|

市場調査レポート

商品コード

1686311

民間航空機用アビオニクス-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Commercial Aircraft Avionics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 民間航空機用アビオニクス-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 105 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

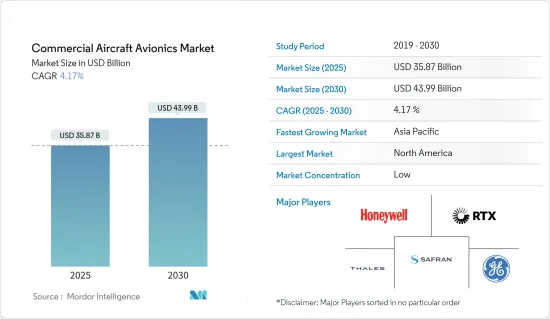

民間航空機用アビオニクス市場規模は2025年に358億7,000万米ドルと推定され、予測期間中(2025年~2030年)のCAGRは4.17%で、2030年には439億9,000万米ドルに達すると予測されます。

主なハイライト

- 世界の航空セクターは、COVID-19パンデミックによる未曾有の混乱に見舞われ、その結果、旅客輸送量が激減し、航空機需要に悪影響を及ぼしました。このセクターは2021年に改善の兆しを見せたもの、民間航空機の納入はCOVID以前の水準を大幅に下回りました。さらに、旅客需要は2023年までにCOVID以前の水準に正常化すると予測されているため、民間航空セクターは緩やかに回復すると予想され、民間航空機アビオニクス市場の成長に課題が残るとみられています。

- 航空分野は、構造や電子機器を含む航空機設計のあらゆる側面を規定する厳しい規制によって管理されています。連邦航空局(FAA)などの著名な航空規制機関は、アビオニクス・システムの取り付けや修理に関して、航空機OEMやサードパーティ・サービス・プロバイダーが遵守すべき厳格なガイドラインを発表しています。

- 同市場は、同地域を運航する航空会社が開始した機体拡大および近代化プログラムの一環として、新型民間航空機の需要が回復していることによって牽引されています。さらに、航空機の整備・修理・運航(MRO)プロバイダー間のパートナーシップの拡大は、航空会社が調達した新世代航空機の整備を可能にする技術力を促進すると予想されます。しかし、COVID-19によるワイドボディ機の早期退役は、ナローボディ機よりもワイドボディ機のアビオニクス・システムのサイズと設置コストがはるかに高いため、アビオニクス・レトロフィット分野に影響を与えると予想されます。

民間航空機用アビオニクス・システム市場の動向

予測期間中はナローボディセグメントが市場を独占

- 民間航空機アビオニクス市場は、ナローボディセグメントが支配的です。ほとんどの格安航空会社(LCC)が、新たな市場機会を開拓するために既存の航空機を近代化し、歴代の航空機の能力に合わせようとしているため、こうした航空機の需要は増加すると予想されます。民間航空機メーカーのエアバスは、2021年の609機から2022年には661機の民間航空機を納入しました。また、ボーイングは2022年に480機の民間航空機を納入しました。

- 例えば、2021年12月、エールフランス-KLMオランダ航空は、エアバスA320ネオ・ファミリー100機と追加60機のオプションの発注を発表しました。この発注はA320ネオとA321ネオの混合機で構成され、最初の納入は2023年後半に予定されています。一方、B737 MAX騒動はボーイング社の市場見通しを阻害したが、FAAからの再認証が成功したことで、B737 MAX機の需要が回復し始めています。複数の航空会社が737 MAXの運航を再開し、737 MAXの新機材を発注し始めています。

