|

市場調査レポート

商品コード

1640620

非接触決済端末:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Contactless Payment Terminals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 非接触決済端末:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

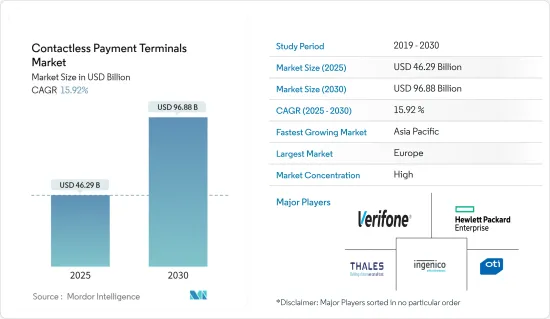

非接触決済端末の市場規模は、2025年に462億9,000万米ドルと予測され、予測期間中(2025-2030年)のCAGRは15.92%で、2030年には968億8,000万米ドルに達すると予測されます。

主なハイライト

- 企業や消費者のデジタル変革傾向の高まりとスマートフォンの普及により、世界の決済・取引の状況は急速に変化しています。スマートフォン、デジタル決済カード、小売POS端末の技術進歩が市場成長の原動力となっています。

- キャッシュレス経済への移行を目指す国が増えつつあるため、消費者のデジタル決済にインセンティブを与えることで、デジタル決済プロバイダーを後押ししています。さらに、世界の非接触型カード取引の拡大が、さまざまなエンドユーザー産業における非接触決済端末の需要を促進しています。

- 非接触型決済は、その利便性と嗜好性から大きな支持を集めています。その結果、さまざまなウェアラブル機器メーカーが近距離無線通信(NFC)技術をほとんどの機器に標準搭載し、財布や財布、携帯電話をいじる必要性をなくすことで利便性を高めています。

- 加えて、スマートフォンを利用した決済方法への世界の消費者の傾倒は、POSシステムでの非接触型決済方法の形で増加しており、そのため、カード・金融サービス・プロバイダーは、自社のカード・ソリューションをスマートフォンで提供するか、サードパーティー・ベンダー経由で提供しています。

- さらに、世界の金融詐欺の増加により、政府の規制機関もここ数年、決済取引の安全確保に取り組んでいます。顧客は安全で信頼性の高いデジタル取引を求めており、安全な決済プロセスを使用する必要性が高まっています。そのため、こうした規制機関はPOS端末の導入にプラスの影響を与えています。世界のモビリティ動向の高まりに伴い、モバイルPOSシステムが人気を集めています。キャッシュレス取引技術の出現により、POSは採用率の増加が見込まれます。

- さらに、技術の進歩が非接触決済端末市場の将来を形成しています。市場開拓ベンダーは、機敏で効率的な決済プラットフォームの開発に注力し、非接触決済の普及と普及率の向上にも取り組んでいます。例えば、昨年2月、デジタル決済のInfibeam Avenues Limited(IAL)は、ハードウェア不要の非接触型モバイルPOS(販売時点情報管理システム)を発表し、決済ソリューションのポートフォリオを拡大すると発表しました。

- COVID-19の大流行中、世界中の消費者は感染から身を守るために人との接触を避ける方法を見つけ始めました。このため、非接触型決済の需要が高まり、非接触型POS端末などさまざまな非接触決済端末の需要が多業種で高まっています。また、パンデミック後も、新興国におけるデジタル決済の普及により、非接触決済端末の需要は急拡大すると予想されます。

非接触決済端末の市場動向

小売業界が主要市場シェアを占める見込み

- 小売業界では非接触決済端末の利用が増加しており、加盟店の販売促進や顧客満足度の向上など、非接触決済端末を導入することで得られるメリットもあることから、市場シェアは高いものと予想されます。小売業者は非接触決済オプションを提供することで、会計プロセスのスピードと効率を高め、よりスムーズで迅速な取引を通じて顧客ロイヤルティを育成しています。

- このセグメントの主な促進要因は、アウトレットと、小売店でのチェックアウトにモバイル・ウォレットを選好することです。モバイルベースのPOS(mPOS)の進化には、タブレットやスマートフォン上の基本的なePOSアプリに接続されたカードリーダーが含まれ、マーチャントのオンボーディングはシンプルである一方、サービスは「従量課金モデル」で提供されます。小売業界では、こうしたケースが非接触決済端末の導入につながる可能性が高いです。

