|

|

市場調査レポート

商品コード

1640437

アクリル繊維:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Acrylic Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アクリル繊維:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

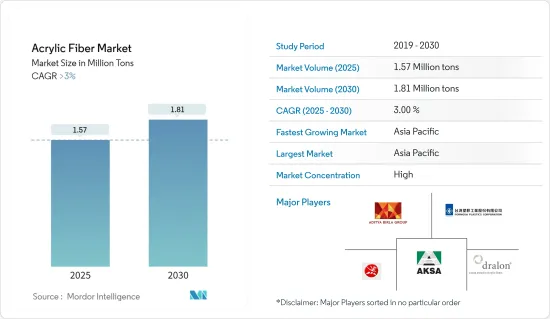

アクリル繊維市場規模は2025年に157万トンと推定され、2030年には181万トンに達すると予測され、予測期間(2025~2030年)のCAGRは3%を超えると予測されます。

2021年のCOVID-19の大流行により、企業、製品、製造施設が減速し、経済活動が低下したため、市場はマイナスの影響を受けました。しかし、予測期間中に市場は回復するとみられます。

主要ハイライト

- 市場の成長を促す主要要因としては、アパレル需要の高さや産業用途の増加が挙げられます。

- その反面、ポリエステルのような代替品が入手可能であることや、アクリル繊維の生産に関する世界的に厳しい規制が市場成長の妨げになると予想されます。

- しかし、アクリル紙の成長機会と将来の市場は、予測期間中に十分な成長機会を提供すると期待されています。

- アジア太平洋は、ASEAN諸国とインドからの高い需要により、アクリル繊維市場を独占しています。

アクリル繊維市場の動向

市場を独占するウールセグメント

- 衣料品へのウールの使用は古代にまでさかのぼります。ウールには、シワになりにくい、吸湿性がある、保温性があるなどの優れた特性があります。ウールの大きな特徴は、時間の経過とともに変形から回復する能力です。それゆえ、この繊維で作られた衣類は魅力的です。

- 100%ウール繊維で織られたり編まれたりした生地は、セーター、パーカー、ブーツ、ブーツの裏地、帽子、手袋、運動着、カーペット、毛布、ローラーブラシ、椅子張り、エリアラグ、防護服、かつら、ヘアエクステンションなどの衣料品を作る際の標準となっています。

- アクリル繊維の大部分はウールとアクリルの混紡に使われ、非常に人気があります。ウール55%とアクリル45%の混紡は丸編みのニット製品に使用されます。この混紡は特にスポーツウェアの製造に使用され、手入れのしやすさ、耐久性、外観の保持、色のスタイリング、口当たりの良さなどの特徴があります。

- 世界では要求に応じてさまざまなブレンドが使用されています。50/50と70/30のアクリルウール混紡は、安価で見栄えが良く、扱いやすい衣料品に人気があります。アクリルウール50/50混紡は耐久性と保形性に優れた軽量衣料に、アクリルウール70/30混紡はスラックスに使われます。

- 国際ウール繊維機構によると、ウール繊維の世界のトップバイヤーは依然として中国だが、米国ではウールの需要が増加しています。2022年11月までの1年間で、米国に持ち込まれたウール衣料品の量は2021年の同時期と比べて47%増加しました。

- したがって、ウールセグメントでのアクリル繊維の需要増が予測期間中に市場を独占すると予想されます。

中国がアジア太平洋市場を独占する

- 中国は世界最大のアクリル繊維生産国で、世界のアクリル繊維生産量の30%以上のシェアを占めています。ASEAN諸国、欧州、米国、日本を中心とする国内外市場からの需要により、中国の繊維産業は年々拡大しています。

- イラン、インド、ベトナム、パキスタン、アラブ首長国連邦は、中国がアクリル繊維を輸出する最大市場の一部です。また、日本、ドイツ、タイ、韓国、トルコなどの国からもアクリル繊維を輸入しています。

