|

市場調査レポート

商品コード

1640550

スチレン-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Styrene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スチレン-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

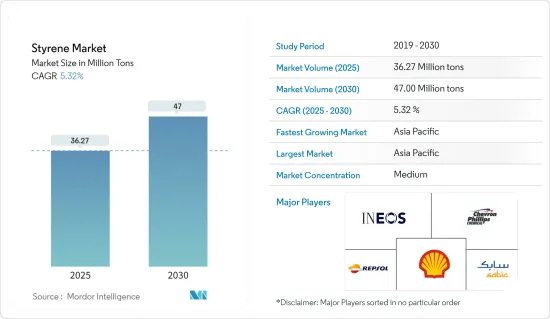

スチレン市場規模は2025年に3,627万トンと推定され、予測期間(2025~2030年)のCAGRは5.32%で、2030年には4,700万トンに達すると予測されます。

COVID-19パンデミックはスチレン市場にマイナスの影響を与えました。しかし、包装、建設、自動車など様々な産業での消費増加により、市場は2021年に大きく回復しました。

主要ハイライト

- 短期的には、民生用電子機器産業からの需要増加が市場成長の主要要因です。

- しかし、包装産業におけるバイオベースプラスチックの使用増加は、市場の成長を抑制する可能性が高いです。

- バイオベースのポリスチレンを開発するための研究が進められており、世界市場に有利な成長機会がまもなく生まれると考えられます。

- アジア太平洋がスチレン市場を独占しており、最大の消費国は中国、日本、ASEAN諸国などです。

スチレン市場の動向

包装産業が市場を牽引

- スチレンは、その良好な特性から包装産業で一般的に使用されています。透明性、耐衝撃性、断熱性に優れた汎用性の高い軽量プラスチックです。これらの特性により、幅広い包装用途に適しています。

- 包装産業におけるスチレンの最も一般的な用途の一つは、発泡ポリスチレン(EPS)または発泡スチロールと呼ばれるポリスチレンフォームの製造です。EPSフォームは、クッション材、生鮮品の断熱包装、軽量輸送コンテナなどの保護包装に広く使用されています。

- スチレンは硬質ポリスチレンの製造にも使われ、食品包装によく使われています。クラムシェル、カップ、トレイなどの透明なポリスチレン容器は、その透明性から外食産業で人気があり、顧客は中身を簡単に見ることができます。

- さらに、ポリスチレンは医療産業でも様々な包装用途に使用されています。IQVIAによると、世界の医薬品市場は近年大きく成長しています。世界の医薬品市場全体の2022年までの市場規模は1兆4,800億米ドルです。これは1兆4,200億米ドルと評価された2021年からのわずかな増加に過ぎないです。

- アジア太平洋では、ライフスタイルの変化、人々の可処分所得の増加、社会人の増加、ファーストフード嗜好の高まりにより、包装食品の需要が伸びています。

- 中国は、一人当たり所得の増加、eコマース大手の台頭などの要因により、世界最大の包装消費国となっています。インドの包装産業は世界第5位であり、インドプラスチック工業協会によると、年間約22~25%で成長しています。高度に熟練した労働力と安価な人件費により、包装・加工食品のコストは欧州よりも40%低く抑えることができます。人口の増加と包装需要の増加が市場を牽引すると予想されます。

- 同様に、2022年には、欧州の飲食品産業は460万人を雇用し、1兆1,000億ユーロ(1兆1,590億米ドル)の収益と2,300億ユーロ(2,423億7,000万米ドル)の付加価値を生み出し、欧州最大の製造業の1つとなっています。これにより、この地域における飲食品産業の成長は、食品包装の需要を増加させ、調査された市場を後押ししています。

- Statistisches Bundesamtによると、ドイツの包装産業の収益は2022年に350億4,000万ユーロ(377億1,000万米ドル)に達し、以前と比較して成長を記録しています。

- このような要因が、包装セグメントからの調査市場の需要を支えていると考えられます。

アジア太平洋が市場を独占する見込み

- アジア太平洋が市場を独占しており、予測期間中もその支配は続くとみられます。

- 同地域全体での包装用途の増加、電気・電子製品の旺盛な需要、自動車・運輸部門の急成長がスチレン市場を積極的に後押ししています。

- ZEVIによると、アジアのエレクトロ市場は2021年に10%増の3兆1,100億ユーロ(3兆6,700億米ドル)に達しました。2022年の需要は13%増加し、2023年の成長率は7%と推定されます。中国市場は世界最大であり、先進工業国の合計市場よりも大きいです。さらに、中国の電子産業は2022年に14%拡大し、2023年には8%の成長が見込まれています。

