|

市場調査レポート

商品コード

1685672

水溶性ポリマー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Water-soluble Polymer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 水溶性ポリマー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

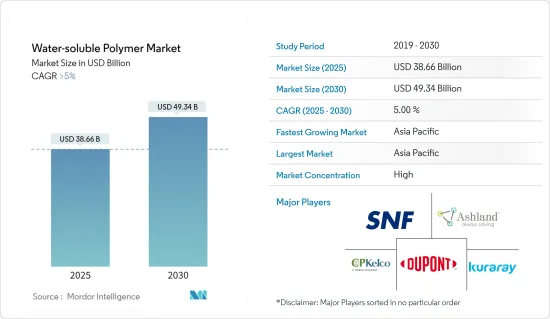

水溶性ポリマーの市場規模は2025年に386億6,000万米ドルと推定され、2030年には493億4,000万米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは5%を超えると予測されます。

COVID-19パンデミックは水溶性ポリマー市場にマイナスの影響を与えました。産業活動の低下、サプライチェーンの混乱、消費者行動の変化は、これらの産業における水溶性ポリマーの需要に影響を与えました。水処理、繊維、パーソナルケア、食品加工など、水溶性ポリマーを利用する多くの産業は、パンデミックの間、操業停止や一時的な操業停止に見舞われました。しかし、経済状況が改善し、プロジェクトが再開されると、上記の産業で使用されるポリマーの需要が増加しました。

市場の成長を後押しする要因は、北米におけるシェールガス産業の成長と、世界の水処理産業からの水溶性ポリマーの需要の高まりです。

しかし、原料価格の変動が予測期間中の水溶性ポリマー市場の成長を妨げると予想されます。

バイオベースのアクリルアミドに対する需要の高まりと、製薬業界における水溶性ポリマーの用途拡大は、予測期間中、メーカーに様々な機会を提供すると予想されます。

アジア太平洋地域は世界の水溶性ポリマー市場を独占しており、予測期間中に最も高いCAGRを維持すると予測されています。

水溶性ポリマー市場の動向

予測期間中、水処理産業が市場を独占する見込み

- 水質と環境保護に関する厳しい規制が、水処理ソリューションの需要を促進しています。水溶性ポリマーは、廃水や飲料水源から有機物、浮遊物質、重金属などの汚染物質を除去し、規制基準に適合させることで、水処理プロセスにおいて重要な役割を果たしています。

- 下水処理場などの自治体インフラや、化学処理施設、パルプ・製紙工場、繊維製造工場などの産業インフラへの投資が、水溶性ポリマーを含む水処理薬品への需要を押し上げています。これらのポリマーは、自治体や産業界の廃水処理プロセスにおいて、汚泥脱水、沈殿、濃縮など様々な目的で利用されています。

- ダラス連邦準備銀行が発表したデータによると、米国を除く世界の工業生産は2023年1月に0.67増加しました。

- ドイツの水処理市場は欧州最大です。主に同国北部地域での水処理活動の活発化が、水処理用ポリマーの需要を押し上げています。連邦環境自然保護省によると、同国の給水・排水処理産業は年間約220億ユーロ(約233億3,000万米ドル)を占めています。

- 2024年1月、グラディアントのH+Eはドイツで、最大級の半導体工場向けの水処理施設の建設を受注しました。プロジェクトは間もなく開始され、2025年に完成する予定です。

- インド政府ジャル・シャクティ省が発表した報告書によると、2022会計年度において、農村人口の61.5%がパイプシステムを通じて敷地内で安全かつ十分な飲料水を利用できるようになっています。近年、インドの農村部で安全な飲料水を利用できる人の数は、2016会計年度の40%未満から大幅に増加しています。

- 持続可能な水管理の実践と、水処理プロセスにおける環境に優しい化学物質の使用が重視されるようになってきています。生分解性で無害な水溶性ポリマーは、効果的な水処理を確保しながら環境フットプリントの削減を目指す環境意識の高い産業や政府にとって好ましい選択肢です。

- こうした要因から、水処理産業の成長が予測期間中の市場を牽引すると予想されます。

予測期間中、アジア太平洋地域が市場を独占する見込み

- アジア太平洋地域では工業化が急速に進んでおり、水処理、食品加工、医薬品、パーソナルケア、農業など様々な産業で水溶性ポリマーの需要が増加しています。

- 農業は多くのアジア太平洋諸国において重要な産業です。水溶性ポリマーは農業において、土壌改良、侵食防止、乾燥・半乾燥地域での保水性向上のために使用されています。農業の近代化と機械化に伴い、これらのポリマーの需要は増加すると予想されます。

