砲兵弾薬- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Artillery Ammunition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1686640

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

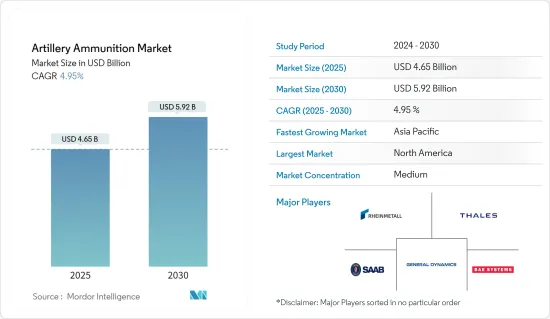

砲兵弾薬市場規模は2025年に46億5,000万米ドルと推定・予測され、予測期間中(2025年~2030年)のCAGRは4.95%で、2030年には59億2,000万米ドルに達すると予測されます。

砲兵弾薬は軍事技術の著しい進歩を象徴するものであり、正確な目標への関与と巻き添え被害の顕著な減少を可能にします。戦争が進化するにつれ、精度の重視と民間人への被害を最小限に抑える必要性が最重要視されるようになり、この先進的な弾薬の需要を牽引しています。

世界の市場動向はダイナミックであり、いくつかの重要な動向の影響を受けています。注目すべき動向の一つは、高度な照準システムの統合とネットワーク中心戦争能力の強化に重点が置かれていることです。さらに、従来の大規模な軍事作戦からの転換を示す非対称戦環境に合わせた弾薬の需要が急増していることも、業界の成長を後押ししています。

各国の軍事費の増加は、軍事兵器や弾薬を更新するための様々な軍事イニシアチブを支えており、これは砲兵弾薬の需要を生み出すと予想されます。弾薬製造企業による、射程距離の延長、殺傷力の向上、精度を高める統合センサーを備えた新型の先進砲弾の開発は、将来の調達のために各国の軍隊を魅了すると予想され、それによって市場は予測期間中に大きな成長を示すことになります。

規制上の課題は、特に国際兵器条約と輸出規制に関するもので、市場の成長を制約します。高度な軍事技術の開発と移転の複雑さは、コストの上昇と開発期間の長期化につながることが多いです。さらに、従来の無誘導砲とは対照的に、精密誘導弾は価格が高いため、特に国防予算に制約のある特定の国にとっては敬遠される可能性があります。

砲弾市場の動向

予測期間中に最も高い成長を遂げると予測される120mm以上のセグメント

120mm以上の砲弾セグメントは、予測期間中に大幅な成長が見込まれています。この拡大の主な動向としては、複数の国による国防支出の増加、より高度な砲兵能力の追求、防衛機構の強化に向けた世界の動向などが挙げられます。さらに、弾薬開発における最先端技術の統合は、当面の間、砲兵システムの射程距離、殺傷力、精度の向上を約束します。

市場の主要企業は、先進的な砲弾の研究開発に多額の投資を行っており、120mm以上のセグメントに重点的に取り組んでいることを示しています。この動向を裏付けるように、スイスは2023年4月、砲兵能力を強化する意向を明らかにしました。ジェネラル・ダイナミクス・欧州・ランド・システムズのピラニアIV 8x8装甲車用に特別に調整された120mm迫撃砲システムの追加購入を発表したのです。このコミットメントをさらに強固なものにするため、スイス連邦軍需局はGDELS-Mowagと契約を結び、さらに16基のMorser 16 120mm迫撃砲システムを確保しました。

2024年7月、エルビット・システムズ社は、イスラエル国防省から精密誘導迫撃砲弾「アイアン・スティング」の2億2,000万米ドルの契約を獲得しました。120mm迫撃砲用に設計されたこの弾薬は、高度なGPSとレーザー誘導技術を利用し、最大10kmの高精度照準能力を実現します。アイアン・スティングは、点爆(PD)、点爆遅延(PDD)、近接センサー(PRX)機能を特徴とする洗練されたマルチモード・フューズ・システムを装備しています。この2年間のアップグレードは、イスラエル国防軍の地上戦闘の有効性と精度を強化することを目的としています。2023年2月、ウクライナの国営兵器会社は、中欧のNATO加盟国と砲弾の共同生産を発表し、他の兵器や軍事用ハードウェアの開発・生産で協力する意向を示しました。さらに、ロシアとウクライナの紛争で緊張が高まるなか、ウクロボロンプロムはウクライナで120ミリ迫撃砲弾の生産を開始しました。