- 市場各社は小売業者向けに革新的でスマートなソリューションを提供しており、小売分野での非接触決済端末の採用を促進すると予想されます。例えば、前年、金融サービスプラットフォームのSquareは、米国内の数百万人の販売者に対し、iPhone向けのTap To Payサービスを開始すると発表しました。また、新たに開始されたiPhoneでのTap to Payは、ハードウェアや追加コストなしにiPhoneから直接非接触型決済を受け付けることを可能にします。

- さらに、小売店や店舗での非接触デビットカードやクレジットカードによる決済の増加は、予測期間中、小売分野における非接触端末の市場需要を促進すると予想されます。例えば、Worldplay社の統計によると、昨年英国で最も利用された決済手段はデビットカードで、POS端末で行われた決済全体の45%と28%をそれぞれ占めています。

欧州が非接触決済端末市場で大きなシェアを占める見込み

- 消費者の習慣の変化、規制状況の開拓、技術革新、COVID-19の流行など、さまざまな理由で決済状況が変化しているため、欧州地域は今後一定期間、大きな市場シェアを占めると予想されます。さらに、さまざまなエンドユーザー産業で非接触決済端末が広く採用され、大きな成長を遂げていることが、今後数年間の市場をさらに牽引します。

- 欧州では、消費者がこの比較的新しい決済方法を日常生活に取り入れるにつれて、決済用のウェアラブルデバイスが普及し続けています。例えば、指輪、ウェアラブルデバイス、ブレスレット、スマートウォッチは、近距離無線通信(NFC)機能を備えています。ウェアラブルには「アクティブ」と「パッシブ」があります。指輪のようなパッシブな腕時計をしていれば、プラスチックカードと同じように、決済端末でPINコードを入力することで承認される取引ができます。スマートウォッチのようなアクティブウォッチを装着している場合は、暗証番号はデバイス自体に挿入され、ワンタップで決済を行うことができます。

- さらに、COVID-19の状況の中、欧州全土で非接触決済が推進され、非接触カードの限度額が大幅に伸びた。同地域では、パンデミック後に非接触型決済に移行する消費者が増えており、これが市場をさらに牽引すると予想されます。

- さらに、同地域の市場ベンダーによる継続的な製品革新が、予測期間中の市場を牽引すると予想されます。例えば、PayPal Holdings Inc.は昨年5月、英国の中小企業向けにTap to Pay with Zettle by PayPalを発表しました。この新機能により、個人販売者や小規模事業者は、追加のハードウェアや手数料なしに、アンドロイド携帯端末で直接非接触対面決済を受け付けることができるようになります。

非接触決済端末産業の概要

非接触決済端末市場は、一部のプレーヤーだけが大きな市場シェアを持つため、統合されています。さらに、消費者の非接触型カードに対する認識向上へのニーズやセキュリティ問題への懸念が、新規参入企業にとって市場参入を困難なものにしています。同市場の主要企業には、Thales Group、OTI、VeriFone Systems Inc.、Hewlett Packard、Ingenico Group SAなどがあります。

- 2023年12月Mastercardが非接触型決済ソリューションを発表し、ナイジェリアの決済事情を一変させる。このソリューションにより、企業はスマートフォンのタップ、リンクによるQRペイ、ペイメントリンクを利用して、迅速かつコスト効率よくカード決済を行えるようになります。非接触型決済は、関係者全員にとって会計をより迅速かつ便利にします。非接触型決済システムを使えば、顧客は現金での支払いや、カードをスワイプして暗証番号を入力する手間を省くことができます。カードを端末や携帯電話にタップすることで、よりスムーズな取引が可能になります。

- 2023年10月SoftpayとDotykackaが協力し、Nexiをアクワイアラーとしてチェコ共和国とスロバキアにタップ・トゥー・フォン決済ソリューションを導入。タップ・トゥ・フォン・テクノロジーのプロバイダーであるソフトペイは、チェコ共和国とスロバキアにおける非接触型決済への需要の高まりに対応するため、多機能POSシステム・ソリューション・プロバイダーであるDotykacka社との戦略的提携を発表しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19が業界に与える影響の評価

第5章 市場力学

- 市場促進要因

- 待ち時間の短縮とレジの迅速化

- 非接触決済に伴う利便性と手軽さ

- 市場抑制要因

- デジタル決済に関するセキュリティ上の懸念

第6章 市場セグメンテーション

- テクノロジー別

- Bluetooth

- 赤外線

- キャリアベース

- Wi-Fi

- その他のテクノロジー

- 決済モード別

- アカウントベース

- クレジットカード/デビットカード

- ストアドバリュー

- スマートカード

- その他の決済モード

- デバイス別

- 統合POS

- mPOS

- PDA

- 無人端末

- 非接触リーダー

- その他のデバイス

- エンドユーザー産業別

- 小売

- 運輸

- 銀行

- 政府機関

- ヘルスケア

- その他のエンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Thales Group

- On Track Innovation LTD.(OTI)

- VeriFone Inc.

