|

市場調査レポート

商品コード

1441695

空挺用ISR:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Airborne ISR - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 空挺用ISR:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

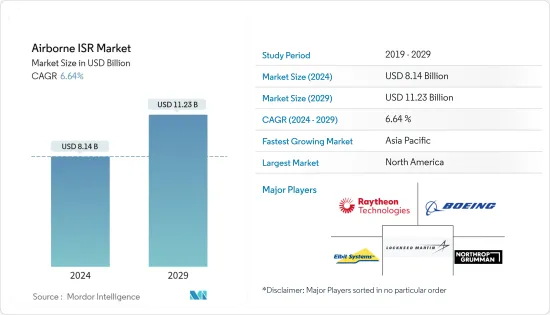

空挺用ISR市場規模は2024年に81億4,000万米ドルと推定され、2029年までに112億3,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に6.64%のCAGRで成長します。

COVID-19のパンデミックとそれに伴うロックダウンにより、いくつかの国のGDPが突然落ち込みました。また、パンデミックにより各国の医療制度に対して巨額かつ衝動的な支出が必要となり、経済資源の不足につながりました。 2020年に世界の軍事支出は増加しましたが、この要因により各国は将来の軍事予算に対して保守的なアプローチを取ることを余儀なくされ、それによって予測期間中の空挺用ISR市場が妨げられると予想されます。パンデミックにより、主要なISRプログラムのサプライチェーンに深刻な混乱が生じ、生産量が減少しました。空挺用ISR業界におけるいくつかの開発プロジェクトの遅延も観察されています。これらの要因は、関連市場のプレーヤーに悪影響を及ぼしています。

ISRの使用量が増加し、国境を守るためにISR技術を採用する国が増えているため、空挺用ISR市場は成長すると予想されています。急速な技術開発により、防衛産業では破壊的な技術が生み出されています。監視用の小型無人システムの使用が増加することで、ISRミッションで使用される電子部品の需要がさらに高まることが予想されます。データの正確性と管理を提供するためのマルチレベル比較分析との高度なデータ統合は、空挺用ISR市場に新たな市場機会を提供する可能性があります。

空挺用ISR市場動向

無人セグメントは予測期間中に最高の成長を遂げる

UAVは、ISRミッションの真のツールとして登場しており、ISRやその他のミッション用に航空資産の調達を計画している国々に低コストの代替手段を提供するため、世界的に需要が高まっています。新しいテクノロジーとプラットフォームの出現により、米国、ロシア、中国などの国の戦争戦略は変化しました。 UAVは視覚的に優れており、特定の場所で先制攻撃や監視を実行できるため、現在の戦争シナリオで広く使用されています。各国が非対称戦争を好む傾向にあるため、重要な意思決定ツールとして機能する重要な情報を収集するために無人航空機が大量に配備されることが予想されます。したがって、いくつかの国と防衛請負業者は、航空機のISR能力を強化するために研究開発投資を大幅に増加させています。たとえば、2021年 11月、UAE政府所有のEDGEグループは、最新の垂直離着陸機QX-5およびQX-6を含む、現地開発の先進的無人航空機(UAV)の製品ポートフォリオに一連の新たな製品を投入しました。(VTOL)ドローンは、諜報、監視、偵察(ISR)用途、国境警備、その他の軍事作戦用に構築されています。したがって、電子戦の採用の増加により、UAVに搭載された優れたISR機器の需要が高まり、空挺用ISR市場の無人セグメントの成長が促進されると予想されます。

2021年は北米が市場を独占

2021年、地域には北米が最大の市場シェアを占めました。米国は、防衛力の近代化に関与する主要な投資家の1つです。米国政府と米国国防総省は、競争の激しい環境に侵入してデータを収集できる新たなISR能力に資金を提供するためのリソースを提供するために、いくつかの航空プラットフォームの売却を開始することを計画しています。空軍は、統合軍司令官に有利な決定を下すために必要な知識を分析、情報提供するためにISRミッションを実施しています。 2021年4月、米国の要件監視評議会は、将来の攻撃偵察機の要件を、航空機の製造を競合する2社が開発した設計を検証する短縮能力開発文書(A-CDD)の形で承認しました。ロッキード・マーティン社のシコルスキー社とベル社は、試作機を製造し、2022年11月から飛行させるための直接競合に参加しています。陸軍はまた、受賞後、ARES(空挺偵察電子戦システム)と呼ばれる2番目の技術実証機を稼働させる準備を進めています。 近年、米国ではマルチミッションの海上哨戒機に対する大きな関心が高まっており、米国は海上監視能力を高めるために海上哨戒機の発注を増やしています。このような発展は、予測期間中にこの地域の市場の成長を促進すると予想されます。