このように、市場の様々な主要企業による先進的な120mm以上の砲弾の研究開発と生産の面での進歩は、120mm以上のセグメントが予測期間中に市場で大きな成長を示すことにつながります。

アジア太平洋が予測期間中に最も高い成長を遂げる

アジアでは、領土紛争や地政学的緊張を含む地域の安全保障上の脅威がエスカレートしています。これに対応するため、各国は防衛力強化への注力を強めており、砲弾需要の急増につながっています。中国、インド、韓国などの国々は、潜在的な脅威に対する抑止力として、先進的な砲兵システムに投資しています。強力な防衛態勢を維持するというこの緊急性が、大口径砲弾の取得を後押ししており、この地域の砲弾市場の成長を維持する動向となっています。

アジア太平洋の数多くの国々が軍隊の近代化を進めています。旧式の砲兵システムを段階的に廃止し、互換性のある弾薬を必要とする先進的なモデルに切り替えています。この近代化努力は、老朽化した装備に対処し、戦闘効果を高めるための最先端技術の統合を目指しています。各国が自走榴弾砲やロケット支援投射砲のような高度な砲兵ソリューションに軸足を移すにつれ、特殊な弾薬の需要が高まり、市場の拡大に拍車がかかります。

アジア太平洋における多国間の防衛演習や同盟関係は、協力的な軍事訓練環境を培っています。こうした合同演習では、戦術目標を達成する上で砲兵が極めて重要な役割を果たすことにスポットが当てられることが多く、砲兵弾薬の需要が高まっています。そのため市場参入企業は、砲兵弾薬の備蓄を強化し、訓練と作戦の両方の需要に十分備えられるようにすることに意欲を燃やしており、市場の成長をさらに後押ししています。

アジア太平洋では、国防予算が大幅に増強され、砲兵弾薬市場の主要な触媒として機能しています。各国政府は、国家安全保障戦略の一環として、これらの資金を砲兵弾薬を含む防衛装備品の取得に充てています。このような財政的コミットメントは、弾薬の直接購入を促進するだけでなく、この地域の活気ある防衛産業基盤を育成し、国内生産を促進します。

2023年1月、エチオピア政府は中国から32基のSH-15(PCL-181)自走榴弾砲を購入しました。PCL-181は、中国の人民解放軍(PLA)陸上部隊が使用するトラック搭載型の155mm自走榴弾砲です。この榴弾砲は、C-295、C-130、Y-9を含むほとんどの中型輸送機で空輸できるほど軽量であるため、エチオピアの即応部隊にとってより柔軟な選択肢となっています。自走榴弾砲は、すべての標準的な155mm NATO弾薬と中国北方工業公司(NORINCO)が開発した固有の弾薬と互換性があります。

砲兵弾薬産業の概要

砲兵弾薬市場は半固有構造を示し、いくつかの企業が顕著な市場シェアを占めています。主な企業は、General Dynamics Corporation、Rheinmetall AG、BAE Systems plc、THALES、Saab ABなどです。

市場開拓のリーダーは、世界の防衛要員のために最先端の砲弾システムを開発することを優先しています。これらの先進システムの研究開発への投資が増加していることは、今後の有望な機会を示唆しています。さらに、メーカー各社は射程距離の延長された大砲砲プラットフォームなどの技術を採用しており、予測期間中の市場の成長見通しを強化しています。

2023年8月、ラインメタル(Rheinmetall AG)は、現代の防護技術に対抗するために調整された次世代120mmKE弾薬を発表しました。2023年9月、ジェネラル・ダイナミクス・オードナンス・アンド・タクティカル・システムズは、米国陸軍から155mm M1128砲弾の生産増強のために2億1,800万米ドルの契約を獲得しました。この契約は、総額9億7,400万米ドルに及ぶ、より大規模な複数年契約の一部であり、砲兵能力の強化に重点を置いていることを強調しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 口径

- 120mm未満

- 120mm以上

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- その他のラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- イスラエル

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- General Dynamics Corporation

- Rheinmetall AG

- BAE Systems plc

- Saab AB

- Nammo AS

- MESKO S.A.

