|

市場調査レポート

商品コード

1444759

大腸がんスクリーニング:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Colorectal Cancer Screening - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 大腸がんスクリーニング:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 118 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

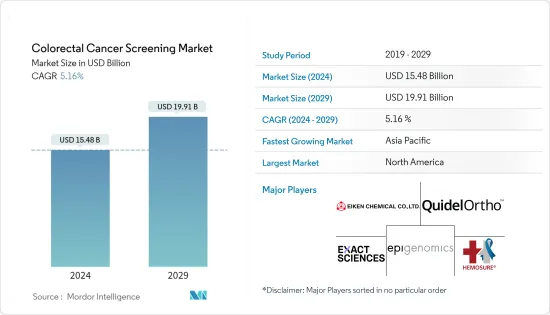

大腸がんスクリーニング市場規模は、2024年に154億8,000万米ドルと推定され、2029年までに199億1,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に5.16%のCAGRで成長します。

COVID-19のパンデミックは、パンデミック中に実施される大腸がんスクリーニングの数が減少したため、調査対象の市場に大きな影響を与えました。たとえば、MDPIが2022年5月に発表した論文によると、カナダで実施された研究では、パンデミック前と比べてパンデミック中に大腸がんの診断数が減少したことが示されました。したがって、COVID-19のパンデミックは当初市場に大きな影響を与えましたが、パンデミックは現在沈静化しており、大腸がんスクリーニング手順は通常どおり行われているため、調査対象の市場は調査の予測期間中に安定した成長を遂げると予想されます。

大腸がんスクリーニング市場の成長の主な要因には、効果的な遺伝子検査の出現、大腸がんの有病率の増加、がん予防への取り組みの増加などが含まれます。

大腸がんの有病率の上昇は、市場の成長を促進する主要な要因の1つです。たとえば、チャイニーズ・メディカル・ジャーナルが2022年3月に発表した報告書によると、中国ではがんの発生率が増加しています。 2022年の中国の新規がん患者数は約482万人で、そのうち59万2,232人が大腸がん患者だった。したがって、大腸がんの発生率の増加により、がんの治療のためのスクリーニング検査の需要が増加しています。

さらに、2022年4月にMDPIが発表した論文によると、大腸がんはカナダで最も一般的ながんの1つと考えられており、2021年には約24,800人が診断されると予測されています。 50はカナダの大腸がん症例の約8%に相当し、最近の研究では、カナダでは若年層の大腸がんの発生率が急速に増加していることが示されています。したがって、大腸がんの有病率の上昇は市場の成長を促進すると予想されます。

さらに、大腸がん予防への取り組みも市場の成長を促進すると予想されます。たとえば、オハイオ大腸がん予防イニシアチブ(OCCPI)は、新たに大腸がん(CRC)と診断された患者とその生物学的近親者を対象に、リンチ症候群のスクリーニングを行う米国全体の取り組みです。 4つの遺伝子のうちの1つの変異を受け継ぎます。

さらに、さまざまな組織や市場関係者による開発も市場の成長を促進すると予想されます。たとえば、2021年4月に米国食品医薬品局は、臨床医が結腸内視鏡検査中に結腸内のポリープや腫瘍の疑いなどの病変を検出できるようにする機械学習に基づく人工知能を使用するデバイスであるGI Geniusの承認を発表しました。

したがって、大腸がんの有病率の上昇やがん予防への取り組みなどの前述の要因が市場の成長を促進すると予想されます。ただし、新興諸国における高額なスクリーニング検査コストと不十分なヘルスケアアクセスが市場の成長を妨げると予想されます。

大腸がん検診市場動向

結腸内視鏡検査セグメントは、予測期間中にかなりの市場シェアを保持すると予想される

結腸鏡検査または結腸鏡検査は、肛門を通過した可撓性チューブ上の電荷結合素子(CCD)カメラまたは光ファイバーカメラを使用した、大腸および小腸の遠位部分の内視鏡検査です。大腸内視鏡検査は、大掛かりな手術を必要とせずに正確な診断と治療を可能にします。さらに、大腸内視鏡でポリープを切除することもできます。ただし、検査の準備として、患者は結腸を洗浄するために下剤を服用する必要があります。大腸がんの負担の増大やタイムリーなスクリーニングに対する公的機関による推奨、技術の進歩、市場での製品の発売などの要因が、予測期間中に同部門の成長を推進するとみられます。

