|

市場調査レポート

商品コード

1639455

飽和ポリエステル樹脂:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Saturated Polyester Resins - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 飽和ポリエステル樹脂:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

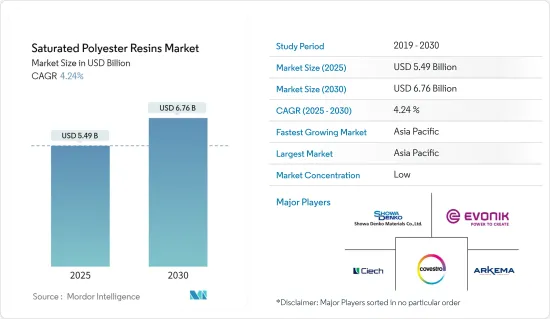

飽和ポリエステル樹脂市場規模は2025年に54億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.24%で、2030年には67億6,000万米ドルに達すると予測されます。

COVID-19の大流行中、飽和ポリエステル樹脂市場は、世界各国における操業やサプライチェーンの制限により低迷を目の当たりにしました。このような要因は、塗料・コーティング産業などの主要エンドユーザーからの需要にマイナスの影響を与えました。しかし、2021年に規制が緩和されると、ポリエステル樹脂の需要は大流行前のレベルまで上昇しました。

主要ハイライト

- 中期的に市場成長を牽引する主要要因は、機械的特性が優れているため、代替品と比較して性能が優れていることです。

- その反面、飽和ポリエステル樹脂の加工・製造コストが高いことが市場成長の妨げになると予想されます。

- 非BPA缶コーティングの動向は、飽和ポリエステル樹脂に新たな成長機会をもたらしています。

- アジア太平洋が市場を独占し、予測期間中に最も高いCAGRで推移すると予想されます。

飽和ポリエステル樹脂の市場動向

粉末コーティング需要の増加

- 飽和ポリエステル樹脂は主に無溶剤の粉体塗料やコーティング剤の製造に使用されます。優れた耐候性、優れた衝撃強度、金属への接着性(湿度の高い条件下でも)などの優れた特性を持つ飽和ポリエステル樹脂は、外装や内装の建築用途、機械、民生用電子機器、スチール家具、園芸用具の塗装に好まれています。

- 世界的には、エレクトロニクス産業における技術の進歩や研究開発活動の急速な革新ペースが、より新しく、より高速で、より信頼性の高いエレクトロニクス製品の需要を牽引しており、そのためコーティング部品のニーズが高まっている

- 日本電子情報技術産業協会(JEITA)によると、世界のエレクトロニクス・IT産業の生産額は、2021年の3兆3,600億米ドルに対し、2022年には前年比1%の成長率を記録し、3兆4,400億米ドルになると推定されています。さらに、2023年には前年比3%の成長が見込まれています。コンシューマー技術協会によると、米国における消費者向け電子機器または技術販売の小売売上高は、2021年の4,610億米ドルに対し、2022年には5,050億米ドルになると推定されています。

- 欧州では、ドイツのエレクトロニクス産業が地域最大です。ZVEIによると、ドイツのエレクトロニクス・デジタル産業の売上高は2022年11月に211億ユーロ(217億米ドル)を占め、2021年11月と比較して14.4%の成長率を記録しました。

- 同様に、成長する建設セクターは、飽和ポリエステル樹脂を使用して製造される無溶剤粉体塗料の使用を促進すると予想されます。これにより、予測期間中に調査された市場の成長を後押ししています。

- 建設部門はアジア太平洋、中東・アフリカで力強い成長を遂げています。中東・アフリカでは、各国政府が非石油部門の開発に力を入れています。例えば、サウジアラビア政府は経済変革計画「ビジョン2030」の下、数多くのインフラプロジェクトを開始しました。これらのプロジェクトは主に、電力、水、炭化水素、建設、道路、鉄道、港湾、空港の各セグメントに関するものです。

- そのため、さまざまなエンドユーザー産業からの粉体塗料需要が堅調に伸びており、飽和ポリエステル樹脂の需要を牽引すると予想されます。

市場を独占するアジア太平洋

- アジア太平洋は、中国、インド、日本のような経済圏からの需要が伸びているため、シェアで世界市場を独占しています。

- アジア太平洋は、予測期間中に飽和ポリエステル樹脂の需要が健全に成長することが期待されています。これは、同地域の建設、自動車、エレクトロニクス産業などにおける塗料・コーティング用途の顕著な成長が予想されるためです。

- 2022年2月、国家開発会議(NDC)によると、中国政府機関は1,800億台湾ドル(64億7,000万米ドル)のインフラ開発計画を提案しました。この計画には、2023~2024年にかけて使用される「将来を見据えたインフラ開発計画」の第4段階予算案が含まれています。

