航空宇宙、防衛テレメトリ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Aerospace And Defense Telemetry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1851230

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

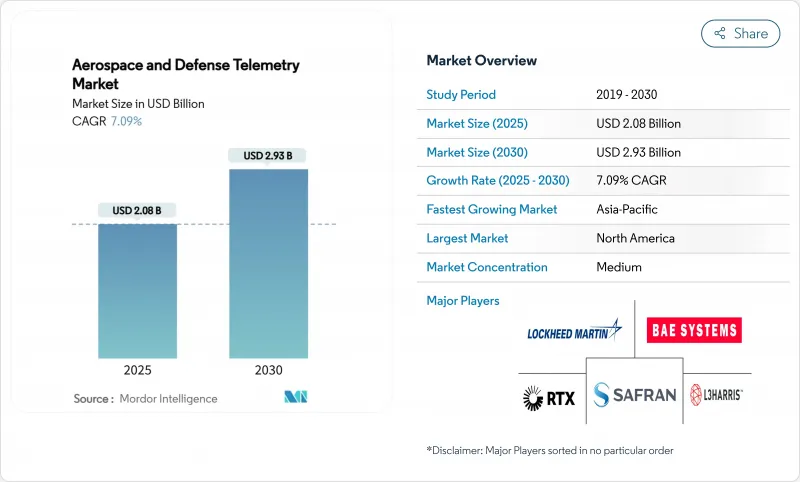

航空宇宙、防衛テレメトリ市場規模は2025年に20億8,000万米ドル、2030年には29億3,000万米ドルに達すると推定・予測され、市場推計・予測期間中のCAGRは7.09%です。

需要の伸びは、レガシーデータパイプから、ミッションデータをリアルタイムで処理し、送信前に非本質的なトラフィックを圧縮するエッジ対応の遠隔測定アーキテクチャへの移行を反映しています。極超音速兵器計画、急増する衛星コンステレーション、搭載される人工知能は、テレメトリ設計ルールを総体的に再形成します。同時に、NATOとインド太平洋の近代化計画は、空中ISR、海軍、ミサイルの各プラットフォームの帯域幅要件を高めています。無線周波数リンクは規模の優位性を維持しながらも、周波数帯域の混雑がミッションの継続性を脅かすような場所では、レーザーと光学システムが迅速な採用を確保しています。宇宙ベースのエッジAIの継続的な統合は、衛星が軌道上でデータをトリアージすることを可能にし、地上ステーションのバックログを削減し、意思決定速度を向上させる。BAEシステムズによるBall Aerospaceの55億米ドルの買収に代表される統合の動きは、既存企業が戦略的優位性を維持するために、いかに特殊な遠隔測定資産をボルト締めしているかを示しています。

世界の航空宇宙、防衛テレメトリ市場の動向と洞察

極超音速および再使用型ロケット計画の拡大

極超音速飛行では、データリンクにかつてない熱やプラズマによるストレスがかかるため、設計者はマッハ5以上の速度でロックを維持できる遠隔測定モジュールの開発を余儀なくされています。2024年のStratolaunchのTalon-A2試験飛行は、キロヘルツのリフレッシュレートでヘルスモニターデータを配信しながら、複数回の出撃に耐える耐衝撃アンテナの必要性を証明しました。アビオニクスは、校正のドリフトなしに繰り返されるヒートサイクルの負荷に耐える必要があるため、再利用性はエンジニアリングの課題をさらに複雑にしています。L3Harris社は、マルチバンド送信機を極超音速滑空機内に組み込み、リアルタイムの火器管制アルゴリズムに供給する軌道とシーカーの状態パケットをストリーミングしています。防衛省は、生存可能な飛行試験用計測器と生産グレードの兵器テレメトリに専用予算を割り当てているため、累積効果は航空宇宙、防衛テレメトリ市場を上昇させています。