- 中国は世界最大の繊維生産・輸出国です。世界の繊維輸出総額のうち、金額ベースで約43%のシェアを占めています。そのため、中国の衣料産業の成長がアクリル繊維市場を押し上げると予想されています。

- 同国は繊維セグメントで著しい成長を遂げています。中国国家統計局によると、2023年、中国の主要繊維企業の総収益は前年比7.2%増加しました。2023年、中国の繊維製品・衣料品の輸出額は過去最高の2,936億米ドルに達しました。

- したがって、このような市場動向はすべて、予測期間中に中国のアクリル繊維市場の需要を高めると予想されます。

アクリル繊維産業のセグメンテーション

アクリル繊維市場はもともと統合されています。市場の主要企業には、Aksa Akrilik Kimya Sanayii AS、Dralon、Jilin Chemical Fiber Group、Aditya Birla Management Corporation Pvt.Ltd、Formosa Plastics Corporationなどがあります(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- アパレルへの高い需要

- 産業用途の増加

- その他の促進要因

- 抑制要因

- ポリエステルのような代替品の入手可能性

- アクリル繊維の生産に関する世界の厳しい規制

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模(数量ベース))

- 形態

- ステープル

- フィラメント

- 混紡

- ウール

- 綿

- その他の混紡(セルロース)

- 用途

- アパレル

- 家庭用家具

- 産業用

- その他の用途(椅子張り)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- ノルディック

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- アラブ首長国連邦

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)分析

- 主要企業の戦略

- 企業プロファイル

- Aditya Birla Management Corporation Pvt. Ltd

- Aksa Akrilik Kimya Sanayii AS

- China Petrochemical Corporation(Sinopec)

- Dralon

- Formosa Plastics Corporation

- Indian Acrylics Limited

- Japan Exlan Co., Ltd

- Jiangsu Zhongxin Resources Group

- Jilin Chemical Fiber Group Co. Ltd

- Kaltex

- Kaneka Corporation

- Mitsubishi Chemical Corporation

- Pasupati Acrylon

- PetroChina Company Limited

- Taekwang Industrial Co. Ltd

- Toray Industries Inc.

- Vardhman Acrylics Ltd

第7章 市場機会と今後の動向

- アクリル紙の将来市場

- その他の機会

The Acrylic Fiber Market size is estimated at 1.57 million tons in 2025, and is expected to reach 1.81 million tons by 2030, at a CAGR of greater than 3% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2021, as the pandemic resulted in the slowdown of businesses, products, and manufacturing facilities, resulting in less economic activity. However, the market is expected to recover during the forecast period.

Key Highlights

- The major factors driving the growth of the market studied include the high demand for apparel and increasing industrial applications.

- On the flip side, the availability of substitutes like polyester and stringent regulations worldwide on the production of acrylic fiber are expected to hinder the growth of the market.

- However, growing opportunities and the future market for acrylic paper are expected to offer ample growth opportunities during the forecast period.

- Asia-Pacific dominated the acrylic fiber market due to high demand from the ASEAN countries and India.

Acrylic Fiber Market Trends

The Wool Segment to Dominate the Market

- The use of wool for clothing dates back to ancient times. Wool has outstanding properties, such as resistance to wrinkles, moisture absorption, and warmth. A significant feature of wool is its ability to recover from deformation over time. Hence, clothing made from these fibers is attractive.

- Fabrics woven or knitted with 100% wool fiber have become a standard in making apparel, such as sweaters, hoodies, boots, boot lining, hats, gloves, athletic wear, carpeting, blankets, roller brushes, upholstery, area rugs, protective clothing, wigs, and hair extensions.

- A majority of acrylic fiber is used to make wool and acrylic blends, which are very popular. A blend of 55% wool and 45% acrylic fiber is used to make circular knit goods. This blend is particularly used in making sportswear, with characteristics like ease of care, durability, appearance retention, color styling, and palatability.

