|

市場調査レポート

商品コード

1637890

住宅用太陽エネルギー-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Residential Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 住宅用太陽エネルギー-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

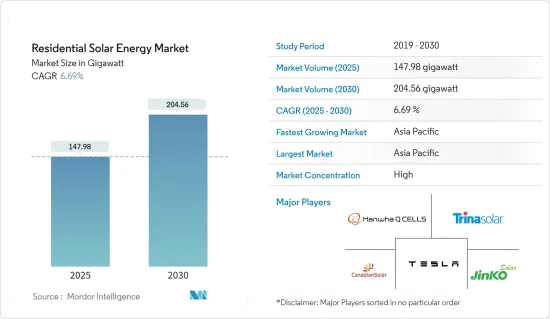

住宅用太陽エネルギー市場規模は2025年に147.98ギガワットと推定され、予測期間(2025~2030年)のCAGRは6.69%で、2030年には204.56ギガワットに達すると予測されます。

主要ハイライト

- 中期的には、有利な政府施策、今後の屋根上太陽光発電プロジェクトへの投資の増加、太陽エネルギー導入の増加につながる太陽エネルギーのコスト削減などの要因が、予測期間中の市場を牽引するとみられます。

- 一方、アフリカなどの地域では、資金調達オプションの不足や住宅用太陽光発電システムの統合が困難であることが、市場の成長を抑制すると予想されます。

- しかし、エネルギーミックスに占める再生可能エネルギーの割合を増やすという野心的な目標が掲げられています。これらの国々の政府もまた、今後数年間で住宅用太陽光発電システムを導入することで再生可能エネルギーの割合を増やすことを計画しています。このことは、予測期間中、住宅用太陽光発電のメーカーやサプライヤーにとって好機となることが期待されます。

- アジア太平洋は、エネルギー需要の増加により、予測期間中最も急成長する市場になると予想されます。この成長は、インド、中国、オーストラリアを含むアジア太平洋諸国における投資の増加と政府の支援施策によるものです。

住宅用太陽エネルギー市場の動向

屋上ソーラー設置の増加が市場を牽引

- 住宅セグメントでの太陽光発電システム導入の増加は、主に電気料金の節約、代替電力源の必要性、気候変動リスクの軽減への期待によるものです。

- 予測期間中、太陽光発電コストの低下、住宅用太陽光発電に対する政府の支援施策、FITプログラムやインセンティブ、さまざまな太陽光エネルギー目標により、屋上用太陽光発電の需要は増加すると予想されます。

- 住宅用屋根上太陽光発電の電力コストは近年急速に低下しています。価格の下落は、世界の住宅用太陽光発電容量の大幅な増加をもたらし、多くの国が住宅用屋根上太陽光発電の目標を増やしています。

- 太陽エネルギー産業協会(SEIA)の統計によると、2023年、米国の住宅用太陽光発電の累積設置容量は約3,626万8,000kWに達します。総設置容量は前年比で23%増加しました。容量の増加は、主に家庭の電気代の高騰と停電によるものです。

- 欧州共同研究センターの分析によると、EUの屋根上太陽光発電は、年間680TWhの太陽光発電が可能です。

- 2024年4月、ドイツ議会は国内の太陽光発電開発を支援する一連の新措置を承認しました。40 kWの屋上太陽光発電設備は、固定価格買取制度の対象となり、現行の価格水準より1.5c/kWh高くなります。さらに、新法は、大規模設置の入札において、地上設置型太陽光発電プロジェクトの上限を20MWから50MWに引き上げます。最後に、一般家庭でもPVバルコニーシステムやスマートエネルギーコミュニティの導入が容易になります。

- こうしたすべての要因が、予測期間中に住宅用太陽光発電の需要を促進すると予想されます。

アジア太平洋が市場を独占する

- アジア太平洋は世界の住宅用太陽光発電市場の30%以上を占めています。予測期間中もその優位性は続くとみられます。

- インドの太陽光発電設備容量は2022年の63.048GWから2023年には72.767GWへと大幅に増加しており、電力需要は今後さらに増加すると予想されます。

- 増加する電力需要に対応し、2030年までに500GWという再生可能エネルギー目標を達成するため、インド政府は2026年までに住宅部門の屋根上太陽光発電の設置容量を約4GWまで増やすことを計画しています。そのため、政府は目標を達成するために、住宅部門が太陽エネルギーを導入するためのさまざまな施策を開始しました。

