|

市場調査レポート

商品コード

1637714

水路輸送ソフトウェアソリューション:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Waterway Transportation Software Solutions - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 水路輸送ソフトウェアソリューション:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

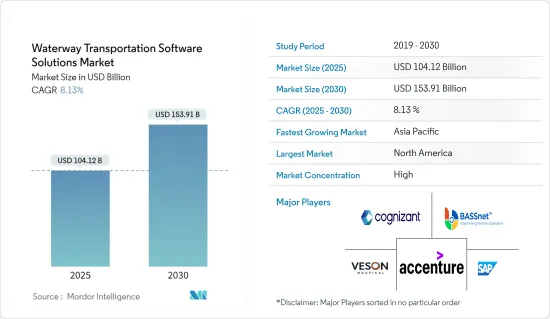

水路輸送ソフトウェアソリューション市場規模は、2025年に1,041億2,000万米ドルと推定され、2030年には1,539億1,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは8.13%です。

どのような新興経済諸国においても、輸送はその開発において重要な役割を果たしています。膨大な量のデジタルデータ構築を活用する動向の高まりや、海運/船舶産業における様々なクラウドサービスの浸透の増加に伴い、先進的な追跡、通信、船舶管理技術の採用が市場の成長を広範囲に牽引しています。

主要ハイライト

- 世界の重量貨物輸送の需要増加により、市場は大きく牽引されています。輸送プロセスの標準化が市場の成長を後押ししています。さらに、コンテナ化の普及と新興港湾の増加が市場開拓に影響を与えています。コンテナ化の採用は産業に劇的な変化をもたらしました。

- 水上貿易におけるパートナーシップの増加は、特にアジア太平洋と中東・アフリカの新興経済諸国における新市場をもたらしました。インドや中国のような新興国市場が需要の変化をもたらし、市場の成長を後押ししています。加えて、世界中の様々な新航路や海港の開拓は、調査対象市場に成長機会を提供しています。

- 機械間(M2M)通信やコンテナ化などの新しい重要な技術開発は、水路輸送に劇的な変化をもたらし、輸送産業を一変させました。これらの技術は、海運組織における作業形態を大きく変えつつあります。一方、海賊事件や船舶事故などの懸念から、海運会社はマネージドサービスや監査ソフトウェアなどのソリューションを選択するようになっており、市場シナリオの中で大きな成長機会が生まれると予想されます。

- しかし、厳しい排出に関する法律や施策の増加、水路輸送ソフトウェアやサービスによって提供される利点に関する認識の欠如は、予測期間を通じて市場全体の成長を制限する可能性のある懸念事項である可能性があります。

- COVID-19パンデミックは海運・海事産業に大きな影響を与えました。検疫(隔離期間)の間、あらゆる種類の水上輸送が停止されたためです。しかし、COVID-19後の市場シナリオでは、水路輸送ソリューションの強化に重点を置き、産業が必要とする重要な業務改善を行う機会があるため、市場は大きな成長機会を目の当たりにすると予想されます。

水路輸送ソフトウェアソリューション市場の動向

新興国市場における新港の設立が市場を牽引する見込み

- 港湾インフラは、港湾を通過する貨物、船舶、旅客にサービスを提供するための港湾業務の主要な基盤です。港湾インフラを拡大するには、資本集約的なさまざまな投資、長いリードタイム、長期的な計画が必要です。港湾インフラの設計は、海運、ロジスティクス、運輸部門の複数のニーズを予測する必要があります。安全で効率的な経済活動を確保するための港湾インフラへの政府投資の増加は、市場を大きく牽引すると予想されます。

- 世界貿易の大半が港湾によって運ばれる中、海は主に地域全体とその内陸輸送網を世界市場につなぐ重要なゲートウェイインフラです。したがって、多くの新興諸国や発展途上国にとって、十分に機能する堅牢な海上輸送インフラの開発は経済成長の重要な要因です。港湾における官民パートナーシップは、港湾運営をより効果的に管理し、新しい港湾インフラを構築・建設するために不可欠なものとなっており、従来はどちらも専ら政府の機能でした。