空挺用ISR業界の概要

空挺ISR市場は非常に細分化されており、複数のプレーヤーがさまざまな軍隊向けにISRプラットフォームとサブシステムを開発しています。 Northrop Grumman Corporation、Boeing、Elbit Systems Ltd、Lockheed Martin Corporation、Raytheon Technologies Corporationは、市場の著名なプレーヤーの一部です。ただし、いくつかの地元企業は、地域のプロジェクトで市場の既存企業と協力して、地域のエンドユーザー防衛力の特定の要件に効果的に応える小規模なサブシステムを設計および統合しています。ベンダーは、自社の製造能力、世界の拠点ネットワーク、提供する製品、研究開発投資、強力な顧客ベースに基づいて競争しています。ベンダーは、熾烈な競争市場環境で生き残り、成功するために、航空機搭載ISRインテグレーターに最先端のシステムを提供する必要があります。防衛 OEMの多くは、自社の空挺用ISRプラットフォームにサードパーティのEO/IR機器を統合しており、さまざまなプラットフォーム上のそのようなシステムの相互統合にかかる研究開発コストを最小限に抑えようとしています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

- USDの通貨換算レート

第2章 調査手法

第3章 エグゼクティブサマリー

- 市場規模と予測、世界、2018~2031年 の市場シェア、2021年

- 用途別の市場シェア、2021年

- 地域別市場シェア、2021年

- 市場の構造と主要参入企業

- 空挺用ISR市場に関する専門家の意見

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション(金額別の市場規模と予測、2018~2031年)

- タイプ

- 有人

- 無人

- 用途

- 海上パトロール

- 空挺地上監視(AGS)

- 空中早期警報(AEW)

- シグナルインテリジェンス(SIGNIT)

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- Lockheed Martin Corporation

- L3Harris Technologies Inc.

- BAE Systems PLC

- Raytheon Technologies Corporation

- Northrop Grumman Corporation

- The Boeing Company

- Saab AB

- Airbus SE

- General Dynamics Corporation

- Elbit Systems Ltd

- Teledyne FLIR LLC

- Textron Inc.

- Leonardo SpA

- Safran SA

- Israel Aerospace Industries(IAI)

- その他の企業

- AeroVironment Inc.

- General Atomics

- BlueBird Aero Systems

- Aeronautics Group

第7章 市場機会と将来の動向

The Airborne ISR Market size is estimated at USD 8.14 billion in 2024, and is expected to reach USD 11.23 billion by 2029, growing at a CAGR of 6.64% during the forecast period (2024-2029).

The COVID-19 pandemic and the resultant lockdowns resulted in a sudden dent in the GDPs of several countries. Also, the pandemic demanded huge and impulsive spending toward the healthcare systems in countries, leading to a scarcity of economic resources. Although the global military spending increased in 2020, this factor is expected to force countries to take a conservative approach toward their future military budgets, thereby hampering the airborne ISR market during the forecast period. The pandemic has resulted in severe disruptions in the supply chains of major ISR programs and has reduced production output. Delays in several developments projects in the airborne ISR industry have also been observed. These factors have negatively impacted players in the related market.

The airborne ISR market is expected to grow as ISR usage is increasing and more countries are adopting ISR technology for securing their borders. Rapid technological developments are breeding disruptive technologies in the defense industry. The increasing use of small unmanned systems for surveillance is further expected to generate demand for electronic components used in ISR missions. Advanced data integration with a multi-level comparative analysis to provide data accuracy and management may provide new market opportunities for the airborne ISR market.

Airborne ISR Market Trends

Unmanned Segment to Experience Highest Growth During the Forecast Period

UAVs have emerged as veritable tools for ISR missions and are, hence, in high demand globally as they provide low-cost alternatives to nations planning to procure aerial assets for ISR and other missions. The emergence of new technologies and platforms has transformed the warfare strategies of nations such as the US, Russia, and China. UAVs are being used extensively in current warfare scenarios due to their visual superiority and capability of performing pre-emptive strikes and surveillance on specific locations. With nations showing a preference for asymmetric warfare, it is expected that UAVs would be deployed in large numbers to collect crucial information that can act as a key decision-making tool. Hence, several nations and defense contractors are significantly increasing R&D investments to enhance their airborne ISR capabilities. For instance, in November 2021, UAE's government-owned EDGE Group launched a series of new additions to its product portfolio of locally developed advanced unmanned aerial vehicles (UAVs), including the QX-5 and QX-6 modern vertical take-off and landing (VTOL) drones that are built for intelligence, surveillance, and reconnaissance (ISR) applications, border security, and other military operations. Thus, the increasing adoption of electronic warfare is expected to drive the demand for superior ISR equipment aboard UAVs, thus, fueling the growth of the unmanned segment of the airborne ISR market.

