|

市場調査レポート

商品コード

1640426

化学注入定量ポンプとバルブ:市場シェア分析、産業動向、成長予測(2025~2030年)Chemical Injection Metering Pumps And Valves - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 化学注入定量ポンプとバルブ:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

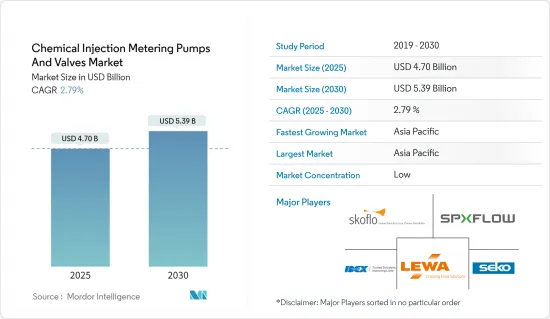

化学注入定量ポンプとバルブの市場規模は2025年に47億米ドルと推定・予測され、予測期間(2025~2030年)のCAGRは2.79%で、2030年には53億9,000万米ドルに達すると予測されます。

COVID-19の発生により、2020年には世界中で全国的な封鎖、製造活動やサプライチェーンの混乱、生産停止が発生し、市場にマイナスの影響を与えました。しかし、2021年には状況が回復し始め、市場の成長軌道が回復しました。

主要ハイライト

- 市場調査の主要促進要因の1つは、廃水処理用途への需要の加速です。

- しかし、一部の用途ではメンテナンスや交換コストが高く、市場成長の妨げになると予想されます。

- エネルギー、電力、化学産業が市場を独占しており、予測期間中も成長が見込まれています。上水・廃水処理産業は、今後数年間で最も高いCAGRで推移すると予想されます。

- アジア太平洋が市場を独占し、北米、欧州がそれに続き、中国、日本、インドなどの国による消費が最も多いです。

- 製薬産業からの需要の高まりが、今後の機会となりそうです。

化学注入定量ポンプ&バルブ市場動向

エネルギー、電力、化学が市場を独占

- エネルギー、電力、化学は、注入定量ポンプとバルブ市場における主要なエンドユーザーセグメントです。紙パルプ産業もこのセグメントに含まれます。

- 化学産業は、最終製品または中間製品の合成で構成されています。定量ポンプとバルブは、異なる温度や化学処理圧力で様々な有毒化学品を処理するのに役立ちます。

- 化学注入システムは、発電にも使用されています。硫酸第二鉄や硫酸などの化学品は、水をボイラー用の超純水に変えるために正確な測定が必要です。

- フランスでは、米国と中東諸国からの輸入が石油製品の需要の大半を満たしています。フランスでは、エネルギーの約60%が化石資源として利用されています。エネルギー源は主に石油製品、天然ガス、石炭です。したがって、エネルギー生成は、原油はサウジアラビア、ロシア、カザフスタン、アルジェリア、ナイジェリアからの輸入に、ガスはロシア、ノルウェー、ナイジェリア、オランダからの輸入に依存しています。

- フランスで消費される石油の95%以上は他国から輸入されています。石油の大部分はロシアから輸入され、フランスの需要を満たしています。しかし、ロシアとウクライナの戦争が始まって以来、EUは欧州市場からロシアの石油を追い出す方法を模索しています。フランスはEU最大の石油輸入国のひとつであるため、フランス政府はすでにアラブ首長国連邦との間で、ロシア産石油の購入を代替するための協議を強化しています。

- ほとんどの石油化学施設では、発電熱を利用してボイラーを稼働させ、現場の電力需要を満たしています。

- 米国国勢調査局によると、鉱業・採石業の収益は、2021年の136億8,000万米ドルに対し、2022年には143億9,000万米ドルに達しました。このセクターからの収益は、2023年には152億5,000万米ドルに達すると予測されています。

- 鉱業と冶金はカナダの主要産業です。カナダは60以上の金属と鉱物を世界各国に供給しています。鉱業は技術革新と新技術に投資し、このセクターを急速に再構築しています。鉱業はまた、統合を示し、今後数年間の同産業の成長展望に関する憶測を呼びました。

- 火力発電所や原子力発電所などの電力産業では、ボイラーシステムに給水するために化学品が必要になることが多いです。

- 投資の増加に伴うエネルギー、電力、化学セグメントの成長は、予測期間中に調査された市場の需要を促進すると考えられます。

アジア太平洋では中国が市場を独占

- アジア太平洋は、化学注入定量ポンプとバルブの需要を支配すると予想されます。中国だけでアジア太平洋の市場の約35%を占めています。

- 定量ポンプとバルブの消費は石油・ガスで高く、同国では下流生産が増加しており、石油化学製品の生産能力も増加しています。

- 中国で顕著な他のエンドユーザー産業は、化学工場であり、市場の多くの大企業は、中国での化学工場を持っており、彼らはさらに、化学注入定量ポンプとバルブの消費を増加させる生産能力を増加しています。他の主要な産業は、国内の水処理施設、さまざまな産業で使用されます。