広帯域テレメトリを必要とする小型衛星コンステレーションの急増

1万台以上のレーザー通信端末を配備したStarlinkは、ダウンリンクの前にトラフィックを横方向にシャトルする低軌道メッシュネットワークの基準アーキテクチャを設定しました。小規模な事業者がこのアプローチを模倣することで、何千ものノード間で帯域幅を動的にネゴシエートする光端末やソフトウェア定義無線の需要が持続的に高まっています。航空宇宙、防衛テレメトリ市場が恩恵を受けるのは、軍事計画者が、敵が地上のゲートウェイを妨害したときに弾力性のあるコマンド・アンド・コントロールを行うための衛星間リンクを重視しているためです。ダイナミックな波形の俊敏性により、コンスタレーション・マネージャーは、ハウスキーピング・トラフィックを圧縮し、リソースの利用率を高め、マージンを保護しながら、緊急のセンサー・データに向けて帯域幅を調整することができます。

帯域幅アクセスに影響するスペクトルの混雑と国際調整の遅れ

ITUの国際周波数マスター登録は、Ku帯、Ka帯、V帯の割り当てに重なる何千ものコンステレーションを申請するオペレータがいるため、バックログが増加しています。保護された帯域を求める国防プラットフォームは、クリアランスまで数カ月待たなければならず、プログラムのスケジュールに支障をきたしています。米国のような国家管轄区域では、FCCオークションがレガシーCバンドを5G用に再利用し、遠隔測定ユーザーをより狭いスライスに押し込めています。国境を越えた連合演習では、周波数の競合により直前になって再計画を余儀なくされ、訓練の価値が低下します。適応型周波数共有無線は有望だが、規制当局はリアルタイムの調整ルールを完全に成文化しておらず、航空宇宙、防衛テレメトリ市場の不確実性を長引かせています。

セグメント分析

レーザー/光リンクが最も拡大し、2025~2030年のCAGRは9.23%。宇宙開発事業団が光通信端末規格v4.0.0を発表し、プライムに明確なコンプライアンス・ロードマップを与えた後、採用が急増しました。マイクロ波システムと比較して、光ビームは10倍から100倍の帯域幅を提供し、傍受のリスクを抑制する空間的な閉じ込めがより厳しくなります。アダプティブ・ビーム・ステアリング・ミラーと組み合わせることで、衛星はマイクロ秒単位で仲間を切り替えられるようになり、地上中継がボトルネックにならないメッシュ・ルーティングがサポートされるようになりました。

無線周波数アーキテクチャは2024年に52.90%の売上を維持し、軍がコマンド・クリティカルなタスクのために信頼する深いインストールベースと全天候型の堅牢性を強調しています。スペクトルの圧力となりつつあるスプーフィング対策への要求が、インテグレーターを2つのモダリティの融合に向かわせ、Kaバンドと光キャリアの間をホップできるハイブリッド端末を発表させる。このような二元性は、高周波の調達を維持すると同時に、航空宇宙、防衛テレメトリ市場に新たな収益をもたらします。Starlinkの展開により、光端末コンポーネントの需要が2桁増となり、レーザー機器サプライヤーのバックログが持続的に増加します。

ソフトウェアとデータ分析プラットフォームは、2025-2030年のCAGRが最速の8.56%です。統合ダッシュボードは現在、遠隔測定、ロジスティクス、環境フィードを融合し、飛行終了の数分後にメンテナンス勧告を生成します。例えば、ボーイングのコンディションベース・スマート・メンテナンス・スイートは、エンジンの振動スペクトルと飛行体制タグをブレンドし、疲労しきい値に近づいている部品にフラグを立てる。

超音速機、超小型衛星、UAVなど、どのノードにも物理的な変換器と電力増幅器チェーンが必要なため、トランスミッタとセンサは2024年に26.54%と最大のスライスを維持した。継続的な小型化により、これらの素子はチップ・スケールのパッケージに圧縮され、エッジ・プロセッサ用のスペースが確保されます。コンポーネントの歩留まり向上とASICマスク・コストの低下により参入障壁が低下し、新規サプライヤが航空宇宙、防衛テレメトリ市場に参入して価格競争に拍車がかかり、大量採用が加速します。

