|

市場調査レポート

商品コード

1639437

産業用ロボティクス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Industrial Robotics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 産業用ロボティクス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

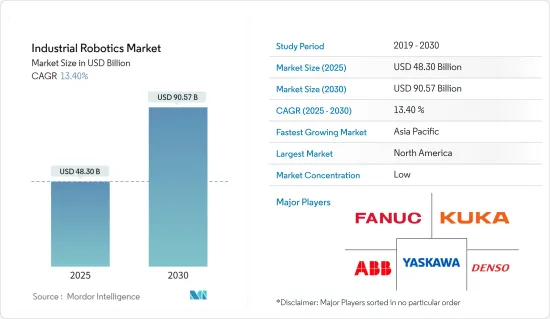

産業用ロボティクスの市場規模は2025年に483億米ドルと推計され、予測期間中(2025-2030年)のCAGRは13.4%で、2030年には905億7,000万米ドルに達すると予測されます。

主なハイライト

- 産業用ロボットは、製造業の産業オートメーションにおいて重要な役割を担っており、産業における多くの中核業務はロボットによって管理されています。各地域の経済成長に伴い、eコマース、エレクトロニクス、自動車産業などが増加しています。

- IoTの普及率の上昇と各地域でのロボットへの投資は、市場の成長に大きく寄与しています。例えば、「メイド・イン・チャイナ2025」の発表は、品質重視とイノベーション主導の製造に移行することで、中国産業を幅広くアップグレードすることを目的としていました。

- 最新の産業革命であるインダストリー4.0は、協働ロボットやAI対応ロボットなどの新技術の開発に拍車をかけ、産業界がロボットを使って多くの工程を合理化し、効率を高め、ミスをなくすことを可能にしました。職場の安全性が高まり、生産能力が向上したことで、産業界はロボットシステムへの投資にさらに拍車をかけています。

- 協働ロボットは、2025年にはロボット販売総額の34%を占めると推定されており(国際ロボット連盟(IFR)調べ)、プラスチック、食品・消費財、半導体・エレクトロニクス、ライフサイエンス、製薬などの産業で産業用ロボットの普及が進むと予想されます。また、フォックスコンのロボットによるアップル社の工場での自動化も注目されます。半導体業界のIC鋳造は、現在の市場需要に影響を与えている採用企業のひとつです。

- 市場を牽引する主な要因としては、(製造プロセスにおいてエンド・ツー・エンドで適切な可視性を必要とする)高品質製品に対する需要の高まり、省エネルギーの必要性、職場の安全性への注目の高まりなどが挙げられます。北米の産業用ロボット販売を監視しているA3(Association for Advancing Automation)によると、製造施設の持続的な増加に加えて、技術の進歩もこの市場を牽引すると予想されています。企業が2022年に発注するロボットは4万4,196台で、2021年より11%多いです。

産業用ロボティクス市場の動向

自動車産業が大きなシェアを占める

- 過去50年間、自動車産業はさまざまな製造工程の組み立てラインでロボットを使用してきました。現在、自動車メーカーはより多くの工程でロボットの利用を模索しています。このような生産ラインにとって、ロボットはより効率的で柔軟性があり、正確で信頼できます。この技術により、自動車産業は最も重要なロボット・ユーザーの1つであり続け、世界的に最も自動化されたサプライ・チェーンの1つとなっています。

- さらに、自動車製造プロセスにおける自動化の採用の拡大、AIとデジタル化の関与が、自動車セクターにおける産業用ロボットの需要を増加させる主な要因となっています。

- 今日の自動車産業では、急速な変化に対応するため、ロボット技術の進歩が加速しています。ロボットソリューションのシミュレーションと仮想試運転は、現在の自動車産業におけるOEM、新興企業、サプライヤーにとって、工場自動化のメリットを最大限に活用することになります。

- 例えば、欧州第2位の自動車メーカーであるPSAグループは、ユニバーサルロボットの協働ロボットUR10で欧州の製造拠点を近代化しています。UBSによると、2025年には欧州で約63億台の電気自動車が販売されると予測されています。

- 自動車製造の業界情勢の変化に対応するため、業界の多くの企業が産業用ロボットを導入しています。例えば、2022年1月、HASCOとしてビジネスを展開する華宇汽車系統有限公司とABBグループは、「次世代のスマート・マニュファクチャリングを推進する」ために、これまでの関係を基に合弁会社を設立したと発表しました。両社は、この合弁事業により、中国の顧客に利益をもたらす自動化ソリューションでHASCOの主導的地位をさらに発展させることができると主張しています。