- 中国汽車工業協会(CAAM)によると、中国は世界最大の自動車生産基地を有し、2022年の自動車総生産台数は2,700万台で、昨年の2,600万台に比べて3.4%の増加を記録します。

- 中国は世界の主要包装産業のひとつです。同国は、カスタマイズ包装の台頭と食品セグメントにおける包装消費財の需要増加により、予測期間中一貫した成長が見込まれています。Interpakによると、中国では食品包装カテゴリーにおいて、包装総量は2023年に4,470億個に達する見込みです。

- 産業誌によると、2021~2022年にかけて、Sinopec Gulei、Zhejiang Petrochemical、Shandong Lihuayaのような会社の新施設を含む、合計350万トン以上の生産能力を持つポリスチレンとABSプラスチックの新工場が立ち上がる見込みです。しかし、国内のエネルギー危機のために遅れが見られる可能性があります。

- 同様に、インド包装産業協会(PIAI)によると、インドの包装産業は予測期間中に22%の成長率が見込まれています。さらに、インドの包装市場は、2020~2025年の間に26.7%のCAGRを記録し、2025年までに2,048億1,000万米ドルに達すると予想されています。したがって、プラスチック射出成形市場はこの地域で成長すると予想されます。

- エレクトロニクスについては、日本電子情報技術産業協会(JEITA)によると、世界のエレクトロニクス・IT産業の生産額は2021年の3兆3,600億米ドルに対し、2022年には3兆4,400億米ドルと推定され、前年比1%の成長率を記録しました。

- このように、上記の要因は、この地域の様々なエンドユーザーからのスチレン需要の高まりを示すものです。

スチレン産業概要

調査した市場は、主要企業によって部分的に細分化されています。主要企業(順不同)には、Shell PLC、Chevron Phillips Chemical Company LLC、SABIC、Repsol、INEOSなどが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 民生用電子機器産業からの需要増加

- 包装産業からの需要増加

- その他の促進要因

- 抑制要因

- 包装産業におけるバイオベースプラスチックの使用の増加

- その他の抑制要因

- 産業のバリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模(数量ベース))

- 製品タイプ

- ポリスチレン

- アクリロニトリル・ブタジエン・スチレン

- スチレンブタジエンゴム

- その他の製品タイプ(スチレン-アクリロニトリル)

- エンドユーザー産業

- 包装

- 建築

- 消費財

- 自動車と輸送

- 電気・電子

- その他のエンドユーザー産業(繊維)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Chevron Phillips Chemical Company

- Covestro AG

- Hanwha Group

- INEOS(INEOS Styrolution)

- LG Chem

- LyondellBasell Industries Holdings BV

- Reliance Industries Ltd

- Repsol

- SABIC

- Shell PLC

- Versalis SpA(Eni SpA)

第7章 市場機会と今後の動向

- バイオベースポリスチレンの開発研究が進行中

- その他の機会

The Styrene Market size is estimated at 36.27 million tons in 2025, and is expected to reach 47.00 million tons by 2030, at a CAGR of 5.32% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the styrene market. However, the market recovered significantly in 2021, owing to rising consumption of various industries, such as packaging, construction, automotive, and others.

Key Highlights

- Over the short term, the growing demand from the consumer electronics industry is a major factor driving the growth of the market studied.

- However, increasing usage of bio-based plastics in the packaging industry is likely to restrain the growth of the market.

- Nevertheless, ongoing research to develop bio-based polystyrene is likely to create lucrative growth opportunities for the global market soon.

- The Asia-Pacific region dominates the styrene market, with the largest consumption coming from countries such as China, Japan, ASEAN countries, etc.

Styrene Market Trends

Packaging Industry to Drive the Market

- Styrene is commonly used in the packaging industry due to its favorable properties. It is a versatile, lightweight plastic with excellent clarity, impact resistance, and thermal insulation. These characteristics make it suitable for a wide range of packaging applications.

- One of the most common uses of styrene in the packaging industry is in producing polystyrene foam, often referred to as expanded polystyrene (EPS) or Styrofoam. EPS foam is widely used for protective packaging, including cushioning materials, insulation for perishable goods, and lightweight shipping containers.

- Styrene is also used to produce rigid polystyrene, which is commonly employed in food packaging. Clear polystyrene containers, such as clamshells, cups, and trays, are popular in the food service industry due to their transparency, allowing customers to view the contents easily.

- Furthermore, polystyrene is also used in the medical and healthcare industries for various packaging applications; IQVIA shows that the global pharmaceutical market has grown significantly in recent years. The total global pharmaceutical market was valued at USD 1.48 trillion by 2022. This is only a slight increase from 2021 when the market was valued at USD 1.42 trillion.

- In Asia-Pacific, the demand for packaged food is growing, owing to lifestyle changes, the growing disposable income of people, the increasing number of working professionals, and the growing preference for fast food.

