|

市場調査レポート

商品コード

1444779

マイクロフルイディクスの世界市場: 市場シェア分析、産業動向・統計、成長予測(2024~2029年)Microfluidics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| マイクロフルイディクスの世界市場: 市場シェア分析、産業動向・統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 118 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

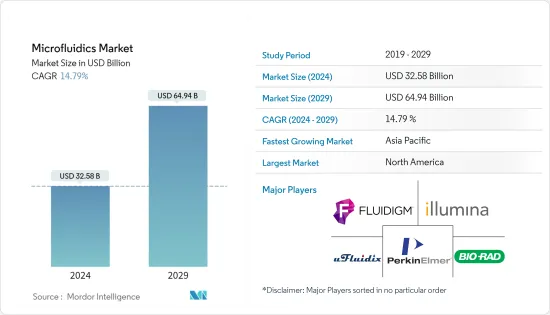

世界のマイクロフルイディクスの市場規模は、2024年に325億8,000万米ドルに達し、2024~2029年の予測期間中にCAGR 14.79%で成長し、2029年までに649億4,000万米ドルに達すると予測されております。

COVID-19のパンデミックはヘルスケア市場に影響を与えました。パンデミックの初期段階では、企業は慢性疾患患者の遠隔監視に使用されるウェアラブルやその他のモバイルデバイス用のさまざまなセンサーデバイスや機器の開発に取り組んでいました。人口におけるCOVID-19の感染者数の多さにより、多数のサンプルを迅速かつ効果的に検査するためのポイントオブケア診断の需要が高まっています。これにより、最終的には多数のマイクロフルイディクス技術の開発が促進され、市場の成長に影響を及ぼしました。たとえば、2022年5月にLife Journalに掲載された記事によると、SARS-CoV-2抗体の検出には、マイクロ流体DA-D4(二重抗原ブリッジングイムノアッセイ法、全サブクラスとアイソタイプを含む全抗体を検出)や、サンドイッチ/競合免疫センサーに基づく方法など、さまざまな技術が用いられています。同じ情報源によると、古典的な多層ソフトリソグラフィー技術を備えた半自動マイクロフルイディクスプラットフォームは、単一デバイスで50個のサンプルを実行しながら、4つのSARS-CoV-2抗原に対する抗体を検出できます。ポイントオブケア診断検査メーカーと高速小型マイクロフルイディクス技術にとって新たな重要な機会が開かれており、予測期間中の市場の成長を牽引すると予想されます。

市場の成長を促進する特定の要因としては、ポイントオブケア検査の需要の増加、慢性疾患の発生率の増加、分析の所要時間の短縮、デバイスの携帯性の向上などが挙げられます。

感染症やがん、糖尿病、心血管疾患などの慢性疾患の負担の増加により、ポイントオブケア検査の需要が増加しており、予測期間中にマイクロフルイディクス市場の需要が促進されると予想されます。たとえば、IDFが発表した2022年の統計によると、ドイツでは2021年に約610万人が糖尿病を抱えており、2030年までに650万人に達すると予測されています。したがって、糖尿病に苦しむ人の数は増加すると予想されています。マイクロフルイディクスエレクトロスプレー技術を使用した糖尿病治療には、B細胞をカプセル化した新規の多孔質マイクロカプセルが必要となります。

2021年1月にPLOS Oneに掲載された研究によると、フランスでは2025年までに約280万人が慢性閉塞性肺疾患(COPD)に罹患すると予想されています。これにより、マイクロフルイディクスチップと少量の血液サンプルを使用したCOPD検査の需要が増加し、市場の成長を促進すると予想されます。 Dementia Australiaが発表した2022年の統計によると、2022年にオーストラリアでは48万7,500人のオーストラリア人が認知症を抱えて生活しており、この数は2058年までに約110万人に達すると予測されています。したがって、対象人口の間で認知症の負担が増大しているため、効果的な認知症対策の必要性が高まっています。創薬、スクリーニング方法、毒物学研究。これにより、体液隔離の維持とともに、神経突起、グリア細胞、内皮細胞、骨格筋細胞の増殖に使用できるマイクロフルイディクスシステムの需要が高まり、器官形成と疾患の病因を研究する機会が得られます。

マイクロフルイディクス工学の発展は、マイクロフルイディクス工学と組み合わせた診断装置やスマートフォンの費用対効果の高い大量生産プロセスの進化にもつながり、ポイントオブケア検査の展開が可能になります。これにより、マイクロフルイディクスデバイスの応用範囲が広がり、今後も拡大すると予想されます。