- THALES

- The Indian Ordnance Factories

- Singapore Technologies Engineering Ltd.

- MSM Group

- Elbit Systems Ltd.

- KNDS N.V.

第7章 市場機会と今後の動向

目次

The Artillery Ammunition Market size is estimated at USD 4.65 billion in 2025, and is expected to reach USD 5.92 billion by 2030, at a CAGR of 4.95% during the forecast period (2025-2030).

Artillery ammunition represents a significant advancement in military technology, allowing for precise target engagement and a marked reduction in collateral damage. As warfare evolves, the emphasis on precision and the need to minimize civilian harm have become paramount, driving the demand for this advanced ammunition.

The global market landscape is dynamic and influenced by several key trends. One notable trend is the heightened emphasis on integrating advanced targeting systems and enhancing network-centric warfare capabilities. In addition, the industry's growth is driven by a surging demand for munitions tailored for asymmetric warfare environments, marking a shift away from traditional large-scale military operations.

The increase in the military spending of various countries supports the various military initiatives to update military weapons and ammunition, which is expected to generate demand for artillery ammunition. The development of new and advanced artillery ammunition by the ammunition manufacturing companies with extended range, increased lethality, and integrated sensors to increase accuracy is anticipated to attract the armies of various countries for their future procurement, thereby leading the market to witness significant growth during the forecast period.

Regulatory challenges constrain market growth, especially concerning international arms treaties and export controls. The complexities of developing and transferring advanced military technologies frequently lead to elevated costs and extended development timelines. Additionally, in contrast to traditional unguided artillery, the steep price of precision-guided munitions may dissuade certain nations, especially those with a constrained defense budget.

Artillery Ammunition Market Trends

120mm & Above Segment Anticipated to Witness Highest Growth During the Forecast Period

The segment for artillery ammunition of 120mm and above is poised for substantial growth during the forecast period. Key drivers of this expansion include heightened defense spending by multiple nations, a push for more advanced artillery capabilities, and a global trend toward bolstering defense mechanisms. Furthermore, the integration of cutting-edge technology in ammunition development promises to enhance artillery systems' range, lethality, and precision in the foreseeable future.

Major players in the market are heavily investing in R&D for advanced artillery ammunition, signaling a robust focus on the 120 mm and above segment. As a testament to this trend, in April 2023, Switzerland unveiled its intent to bolster its artillery capabilities. They announced the acquisition of an additional batch of 120mm mortar systems, specifically tailored for the General Dynamics European Land Systems Piranha IV 8x8 armored vehicle. Further solidifying this commitment, the Swiss Federal Office for Armaments inked a deal with GDELS-Mowag, securing 16 more Morser 16 120mm mortar systems units.

In July 2024, Elbit Systems Ltd. secured a USD 220 million contract from the Israel Ministry of Defense for its "Iron Sting" precision-guided mortar munitions. Designed for 120mm mortars, these munitions utilize advanced GPS and laser guidance technologies, achieving high-precision targeting capabilities up to 10 kilometers. The Iron Sting is equipped with a sophisticated multi-mode fuze system, featuring Point Detonation (PD), Point Detonation Delay (PDD), and Proximity Sensor (PRX) functionalities. This two-year upgrade aims to bolster the ground combat effectiveness and accuracy of the Israeli Defense Forces. In February 2023, Ukraine's state arms company announced a joint production of artillery shells with a NATO member from Central Europe, signaling intentions to collaborate on developing and producing other arms and military hardware. Additionally, as tensions escalated in the Russia-Ukraine conflict, Ukroboronprom commenced production of 120-mm mortar rounds in Ukraine.