- 同市場では、主要な市場参入企業による様々な重要な買収、合併、投資が行われており、その戦略の一環として、事業と全体的なプレゼンスを向上させ、顧客にリーチし、広範なアプリケーションに対する顧客の要求を満たし、満たすことができるようになっています。例えば、2023年3月、Saigon Newport Corporationは、2年以上にわたる成功裏の操業の後、Tan Cang Que Vo Dry Port(ICD)の正式な立ち上げを宣言しました。Tan Cang Que Vo Dry Port(ICD)の立ち上げ式には、運輸省、海軍、バクニン省、バクザン省の地方自治体、関連省庁の代表者、船会社、パートナー企業、輸出入企業、物流企業、協会、専門機関、報道機関から250人の出席者が出席しました。

- 2022年9月、国際海事機関(IMO)は英連邦事務局と戦略的パートナーシップ協定を締結し、両機関はサステイナブル海上輸送システムとプラクティスの採用を促進・促進する活動を通じて、特定の開発途上国の港湾・海事セクターを強化することを約束しました。

- Cargotec Oyjによると、世界のコンテナ処理量は2025年まで増加し続けると予測されています。2022年には、アジア太平洋で約5億5,300万TEU相当のコンテナが処理されたが、同地域内で約6億1,700万TEU相当のコンテナという画期的な数字に達する可能性が高いと予想され、その結果、市場の成長と拡大に十分な機会が生まれると考えられます。

北米が最大の市場シェアを占める展望

- 北米は、技術ベースのソリューションにとって最も重要な市場のひとつです。さらに、新技術の開発と実装を中心に、世界経済における強力な参入企業となることが期待されています。工業用品の販売に関しては、インターネットの影響力の増大に伴い、工業部門が着実に成長しています。

- 米国の石油生産の拡大と石油生産地の変化によって、石油を精製所やターミナルに運ぶためのさまざまな輸送手段の利用が増加しています。パイプラインは石油輸送の主要な輸送手段のひとつであり続けたが、近年は水上輸送の重要性が大幅に増しています。

- 北米の海洋産業に変化をもたらしている重要な技術には、デジタル化の動向の高まり、インダストリー4.0の拡大傾向、AI(人工知能)、クラウドコンピューティング、ビッグデータ、サイバーセキュリティ、IoT(モノのインターネット)、デジタルツイン、ブロックチェーン、機械学習、ロボット工学など、さまざまな先端技術の全体的な利用の増加があります。

- さらに、貿易障壁の減少により、カナダや米国など北米のさまざまな国の輸送インフラやサービスに関する情報のニーズが高まっています。カナダ・米国自由貿易協定とそれに続く北米自由貿易協定という2つの重要なイニシアチブは、これらの国間の物品サービス貿易の自由化にとって重要な指標であり、予測期間を通じて市場の成長と拡大のための十分な成長機会を創出しました。

- さらに、同市場では大規模な買収、合併、政府投資が行われています。例えば、2022年12月、ジョン・ベル・エドワーズ州知事は、ルイジアナ州、ニューオーリンズ港、世界の海運産業のリーダー2社による歴史的な官民パートナーシップを宣言し、ミシシッピ川下流に18億米ドルの最新鋭コンテナ施設を建設しました。セント・バーナード・パリッシュに新設されるルイジアナ・インターナショナル・ターミナル(LIT)は、あらゆるサイズの船舶に対応し、ルイジアナ州の輸出入能力を飛躍的に高めています。これは、予測期間中に十分な成長機会を生み出すと期待されます。

水路輸送ソフトウェアソリューション産業概要

SAP SE、Cognizant、Accenture PLC、Bass Software Ltdなどの主要企業が存在するため、市場における企業間の競合関係は高いです。研究開発への継続的な投資により、各社は製品を革新し、市場に新製品を投入することができます。

- 2023年3月-Union Minister for Shipping Ports and Waterways and Ayushは、MoPSWのリアルタイムパフォーマンス・モニタリング・ダッシュボード「Sagar Manthan」を事実上導入しました。これは主に、同省とその他の子会社に関連するすべての統合データを備えたデジタルプラットフォームです。このダッシュボードは、よく調整されたリアルタイムの情報を改善することにより、様々な部門の業務に変革をもたらすと考えられます。

- 2023年2月-IBS SoftwareがAccentureの貨物・物流ソフトウェアを買収。この買収により、貨物サプライチェーンにおけるIBSの足跡が拡大し、デジタルトランスフォーメーションとイノベーションが加速します。AFLSは、航空会社や海上輸送会社が貨物業務を管理し、デジタルトランスフォーメーションとイノベーションを通じて成長するための技術プラットフォームを記載しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- バリューチェーン/サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場力学

- 市場促進要因

- 貨物量の増加

- 新興諸国における新港の設立

- 市場抑制要因

- 厳しい排出規制と施策

第6章 市場セグメンテーション

- 展開別

- オンプレミス

- クラウド

- ハイブリッド

- エンドユーザー産業別

- 小売

- 石油・ガス

- 製造・産業

- 航空宇宙・防衛

- 化学

- 建設

- 医療

- 飲食品

- その他のエンドユーザー産業別

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- SAP SE

- Cognizant Technology Solutions Corp

- Accenture PLC

- Veson Nautical Corporation

- DNV GL(GL Maritime Software GmbH)

- Aljex Software Inc.