- さらに、世界的に成長する自動車部門は、自動車部品の溶接、パレタイジング、部品挿入、ピック&ペールアプリケーション、および他の多くの用途のための産業用ロボットの成長をサポートしています。さらに2022年7月、ヤマハモーターロボティクスはMotek 2022でアドバンスト・オートメーション向けの最新ロボットを展示すると発表しました。同社はスカラロボット、直交ロボット、単軸ロボット、LCMR200リニアコンベアモジュールのデモを行い、その速度、精度、柔軟性を強調します。

北米が大きな市場シェアを占める

- この地域の政府も、ロボティクス市場における最新技術の開拓を支援するイニシアチブを取ることで、ロボット工学の導入を奨励しています。例えば、米国連邦政府は、国産ロボットの製造能力を強化し、この分野での研究活動を奨励するため、国家ロボット工学構想(NRI)プログラムを開始しました。

- 2022年2月、米国鉄鋼とロボット工学・AIスタジオのカーネギー鋳造は、戦略的投資と提携を発表しました。ピッツバーグを拠点とする2つの新興企業は、高度なロボット工学と人工知能を活用した産業オートメーションの加速と拡大のために協力します。カーネギー鋳造は今回の資金調達により、高度製造、産業用ロボット、統合システム、自律型モビリティ、音声分析などの分野におけるロボティクスとAI技術の産業オートメーション・ポートフォリオを販売し、規模を拡大します。

- 2022年3月、キノバ・ロボティクスはカナダ初の産業用協働ロボット、リンク6を発表しました。リンク6はカナダ初の産業用協働ロボットで、製品の品質と一貫性を高めながら日々の生産性を向上させる自動化ソリューションを備えています。リンク6ロボットアームは、経験豊富な産業用インテグレーターや、特にロボットの専門知識を持たないオペレーターなど、あらゆるユーザーを念頭に開発・構築されており、長いリーチと高速動作により、迅速なサイクルタイムを実現します。Kinovaのリンク6コントローラーは、市場で最も高い処理能力とメモリー容量を備えています。また、オプションのGPUにも対応しており、コントローラをコンパクトに保ちながら、将来のAIソリューションに対応することができます。

- Association for Advancing Automation(A3)によると、北米の企業が2021年第2四半期に発注したロボットは98億5,300万台で、2020年に比べ5,196台と大幅に増加し、新たな雇用機会につながっています。さらに、Robotic Industries Association(RIA)によると、産業用ロボットの年初来の増加の最も重大な要因は、自動車OEMがプロセスオートメーション用に購入したユニットが83%増加したことです。

産業用ロボティクス産業の概要

産業用ロボティクス市場は非常に細分化されています。インダストリー4.0は、各地域でデジタル化への取り組みが進んでおり、産業用ロボット市場に有利な機会をもたらしています。時折開催されるロボット見本市の数を考慮すると、透明度は高いです。全体として、既存プレイヤー間の競争企業間の敵対関係は高いです。イノベーションに焦点を当てた、大企業と新興企業の買収や提携が予測されます。市場の主要企業としては、ABBと安川電機が挙げられます。この分野の主な発展には以下のようなものがある:

- 2024年5月:産業用ロボットメーカーのABBは、Automate 2024で最新のモジュール式大型ロボットを発表しました。これらのロボットアームは、先に発表されたIRB 5710-5720およびIRB 6710-6740モデルと合わせて、現在46のバリエーションがラインナップされています。これらのバリエーションは、70~620キログラム(約150~1,350ポンド)の可搬重量を管理することができます。

- 2024年3月Mobile Industrial Robotsは、最新製品である自律型パレットジャッキMiR1200を発表しました。高度な3Dビジョン技術を搭載したMiR1200パレットジャッキは、労働集約的なマテリアルハンドリングを合理化するために設計されています。このロボットは動的に経路を適応させることができ、床上のゆるい物体や頭上の障害物などの障害物がある場合でもナビゲーションを保証します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- 労働安全重視の高まり

- 産業用ロボットの新技術

- 市場抑制要因

- 熟練労働者の不足

第6章 市場セグメンテーション

- ロボットタイプ別

- 多関節ロボット

- リニアロボット

- 円筒型ロボット

- パラレルロボット

- スカラロボット

- その他のロボット

- エンドユーザー産業別

- 自動車

- 化学・製造

- 建設

- 電気・電子

- 飲食品

- 機械・金属

- 製薬

- その他エンドユーザー産業(ゴム、光学)

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- アジア

- 日本

- 中国

- インド

- 韓国

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- ABB Ltd.