Thus, the advancements in terms of research and development and production of advanced 120mm and above artillery ammunition by various key players in the market will lead to the 120mm and above segment witnessing significant growth in the market during the forecast period.

Asia-Pacific to Witness Highest Growth During the Forecast Period

Regional security threats, including territorial disputes and geopolitical tensions, are escalating in Asia. In response, nations are intensifying their focus on bolstering defense capabilities, leading to a surge in demand for artillery ammunition. Countries like China, India, and South Korea are channeling investments into advanced artillery systems, viewing them as deterrents against potential threats. This urgency to uphold a formidable defense posture is driving the acquisition of high-caliber artillery munitions, a trend poised to sustain the region's artillery ammunition market growth.

Numerous nations in the Asia Pacific are modernizing their military forces. They're phasing out older artillery systems in favor of advanced models, which demand compatible ammunition. This modernization effort addresses aging equipment and aims to integrate cutting-edge technology for enhanced combat effectiveness. As nations pivot towards sophisticated artillery solutions-like self-propelled howitzers and rocket-assisted projectiles-the demand for specialized ammunition rises, fueling market expansion.

Multinational defense exercises and alliances in the Asia Pacific cultivate a collaborative military training environment. These joint exercises often spotlight artillery's pivotal role in achieving tactical goals, amplifying the demand for artillery ammunition. Participating nations are thus motivated to bolster their artillery ammunition reserves, ensuring they're well-equipped for both training and operational demands, further propelling market growth.

Across the Asia Pacific, defense budgets are witnessing significant boosts, acting as a primary catalyst for the artillery ammunition market. Governments are channeling these funds into defense equipment acquisitions, artillery ammunition included, as part of their national security strategies. This financial commitment not only facilitates direct ammunition purchases but also champions domestic production, nurturing a vibrant defense industrial base in the region.

In January 2023, the Ethiopia government purchased 32 SH-15 (PCL-181) self-propelled howitzers from China. The PCL-181 is a truck-mounted, 155mm self-propelled howitzer used by China's People's Liberation Army (PLA) Ground Force. These howitzers are light enough to be airlifted by most medium transport aircraft, including C-295, C-130, and Y-9, making it a more flexible option for Ethiopia's rapid reaction units. PCL-181) self-propelled howitzers are compatible with all standard 155mm NATO ammunition and indigenous ammunition developed by China North Industries Corporation (NORINCO).

Artillery Ammunition Industry Overview

The artillery ammunition market exhibits a semi-consolidated structure, with several players commanding notable market shares. Key players include General Dynamics Corporation, Rheinmetall AG, BAE Systems plc, THALES, and Saab AB.

Market leaders prioritize developing cutting-edge artillery ammunition systems for global defense personnel. Increased investments in R&D for these advanced systems signal promising opportunities ahead. Furthermore, manufacturers are adopting technologies such as extended-range cannon artillery platforms, bolstering the market's growth prospects during the forecast period.

In August 2023, Rheinmetall AG unveiled a next-gen 120mm KE ammunition tailored to counter modern protection technologies. In September 2023, General Dynamics Ordnance and Tactical Systems clinched a USD 218 million contract from the US Army to boost production of the 155 mm M1128 artillery shells. This contract is a segment of a larger multiyear agreement, totaling USD 974 million, underscoring the focus on enhancing artillery capabilities.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Caliber

- 5.1.1 Below 120mm

- 5.1.2 120mm & Above

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 France

- 5.2.2.3 Germany

- 5.2.2.4 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Mexico

- 5.2.4.3 Rest of Latin America

- 5.2.5 Middle East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 South Africa

- 5.2.5.4 Israel

- 5.2.5.5 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 General Dynamics Corporation

- 6.2.2 Rheinmetall AG

- 6.2.3 BAE Systems plc

- 6.2.4 Saab AB

- 6.2.5 Nammo AS

- 6.2.6 MESKO S.A.

- 6.2.7 THALES

- 6.2.8 The Indian Ordnance Factories

- 6.2.9 Singapore Technologies Engineering Ltd.

- 6.2.10 MSM Group

- 6.2.11 Elbit Systems Ltd.

- 6.2.12 KNDS N.V.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日