- Descartes Systems Group

- HighJump Software Inc.

- Trans-i Technologies Inc.

- Bass Software Ltd.

第8章 投資分析

第9章 市場機会と今後の動向

The Waterway Transportation Software Solutions Market size is estimated at USD 104.12 billion in 2025, and is expected to reach USD 153.91 billion by 2030, at a CAGR of 8.13% during the forecast period (2025-2030).

Transportation plays a vital role in the development of any economy. With the rising trend of utilizing huge amounts of digital data building and the increased penetration of various cloud services in the shipping/marine industry, adopting advanced tracking, communication, and ship management technology is extensively driving the market's growth.

Key Highlights

- The market studied is heavily driven by the increasing demand for global heavy freight transportation. The rise in the standards of transportation processes has boosted the market's growth. Additionally, the growing popularity of containerization and the increase in the number of new ports have influenced the development of the market studied. The introduction of containerization has brought about a dramatic shift in the industry.

- The increasing partnerships in the waterborne trade have resulted in new markets, especially in the developing economies of Asia-Pacific and the Middle East & Africa. Developing countries like India and China are responsible for the demand shift, propelling the market's growth. In addition, developing various new sea routes and seaports across the globe provides growth opportunities for the market studied.

- New vital technological developments, such as machine-to-machine (M2M) communication and containerization, have transformed the transportation industry with drastic changes in waterway transport. These technologies are significantly transforming the work patterns in shipping organizations. On the other hand, concerns related to various piracy incidents and ship accidents, which have made shipping companies opt for solutions, including managed services and audit software, are expected to create immense growth opportunities within the market scenario.

- However, the rise in stringent emission laws and policies and the absence of awareness about the advantages offered by waterway transportation software and services could be a matter of concern that could limit the market's overall growth throughout the forecast period.

- The COVID-19 pandemic significantly impacted the shipping and maritime industries. The setback resulted from halting all types of shipments by water during this quarantine (period of isolation), as the movement of such shipments by sea could spread the virus from one port to another. However, in the post-COVID-19 market scenario, the market is expected to witness significant growth opportunities since there lies a chance for industries to make much-needed critical operational improvements with considerable emphasis on enhancing waterway transportation solutions.

Waterway Transportation Software Solutions Market Trends

Establishment of New Ports in Developing Countries is Expected to Drive the Market

- Port infrastructure is the prime foundation of port operations for servicing cargo, ships, and passengers passing throughout the port. Expanding port infrastructure requires various capital-intensive investments, long lead times, and long-term planning. Port infrastructure design needs to anticipate the multiple needs of the shipping, logistics, and transportation sectors. An increase in government investments in port infrastructures to ensure safe and efficient economic activities is expected to drive the market significantly.

- With most of the global trade carried by ports, the sea is a critical gateway infrastructure that mainly connects an entire region and its inland transportation network to the worldwide market. Therefore, developing well-functioning, robust maritime transport infrastructure is a significant factor of economic growth for many emerging and developing countries. Public-private partnerships in ports have become vital to managing port operations more effectively and creating and building new port infrastructure, traditionally both exclusively government functions.

- The market is witnessing various significant acquisitions, mergers, and investments by key market players as part of its strategy to improvise business and its overall presence to reach customers and meet and fulfill their requirements for a broad range of applications. For instance, in March 2023, Saigon Newport Corporation declared the official launch of Tan Cang Que Vo Dry Port (ICD) after more than two years of successful operation. Esteemed leaders from the Ministry of Transport, the Navy, and local authorities of Bac Ninh, Bac Giang Province, along with representatives from relevant ministries, 250 attendees from shipping lines, partners, import and export enterprises, logistics enterprises, associations, and specialized agencies, media agencies were present at the launch of Tan Cang Que Vo Dry Port (ICD) as a Dry Port and inland clearance point.