新興企業は、マイクロフルイディクス技術とデバイスの開発に重点を置き、さまざまな戦略的イニシアチブの採用を増やしており、予測期間中に市場の成長を推進すると予想されます。たとえば、2021年6月、特許取得済みのピコドロップレット技術に裏打ちされた単一細胞分析システムを商品化する企業であるSphere Fluidicsと、組織工学および単一細胞技術向けソリューションのパイオニアであるClexBioは、生体適合性のあるCYTRIXマイクロフルイディクスハイドロゲルキットを発売しました。 2021年1月、LumiraDxは日本とブラジルでSARS-CoV-2抗原を検出するためのマイクロフルイディクス免疫蛍光アッセイを承認しました。

ただし、マイクロフルイディクス技術と既存のワークフローの統合、および価格の高さによる新興諸国での普及の低さは、予測期間中の市場の成長を妨げると予想されます。

マイクロフルイディクス市場の動向

ポイントオブケア診断セグメントは、予測期間中に高いCAGRで推移すると予想されます

ポイントオブケア診断セグメントは、慢性疾患の有病率の上昇、ポイントオブケア検査装置の需要の増加、技術進歩の高まりなどの要因により、予測期間中にマイクロフルイディクス市場が大幅に成長すると予想されています。たとえば、GLOBOCAN 2020によると、2020年に世界で新たにがんの症例が1,928万2,789件あり、その数は2040年までに2,888万7,940件に増加すると予想されています。したがって、がん症例の予想される増加により、ポイントオブケアの需要が増加すると予想されます。診断、市場の成長を推進します。

2021年にFrontiers in Bioengineering and Biotechnologyに掲載された記事によると、リアルタイムPCR検査であるRevogeneは、マイクロフルイディクスカートリッジを使用することで、C.ディフィシル、連鎖球菌Bおよび連鎖球菌Aを約2分で検出できます。これにより、ポイントオブケア検査におけるマイクロフルイディクス工学の需要が増加し、この分野の成長が促進されると予想されます。

ポイントオブケア診断(POC)は、ヘルスケア、特に病気の診断に不可欠です。 POC診断は、患者の近くで使用される他の従来の方法と比較して病気を迅速に検出できるため、病気の状態のより適切な診断、監視、管理につながり、ヘルスケア専門家が患者に関して迅速な医学的決定を下すのに役立ちます。マイクロフルイディクス技術はポイントオブケア診断に適しており、COVID-19のパンデミック下で役立つ迅速かつ手頃な価格のポイントオブケア診断ツールを提供する可能性があり、このことがこの分野の成長を加速させました。

このデバイスに関連する主な利点は、迅速かつ正確な応答、費用対効果、および携帯性です。ポイントオブケア診断では、複雑なサンプル中の複数の分析物を検査できるチップベースのデバイスを開発する研究が行われています。したがって、マイクロフルイディクス工学の統合は、ポイントオブケア診断の即興化に貢献すると考えられています。

したがって、POC診断の範囲の拡大により、マイクロフルイディクス工学が大幅に成長し、新しいデバイスの開発が可能になる可能性があります。

北米が予測期間中に研究された市場を独占すると予想される

北米はマイクロフルイディクス市場を独占しており、確立されたヘルスケア制度や一般人口の間での新しい治療法の採用の増加、国民の間での感染症や慢性疾患の有病率の増加などの要因により、予測期間を通じて主要なシェアを維持すると予想されています。

マイクロフルイディクス工学は、多額の研究開発予算が投入され、この地域で大きく成長している分野です。たとえば、2021年 9月の米国製薬研究および製造業者のデータ更新によると、PhRMA会員企業は、新しい治療法と治癒法の探索に1兆1,000億米ドル以上を投資しており、その中には2021年の1,023億米ドルが含まれます。予測期間中のセグメントの成長。ポイントオブケア診断では、分子診断、感染症、慢性疾患などのさまざまな用途にマイクロフルイディクス技術が使用されており、使いやすく迅速な統合マイクロフルイディクスデバイスの製造を目指しています。

2020年8月、イリノイ大学アーバナシャンペーン校の研究者らは、新型COVID-19分子検査のプロトタイプと、サンプルを研究室に送る必要のない、スマートフォンで結果を読み取るためのポータブル機器をデモンストレーションしました。