- 中国では、2021年に完成した開発のうち、住宅が最大の割合を占めました。住宅用建築物は完成床面積の67%以上を占めました。経済成長に伴い、農村部から都市部へ移動する人が増え、住宅へのニーズが高まっています。さらに、中国には世界最大の建設市場があり、世界全体の建設投資の20%を占めています。中国は2030年までに約13兆米ドルを建築物に投じると予想されており、世界の飽和ポリエステル樹脂市場にとって明るい市場展望となっています。

- アジア太平洋は、世界で最も価値のある自動車メーカーの本拠地です。中国、インド、日本、韓国などの新興諸国がその拠点となっています。飽和ポリエステル樹脂をベースとした塗料やコーティング剤は金属表面への高い接着性を持つため、自動車産業での使用が増加しています。

- 中国汽車工業協会(CAAM)によると、中国は世界最大の自動車生産拠点であり、2022年の自動車総生産台数は2,700万台と、昨年の2,600万台から3.4%増加します。さらに、2022年の最初の7ヵ月間に、中国は1,457万台の自動車を生産し、前年比31.5%の成長率を記録しました。さらに、2022年7月のバッテリー式電気自動車の台数は、2021年1~7月と比較して117.2%増加しました。2022年7月の同国の電気自動車販売台数は約61万7,000台と推定されます。

- さらに、インドでは、インド自動車工業会(SIAM)によると、2021~22年度(2021年4月~2022年3月)の自動車生産台数は、2020年4月~2021年3月の2,266万台に対し、2,203万台でした。さらに、インド経済モニタリングセンター(CMIE)によると、自動車生産台数は2022年6月の16万9,520台から2022年7月には19万3,630台に増加しました。このような要因が、調査対象市場の需要を増加させると思われる

- 上記の要因は、予測期間中、同地域における飽和ポリエステル樹脂の需要を促進すると予想されます。

飽和ポリエステル樹脂産業概要

飽和ポリエステル樹脂市場は部分的にセグメント化されており、主要企業が占める割合は小さいです。これらの大手企業には、Arkema Group、Covestro AG、Showa Denko Materials、Evonik Industries AG、CIECH SAが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 包装産業からの需要増加

- アジア太平洋と中東欧における急速な工業化

- その他の促進要因

- 抑制要因

- 高い加工・製造コスト

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- タイプ

- 液状飽和ポリエステル樹脂

- 固形飽和樹脂

- 用途

- 粉末コーティング

- コイル・缶塗料

- 自動車用塗料

- 包装用塗料

- 工業用塗料

- その他

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- ALLNEX GMBH

- Arkema Group

- CIECH SA

- Covestro AG

- DIC CORPORATION

- Eternal Materials Co. Ltd

- Evonik Industries AG

- Showa Denko Materials Co. Ltd

- Hitech Industries FZE

- Hexion

- Novaresine SRL

- DSM

- Sir Industriale

- Stepan Company

- Nippon Gohsei

第7章 市場機会と今後の動向

- 低VOC排出による飽和ポリエステル樹脂の使用増加

- その他の機会

The Saturated Polyester Resins Market size is estimated at USD 5.49 billion in 2025, and is expected to reach USD 6.76 billion by 2030, at a CAGR of 4.24% during the forecast period (2025-2030).

During the COVID-19 pandemic, the saturated polyester resin market witnessed a downturn due to operational and supply chain restrictions in various countries across the globe. Factors like these negatively impacted the demand from key end users like Paints and Coatings industry, among others. However, as the restriction eased in 2021, the demand for polyester resin rose to pre-pandemic levels.

Key Highlights

- Over the medium term, the major factor driving the market's growth is their better performance compared to their alternatives because of their superior mechanical properties.

- On the flip side, the high processing and manufacturing cost of saturated polyester resins is expected to hinder the studied market's growth.

- The growing trend of non-BPA can coatings creates new growth opportunities for saturated polyester resins.

- The Asia-Pacific region is expected to dominate the market and will likely witness the highest CAGR during the forecast period.

Saturated Polyester Resins Market Trends

Increasing Demand for Powder Coatings

- Saturated polyester resins are primarily used to manufacture solvent-free powder paints and coatings. Its superior properties, such as good weather resistivity, excellent impact strength, and adhesion to metals (even under humid conditions), saturated polyester resins are favored for exterior and interior architectural applications, coating machinery, domestic appliances, steel furniture, and garden tools.

- Globally the rapid pace of innovation in terms of the advancement of technologies and R&D activities in the electronics industry is driving the demand for newer, faster, and more reliable electronic products, thus increasing the need for coated components.

- According to the Japan Electronics and Information Technology Industries Association (JEITA), the production by the global electronics and IT industry was estimated at USD 3.44 trillion in 2022, registering a growth rate of 1% year on year, compared to USD 3.36 trillion in 2021. Moreover, the industry is expected to grow by 3% year on year by 2023. According to the Consumer Technology Association, the retail revenue from consumer electronics or technology sales in the United States was estimated at USD 505 billion in 2022, compared to USD 461 billion in 2021.