- 廃水処理は主に石炭、鉄鋼、鉄鋼産業が日々の活動に真水を必要とするためです。中国北部には、国内の石炭関連産業の約90%があります。

- 中国政府は、この地域の貴重な水資源を改善するため、水の使用と排出に関する規制を制定しました。最近、政府は華北の石炭・化学工場に対する規制を強化し、ゼロ液体排出(ZLD)を義務付けています。

- 中国の飲食品産業は巨大で、国内経済において重要な役割を果たしています。購買力のある中産階級の人口が増加し、食品の安全性と品質への関心が高まっているため、飲食品産業は今後も成長を続けると予想されます。

- 石油・ガス上流産業では、メーカーは常に生産能力、プロセス全体の効率、機械のダウンタイムの改善を追求しています。石油・ガス会社は、生産量の増加、腐食の低減、石油・ガス・水の分離、あらゆる探査・回収活動の収益性向上のために、化学注入定量ポンプとバルブを使用しています。

- 中国は世界第2位の石油・ガス消費国ですが、生産国としては世界第6位に過ぎません。石油の大消費国である中国の石油消費量は、成長率を変動させながら年々増加しています。しかし、石油供給がまだ需要を満たしていないため、中国は主に輸入に頼っています。

- 予測期間における上記の様々なエンドユーザー産業の成長は、国内の化学注入定量ポンプとバルブの需要を押し上げると予想されます。

化学注入定量ポンプとバルブ産業概要

世界の化学注入定量ポンプとバルブ市場は非常にセグメント化されており、主要企業5社の市場シェアは非常に小さいです。主要企業は、Idex Corporation、SPX Flow、Lewa GmbH、SkoFlo Industries Inc.、Seco SpAなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 廃水処理用途からの需要の加速

- 環境規制のための強固な運用手順

- その他の促進要因

- 抑制要因

- 用途によってはメンテナンスと交換コストが高い

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- ポンプタイプ

- ダイヤフラム

- ピストン/プランジャー

- その他のポンプタイプ

- エンドユーザー産業

- エネルギー、電力、化学

- 石油・ガス

- 上下水道治療

- 飲食品

- 製薬

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- オーストラリアとニュージーランド

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- ロシア

- スペイン

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング/シェア(%)分析

- 主要企業の戦略

- 企業プロファイル

- Cameron(Schlumberger)

- Hunting PLC

- Idex Corporation

- ITC Dosing Pumps

- Lewa GmbH

- McFarland-Tritan LLC

- Milton Roy

- ProMinent

- Seepex GmbH

- Seko SpA

- SkoFlo Industries Inc.

- SPX FLOW Inc.

- Swelore Engineering Pvt Ltd.

第7章 市場機会と今後の動向

- 製薬産業における需要の高まり

- 技術的に先進的薬液注入システムの開発

The Chemical Injection Metering Pumps And Valves Market size is estimated at USD 4.70 billion in 2025, and is expected to reach USD 5.39 billion by 2030, at a CAGR of 2.79% during the forecast period (2025-2030).

Due to the COVID-19 outbreak, nationwide lockdowns worldwide, disruption in manufacturing activities and supply chains, and production halts negatively impacted the market in 2020. However, the conditions started recovering in 2021, restoring the market's growth trajectory.

Key Highlights

- One of the major factors driving the market study is the accelerating demand for wastewater treatment applications.

- However, high maintenance and replacement costs in some applications are expected to hinder the market's growth.

- The energy, power, and chemicals industry dominated the market and is expected to grow during the forecast period. The water and wastewater treatment industry is expected to register the highest CAGR in the coming years.

- Asia-Pacific dominated the market, followed by North America and Europe, with the largest consumption from countries such as China, Japan, and India.

- Growing demand from the pharmaceutical industry will likely act as an opportunity in the future.

Chemical Injection Metering Pumps & Valves Market Trends

Energy, Power, and Chemicals to Dominate the Market

- Energy, power, and chemicals are major end-user segments in the injection metering pumps and valves market. Even the pulp and paper industry is considered in this segment.

- The chemical industry consists of the synthesis of finished or intermediate products. Metering pumps and valves help handle various toxic chemicals at different temperatures and chemical processing pressures.

- Chemical injection systems also find major use in power generation. Chemicals, such as ferric sulfate and sulphuric acid, are needed in precise measurements to transform water into ultra-pure water for boilers.

- In France, imports from the United States and Middle Eastern countries meet most of the demand for petroleum products. Around 60% of the energy is utilized in the form of fossil resources in France. Energy is primarily derived from petroleum products, natural gas, and coal. Hence energy generation depends on imports from Saudi Arabia, Russia, Kazakhstan, Algeria, and Nigeria for crude oil while upon Russia, Norway, Nigeria, and the Netherlands for gas.