- 再生可能エネルギー発電省(MNRE)の系統連系屋根上太陽光発電プログラムは、屋根上システムの最初の発電容量3kWに対して40%、上限10kWまで20%の補助金を提供することを目的としています。

- 制度とは別に、インドでは電気料金が上昇しているため、住宅部門の屋上太陽光発電市場は魅力的と考えられます。インドの平均的な電気料金は1ユニットあたり6~9インドルピー程度であり、電力需要の増加により上昇する可能性が高いです。2023年上半期には、アッサム州、カルナータカ州、マハラシュトラ州、タミル・ナードゥ州といったインド各州が、住宅用電力料金の値上げを実施しました。そのため、人々は電気代を削減またはゼロにするために、自宅に屋上太陽光発電システムを導入する可能性が高いです。

- 中国政府は2023年末に、政党や政府機関の建物の屋上の50%、学校や病院などの公共施設の40%、工業・商業地域の30%、農村家庭の20%をソーラーパネルでカバーすることを提案しています。31省676県がこの計画に登録しています。

- このような要因から、住宅用太陽エネルギーの需要は、予測期間中にアジア太平洋で増加すると予想されます。

住宅用太陽エネルギー産業概要

住宅用太陽エネルギー市場は細分化されています。同市場の主要企業(順不同)には、Trina Solar、Canadian Solar Inc.、JinkoSolar Holding、Hanwha Q Cells、Tesla Inc.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 世界の再生可能エネルギーミックス(2023年)

- 住宅用太陽エネルギーの設置容量と2029年までの予測

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 有利な政府施策

- 太陽エネルギーシステムのコスト削減

- 抑制要因

- アフリカのような地域における住宅用太陽光発電システムの統合の難しさと結びついた融資オプションの欠如

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション-地域別

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- ロシア

- ノルディック

- トルコ

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- チリ

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- カタール

- ナイジェリア

- エジプト

- その他の中東・アフリカ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Trina Solar Co. Ltd

- Yingli Green Energy Holding Company Limited

- Canadian Solar Inc.

- JinkoSolar Holding Co. Ltd

- JA Solar Holdings Co. Ltd

- Sharp Corporation

- ReneSola Ltd

- Hanwha Q Cells Co. Ltd

- SunPower Corporation

- Tesla Inc.

- List of Other Prominent Players

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- 世界の総エネルギーミックスにおける再生可能エネルギー比率を高めるための野心的目標

目次

Product Code: 48265

The Residential Solar Energy Market size is estimated at 147.98 gigawatt in 2025, and is expected to reach 204.56 gigawatt by 2030, at a CAGR of 6.69% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as favorable government policies, increasing investments in upcoming rooftop solar projects, and the reduced cost of solar energy, which has led to increased adoption of solar energy, are expected to drive the market during the forecast period.

- On the other hand, the lack of financing options and the difficulties in integrating residential solar PV systems in regions like Africa are expected to restrain the market's growth.

- However, ambitious targets are being undertaken to increase the renewable share in their energy mix. Governments across these nations also plan to increase the renewable energy share by deploying residential solar PV systems in the coming years. This factor, in turn, is expected to act as an opportunity for residential solar energy manufacturers and suppliers during the forecast period.

- Asia-Pacific is expected to be the fastest-growing market during the forecast period due to the rising energy demand. This growth is attributed to increasing investments and supportive government policies in Asia-Pacific countries, including India, China, and Australia.

Residential Solar Energy Market Trends

Increasing Rooftop Solar Installations to Drive the Market

- The increasing adoption of solar PV systems in the residential sector is primarily driven by expected savings in electricity costs, the need for an alternative source of electricity, and the desire to mitigate climate change risk.

- During the forecast period, the demand for rooftop solar PV is expected to increase due to decreasing solar PV costs, supportive government policies for residential solar PV, FIT programs and incentives, and various solar energy targets.

- The cost of electricity for residential rooftop solar PV applications has rapidly declined in recent years. The falling price has resulted in a massive increase in the global residential PV capacity, and many countries are increasing their residential rooftop targets.

- The Solar Energy Industry Association (SEIA) statistics show that, in 2023, the cumulative residential solar PV installed capacity in the United States accounted for about 36.268 GW. The total installed capacity grew by 23% compared to the previous year. The hike in capacity is mainly due to high household electricity bills and power outages.

- A European Joint Research Centre analysis shows that EU rooftop PV could produce 680 TWh of solar electricity annually.