- Different blends are used worldwide depending on the requirements. The 50/50 and 70/30 acrylic wool blends are popular among those apparel that are inexpensive, look good, and are easy to handle. The 50/50 acrylic wool blend is used to make lightweight apparel that has excellent durability and shape retention, while the 70/30 acrylic wool blend is used to make slacks.

- According to the International Wool Textile Organization, China remains the top buyer of wool fiber globally, yet there is an increasing demand for wool in the United States. During the year that concluded in November 2022, the quantity of wool clothing brought into the United States increased by 47% compared to the same period in 2021.

- Hence, increasing demand for acrylic fiber in the wool segment is expected to dominate the market over the forecast period.

China to Dominate the Market in Asia-Pacific

- China is the largest producer of acrylic fibers in the world, accounting for a share of more than 30% of global acrylic fiber production. Owing to the demand from domestic and international markets, primarily from ASEAN countries, Europe, the United States, and Japan, the textile industry in China has expanded over the years.

- Iran, India, Vietnam, Pakistan, and the United Arab Emirates are some of the largest markets where China exports acrylic fibers. The country also imports acrylic fiber from countries like Japan, Germany, Thailand, South Korea, and Turkey.

- China is the largest textile-producing and exporting country in the world. It holds about 43% share of the world's total textile exports in terms of value. Thus, the growth in China's clothing industry is anticipated to boost the market for acrylic fibers.

- The country has witnessed significant growth in the textiles segment. According to the National Bureau of Statistics of China, in 2023, the combined earnings of China's leading textile companies increased by 7.2% compared to the previous year. In 2023, China's exports of textiles and clothing reached a record high of USD 293.6 billion.

- Hence, all such market trends are expected to add to the demand for the acrylic fibers market in China during the forecast period.

Acrylic Fiber Industry Segmentation

The acrylic fiber market is consolidated in nature. Some of the major players in the market include (not in any particular order) Aksa Akrilik Kimya Sanayii AS, Dralon, Jilin Chemical Fiber Group Co. Ltd, Aditya Birla Management Corporation Pvt. Ltd, and Formosa Plastics Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 High Demand for Use in Apparel

- 4.1.2 Increasing Industrial Application

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Availability of Substitutes, like Polyester

- 4.2.2 Stringent Regulations Worldwide on the Production of Acrylic Fiber

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Form

- 5.1.1 Staple

- 5.1.2 Filament

- 5.2 Blending

- 5.2.1 Wool

- 5.2.2 Cotton

- 5.2.3 Other Blendings (Cellulose)

- 5.3 Application

- 5.3.1 Apparel

- 5.3.2 Household Furnishing

- 5.3.3 Industrial

- 5.3.4 Other Applications (Upholstery)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Nigeria

- 5.4.5.4 Qatar

- 5.4.5.5 Egypt

- 5.4.5.6 United Arab Emirates

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aditya Birla Management Corporation Pvt. Ltd

- 6.4.2 Aksa Akrilik Kimya Sanayii AS

- 6.4.3 China Petrochemical Corporation (Sinopec)

- 6.4.4 Dralon

- 6.4.5 Formosa Plastics Corporation

- 6.4.6 Indian Acrylics Limited

- 6.4.7 Japan Exlan Co., Ltd

- 6.4.8 Jiangsu Zhongxin Resources Group

- 6.4.9 Jilin Chemical Fiber Group Co. Ltd

- 6.4.10 Kaltex

- 6.4.11 Kaneka Corporation

- 6.4.12 Mitsubishi Chemical Corporation

- 6.4.13 Pasupati Acrylon

- 6.4.14 PetroChina Company Limited

- 6.4.15 Taekwang Industrial Co. Ltd

- 6.4.16 Toray Industries Inc.

- 6.4.17 Vardhman Acrylics Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Future Market for Acrylic Paper

- 7.2 Other Opportunities