この地域の主要な市場プレーヤーによる製品発売の増加により、市場の成長が促進されます。たとえば、2021年 1月にLexaGeneは、米国で緊急使用許可(EUA)を取得した後、MiQLabシステムを研究専用からSARS-CoV-2ウイルスを検出するためのPOC使用まで開始しました。 2021年 10月、LumiraDxは、LumiraDx SARS-CoV-2およびインフルエンザ A/B検査を緊急使用許可(EUA)のために食品医薬品局(FDA)に提出しました。マイクロフルイディクス免疫蛍光アッセイは、インフルエンザやCOVID-19が疑われる患者の感染を迅速に検証し、診断や臨床上の意思決定に役立てることができます。

したがって、上記の要因により、北米のマイクロフルイディクス市場は健全な速度で成長すると予想されます。

マイクロフルイディクス産業の概要

マイクロフルイディクス市場はかなり競争が激しく、市場シェアの点では、現在市場を独占している大手企業はほとんどありません。しかし、技術の進歩と製品の革新に伴い、中規模から中小企業は手頃な価格で新技術を導入することで市場での存在感を高めています。 uFluidix、Bio-Rad Laboratories Inc.、Fluidigm Corporation、Illumina Inc.、PerkinElmer Inc.などの企業が市場のかなりのシェアを占めています。主要企業は、世界市場での地位を確保するために、買収、提携、先進製品の発売など、さまざまな戦略的提携に関与してきました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 研究の前提条件と市場の定義

- 研究範囲

第2章 研究手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- ポイントオブケア検査の需要の増加

- 慢性疾患の発生率の増加

- 分析の所要時間の短縮とデバイスの移植性の向上

- 市場抑制要因

- マイクロフルイディクス技術と既存のワークフローの統合

- 価格が高いため、新興諸国での低い普及率

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品タイプ別

- マイクロフルイディクスベースデバイス

- マイクロフルイディクスコンポーネント

- マイクロフルイディクスチップ

- マイクロポンプ

- マイクロニードル

- その他の製品タイプ

- 用途別

- ドラッグデリバリー

- ポイントオブケア診断

- 製薬・バイオテクノロジー研究

- ハイスループットスクリーニング

- プロテオミクス

- ゲノミクス

- 細胞ベースアッセイ

- キャピラリー電気泳動

- その他の製薬・バイオテクノロジー研究

- 臨床診断

- その他の用途

- 素材別

- ポリマー

- シリコーン

- ガラス

- その他の素材

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- フランス

- 英国

- ドイツ

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- UFluidix

- Bio-Rad Laboratories Inc.

- Emulate Inc.

- Dolomite Microfluidics(Blacktrace Holdings Ltd)

- Sphere Fluidics Limited

- FluIdigm Corporation

- Illumina Inc.

- Micronit Microfluidics

- PerkinElmer Inc.

- Hesperos Inc.

- ZEON CORPORATION

- Bartels-Mikrotechnik

- Agilent Technologies Inc.

- Quidel Corporation

- Fluigent SA

- Nanomix Inc.

- Biosurfit SA

第7章 市場機会と将来の動向

The Microfluidics Market size is estimated at USD 32.58 billion in 2024, and is expected to reach USD 64.94 billion by 2029, growing at a CAGR of 14.79% during the forecast period (2024-2029).

The COVID-19 pandemic had an impact on the healthcare market. During the initial phase of the pandemic, companies were engaged in developing various sensor devices and equipment for wearables and other mobile devices that are used for remote monitoring of chronically ill patients. The high number of COVID-19 cases among the population has increased the demand for point-of-care diagnostics for rapid and effective testing of a large number of samples. This has ultimately increased the development of numerous microfluidic technologies, which has impacted the market's growth. For instance, according to an article published in the Life Journal in May 2022, different techniques are used to detect SARS-CoV-2 antibodies, such as the microfluidic DA-D4 (double-antigen bridging immunoassay technique, which detects total antibodies including all subclasses and isotypes) and sandwich/competitive immune-sensors based methods that help run three samples per device and provide accurate results. As per the same source, the semi-automated microfluidic platform with the classic multilayer soft-lithography technique can detect antibodies against four SARS-CoV-2 antigens while running 50 samples in a single device. New significant opportunities are opening for point-of-care diagnostic test-makers and rapid, miniaturized microfluidic technologies, which are expected to drive the market's growth over the forecast period.