- In Europe, the German electronics industry is the largest in the region. According to the ZVEI, Germany's electro and digital industry turnover accounted for EUR 21.1 billion (USD 21.7 billion) in November 2022, witnessing a growth rate of 14.4% compared to November 2021.

- Similarly, the growing construction sector is expected to drive the usage of solvent-free powder coatings manufactured using saturated polyester resins. It is thereby boosting the growth of the market studied during the forecast period.

- The construction sector is witnessing robust growth in Asia-Pacific, Middle East & Africa. In the Middle East & Africa region, governments are trying to develop the non-oil sectors. For Instance, Under the Vision 2030 economic transformation plan, the Saudi Arabian government initiated numerous infrastructure projects. These projects majorly cover projects related to the power, water, hydrocarbons, construction, road, rail, seaport, and airport sectors.

- Hence, the robust growth in the demand for powder coatings from various end-user industries is expected to drive the demand for saturated polyester resins.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominated the global market in terms of share, owing to the growing demand from economies like China, India, and Japan.

- Asia-Pacific is expected to witness healthy growth in the demand for saturated polyester resins during the forecast period. It is due to the expected noticeable growth of paints and coatings applications in industries like construction, automotive, and electronics industries, among others in the region.

- In February 2022, the Chinese government agencies proposed a TWD 180 billion (USD 6.47 billion) infrastructure development plan, according to the National Development Council (NDC). It includes the proposed budget for the fourth stage of the Forward-looking Infrastructure Development Program would be used from 2023-2024.

- In China, residential buildings comprised the largest portion of finished development in 2021. Construction intended for housing accounted for over 67% of the completed floor space. As the economy grows, more people move from rural to urban regions, increasing the need for residential accommodation. In addition, the country includes the largest construction market in the world, encompassing 20% of all construction investments globally. China is expected to spend nearly USD 13 trillion on buildings by 2030, creating a positive market outlook for the global saturated polyester resins market.

- The Asia-Pacific region is home to some of the world's most valuable vehicle manufacturers. Developing countries such as China, India, Japan, South Korea. As paints and coatings based on saturated polyester resins offer high adhesion to metallic surfaces, These are increasingly used in the automotive industry.

- According to the China Association of Automobile Manufacturers (CAAM), China contains the largest automotive production base in the world, with a total vehicle production of 27 million units in 2022, registering an increase of 3.4 % compared to 26 million units produced last year. Further, in the first 7 months of 2022, the country produced 14.57 million units of cars, registering a growth rate of 31.5% Year on Year. Furthermore, in July 2022, the number of battery-powered electric vehicles increased by 117.2% compared to January-July in 2021. In July 2022, the country's electric vehicle sales were estimated at around 617 thousand units.

- Moreover, in India, during FY 2021-22 (April 2021 to March 2022), according to the Society of Indian Automobile Manufacturers (SIAM), the country's automotive industry produced a total of 22.03 million vehicles compared to 22.66 million units during April 2020 to March 2021. Further, according to the Centre for Monitoring Indian Economy (CMIE), car production increased to 193.63 thousand units in July 2022 from 169.52 thousand units in June 2022. Such factors are likely to increase the demand for the studied market

- The factors above are expected to drive the demand for saturated polyester resins in the region during the forecast period.

Saturated Polyester Resins Industry Overview

The saturated polyester resins market is partially fragmented, with the top players accounting for a small chunk of the market. These major players include Arkema Group, Covestro AG, Showa Denko Materials Co. Ltd, Evonik Industries AG, and CIECH SA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Packaging Industry

- 4.1.2 Rapid Industrialization in Asia-Pacific and Central and Eastern Europe

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Processing and Manufacturing Cost

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Liquid Saturated Polyester Resin

- 5.1.2 Solid Saturated Resin

- 5.2 Application

- 5.2.1 Powder Coatings

- 5.2.2 Coil and Can Coatings

- 5.2.3 Automotive Paints

- 5.2.4 Packaging

- 5.2.5 Industrial Paints

- 5.2.6 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ALLNEX GMBH

- 6.4.2 Arkema Group

- 6.4.3 CIECH SA

- 6.4.4 Covestro AG

- 6.4.5 DIC CORPORATION

- 6.4.6 Eternal Materials Co. Ltd

- 6.4.7 Evonik Industries AG

- 6.4.8 Showa Denko Materials Co. Ltd

- 6.4.9 Hitech Industries FZE

- 6.4.10 Hexion

- 6.4.11 Novaresine SRL

- 6.4.12 DSM

- 6.4.13 Sir Industriale

- 6.4.14 Stepan Company

- 6.4.15 Nippon Gohsei

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Usage of Saturated Polyester Resins Due to Low VOC Emissions

- 7.2 Other Opportunities