|

市場調査レポート

商品コード

1640483

サブシーシステム:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Subsea Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| サブシーシステム:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

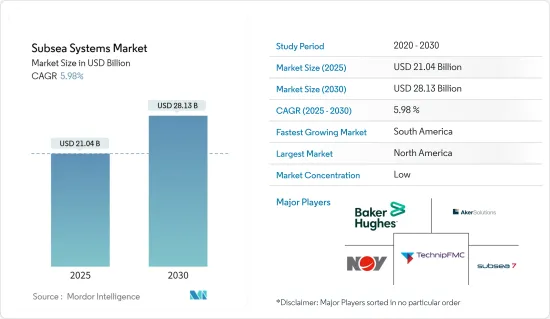

2025年のサブシーシステム市場規模は210億4,000万米ドルと推定され、2030年には281億3,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは5.98%です。

市場は、COVID-19の発生、原油価格の暴落、進行中のプロジェクトの遅れによってマイナスの影響を受けました。現在、市場は大流行前の水準まで回復しています。

主要ハイライト

- 景気後退期後の石油・ガス価格の上昇、オフショア石油・ガスセグメントへの投資の増加といった要因が、予測期間中のオフショア石油・ガス機器サービス市場、ひいては海底システム市場の主要促進要因になるとみられます。さらに、オフショアプロジェクトの実行可能性が向上し、深海や超深海の埋蔵量における活動が活発化していることも、市場を押し上げる可能性が高いです。

- しかし、海底機器の設置コストが高いことや、海洋掘削と生産に伴うリスクが、海底システム市場の成長を妨げると予想されます。

- ブラジル、エジプト、米国、イラン、カタールのような国々で深海活動が増加していることは、サブシーシステム市場の参入企業にいくつかの機会を創出する可能性が高いです。

- 南米は、サブシーシステム市場の急成長が期待されます。需要の大部分は、深海や超深海での最近の活動やいくつかの今後のプロジェクトのためにブラジルから来ています。

サブシーシステム市場の動向

市場を独占する海底生産セグメント

- 近年、成熟しつつある陸上油田の増加に伴い、オフショア探査・生産(E&P)活動が拡大しています。例えば、原油生産の最重要流域であるパーミアン・ベースンでは、古い油井からの生産量が減少し始めており、こうした地域での発見を増やす必要があります。

- Baker Hughes Companyによると、2023年3月現在、アジア太平洋では90基のオフショア・リグが稼動しています。探査の増加に伴い、海洋での発見が増えればリグ数は大幅に増加すると予想され、ひいては海底生産システムの需要を押し上げることになります。

- 例えば、2022年2月、EniSpAはアブダビで初の探鉱井を掘削したと発表しました。同社はまた、アブダビ沖ブロック2(アラブ首長国連邦)で水深115フィートで掘削中の最初の試掘井XF-002から良好な結果を記録したことを明らかにしました。

- 南米、北米、欧州での深海と超深海活動の活発化に伴い、深海油田の生産量は2025年までに日量760万バレル、2040年までに日量900万バレルに達すると予想されています。したがって、海底生産システムの需要は増加し、市場をさらに牽引すると予想されます。

- そのため、石油・ガス産業は、需要の増加に対応するため、石油・ガスの探索をより深い地域へとシフトしています。したがって、海底生産システムのシェアは、海底システムセグメントの中で最大となり、市場を牽引すると予想されます。

市場成長を支配する南米

- エネルギー需要の急増に伴い、さまざまな国、大手企業、投資家が深海に関心を移しています。深海は、数十年にわたって石油・ガスの供給を保証する可能性を秘めているからです。しかし、そのためには、海底深度数千メートルに埋蔵された石油・ガスを生産する技術を採用する必要があります。そのため、回収率を向上させ、全体的なコストを削減するための海底システムの必要性が高まっている

- 2021年のブラジルの原油・コンデンセート生産量は日量平均299万バレルで、2019年に比べ日量平均15万バレル以上増加しました。EIAによると、ブラジルは深海・超深海プロジェクトの開発で世界をリードしています。近年、石油・ガスセクターの自由化など政府の施策変更により、外国からの投資が誘致されています。