- 例えば、2022年1月、ボーイングはカタール航空から737 MAX 10を25機、さらに25機購入するオプションとともに大口受注したと発表しました。同航空会社はまた、次期777X型機34機の発注と、さらに16機のオプション契約を結びました。GEアビエーション、コリンズ・エアロスペース、L3ハリス・テクノロジーズ・インク、ホネウィウェル・インターナショナル・インク、コブハムPLCなどの企業は、ボーイング737および777ファミリーの航空機にアビオニクス部品を提供しています。国内航空旅客輸送量の回復が早まれば、ナローボディ航空機の新規受注も増加すると予想され、ナローボディ・プログラムに関連するアビオニクス・システム・プロバイダーの成長見通しを後押しする可能性があります。

北米が市場で最も高いシェアを占める

- この地域の航空宇宙産業は成熟しており、堅調な航空基盤に強く支えられています。航空交通量の増加により、地域航空会社や国際航空会社が複数の航空機を調達しています。米国を拠点とする大手航空機製造会社(OEM)の1つであるボーイングは、アビオニクス・システムに膨大な需要を生み出しています。

- 原材料の入手可能性、政治的安定性、生産コストの低さといった要因が、この地域における新たな航空宇宙製造施設の設立を後押ししています。また、航空燃料価格の変動が引き金となり、北米では低燃費の新世代航空機に対する需要が急増しています。そのため、航空機OEMは増え続ける需要に対応するため、生産能力を増強し始めています。

- エアバスは、2022年初頭にA220型機の生産数を月産6機程度に増やすと発表しました。エアバスは、2025年までにA220の生産能力を14機(ミラベル工場で毎月10機、モービル工場で毎月4機)に引き上げることを目標としています。米国を拠点とする4つの顧客、すなわちジェットブルー、デルタ航空、ブリーズ・エアウェイズ、エア・リース・コーポレーションが、A220プログラムの受注残の半分以上を占めています。レイセオン・テクノロジーズ・コーポレーションは、オンボード・コンピューター、ウェザー・マッピング・レーダー、電子飛行計器システムなど、A220に統合されているアビオニクス・サブシステムの大部分を提供しています。この地域の他の航空会社も、パンデミック後の成長を狙っています。

- 例えば、ユナイテッド航空は2022年12月、787ドリームライナー100機と、さらに100機を追加するオプションという、米国の航空会社による商業航空史上最大のワイドボディ機発注を発表しました。この発注により、ユナイテッド航空は2032年までに700機の新型ナローボディおよびワイドボディ機の納入を見込んでおり、2023年には週平均2機、2024年には週平均3機の納入を見込んでいます。こうした開発は、予測期間中の北米市場の見通しを明るいものにしています。

民間航空機用アビオニクス・システム産業の概要

民間航空機用アビオニクス市場は、多数のアビオニクス・システム・プロバイダーが存在するため、適度に断片化されています。Raytheon Technologies Corporation、General Electric Company、Honeywell International Inc.、Safran、およびTHALESは、市場における著名な企業の一部です。活発な企業の市場シェアは、民間航空機の高い納入量によって後押しされています。主要OEMの市場支配力は、自社製品を優れたものにし、要求される安全基準の遵守を確実にする高性能アビオニクス・コンポーネントとサブシステムの絶え間ない研究開発によって支えられています。複数のバリエーションと継続的な製品開発サイクルが利用可能なため、このようなシステムの運用寿命が向上します。

例えば、2023年6月のパリ・エアショーで、エンブラエル・サービシズ&サポート社は、Eジェット機用の次世代バージョンの航空機健全性分析・診断(AHEAD)システムを発表しました。このAHEADシステムは、着陸装置、航法、空気圧など、複数のシステムからの動向を統合・分析し、異常を検知して重大な事態になる前に潜在的な問題を特定することができます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- サブシステム

- ヘルスモニタリングシステム

- 飛行管理・制御システム

- 通信およびナビゲーション

- コックピットシステム

- 視覚化および表示システム

- その他のサブシステム

- 航空機タイプ

- ナローボディ

- ワイドボディ

- リージョナル機

- フィット

- ラインフィット

- レトロフィット

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- カタール

- その他の中東・アフリカ

- ラテンアメリカ

- ブラジル

- メキシコ

- その他のラテンアメリカ

- 北米

第6章 競合情勢

- Vendor Share Analysis

- 企業プロファイル

- Honeywell International Inc.

