Market Size and Forecast, Global, 2018 - 2027

- 3.2 Market Share by MRO Type, 2021

- 3.3 Market Share by Geography, 2021

- 3.4 Structure of the Market and Key Participants

- 3.5 Expert Opinion on the Commercial Aircraft Maintenance, Repair, and Overhaul (MRO) Market

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size and Forecast by Value - USD billion, 2018 - 2027)

- 5.1 MRO Type

- 5.1.1 Airframe

- 5.1.2 Engine

- 5.1.3 Component

- 5.1.4 Line

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 France

- 5.2.2.3 Germany

- 5.2.2.4 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Rest of Latin America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 Qatar

- 5.2.5.4 Rest of Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 AAR Corp.

- 6.2.2 Delta TechOps (Delta Air Lines Inc.)

- 6.2.3 GE Aviation

- 6.2.4 Hong Kong Aircraft Engineering Co. Ltd

- 6.2.5 Lufthansa Technik AG

- 6.2.6 Raytheon Technologies Corporation

- 6.2.7 SIA Engineering Company Ltd

- 6.2.8 TAP Maintenance & Engineering

- 6.2.9 Singapore Technologies Engineering Ltd

- 6.2.10 MTU Aero Engines AG

- 6.2.11 Rolls-Royce Holding PLC

- 6.2.12 Safran SA

- 6.2.13 Air India Engineering Services Ltd

- 6.2.14 Emirates Engineering

- 6.2.15 StandardAero

- 6.2.16 AFI KLM E&M

- 6.2.17 Avia Solutions Group PLC

- 6.2.18 Garuda Indonesia (GMF AeroAsia)