- 世界の多くの外国企業が、今後10年間の海洋炭化水素活動への投資市場としてブラジルを偵察しています。例えば、2022年10月、ONGC Videsh Ltd(OVL)は、ブラジルのオフショア炭化水素ブロックに10億米ドルの投資を計画しています。こうしたプロジェクトは、予測期間中の海底システム市場にプラスの影響を与える可能性が高いです。

- 同様に、アルゼンチンの国営エネルギー会社YPFは、最初のオフショアプロジェクトで日産20万バレルを見込んでおり、同国での生産再開に伴い、サブシーシステムの需要が高まると考えられます。

- したがって、深海や超深海における今後のプロジェクトが、南米地域における予測期間中のサブシーシステム市場の成長を牽引する可能性が高いです。

サブシーシステム産業概要

サブシーシステム市場は適度に統合されています。同市場の主要企業(順不同)には、Subsea 7 SA、TechnipFMC PLC、Akastor ASA、National-Oilwell Varco Inc.、Baker Hughes Co.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2028年までの市場規模(10億米ドル)と需要予測

- オフショアCAPEXの過去実績と需要予測(10億米ドル)(水深別、2019~2028年)

- オフショアCAPEXの過去実績と需要予測(10億米ドル)(地域別、2019~2028年)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- オフショア石油・ガスプロジェクトの実行可能性の向上

- 南北アメリカ、アジア太平洋、中東・アフリカにおける深海石油・ガス探査・生産活動の活発化

- 抑制要因

- 複数地域における海洋探査・生産活動の禁止

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 市場タイプ

- 海底生産システム

- 海底処理システム

- コンポーネント

- 海底アンビカルライザーとフローライン(SURF)

- ツリー

- ウェルヘッド

- マニホールド

- その他

- 地域

- 北米

- カナダ

- メキシコ

- 米国

- その他の北米地域

- 欧州

- ノルウェー

- 英国

- フランス

- イタリア

- アジア太平洋

- 中国

- インド

- 日本

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- イラン

- イラク

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Akastor ASA

- Subsea 7 SA

- TechnipFMC PLC

- National-Oilwell Varco Inc.

- Baker Hughes Co.

- Schlumberger Ltd

- Halliburton Co.

- Oceaneering International

- Kerui Group Co. Ltd

- Dril-Quip Inc.

第7章 市場機会と今後の動向

- 海底生産・処理システムの技術進歩

The Subsea Systems Market size is estimated at USD 21.04 billion in 2025, and is expected to reach USD 28.13 billion by 2030, at a CAGR of 5.98% during the forecast period (2025-2030).

The market was negatively impacted by the outbreak of COVID-19, the crash in the price of crude oil, and delays in ongoing projects. Currently, the market has rebounded to pre-pandemic levels.

Key Highlights

- Factors such as the increase in oil prices after the downturn period and growing investments in the offshore oil and gas sector are expected to be major drivers for the offshore oil and gas equipment and services market and, in turn, the subsea systems market during the forecast period. Moreover, the improving viability of offshore projects and rising activity in deepwater and ultra-deepwater reserves are likely to boost the market.

- However, the high installation cost of subsea equipment and risks associated with offshore drilling and production are expected to hinder the growth of the subsea systems market.

- Increasing deepwater activities in countries like Brazil, Egypt, the United States, Iran, and Qatar is likely to create several opportunities for the players in the subsea systems market.

- South America is expected to be the fastest-growing market for subsea systems. The majority of the demand comes from Brazil due to its recent activities in deepwater and ultra-deepwater and several upcoming projects.

Subsea Systems Market Trends

Subsea Production Segment to Dominate the Market

- With the rising number of maturing onshore oilfields in recent years, there has been growth in offshore exploration and production (E&P) activities. For instance, in the Permian Basin, the most critical basin in terms of crude oil production, the production from old wells has started to decline, and there needs to be more scope for discovery in these areas.

- According to Baker Hughes, as of March 2023, Asia-Pacific has 90 active offshore rigs. With the increasing exploration, rig counts are expected to grow significantly as more offshore discoveries are made, which, in turn, will boost the demand for the subsea production system.