大腸がんの罹患率の上昇は、この部門の成長を促進する主な要因の1つです。たとえば、国立がん研究センターが2022年6月に発表したデータによると、2022年には日本で推定1,019,000人の新規がん患者が発生すると予想され、このうち158,200人の新規大腸がん患者が発生すると予想されています。

同様に、Cancer Australiaが2022年 8月に更新したデータによると、2022年にオーストラリアで新たに大腸がんと診断される患者数は15,713人で、このうち男性8,300人、女性7,413人であると推定されています。したがって、大腸がんの有病率の上昇により、結腸内視鏡検査装置の使用が増加すると予想されます。

さらに、主要な市場プレーヤーによる製品発売の増加も、この分野の成長を後押しすると予想されます。たとえば、2022年 8月にメドトロニックインドは、大腸がんの結腸内視鏡検査用のAIを活用したモジュールを発売しました。このデバイスは高度なAIソフトウェアを使用して、さまざまなサイズ、形状、形態の疑わしいポリープを視覚的なマーカーでリアルタイムに強調表示します。

したがって、大腸がんの有病率の上昇や主要市場プレーヤーによる製品発売の増加などの前述の要因が、セグメントの成長を促進すると予想されます。

北米は予測期間中に市場でかなりのシェアを握ると予想される

北米が市場の大きなシェアを占めると予想されます。米国とカナダには、大腸がんの治療と診断のための十分に構造化されたヘルスケア制度があります。この地域における大腸がんの有病率の上昇、大腸がんに対する調査資金の増加、主要市場プレーヤーによる開発の増加などの要因が、この地域の市場の成長を後押しすると予想されます。

この地域における大腸がんの罹患率の高さは、市場の成長を促進する主要な要因の1つです。たとえば、2022年 5月にカナダがん協会が発表したデータによると、大腸がんは、2022年にカナダで4番目に多く診断されるがんになると予想されており、カナダではがんによる死亡原因の2番目になると予想されていました。男性ではがんによる死亡原因の第3位であり、女性ではがんによる死亡原因の第3位となっています。したがって、この国における大腸がんの高い有病率は、市場の成長を促進する主要な要因です。

さらに、2023年に米国がん協会が発表したデータによると、2023年に米国で結腸がんおよび直腸がんの新規症例数は153,020人になると推定されており、そのうち106,970人が結腸がん、46,050人が結腸がんであると予想されています。直腸がんと予想されます。したがって、国内の結腸がんと直腸がんの罹患率が高いため、市場の成長が促進されると予想されます。また、同じ情報源によると、スクリーニングは結腸、直腸、子宮頸部の前がんを検出して除去することで大腸がんの予防に役立ち、またスクリーニングはこれらのがんによる死亡率を低下させることも観察されています。したがって、大腸がんスクリーニングの重要性の高まりも市場の成長を促進すると予想されます。

さらに、主要な市場プレーヤーによる製品発売の増加も市場の成長を促進すると予想されます。たとえば、2021年 7月にFDAは、Pillar Biosciences, Inc.による大腸がんに対するONCO/Reveal Dx Lung &Colon Cancer Assay(O/RDx-LCCA)を承認しました。

したがって、大腸がんの有病率の上昇や製品発売の増加などの前述の要因が、この地域の市場の成長を促進すると予想されます。

大腸がんスクリーニング業界の概要

大腸がんスクリーニング市場は、大小さまざまなプレーヤーが存在するため、適度に統合されています。その中には、Abbott Laboratories、Epigenomics Inc.、Exact Sciences Corporation、F. Hoffmann-La Roche AG、Hemosure Inc.、Quidel Corporation、Siemens Healthineers AG、Sysmex Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 効果的な遺伝子検査の登場

- 大腸がんの罹患率の増加

- がん予防への取り組みを強化

- 市場抑制要因

- 高額なスクリーニング検査費用

- 新興諸国におけるヘルスケアアクセスの不足

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- スクリーニング検査別

- 便ベースの検査

- 結腸内視鏡検査

- CTコロノグラフィー(バーチャル大腸内視鏡検査)

- 柔軟なS状結腸鏡検査

- その他のスクリーニング検査

- エンドユーザー別

- 病院

- 独立した診断研究所

- その他のエンドユーザー

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Eiken Chemical Co. Ltd

- Epigenomics Inc.