Certain factors propelling the market's growth are the increasing demand for point-of-care testing, rising incidences of chronic diseases, the faster turn-around time for analysis, and improved portability of devices.

The rising burden of infectious diseases and chronic diseases such as cancer, diabetes, cardiovascular diseases, and others increases the demand for point-of-care testing, which is expected to propel the demand for the microfluidics market over the forecast period. For instance, according to the 2022 statistics published by IDF, in Germany, about 6.1 million people were living with diabetes in 2021, which is projected to reach 6.5 million by 2030. Thus, the expected increase in the number of people suffering from diabetes raises the need for novel porous microcapsules encapsulating B cells for diabetes treatment using microfluidic electrospray technology.

A study published in PLOS One in January 2021 stated that about 2.8 million people are expected to have the chronic obstructive pulmonary disease (COPD) by 2025 in France. This is anticipated to increase the demand for testing for COPD using microfluidic chips and small samples of blood, hence boosting the market's growth. According to the 2022 statistics published by Dementia Australia, 487,500 Australians are living with dementia in Australia in 2022, and this number is projected to reach about 1.1 million by 2058. Thus, the increasing burden of dementia among the target population raises the need for effective drug discovery, screening methods, and toxicology studies. This increases the demand for microfluidics systems that can be used to grow neurites, glial cells, endothelial cells, and skeletal muscle cells, along with the maintenance of fluid isolation, and provides an opportunity to investigate organogenesis and disease etiology.

The developments in microfluidics are also leading to the evolution of a cost-effective mass-production process of diagnostic devices and smartphones being paired with microfluidics, thus enabling the deployment of point-of-care testing. This has widened the application of microfluidic devices and is expected to expand.

The rising company focus on developing microfluidics technologies and devices and increasing adoption of various strategic initiatives are expected to drive the market's growth over the forecast period. For instance, in June 2021, Sphere Fluidics, a company commercializing single-cell analysis systems underpinned by its patented picodroplet technology, and ClexBio, a pioneer in solutions for tissue engineering and single-cell techniques, launched the biocompatible CYTRIX Microfluidic Hydrogel Kit. In January 2021, LumiraDx approved a microfluidic immunofluorescence assay to detect SARS-CoV-2 antigens in Japan and Brazil.

However, the integration of microfluidics technology with existing workflows and the low adoption in developing countries due to high prices are expected to hinder the market's growth over the forecast period.

Microfluidics Market Trends

The Point-of-Care Diagnostics Segment is Expected to Register a High CAGR During the Forecast Period

The point-of-care diagnostics segment is expected to witness significant growth in the microfluidics market over the forecast period due to factors such as the rising prevalence of chronic diseases, increasing demand for point-of-care testing devices, and rising technological advancements. For instance, according to GLOBOCAN 2020, there were 19,282,789 new cancer cases worldwide in 2020, with the number expected to rise to 28,887,940 cases by 2040. Thus, an expected increase in cancer cases is anticipated to increase the demand for point-of-care diagnostics, propelling the market's growth.

According to an article published in Frontiers in Bioengineering and Biotechnology in 2021, Revogene, a real-time PCR test, can detect C. difficile, Strep B, and Streptococcus A in about two minutes by using the microfluidic cartridge. This is expected to increase the demand for microfluidics in point-of-care testing, boosting the segment's growth.

Point-of-care diagnostics (POC) is integral to healthcare, especially in disease diagnosis. POC diagnostics offers rapid detection of diseases compared to other conventional methods used near the patients, which leads to better diagnosis, monitoring, and management of disease status and helps healthcare professionals make quick medical decisions regarding the patient. Microfluidics technology is well-suited for point-of-care diagnostics and has the potential to offer rapid and affordable point-of-care diagnostic tools to help during the COVID-19 pandemic, which has increased the segment's growth.

The major advantages associated with the devices are rapid and precise response, cost-effectiveness, and portability. Research is being done in point-of-care diagnostics to develop a chip-based device that can examine multiple analytes in complex samples. Hence, the integration of microfluidics is believed to contribute to the improvisation of point-of-care diagnostics.

Therefore, due to the growth in the range of POC diagnostics, there will be a significant growth in microfluidics, which may enable the development of new devices.