- Over 95% of the oil consumed in France is imported from other nations. A large share of oil is imported from Russia to fulfill the country's demand. However, since the onset of the Russia-Ukraine war, European Union has been finding ways to push out Russian oil from the European market. Since France is one of the largest oil importers in the European Union, the French government has already strengthened talks with United Arab Emirates (UAE) to replace Russian oil purchases.

- Most petrochemical facilities use generated heat to run boilers to meet site power requirements.

- As per the United States Census Bureau, revenue in mining and quarrying amounted to USD 14.39 billion in 2022, compared to USD 13.68 billion in 2021. The revenue from this sector is projected to amount to USD 15.25 billion in 2023.

- Mining and metallurgy are key industries in the country. Canada supplies over 60 metals and minerals to different countries worldwide. The mining industry invests in innovation and new technologies, rapidly reshaping the sector. The mining industry also witnessed consolidations, which led to speculations regarding the growth prospects for the industry in the coming years.

- Power industries, such as thermal and nuclear plants, often require chemicals to inject the feed water into the boiler system.

- The growth in the energy, power, and chemicals sectors with increasing investments is likely to drive the demand in the market studied during the forecast period.

China to Dominate the Market in Asia-Pacific Region

- Asia-Pacific region is expected to dominate the demand for chemical injection metering pumps and valves. China alone accounts for about 35% of the market in the Asia-Pacific region.

- The consumption of metering pumps and valves is high in oil and gas; the downstream production has increased in the country, which has also increased the production capacities of petrochemicals; therefore, it will augment the consumption of chemical injection metering pumps and valves in the country.

- The other end-user industry prominent in China is the chemical plants, many big companies in the market have their chemical plants in China, and they have even increased their production capacities, which will increase the consumption of chemical injection metering pumps and valves. The other major industry is a water treatment facility in the country, used in different industries.

- Wastewater treatment is mainly because the coal, steel, and iron industries require fresh water for daily activities. North China has approximately 90% of the country's coal-based industries.

- The Chinese government has enacted water use and discharge regulations to improve the region's precious water resources. Recently, the government has tightened the rules for coal and chemical plants in North China, which require zero-liquid discharge (ZLD).

- China's food and beverage industry is enormous and plays an important role in the country's economy. The food and beverages industry is expected to continue growing because of the increasing middle-class population with more purchase power and growing attention to food safety and quality.

- In the upstream Oil & Gas industry, manufacturers constantly seek to improve their production capacities, overall process efficiency, and machinery downtime. Oil and gas companies use chemical Injection metering pumps and valves to increase production, reduce corrosion, separate oil/gas/water, and improve the profitability of all exploration and recovery efforts.

- China is the world's second-largest consumer of oil and gas but only the sixth-largest producer of the same. As a big oil consumer, China's oil consumption is increasing yearly with fluctuating growth rates. However, China mainly relies on imports because the oil supply still cannot meet the demand.

- The growth in those mentioned above various end-user industries in the forecast period is expected to boost the demand for chemical injection metering pumps and valves in the country.

Chemical Injection Metering Pumps & Valves Industry Overview

The global chemical injection metering pumps and valves market is highly fragmented, with the top 5 players accounting for a very small market share. The major companies include Idex Corporation, SPX Flow, Lewa GmbH, SkoFlo Industries Inc., and Seko SpA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Accelerating Demand from Wastewater Treatment Applications

- 4.1.2 Robust Operational Procedures for Regulating Environmental Concerns

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Maintenance and Replacement Costs in Some Applications

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Pump Type

- 5.1.1 Diaphragm

- 5.1.2 Piston/Plunger

- 5.1.3 Other Pump Types

- 5.2 End-user Industry

- 5.2.1 Energy, Power, and Chemicals

- 5.2.2 Oil and Gas

- 5.2.3 Water and Wastewater Treatment

- 5.2.4 Food and Beverage

- 5.2.5 Pharmaceutical

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Australia and New Zealand

- 5.3.1.7 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Spain

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking/Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Cameron (Schlumberger)

- 6.4.2 Hunting PLC

- 6.4.3 Idex Corporation

- 6.4.4 ITC Dosing Pumps

- 6.4.5 Lewa GmbH

- 6.4.6 McFarland-Tritan LLC

- 6.4.7 Milton Roy

- 6.4.8 ProMinent

- 6.4.9 Seepex GmbH

- 6.4.10 Seko SpA

- 6.4.11 SkoFlo Industries Inc.

- 6.4.12 SPX FLOW Inc.

- 6.4.13 Swelore Engineering Pvt Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Demand in the Pharmaceutical Industry

- 7.2 Development of Technologically Advanced Chemical Injection Systems