- Yaskawa Electric Corporation

- Denso Corporation

- Fanuc Corporation

- KUKA AG

- Kawasaki Robotics

- Toshiba Corporation

- Panasonic Corporation

- Staubli Mechatronics Company

- Yamaha Robotics

- Epson Robots

- Comau SPA

- Adept Technologies

- Nachi Robotic Systems Inc.

第8章 投資分析

第9章 市場の将来展望

The Industrial Robotics Market size is estimated at USD 48.30 billion in 2025, and is expected to reach USD 90.57 billion by 2030, at a CAGR of 13.4% during the forecast period (2025-2030).

Key Highlights

- Industrial robots play a crucial role in manufacturing industrial automation, with many core operations in industries being managed by robots. With economic growth across regions, e-commerce, electronics, and the automotive industry, among others, have increased.

- Rising penetration of the IoT and investments in robotics across regions have been major contributors to the market's growth. For instance, the 'Made in China 2025' announcement aimed to broadly upgrade the Chinese industry by moving toward quality-focused and innovation-driven manufacturing.

- Industry 4.0, the newest industrial revolution, has fueled the development of new technologies, like collaborative robots, AI-enabled robots, etc., and has enabled industries to use robots to streamline many processes, increase efficiency, and eliminate errors. Increased workplace safety and improved production capabilities have further driven industries to invest in robotic systems.

- Owing to collaborative robots, which are estimated to account for 34% of the total robot sales in 2025 (according to the International Federation of Robots (IFR), the penetration of industrial robots is expected to rise across industries, such as plastics, food and consumer goods, semiconductors and electronics, life sciences, and pharmaceuticals. Another notable factory automation is expected at Apple's factories through Foxconn's robots. Semiconductor industry IC foundries have been among the adopters that have impacted the current market demands.

- Some of the major factors driving the market include rising demand for high-quality products (which need proper end-to-end visibility in the manufacturing process), the need for energy conservation, and rising focus on workplace safety. Incremental advancements in technology, coupled with a sustained increase in the development of manufacturing facilities, are also expected to drive this market, for instance, According to the Association for Advancing Automation (A3), which monitors industrial robot sales in North America. Companies ordered 44,196 robots in 2022, 11% more than in 2021.

Industrial Robotics Market Trends

Automotive Industry to Hold Major Share

- For the past 50 years, the automotive industry has used robots in its assembly lines for various manufacturing processes. Currently, automakers are exploring the use of robotics in more procedures. Robots are more efficient, flexible, accurate, and dependable for such production lines. This technology enables the automotive industry to remain one of the most significant robot users and possess one of the most automated supply chains globally.

- Furthermore, the growing adoption of automation in the automotive manufacturing process and the involvement of AI and digitalization are the primary factors increasing the demand for industrial robots in the automotive sector.

- In today's automotive industry, the advancement of robotics technology has accelerated to keep up with the rapid changes in the automotive industry. A robotics solution simulation and virtual commissioning will utilize the maximum benefits of factory automation for OEMs, startups, and suppliers in the present automotive industry.

- For instance, For instance, Europe's second-largest car manufacturer, PSA Group, modernizes its European manufacturing sites with Universal Robots' UR10 collaborative robots. According to UBS, around 6.3 billion electric vehicles are forecast to be sold in Europe in 2025.

- To cater to the changing landscape of automotive manufacturing, many players in the industry are adopting industrial robots. For instance, in January 2022, Huayu Automotive Systems Co., which does business as HASCO, and ABB Group announced that they have created a joint venture building on their existing relationship "to drive the next generation of smart manufacturing." The companies claimed that the joint venture would enable them to further develop HASCO's leading position with automated solutions that benefit customers in China.

- Further, the growing automotive sector worldwide supports the growth of industrial robotics for welding car parts, palletizing, part insertion, pick-and-pale applications, and many other uses. Moreover, in July 2022, Yamaha Motor Robotics announced to showcase of its latest robots for Advanced Automation at Motek 2022. The company will demonstrate SCARA, cartesian and single-axis robots, and the LCMR200 linear conveyor module, highlighting their speed, accuracy, and flexibility.