- China is the world's largest packaging consumer across the world owing to the factors such as growing per capita income, coupled with rising e-commerce giants in the country. India's packaging industry is the fifth-largest in the world, and it is growing at about 22-25% per year, as per the Plastics Industry Association of India. Packaging and processing food costs can be 40% lower than in Europe because of highly skilled labor and cheap labor costs. The growing population and increasing demand for packaging are expected to drive the market.

- Similarly, in 2022, the Europe food and beverages industry employs 4.6 million people and generates EUR 1.1 trillion (USD 1.159 trillion) in revenue and EUR 230 billion (USD 242.37 billion) in value-added, making it one of the largest manufacturing industries in Europe. Thereby, the growing food and beverages industry in the region is increasing the demand for food packaging, as well as boosting the market studied.

- According to Statistisches Bundesamt, the revenue of the packaging industry in Germany has reached EUR 35.04 billion (USD 37.71 billion) in 2022 and has registered growth when compared to previous years.

- Such factors are likely to support the demand for the studied market from the packaging segment.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific dominated the market and will likely continue its dominance during the forecast period.

- Increasing packaging applications across the region, robust demand for electrical and electronic products, and the rapid growth of automotive and transportation sectors are actively boosting the styrene market.

- According to ZEVI, the Asian electro market reached EUR 3.11 trillion (USD 3.67 trillion) in 2021, a 10% rise. The demand increased by 13% in 2022 and estimated a 7% growth rate for 2023. China's market is the largest in the world, even more significant than the combined markets of all industrialized countries. In 2021, the Chinese market contributed EUR 2.07 trillion (USD 2.45 trillion), or 41.6% of the world market; additionally, the Chinese electronic industry expanded by 14% in 2022, and the sector is expected to grow by 8% in 2023.

- According to the China Association of Automobile Manufacturers (CAAM), China has the largest automotive production base in the world, with a total vehicle production of 27 million units in 2022, registering an increase of 3.4 % compared to 26 million units produced last year.

- China is one of the key packaging industries in the world. The country is expected to witness consistent growth during the forecast period due to the rise of customized packaging and increased demand for packaged consumer goods in the food segment. According to Interpak, in China, in the foodstuff packaging category, total packaging is expected to reach 447 billion units in 2023.

- According to industry publications, in 2021-2022, new factories for polystyrene and ABS plastics were expected to launch with a combined capacity of over 3.5 million tons, including new facilities for companies like Sinopec Gulei, Zhejiang Petrochemical, and Shandong Lihuaya. However, a delay may be observed due to the energy crisis in the country.

- Similarly, according to the Packaging Industry Association of India (PIAI), the Indian packaging industry is expected to grow at a rate of 22% during the forecast period. Moreover, the Indian packaging market is expected to reach USD 204.81 billion by 2025, registering a CAGR of 26.7% between 2020 and 2025. Therefore, the plastic injection molding market is expected to grow in the region.

- Considering electronics, according to the Japan Electronics and Information Technology Industries Association (JEITA), the production by the global electronics and IT industry was estimated at USD 3.44 trillion in 2022, registering a growth rate of 1% year on year, compared to USD 3.36 trillion in 2021.

- Thus, the abovementioned factors indicate the rising demand for styrene from various end users in the region.

Styrene Industry Overview

The market studied is partially fragmented among the top players. The key players (not in any particular order) include Shell PLC, Chevron Phillips Chemical Company LLC, SABIC, Repsol, and INEOS, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand from the Consumer Electronics Industry

- 4.1.2 Increasing Demand from Packaging Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Increasing Usage of Bio-based Plastics in the Packaging Industry

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Polystyrene

- 5.1.2 Acrylonitrile Butadiene Styrene

- 5.1.3 Styrene Butadiene Rubber

- 5.1.4 Other Product Types (Styrene-Acrylonitrile)

- 5.2 End-user Industry

- 5.2.1 Packaging

- 5.2.2 Construction

- 5.2.3 Consumer Goods

- 5.2.4 Automotive and Transportation

- 5.2.5 Electrical and Electronics

- 5.2.6 Other End-user Industries (Textile)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Chevron Phillips Chemical Company

- 6.4.2 Covestro AG

- 6.4.3 Hanwha Group

- 6.4.4 INEOS (INEOS Styrolution)

- 6.4.5 LG Chem

- 6.4.6 LyondellBasell Industries Holdings BV

- 6.4.7 Reliance Industries Ltd

- 6.4.8 Repsol

- 6.4.9 SABIC

- 6.4.10 Shell PLC

- 6.4.11 Versalis SpA (Eni SpA)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Ongoing Research to Develop Bio-based Polystyrene

- 7.2 Other Opportunities