- インドネシア統計局およびインドネシア農業省によると、インドネシアにおけるパーム油の生産量は2017年の3,494万トンから2022年には4,558万トンに増加します。

- フィリピン統計局が発表したデータによると、フィリピンにおけるトウモロコシの生産量は2022年に826万トンに達し、2016年の722万トンから増加しました。

- アジア太平洋の建設業界は、特に中国、インド、東南アジアで活況を呈しています。水溶性ポリマーは、セメント系、モルタル、グラウトなどの建設資材に幅広く使用されており、市場での優位性に寄与しています。

- 国土交通省が発表した報告書によると、日本の建設投資総額は2018年の61兆8,300億人民元(4,100億米ドル)から2023年には70兆3,200億人民元(4,700億米ドル)に増加しました。

- 以上の要因から、予測期間中、アジア太平洋地域が水溶性ポリマー市場を独占すると予想されます。

水溶性ポリマー産業の概要

水溶性ポリマー市場は細分化されています。主なプレーヤー(順不同)としては、SNF Group, Ashland, DuPont, CP Kelco U.S. Inc., and Arkemaなどが挙げられます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 北米におけるシェールガス産業の成長

- アジア太平洋における水処理産業の急成長

- 抑制要因

- 原材料価格の変動

- その他の阻害要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- タイプ

- ポリアクリルアミド

- ポリビニルアルコール

- グアーガム

- ゼラチン

- キサンタンガム

- ポリアクリル酸

- ポリエチレングリコール

- その他のタイプ(セルロースエーテル、ペクチン、でんぷん)

- エンドユーザー産業

- 水治療

- 飲食品

- パーソナルケアと衛生

- 石油・ガス

- パルプ・製紙

- 製薬

- その他エンドユーザー産業(農薬)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- インドネシア

- マレーシア

- タイ

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- トルコ

- ロシア

- ノルディック

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ナイジェリア

- エジプト

- カタール

- アラブ首長国連邦

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Arkema

- Ashland

- BASF SE

- CP Kelco U.S. Inc.

- DuPont

- Gantrade Corporation

- Kemira

- Kuraray Co. Ltd

- Merck KGaA

- Mitsubishi Chemical Corporation

- Nouryon

- Polysciences Inc.

- SNF Group

- Sumitomo Seika Chemicals Co. Ltd

第7章 市場機会と今後の動向

- バイオベースのアクリルアミドに対する需要の増加

- 製薬業界における用途の拡大

The Water-soluble Polymer Market size is estimated at USD 38.66 billion in 2025, and is expected to reach USD 49.34 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The COVID-19 pandemic negatively affected the water-soluble polymer market. Reduced industrial activity, supply chain disruptions, and changes in consumer behavior affected demand for water-soluble polymers in these industries. Many industries utilizing water-soluble polymers, such as water treatment, textiles, personal care, and food processing, experienced slowdowns or temporary shutdowns during the pandemic. However, as economic conditions improved and projects resumed, the demand for polymers used in the abovementioned industries increased.

The factors driving the market's growth are the growing shale gas industry in North America and the rising demand for water-soluble polymers from the global water treatment industry.

However, fluctuations in raw material prices are expected to hamper the growth of the water-soluble polymer market during the forecast period.

The rising demand for bio-based acrylamide and growing applications of water-soluble polymers in the pharmaceutical industry are expected to offer various opportunities for manufacturers during the forecast period.

Asia-Pacific dominated the global water-soluble polymer market, and it is projected to hold the highest CAGR during the forecast period.

Water-soluble Polymer Market Trends

The Water Treatment Industry is Expected to Dominate the Market during the Forecast Period

- Stringent regulations for water quality and environmental protection drive the demand for water treatment solutions. Water-soluble polymers play a crucial role in water treatment processes by aiding in the removal of contaminants, such as organic matter, suspended solids, and heavy metals, from wastewater and drinking water sources to meet regulatory standards.

- Investments in municipal infrastructure, such as sewage treatment plants, and industrial infrastructure, including chemical processing facilities, pulp and paper mills, and textile manufacturing plants, drive the demand for water treatment chemicals, including water-soluble polymers. These polymers are utilized for various purposes, such as sludge dewatering, sedimentation, and thickening, in both municipal and industrial wastewater treatment processes.

- Global industrial production, excluding the United States, increased by 0.67 in January 2023, according to the data published by the Federal Reserve Bank of Dallas.