- Exact Sciences Corporation

- Polymedco Inc

- Hemosure Inc.

- F. Hoffmann-La Roche AG

- QuidelOrtho Corporation

- Siemens Healthineers AG

- Sysmex Corporation

- Olympus Corporation

第7章 市場機会と将来の動向

The Colorectal Cancer Screening Market size is estimated at USD 15.48 billion in 2024, and is expected to reach USD 19.91 billion by 2029, growing at a CAGR of 5.16% during the forecast period (2024-2029).

The COVID-19 pandemic significantly impacted the studied market, as there was less number of colorectal cancer screenings taking place during the pandemic. For instance, according to an article published by MDPI in May 2022, a study was conducted in Canada which showed that there was a reduction in the number of colorectal cancer diagnoses during the pandemic when compared to the pre-pandemic period. Thus, the COVID-19 pandemic significantly impacted the market initially, however as the pandemic has currently subsided, colorectal cancer screening procedures are taking place normally, hence the studied market is expected to have stable growth during the forecast period of the study.

The major factors for the growth of the colorectal cancer screening market include the advent of efficacious genetic tests, an increase in the prevalence of colorectal cancer, and increasing cancer prevention initiatives.

The rising prevalence of colorectal cancer is one of the major factors driving the market growth. For instance, as per the report published by the Chinese Medical Journal in March 2022, China is experiencing a greater incidence of cancers. In 2022, there were approximately 4,820,000 new cancer cases in China, in which 592,232 were colorectal cancer cases. Thus, the greater incidence of colorectal cancers has increased the demand for screening tests for the treatment of cancers.

Furthermore, according to an article published by MDPI in April 2022, colorectal cancer is considered to be one of the most common cancers in Canada with approximately 24,800 cases projected to have been diagnosed in 2021. Although the incidence of CRC among adults under the age of 50 represents approximately 8% of CRC cases in Canada, recent studies have shown that the incidence of colorectal cancer in younger people is rising rapidly in Canada. Thus, the rising prevalence of colorectal cancer is expected to boost market growth.

Moreover, colorectal cancer prevention initiatives are also expected to boost market growth. For instance, The Ohio Colorectal Cancer Prevention Initiative (OCCPI), is a statewide initiative in Ohio, United States to screen newly diagnosed colorectal cancer (CRC) patients and their biological relatives for Lynch syndrome, a cancer-causing condition that occurs when a person inherits a mutation in one of four genes.

Additionally, the developments by various organizations and market players are also expected to boost the market growth. For instance, in April 2021, the US Food and Drug Administration announced the approval of GI Genius, a device using artificial intelligence based on machine learning to help clinicians detect lesions like polyps or suspected tumors in the colon during a colonoscopy.

Thus, the aforementioned factors such as the rising prevalence of colorectal cancer and cancer prevention initiatives are expected to boost the market growth. However, high screening tests costs and inadequate healthcare access in developing countries are expected to impede the market growth.

Colorectal Cancer Screening Market Trends

Colonoscopy Segment is Expected to Hold a Significant Market Share Over the Forecast Period

Colonoscopy or coloscopy is the endoscopic examination of the large bowel and the distal part of the small bowel with a charged coupled device (CCD) camera or a fiber optic camera on a flexible tube passed through the anus. Colonoscopy allows accurate diagnosis and treatment without the need for a major operation. In addition, a colonoscope can also remove the polyps. However, in preparation for the test, the patient has to take a dose of laxatives to cleanse the colon. Factors such as the growing burden of colorectal cancer and recommendations by public organizations for timely screening, technological advancements, and the launch of products in the market are likely to propel the segment's growth over the forecast period.

The rising prevalence of colorectal cancer is one of the major factors driving the segment's growth. For instance, according to the data published by National Cancer Center Japan in June 2022, an estimated 1,019,000 new cases of cancer were expected in Japan in 2022, out of which 158,200 new cases of colorectal cancer were expected.