North America to Hold a Significant Market Share

- The government in the region is also encouraging the adoption of robotics by taking initiatives to support the development of modern technologies in the robotics market. For instance, the US federal government has commenced the National Robotics Initiative (NRI) program to bolster the capabilities of building domestic robots and encourage research activities in the field.

- In February 2022, United States Steel and Carnegie Foundry, a robotics and AI studio, announced a strategic investment and relationship. The two Pittsburgh-based startups will collaborate to accelerate and expand industrial automation powered by advanced robotics and artificial intelligence. Carnegie Foundry will use this funding to market and scale its industrial automation portfolio of robotics and AI technologies in advanced manufacturing, industrial robots, integrated systems, autonomous mobility, speech analytics, and other areas.

- In March 2022, Kinova Robotics introduced Link 6, Canada's first industrial collaborative robot. Link 6 is Canada's first industrial collaborative robot, with automation solutions that increase daily productivity while enhancing product quality and consistency. The Link 6 robotic arm is developed and constructed with any user in mind, both for experienced industrial integrators and operators with no particular robotic expertise, achieving quick cycle times through longer reach and fast movements. The Link 6 controller from Kinova has the market's most processing power and memory capacity. It supports an optional GPU, making it ready for use with future AI solutions while keeping the controller compact.

- Association for Advancing Automation (A3), companies in North America ordered 9,853 million robots in the second quarter of 2021, which is a significant increase compared to 2020, with 5,196 sales, leading to new job opportunities. Further, according to Robotic Industries Association (RIA), the most critical driver of the year-to-date increase in industrial robots was an 83% growth in units purchased by automotive OEMs for process automation.

Industrial Robotics Industry Overview

The industrial robotics market is highly fragmented. Industry 4.0, with digitalization initiatives across regions, provides lucrative opportunities in the industrial robots market. The degree of transparency is high, considering the number of robotic trade exhibits across conducted areas occasionally. Overall, the competitive rivalry among existing players is high. The acquisitions and collaboration of large companies with startups are predicted, focusing on innovation. A few major players in the market are ABB and Yaskawa. Some of the key developments in the area are:

- May 2024: ABB, an industrial robot manufacturer, unveiled its latest modular large robots at Automate 2024. These robot arms, in conjunction with the previously released IRB 5710-5720 and IRB 6710-6740 models, now present a lineup of 46 variants. These variants are capable of managing payloads ranging from 70 to 620 kilograms (approximately 150 to 1,350 pounds).

- March 2024: Mobile Industrial Robots has unveiled its latest product, the MiR1200 autonomous pallet jack. Equipped with advanced 3D vision technology, the MiR1200 Pallet Jack is designed to streamline labor-intensive materials handling. This robot can adapt its route dynamically, ensuring navigation even in the presence of obstacles, such as loose objects on the floor or overhead hindrances.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Emphasis on Workplace Safety

- 5.1.2 Emerging Technologies in Industrial Robots

- 5.2 Market Restraints

- 5.2.1 Lack of Skilled Workforce

6 MARKET SEGMENTATION

- 6.1 By Type of Robot

- 6.1.1 Articulated Robots

- 6.1.2 Linear Robots

- 6.1.3 Cylindrical Robots

- 6.1.4 Parallel Robots

- 6.1.5 SCARA Robots

- 6.1.6 Other Types of Robot

- 6.2 By End-user Industry

- 6.2.1 Automotive

- 6.2.2 Chemical and Manufacturing

- 6.2.3 Construction

- 6.2.4 Electrical and Electronics

- 6.2.5 Food and Beverage

- 6.2.6 Machinery and Metal

- 6.2.7 Pharmaceutical

- 6.2.8 Other End-user Industries (Rubber, Optics)

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 France

- 6.3.2.3 Germany

- 6.3.3 Asia

- 6.3.3.1 Japan

- 6.3.3.2 China

- 6.3.3.3 India

- 6.3.3.4 South Korea

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Ltd.

- 7.1.2 Yaskawa Electric Corporation

- 7.1.3 Denso Corporation

- 7.1.4 Fanuc Corporation

- 7.1.5 KUKA AG

- 7.1.6 Kawasaki Robotics

- 7.1.7 Toshiba Corporation

- 7.1.8 Panasonic Corporation

- 7.1.9 Staubli Mechatronics Company

- 7.1.10 Yamaha Robotics

- 7.1.11 Epson Robots

- 7.1.12 Comau SPA

- 7.1.13 Adept Technologies

- 7.1.14 Nachi Robotic Systems Inc.