- The German water treatment market is the largest in Europe. The increasing water treatment activities, primarily in the country's northern region, are boosting the demand for water treatment polymers. According to the Federal Ministry for the Environment and Nature Conservation, the country's water supply and wastewater treatment industries account for about EUR 22 billion ( approximately USD 23.33 billion) annually.

- In January 2024, Gradiant's H+E won a contract in Germany to build a water treatment facility for one of the largest semiconductor fabs. The project is expected to commence soon and be completed in 2025.

- According to the report published by the Ministry of Jal Shakti of the Government of India, 61.5% of the rural population had access to safe and adequate drinking water in their premises through a pipe system during the financial year 2022. In recent years, the number of rural people in India who have access to safe drinking water has increased significantly, from less than 40% in the financial year 2016.

- There is a growing emphasis on sustainable water management practices and the use of eco-friendly chemicals in water treatment processes. Water-soluble polymers that are biodegradable and non-toxic are preferred choices for eco-conscious industries and governments aiming to reduce their environmental footprint while ensuring effective water treatment.

- Due to these factors, the growth in the water treatment industry is anticipated to drive the market over the forecast period.

Asia-Pacific is Expected to Dominate the Market during the Forecast Period

- Asia-Pacific is experiencing rapid industrialization, leading to increased demand for water-soluble polymers across various industries such as water treatment, food processing, pharmaceuticals, personal care, and agriculture.

- Agriculture is a significant industry in many Asia-Pacific countries. Water-soluble polymers are used in agriculture for soil conditioning, erosion control, and improving water retention in arid and semi-arid regions. As agricultural practices modernize and mechanize, the demand for these polymers is expected to rise.

- According to Statistics Indonesia and the Ministry of Agriculture Indonesia, the production volume of palm oil in Indonesia increased from 34.94 million metric tons in 2017 to 45.58 million metric tons in 2022.

- According to the data published by the Philippine Statistics Authority, the production volume of corn in the Philippines reached 8.26 million metric tons in 2022, which increased from 7.22 million metric tons in 2016.

- The Asia-Pacific construction industry is booming, especially in China, India, and Southeast Asia. Water-soluble polymers are extensively used in construction materials such as cementitious systems, mortars, and grouts, contributing to their dominance in the market.

- According to the report released by the Ministry of Land, Infrastructure, Transport and Tourism, the total investment in construction in Japan increased from CNY 61.83 trillion (USD 0.41 trillion) in 2018 to CNY 70.32 trillion (USD 0.47 trillion) in 2023.

- Based on the abovementioned factors, Asia-Pacific is expected to dominate the water-soluble polymer market during the forecast period.

Water-soluble Polymer Industry Overview

The water-soluble polymer market is fragmented in nature. The major players (not in any particular order) include SNF Group, Ashland, DuPont, CP Kelco U.S. Inc., and Arkema.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Shale Gas Industry in North America

- 4.1.2 Surging Water Treatment Industry in Asia-Pacific

- 4.2 Restraints

- 4.2.1 Fluctuating Prices of Raw Materials

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Polyacrylamide

- 5.1.2 Polyvinyl Alcohol

- 5.1.3 Guar Gum

- 5.1.4 Gelatin

- 5.1.5 Xanthan Gum

- 5.1.6 Polyacrylic Acid

- 5.1.7 Polyethylene Glycol

- 5.1.8 Other Types (Cellulose Ethers, Pectin, and Starch)

- 5.2 End-user Industry

- 5.2.1 Water Treatment

- 5.2.2 Food and Beverage

- 5.2.3 Personal Care and Hygiene

- 5.2.4 Oil and Gas

- 5.2.5 Pulp and Paper

- 5.2.6 Pharmaceutical

- 5.2.7 Other End-user Industries (Agrochemicals)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Indonesia

- 5.3.1.6 Malaysia

- 5.3.1.7 Thailand

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 Russia

- 5.3.3.8 NORDIC

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Egypt

- 5.3.5.5 Qatar

- 5.3.5.6 United Arab Emirates

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Arkema

- 6.4.2 Ashland

- 6.4.3 BASF SE

- 6.4.4 CP Kelco U.S. Inc.

- 6.4.5 DuPont

- 6.4.6 Gantrade Corporation

- 6.4.7 Kemira

- 6.4.8 Kuraray Co. Ltd

- 6.4.9 Merck KGaA

- 6.4.10 Mitsubishi Chemical Corporation

- 6.4.11 Nouryon

- 6.4.12 Polysciences Inc.

- 6.4.13 SNF Group

- 6.4.14 Sumitomo Seika Chemicals Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for Bio-based Acrylamide

- 7.2 Growing Application in the Pharmaceutical Industry