North America Dominated the Market in 2021

North America held the largest market share by geography in 2021. The US is one of the leading investors involved in the modernization of its defense capabilities. The US government and US DoD are planning to begin divesting a few aerial platforms to provide resources to fund emerging ISR capabilities that can penetrate and collect data in the highly contested environment. The Air Force conducts ISR missions to analyze, inform, and provide joint force commanders with the knowledge needed to achieve advantageous decisions. In April 2021, the US Army's Requirements Oversight Council approved the requirements for its Future Attack Reconnaissance Aircraft in the form of an Abbreviated Capabilities Development Document (A-CDD) that validates the designs developed by the two companies competing to build the aircraft. Lockheed Martin's Sikorsky and Bell are in a head-to-head competition to build prototypes and fly them beginning in November 2022. The Army is also in the process of bringing online a second technology demonstrator called ARES or Airborne Reconnaissance and Electronic Warfare System after awarding a contract to L3Harris Technologies in November 2020. ARES is based on a Bombardier Global Express 6500 jet that will have a different signals intelligence package on it than Artemis. There has been significant interest in multi-mission maritime patrol aircraft in the US in recent years, which has led to the US placing more orders for maritime patrol aircraft in order to increase its maritime surveillance capabilities. Such developments are expected to drive market growth in the region during the forecast period.

Airborne ISR Industry Overview

The airborne ISR market is highly fragmented, with multiple players developing ISR platforms and subsystems for various armed forces. Northrop Grumman Corporation, Boeing, Elbit Systems Ltd, Lockheed Martin Corporation, and Raytheon Technologies Corporation are some of the prominent players in the market. However, several local players collaborate with the market incumbents on regional projects to design and integrate smaller subsystems that effectively serve the specific requirements of the regional end-user defense forces. Vendors are competing based on their in-house manufacturing capabilities, global footprint network, product offerings, R&D investments, and a strong client base. Vendors must provide state-of-the-art systems to airborne ISR integrators to survive and succeed in the intensely competitive market environment. A majority of the defense OEMs integrate third-party EO/IR equipment onboard their airborne ISR platforms and try to minimize R&D costs involved in the cross-integration of such systems onboard different platforms.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Currency Conversion Rates for USD

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

- 3.1 Market Size and Forecast, Global, 2018 - 2031

- 3.2 Market Share by Type, 2021

- 3.3 Market Share by Application, 2021

- 3.4 Market Share by Geography, 2021

- 3.5 Structure of the Market and Key Participants

- 3.6 Expert Opinion on Airborne ISR Market

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size and Forecast by Value - USD billion, 2018 - 2031)

- 5.1 Type

- 5.1.1 Manned

- 5.1.2 Unmanned

- 5.2 Application

- 5.2.1 Maritime Patrol

- 5.2.2 Airborne Ground Surveillance (AGS)

- 5.2.3 Airborne Early Warnings (AEW)

- 5.2.4 Signals Intelligence (SIGNIT)

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 US

- 5.3.1.1.1 By Type

- 5.3.1.2 Canada

- 5.3.1.2.1 By Type

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.1.1 By Type

- 5.3.2.2 France

- 5.3.2.2.1 By Type

- 5.3.2.3 Gemany

- 5.3.2.3.1 By Type

- 5.3.2.4 Russia

- 5.3.2.4.1 By Type

- 5.3.2.5 Rest of Europe

- 5.3.2.5.1 By Type

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.1.1 By Type

- 5.3.3.2 India

- 5.3.3.2.1 By Type

- 5.3.3.3 Japan

- 5.3.3.3.1 By Type

- 5.3.3.4 South Korea

- 5.3.3.4.1 By Type

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.3.5.1 By Type

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.1.1 By Type

- 5.3.4.2 Rest of Latin America

- 5.3.4.2.1 By Type

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.1.1 By Type

- 5.3.5.2 United Arab Emirates

- 5.3.5.2.1 By Type

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.5.3.1 By Type

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Lockheed Martin Corporation

- 6.2.2 L3Harris Technologies Inc.

- 6.2.3 BAE Systems PLC

- 6.2.4 Raytheon Technologies Corporation

- 6.2.5 Northrop Grumman Corporation

- 6.2.6 The Boeing Company

- 6.2.7 Saab AB

- 6.2.8 Airbus SE

- 6.2.9 General Dynamics Corporation

- 6.2.10 Elbit Systems Ltd

- 6.2.11 Teledyne FLIR LLC

- 6.2.12 Textron Inc.

- 6.2.13 Leonardo SpA

- 6.2.14 Safran SA

- 6.2.15 Israel Aerospace Industries (IAI)

- 6.3 Other Companies

- 6.3.1 AeroVironment Inc.

- 6.3.2 General Atomics

- 6.3.3 BlueBird Aero Systems

- 6.3.4 Aeronautics Group