- In September 2022, The International Maritime Organization (IMO) signed a strategic partnership agreement with the Commonwealth Secretariat, under which both organizations committed to strengthening the port and maritime sectors in selected developing countries through activities that would promote and facilitate the adoption of sustainable maritime transport systems and practices.

- According to Cargotec Oyj, global container throughput is projected to keep increasing until 2025. In 2022, some 553 million TEUs worth of containers were processed in the Asia-Pacific region, and it was expected that it would likely reach a landmark of around 617 million TEUs worth of containers within the region, which in turn would create ample opportunities for the market to grow and expand.

North America is Expected to Hold the largest Market Share

- North America is one of the most significant markets for technology-based solutions. It is further expected to be a strong player in the global economy, primarily in developing and implementing new technologies. The industrial sector is growing steadily, in line with the increasing influence of the internet, regarding the sales of industrial goods.

- The expansion of US oil production and changes in the location of oil production have increased the use of various transportation modes to move the oil to refineries and terminals. Although pipelines continued to be one of the predominant modes for carrying oil, the prominence of water transportation has been increasing substantially in recent years.

- Some of the crucial technologies that are altering the North American marine industry are the rise in the trend of digitalization, the growing trend of Industry 4.0, the increase in the overall usage of various advanced technologies like AI (artificial intelligence), cloud computing, big data, cyber security, internet of things (IoT), digital twin, blockchain, machine learning, and robotics.

- Moreover, reduced trade barriers have increased the need for information on transportation infrastructure and services within various countries in North America, such as Canada and the United States. Two key initiatives, the Canada-US Free Trade Agreement and the subsequent North American Free Trade Agreement, were significant indicators for the liberalization of trade in goods and services between these countries, creating ample growth opportunities for the market to grow and expand throughout the forecast period.

- Furthermore, the market is witnessing significant acquisitions, mergers, and government investments. For instance, in December 2022, Gov. John Bel Edwards declared a historic public-private partnership between Louisiana, the Port of New Orleans, and two global maritime industry leaders to build a USD 1.8 billion state-of-the-art container facility on the Lower Mississippi River. The new Louisiana International Terminal (LIT) in St. Bernard Parish would be able to serve vessels of all sizes, dramatically increasing Louisiana's import and export capacity. This is expected to create ample growth opportunities for the forecast period.

Waterway Transportation Software Solutions Industry Overview

The competitive rivalry among the players in the market is high due to the presence of some key players like SAP SE, Cognizant, Accenture PLC, Bass Software Ltd, and many more. Continuous investments in research and development have thus allowed the companies to innovate their products and introduce new products in the market, which, in turn, has allowed them to gain a competitive advantage over other players.

- March 2023 - Union Minister for Shipping Ports and Waterways and Ayush virtually introduced the Real-time Performance Monitoring Dashboard of MoPSW 'Sagar Manthan.' It is primarily a digital platform with all the integrated data related to the ministry and other subsidiaries. This dashboard would transform the workings of various departments by improving well-coordinated real-time information.

- February 2023 - IBS software acquired Accenture freight and logistics software. Acquisition to help expand IBS footprint in the freight supply chain, accelerating digital transformation & innovation. AFLS provides technology platforms to help airline and ocean transportation companies manage freight operations and grow through digital transformation and innovation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain / Supply Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Buyers/Consumers

- 4.3.2 Bargaining Power of Suppliers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Volume of Cargo

- 5.1.2 Establishment of New Ports in Developing Countries

- 5.2 Market Restraints

- 5.2.1 Stringent Emission Laws and Policies

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.1.3 Hybrid

- 6.2 By End-user Vertical

- 6.2.1 Retail

- 6.2.2 Oil and Gas

- 6.2.3 Manufacturing and Industrial

- 6.2.4 Aerospace and Defense

- 6.2.5 Chemical

- 6.2.6 Construction

- 6.2.7 Healthcare

- 6.2.8 Food and Beverage

- 6.2.9 Other End-user Verticals

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 SAP SE

- 7.1.2 Cognizant Technology Solutions Corp

- 7.1.3 Accenture PLC

- 7.1.4 Veson Nautical Corporation

- 7.1.5 DNV GL (GL Maritime Software GmbH

- 7.1.6 Aljex Software Inc.

- 7.1.7 Descartes Systems Group

- 7.1.8 HighJump Software Inc.

- 7.1.9 Trans-i Technologies Inc.

- 7.1.10 Bass Software Ltd.