- In April 2024, the German parliament approved a new series of measures to support solar PV development in the country. Rooftop solar PV installations of 40 kW are made eligible for feed-in tariffs that will be EUR 1.5c/kWh higher than current tariff levels. In addition, the new law increases the limit for ground-mounted solar projects from 20 MW to 50 MW in tenders for large-scale installations. Finally, it will become easier for households to deploy PV balcony systems and smart energy communities.

- All such factors are expected to drive the demand for residential solar energy over the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific accounted for more than 30% of the global residential solar PV market. It is expected to continue its dominance during the forecast period.

- India's solar PV installed capacity increased significantly from 63.048 GW in 2022 to 72.767 GW in 2023, and the demand for power is expected to increase further in the coming years.

- To cater to the rising power demand and meet its renewable energy target of 500 GW by 2030, the Indian government plans to increase the installed capacity of rooftop solar energy in the residential sector to around 4 GW by 2026. Thus, the government has initiated various policies for the residential sector to adopt solar energy to achieve the target.

- The Ministry of New and Renewable Energy (MNRE)'s grid-connected rooftop solar program aims to offer a 40% subsidy for the first 3 kW of generation capacity in rooftop systems and a 20% subsidy up to a 10 kW ceiling.

- Apart from schemes, the rooftop solar energy market for the residential sector seems appealing in India due to its increasing electricity tariff. On average, the electricity tariff in India is around INR 6-9 per unit, which is likely to increase due to a rise in electricity demand. In H1 2023, Indian states like Assam, Karnataka, Maharashtra, and Tamil Nadu raised their tariff for residential users. Hence, people are likely to adopt rooftop solar PV systems in their homes to reduce or make zero electricity bills.

- At the end of 2023, the Chinese government proposed to cover 50% of rooftop space with solar panels on party and government buildings, 40% of schools, hospitals, and other public facilities, 30% of industrial and commercial areas, and 20% of rural households. A total of 676 counties from 31 provinces have registered for the scheme.

- Owing to such factors, the demand for residential solar energy is expected to increase in Asia-Pacific over the forecast period.

Residential Solar Energy Industry Overview

The residential solar energy market is fragmented. Some of the major players in the market (in no particular order) include Trina Solar Co. Ltd, Canadian Solar Inc., JinkoSolar Holding Co. Ltd, Hanwha Q Cells Co. Ltd, and Tesla Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Renewable Energy Mix, Global, 2023

- 4.3 Residential Solar Energy Installed Capacity and Forecast, till 2029

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Favorable Government Policies

- 4.6.1.2 Reduced Cost of Solar Energy Systems

- 4.6.2 Restraints

- 4.6.2.1 Lack of Financing Options Coupled with Difficulties in Integrating Residential Solar PV Systems in Regions like Africa

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION - By Geography

- 5.1 North America

- 5.1.1 United States

- 5.1.2 Canada

- 5.1.3 Rest of North America

- 5.2 Europe

- 5.2.1 Germany

- 5.2.2 France

- 5.2.3 United Kingdom

- 5.2.4 Italy

- 5.2.5 Spain

- 5.2.6 Russia

- 5.2.7 NORDIC

- 5.2.8 Turkey

- 5.2.9 Rest of Europe

- 5.3 Asia-Pacific

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 Australia

- 5.3.5 Malaysia

- 5.3.6 Thailand

- 5.3.7 Indonesia

- 5.3.8 Vietnam

- 5.3.9 Rest of Asia-Pacific

- 5.4 South America

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Chile

- 5.4.4 Colombia

- 5.4.5 Rest of South America

- 5.5 Middle East and Africa

- 5.5.1 Saudi Arabia

- 5.5.2 United Arab Emirates

- 5.5.3 South Africa

- 5.5.4 Qatar

- 5.5.5 Nigeria

- 5.5.6 Egypt

- 5.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Trina Solar Co. Ltd

- 6.3.2 Yingli Green Energy Holding Company Limited

- 6.3.3 Canadian Solar Inc.

- 6.3.4 JinkoSolar Holding Co. Ltd

- 6.3.5 JA Solar Holdings Co. Ltd

- 6.3.6 Sharp Corporation

- 6.3.7 ReneSola Ltd

- 6.3.8 Hanwha Q Cells Co. Ltd

- 6.3.9 SunPower Corporation

- 6.3.10 Tesla Inc.

- 6.4 List of Other Prominent Players

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Ambitious Targets to Increase the Renewable Share in Total Energy Mix Worldwide