- General Electric Company

- THALES

- BAE Systems plc

- Cobham Limited

- Esterline Technologies Corporation(TransDigm Group)

- Diehl Stiftung & Co. KG

- L3Harris Technologies Inc.

- Raytheon Technologies Corporation

- Meggitt PLC

- Teledyne Technologies Incorporated

- Safran

第7章 市場機会と今後の動向

The Commercial Aircraft Avionics Market size is estimated at USD 35.87 billion in 2025, and is expected to reach USD 43.99 billion by 2030, at a CAGR of 4.17% during the forecast period (2025-2030).

Key Highlights

- The global aviation sector underwent an unprecedented disruption due to the COVID-19 pandemic, resulting in a drastic reduction in passenger traffic that negatively impacted aircraft demand. Though the sector showed signs of improvement in 2021, the deliveries of commercial aircraft were significantly lower than the pre-COVID levels. Furthermore, the commercial aviation sector is expected to recover slowly, as travel demand is projected to normalize to pre-COVID levels by 2023, which is expected to challenge the growth of the commercial aircraft avionics market.

- The aviation sector is governed by stringent regulations that stipulate all aspects of aircraft design, including structures and electronics. Prominent aviation regulatory agencies, such as the Federal Aviation Administration (FAA), have issued strict guidelines for adherence by aircraft OEMs and third-party service providers regarding avionics systems fitment and repair.

- The market is driven by the recovering demand for new commercial aircraft as part of the fleet expansion and modernization programs initiated by airlines operating in the region. Additionally, the increasing partnership between aircraft maintenance, repair, and operations (MRO) providers is expected to drive their technical capabilities, enabling them to service new-generation aircraft procured by airlines. However, the early retirement of widebody jets due to COVID-19 is anticipated to impact the avionics retrofit sector since the size and installation costs of avionics systems on a widebody are much higher than a narrowbody aircraft.

Commercial Aircraft Avionics Systems Market Trends

Narrowbody Segment to Dominate the Market During the Forecast Period

- The narrowbody segment dominated the commercial aircraft avionics market. The demand for such aircraft is anticipated to increase as most low-cost carriers (LCCs) are trying to modernize their existing fleets to exploit new market opportunities and match the competencies of successive aircraft versions. Airbus, a commercial aircraft manufacturer, delivered 661 commercial aircraft in 2022, up from 609 in 2021. Also, Boeing delivered 480 commercial aircraft in 2022.

- For instance, in December 2021, Air France-KLM announced an order for 100 Airbus A320 neo family aircraft, along with options for an additional 60 planes. The order consists of a mix of A320 neo and A321 neo aircraft, with the first deliveries expected in the second half of 2023. On the other hand, though the B737 MAX fiasco has hampered the market prospects for The Boeing Company, the successful recertification from the FAA has started driving back the demand for B737 MAX aircraft. Several airlines have started resuming operations on the 737 MAX jets and ordering new 737 MAX aircraft.

- For instance, in January 2022, Boeing announced that it had won a major order from Qatar Airways for 25 737 Max 10 jets, along with options to buy 25 more aircraft. The airline also signed an order for 34 of the upcoming 777X, as well as options for 16 more jets. Companies like GE Aviation, Collins Aerospace, L3Harris Technologies Inc., Honewywell International Inc., and Cobham PLC provide avionic components for the Boeing 737 and 777 families of aircraft. The quicker recovery of domestic air passenger traffic is also anticipated to rake in new orders for the narrowbody aircraft, which may drive the growth prospects of avionics systems providers associated with the narrowbody programs.

North America Held Highest Shares in the Market

- The aerospace industry in the region is mature and strongly supported by a robust aviation base. Higher air traffic has resulted in the procurement of several aircraft by regional and international airline operators. Boeing, one of the major aircraft original equipment manufacturers (OEMs) based in the United States, generates a huge demand for avionics systems.