North America is Expected to Dominate the Market Studied During the Forecast Period

North America dominates the microfluidics market and is expected to hold the major share over the forecast period due to factors such as the well-established healthcare system and the higher adoption of novel therapeutics among the general population, increasing prevalence of infectious and chronic diseases among the population in the region.

Microfluidics is a vastly growing field in the region with a high budget for R&D. For instance, according to the Pharmaceutical Research and Manufacturers of America data updates from September 2021, PhRMA member companies have invested more than USD 1.1 trillion in the search for new treatments and cures, including USD 102.3 billion in 2021. These are expected to increase the segment's growth during the forecast period. The point-of-care diagnostics uses microfluidic technology for various applications, like molecular diagnostics, infectious diseases, and chronic diseases, which aim to produce integrated microfluidic devices that are easy to use and rapid.

In August 2020, researchers from the University of Illinois at Urbana-Champaign demonstrated a prototype of a rapid COVID-19 molecular test and a portable instrument for reading the results with a smartphone, which does not require sending samples to a lab.

Increasing product launches by key market players in the region boosts the market's growth. For instance, in January 2021, LexaGene launched the MiQLab system from research-only use to POC use to detect the SARS-CoV-2 virus after receiving emergency use authorization (EUA) in the United States. In October 2021, LumiraDx submitted the LumiraDx SARS-CoV-2 & Flu A/B Test to the Food and Drug Administration (FDA) for Emergency Use Authorization (EUA). The microfluidic immunofluorescence assay can quickly verify infection for patients suspected of flu and COVID-19 to aid in diagnosis and clinical decision-making.

Thus, due to the above-mentioned factors, the microfluidics market in North America is expected to grow at a healthy rate.

Microfluidics Industry Overview

The microfluidics market is fairly competitive, and in terms of market share, few major players currently dominate the market. However, with technological advancements and product innovations, mid-size to smaller companies are increasing their market presence by introducing new technologies at affordable prices. Companies like uFluidix, Bio-Rad Laboratories Inc., Fluidigm Corporation, Illumina Inc., and PerkinElmer Inc. hold a substantial share of the market. The key players have been involved in various strategic alliances such as acquisitions, collaborations, and launches of advanced products to secure their positions in the global market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Point-of-care Testing

- 4.2.2 Increasing Incidences of Chronic Diseases

- 4.2.3 Faster Turn-around Time for Analysis and Improved Portability of Devices

- 4.3 Market Restraints

- 4.3.1 Integration of Microfluidics Technology with Existing Workflows

- 4.3.2 Low Adoption in Developing Countries Due to High Prices

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product Type

- 5.1.1 Microfluidic-based Devices

- 5.1.2 Microfluidic Components

- 5.1.2.1 Microfluidic Chips

- 5.1.2.2 Micro Pumps

- 5.1.2.3 Microneedles

- 5.1.2.4 Other Product Types

- 5.2 By Application

- 5.2.1 Drug Delivery

- 5.2.2 Point-of-care Diagnostics

- 5.2.3 Pharmaceutical and Biotechnology Research

- 5.2.3.1 High-throughput Screening

- 5.2.3.2 Proteomics

- 5.2.3.3 Genomics

- 5.2.3.4 Cell-based Assay

- 5.2.3.5 Capillary Electrophoresis

- 5.2.3.6 Other Pharmaceutical and Biotechnology Research

- 5.2.4 Clinical Diagnostics

- 5.2.5 Other Applications

- 5.3 By Material

- 5.3.1 Polymer

- 5.3.2 Silicone

- 5.3.3 Glass

- 5.3.4 Other Materials

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 France

- 5.4.2.2 United Kingdom

- 5.4.2.3 Germany

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 UFluidix

- 6.1.2 Bio-Rad Laboratories Inc.

- 6.1.3 Emulate Inc.

- 6.1.4 Dolomite Microfluidics (Blacktrace Holdings Ltd)

- 6.1.5 Sphere Fluidics Limited

- 6.1.6 FluIdigm Corporation

- 6.1.7 Illumina Inc.

- 6.1.8 Micronit Microfluidics

- 6.1.9 PerkinElmer Inc.

- 6.1.10 Hesperos Inc.

- 6.1.11 ZEON CORPORATION

- 6.1.12 Bartels-Mikrotechnik

- 6.1.13 Agilent Technologies Inc.

- 6.1.14 Quidel Corporation

- 6.1.15 Fluigent SA

- 6.1.16 Nanomix Inc.

- 6.1.17 Biosurfit SA