Similarly, according to the data updated by Cancer Australia in August 2022, it was estimated that 15,713 new cases of colorectal cancer will be diagnosed in Australia in 2022, out of which 8,300 were males and 7,413 were females. Thus, the rising prevalence of colorectal cancer is expected to boost the usage of colonoscopy devices.

Furthermore, the rising product launches by key market players are also expected to boost the segment growth. For instance, in August 2022, Medtronic India launched an AI-powered module for colonoscopy of colorectal cancer. The device uses advanced AI software to highlight suspicious polyps of various sizes, shapes, and morphologies with a visual marker in real-time.

Thus, the aforementioned factors such as the rising prevalence of colorectal cancer and the increasing product launches by major market players are expected to boost segment growth.

North America is Expected to Hold a Significant Share in the Market Over the Forecast Period

North America is expected to account for a significant share of the market. The United States and Canada have a well-structured healthcare system for the treatment and diagnosis of colorectal cancer. Factors such as the rising prevalence of colorectal cancer in the region, rising research funding for colorectal cancer, and increasing developments by major market players are expected to boost the market growth in the region.

The high prevalence of colorectal cancers in the region is one of the major factors driving the market growth. For instance, according to the data published by the Canadian Cancer Society in May 2022, colorectal cancer was expected to be the fourth most commonly diagnosed cancer in Canada in 2022, and it was also expected to be the second leading cause of death from cancer in men and the third leading cause of death from cancer in women. Thus, the high prevalence of colorectal cancer in the country is a major factor driving the market growth.

Furthermore, according to the data published by the American Cancer Society in 2023, it is estimated that there will be 153,020 new cases of colon and rectum cancers in the United States in 2023, out of which 106,970 are expected to be colon cancers and 46,050 are expected to be rectum cancer. Thus, the high prevalence of colon and rectum cancers in the country is expected to boost market growth. Also, according to the same source, it has been observed that screening can help prevent colorectal cancers by detecting and removing precancers in the colon, rectum, and uterine cervix, and screening can also reduce mortality for these cancers. Thus, the rising importance of colorectal cancer screening is also expected to boost market growth.

Moreover, the rising product launches by major market players are also expected to boost market growth. For instance, in July 2021, FDA approved the ONCO/Reveal Dx Lung & Colon Cancer Assay (O/RDx-LCCA) for colorectal cancer by Pillar Biosciences, Inc.

Thus, the aforementioned factors such as the rising prevalence of colorectal cancer and the increasing product launches are expected to boost the market growth in the region.

Colorectal Cancer Screening Industry Overview

The colorectal cancer screening market is moderately consolidated due to the presence of many small and large players. Some of them include Abbott Laboratories, Epigenomics Inc., Exact Sciences Corporation, F. Hoffmann-La Roche AG, Hemosure Inc., Quidel Corporation, Siemens Healthineers AG, and Sysmex Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advent of Efficacious Genetic Tests

- 4.2.2 Increase in Prevalence of Colorectal Cancer

- 4.2.3 Increasing Cancer Prevention Initiatives

- 4.3 Market Restraints

- 4.3.1 High Screening Tests Costs

- 4.3.2 Inadequate Healthcare Access in Developing Countries

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Screening Test

- 5.1.1 Stool-based Tests

- 5.1.2 Colonoscopy

- 5.1.3 CT Colonography (Virtual Colonoscopy)

- 5.1.4 Flexible Sigmoidoscopy

- 5.1.5 Other Screening Tests

- 5.2 By End User

- 5.2.1 Hospitals

- 5.2.2 Independent Diagnostic Labs

- 5.2.3 Other End Users

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Eiken Chemical Co. Ltd

- 6.1.2 Epigenomics Inc.

- 6.1.3 Exact Sciences Corporation

- 6.1.4 Polymedco Inc

- 6.1.5 Hemosure Inc.

- 6.1.6 F. Hoffmann-La Roche AG

- 6.1.7 QuidelOrtho Corporation

- 6.1.8 Siemens Healthineers AG

- 6.1.9 Sysmex Corporation

- 6.1.10 Olympus Corporation