- For instance, in February 2022, EniSpA announced its first exploration well in Abu Dhabi. The company also revealed that it had recorded positive results from its first exploration well, XF-002, currently under drilling in offshore Block 2 Abu Dhabi (UAE) at 115 feet of water depth.

- With the increasing deepwater and ultra-deepwater activities in the South American, North American, and European regions, the deepwater fields' production is expected to reach 7.6 million barrels per day by 2025 and 9 million barrels per day by 2040. Hence, the demand for subsea production systems is expected to increase and further drive the market.

- Therefore, the oil and gas industry is shifting toward deeper regions to search for oil and gas to meet the increasing demand. Hence, the subsea production systems share is expected to be the largest among subsea system segments and drive the market.

South America to Dominate the Market Growth

- As the energy demand increases rapidly, various countries, major companies, and investors are shifting their interest toward deep water, as it holds the potential for a guaranteed supply of oil and gas for a few decades. However, this requires employing technology to produce oil and gas reserves buried thousands of meters deep in the ocean floor. This has increased the need for subsea systems to improve recovery and reduce overall costs.

- In 2021, Brazil produced an average of 2.99 million barrels per day of crude oil and condensate, representing an average increase of more than 150,000 barrels per day compared with 2019. According to the EIA, Brazil is a global leader in developing deep and ultra-deepwater projects. In recent years, changes in government policies, such as liberalization in the oil and gas sector, have attracted foreign investment.

- Many foreign players worldwide are scouting Brazil for a potential investment market in offshore hydrocarbon activities during the next decade. For instance, in October 2022, ONGC Videsh Ltd (OVL) planned to invest USD 1 billion in a Brazilian offshore hydrocarbon block. Such projects are likely to impact the subsea systems market during the forecast period positively.

- Similarly, Argentina's state-backed energy company YPF expects its first offshore project to produce up to 200,000 barrels per day, which would drive the demand for subsea systems in the country as production resumes.

- Hence, the upcoming projects in deep-water and ultra-deep-water are likely to drive the growth of the subsea systems market during the forecast period in the South American region.

Subsea Systems Industry Overview

The subsea systems market is moderately consolidated. Some of the key players in the market (in no particular order) include Subsea 7 SA, TechnipFMC PLC, Akastor ASA, National-Oilwell Varco Inc., and Baker Hughes Co., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2028

- 4.3 Historic and Demand Forecast of Offshore CAPEX in billions, by Water Depth, 2019-2028

- 4.4 Historic and Demand Forecast of Offshore CAPEX in billions, by Region, 2019-2028

- 4.5 Recent Trends and Developments

- 4.6 Government Policies and Regulations

- 4.7 Market Dynamics

- 4.7.1 Drivers

- 4.7.1.1 Improved Viability Of Offshore Oil And Gas Projects

- 4.7.1.2 Rising Deep Water Oil & Gas Exploration And Production Activities In The Americas, Asia-pacific, And Middle-east & Africa Region

- 4.7.2 Restraints

- 4.7.2.1 Ban On Offshore Exploration And Production Activities In Multiple Regions

- 4.7.1 Drivers

- 4.8 Supply Chain Analysis

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Consumers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitute Products and Services

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Subsea Production Systems

- 5.1.2 Subsea Processing Systems

- 5.2 Component

- 5.2.1 Subsea Umbical Riser and Flowlines (SURF)

- 5.2.2 Trees

- 5.2.3 Wellhead

- 5.2.4 Manifolds

- 5.2.5 Other Components

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 Canada

- 5.3.1.2 Mexico

- 5.3.1.3 United States of America

- 5.3.1.4 Rest of the North America

- 5.3.2 Europe

- 5.3.2.1 Norway

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Rest of the Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of the South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Iran

- 5.3.5.4 Iraq

- 5.3.5.5 Rest of the Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Akastor ASA

- 6.3.2 Subsea 7 SA

- 6.3.3 TechnipFMC PLC

- 6.3.4 National-Oilwell Varco Inc.

- 6.3.5 Baker Hughes Co.

- 6.3.6 Schlumberger Ltd

- 6.3.7 Halliburton Co.

- 6.3.8 Oceaneering International

- 6.3.9 Kerui Group Co. Ltd

- 6.3.10 Dril-Quip Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technology Advancements In Subsea Production And Processing Systems