地域分析

米国国防総省が極超音速滑空機や次世代ISRプラットフォームの契約を締結し、国内ラインが多忙を極めているため、北米が2024年に36.14%の最大シェアを維持した。プライム・コントラクターはテレメトリーの研究開発をフルシステム入札にバンドルすることで、価値をオンショアに維持し、強固なエンジニアリング・パイプラインを維持しています。宇宙新興企業に対するベンチャーキャピタルの旺盛な投資意欲は、この地域のリーダーシップをさらに強固なものにしています。

アジア太平洋地域は2030年までのCAGRが9.01%と最も急速に上昇します。中国は、プラグアンドプレイの光ターミナルを搭載した小型衛星バスの工場生産量を拡大し、インドは、再使用型打上げの野心によって、熱サイクル試験用の一貫したテレメトリ・コンポーネントの需要が高まる。日本は、ロボット工学の専門知識を小型化された月探査機や小惑星探査機のトランシーバーに注ぎ込み、地域のサプライヤーを超小型ハードウェアの世界的な価格設定者に変貌させる。

欧州は、SESAR 3.0の下で自律的かつ持続可能な航空交通の目標を追求し、地域のインテグレーターに、乗員・非乗員の機体内にサイバー耐性のあるソフトウェア定義無線を採用するよう促しています。2025年後半に施行が予定されているEU宇宙法では、EUの軌道スロットで運用されるテレメトリ暗号化アルゴリズムのコンプライアンス・ログが義務付けられます。この新しいルールブックは、調達に若干の遅れをもたらす可能性があるが、最終的には規格の調和を図り、航空宇宙、防衛テレメトリ市場における認定ベンダーの対応可能な需要を拡大します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 極超音速ロケットと再使用ロケット計画の拡大

- 広帯域テレメトリを必要とする小型衛星コンステレーションの急増

- 防衛アライアンス全体における空中ISRプラットフォームの近代化

- リアルタイムデータ処理のための宇宙ベースのエッジAIの出現

- 防衛遠隔測定における商用ソフトウェア定義無線の採用増加

- 状態ベースのメンテナンスのためのパッシブ・テレメトリーの利用拡大

- 市場抑制要因

- 周波数帯域の輻輳と国際調整の遅れが帯域幅アクセスに影響

- 小型UAVプラットフォームのサイズ、重量、電力(SWaP)の制限がテレメトリー統合を制約する

- 国境を越えた技術移転を制限する輸出規制とサイバー主権条項

- テレメトリーシステムの予算を制限する衛星打ち上げ保険料の上昇

- バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- コミュニケーションテクノロジー別

- 無線周波数

- 衛星

- レーザー/光学

- イーサネット/光ファイバー

- コンポーネント別

- トランスミッタおよびセンサ

- アンテナおよび変調器

- ソフトウェアとデータ分析プラットフォーム

- 信号処理ユニット

- 地上受信設備

- プラットフォーム別

- 航空機

- 宇宙船とロケット

- 無人航空機(UAV)

- ミサイルおよび発射体

- 船舶

- 地上ステーション

- エンドユーザー別

- 航空宇宙

- 防衛

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他のアジア太平洋地域

- 南米

- ブラジル

- その他南米

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- その他中東

- アフリカ

- 南アフリカ

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- BAE Systems plc

- Lockheed Martin Corporation

- L3Harris Technologies, Inc.

- Safran SA

- Honeywell International Inc.

- Thales Group

- RTX Corporation

- Kongsberg Gruppen ASA

- Curtiss-Wright Corporation

- Leonardo S.p.A

- AstroNova Inc.

- Orbit Communications Systems Ltd.

- Kratos Defense & Security Solutions, Inc.

- Teledyne Technologies Incorporated

- Viasat Inc.

- General Dynamics Mission Systems(General Dynamics Corporation)

- Rohde & Schwarz GmbH & Co KG

- Sierra Nevada Company, LLC.

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日