- Factors such as the availability of raw materials, political stability, and low production costs have driven the establishment of new aerospace manufacturing facilities in the region. Also, fluctuations in aviation fuel prices have triggered a surge in demand for fuel-efficient new-generation aircraft in North America. Hence, aircraft OEMs have started increasing their production capabilities to cope with the ever-increasing demand.

- Airbus announced that it would increase the production rate of the A220 aircraft to around six per month in early 2022. It aims to increase the A220 production rate to 14 by 2025, i.e., 10 aircraft produced each month at its Mirabel facility and four at Mobile. Four United States-based customers, namely JetBlue, Delta Air Lines, Breeze Airways, and Air Lease Corporation, constitute more than half of the backlog of the A220 program. Raytheon Technologies Corporation provides a majority of avionics subsystems integrated into the A220, including onboard computers, weather mapping radar, and electronic flight instrument systems. Other airlines in the region are also looking for post-pandemic growth.

- For instance, in December 2022, United Airlines announced its largest widebody aircraft order by a US carrier in commercial aviation history, for 100 new 787 Dreamliners plus options to add 100 more. With this order, the airline is now expecting new deliveries of 700 new narrowbody and widebody aircraft by 2032, on an average of 2 aircraft per week in 2023 and 3 aircraft per week in 2024. Such developments render a positive outlook for the market in North America during the forecast period.

Commercial Aircraft Avionics Systems Industry Overview

The commercial aircraft avionics market is moderately fragmented in nature due to the presence of a large number of avionics systems providers. Raytheon Technologies Corporation, General Electric Company, Honeywell International Inc., Safran, and THALES are some of the prominent players in the market. The market share of the active players is boosted by the high delivery volumes of commercial aircraft. The market dominance of key OEMs is supported through relentless R&D of high-performance avionic components and subsystems that render their products superior and ensure adherence to required safety standards. The availability of several variants and continuous product development cycles enables the enhanced operating life of such systems.

For instance, in June 2023, at the Paris Air Show, Embraer Services & Support launched the next-generation version of its aircraft health analysis and diagnosis (AHEAD) system for its E-Jets. This AHEAD system will integrate and analyze trends from several systems, such as landing gear, navigation, pneumatics, etc., and can detect anomalies and identify potential issues before they become critical.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Subsystem

- 5.1.1 Health Monitoring Systems

- 5.1.2 Flight Management and Control Systems

- 5.1.3 Communication and Navigation

- 5.1.4 Cockpit Systems

- 5.1.5 Visualizations and Display Systems

- 5.1.6 Other Subsystems

- 5.2 Aircraft Type

- 5.2.1 Narrowbody

- 5.2.2 Widebody

- 5.2.3 Regional Aircraft

- 5.3 Fit

- 5.3.1 Linefit

- 5.3.2 Retrofit

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Middle-East and Africa

- 5.4.4.1 United Arab Emirates

- 5.4.4.2 Saudi Arabia

- 5.4.4.3 Qatar

- 5.4.4.4 Rest of Middle-East and Africa

- 5.4.5 Latin America

- 5.4.5.1 Brazil

- 5.4.5.2 Mexico

- 5.4.5.3 Rest of Latin America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Share Analysis

- 6.2 Company Profiles

- 6.2.1 Honeywell International Inc.

- 6.2.2 General Electric Company

- 6.2.3 THALES

- 6.2.4 BAE Systems plc

- 6.2.5 Cobham Limited

- 6.2.6 Esterline Technologies Corporation (TransDigm Group)

- 6.2.7 Diehl Stiftung & Co. KG

- 6.2.8 L3Harris Technologies Inc.

- 6.2.9 Raytheon Technologies Corporation

- 6.2.10 Meggitt PLC

- 6.2.11 Teledyne Technologies Incorporated

- 6.2.12 Safran