- Hewlett Packard Enterprise Development LP

- Ingenico Group SA

- Visiontek Products LLC

- PayPal Holdings Inc.

- Castles Technologies

- ID Tech Solutions

- NEC Corporation

第8章 投資分析

第9章 市場の将来

The Contactless Payment Terminals Market size is estimated at USD 46.29 billion in 2025, and is expected to reach USD 96.88 billion by 2030, at a CAGR of 15.92% during the forecast period (2025-2030).

Key Highlights

- The global landscape of payments and transactions is changing rapidly, owing to the growing enterprises and consumer propensity toward digital transformation and the proliferation of smartphones. Technological advancements in smartphones, digital payment cards, and retail POS terminals fuel market growth.

- More and more countries are moving toward becoming cashless economies, thus encouraging digital payment providers by incentivizing their consumers' digital forms of payments. In addition, growing contactless card transactions worldwide drive the demand for contactless payment terminals in various end-user industries.

- Contactless payments are gaining significant traction due to their convenience and preference. As a result, various wearable device manufacturers are incorporating near-field communication (NFC) technology as a standard into most devices to provide greater convenience by removing the need to fumble with a wallet, purse, or phone.

- In addition, the global consumer inclination toward payment methods involving smartphones is increasing in the form of contactless payment methods at POS systems, owing to which card and financial service providers are either offering their card solutions on smartphones or via third-party vendors.

- Additionally, the rising financial frauds worldwide have influenced government regulatory bodies to secure payment transactions over the past few years. With customers demanding safe and reliable digital transactions, the need for using secure payment processes has increased. Therefore, these regulatory bodies have positively impacted the adoption of POS terminals. With the increasing mobility trends worldwide, mobile POS systems are gaining traction. With the advent of cashless transactional technologies, POS is expected to witness an increase in adoption rates.

- Moreover, technological advancements are shaping the future of the contactless payment terminals market. Market vendors are focusing on developing payment platforms that are agile and efficient and also increase the penetration and reach of contactless payments. For instance, in February last year, digital payments player Infibeam Avenues Limited (IAL) announced to broaden its payment solutions portfolio by launching a no-hardware contactless mobile point of sale (POS), which will facilitate card payment transactions for small vendors through a tap-on-phone technology.

- During the COVID-19 pandemic, consumers worldwide started finding ways to avoid human contact in order to protect themselves from getting affected. Due to this, the demand for contactless payments has increased, boosting the demand for various contactless payment terminals, such as contactless POS terminals, in multiple industries. In addition, even after the pandemic, the demand for contactless payment terminals is expected to grow rapidly, owing to the proliferation of digital payments in emerging economies.

Contactless Payment Terminals Market Trends

Retail Industry is Expected to Hold Major Market Share

- With the increased use of contactless payment terminals in retail, together with benefits arising from placing them on offer like promotion of sales at merchants and improved customer satisfaction, it is expected to have a strong market share. Retailers provide a contactless payment option to enhance the speed and efficiency of the checkout process, fostering customer loyalty through smoother and quicker transactions.

- Point-of-sale terminals (POS) across retail stores and The primary drivers for this segment are outlets and a preference of mobile wallets to check out from retail stores. The evolution of mobile-based POS (mPOS) includes an card reader connected to a basic ePOS app on a tablet or smartphone, and while Merchant onboarding is simple, where the service is delivered on a 'pay-as-you-go model. In the retail sector, these cases are likely to lead to deployment of Contactless Payment Terminals.

- Market players offer innovative and smart solutions for retailers, expected to drive the adoption of contactless payment terminals in the retail segment. For instance, the previous year, Square, a financial services platform, It's announced to its millions of sellers in the United States that it will be launching a Tap To Pay service for iPhone. In addition, the newly launched Tap to Pay on iPhone enables all sizes of vendors Accepting contactless payments directly from their iPhones without any hardware or additional costs is also available as an application in Square Point Of Sale'siOS point of sale applications.

- Moreover, the growth in contactless debit card and credit card transactions in retail stores and outlets is anticipated to drive the market demand for contactless terminals in the retail sector over the forecast period. For example, the most popular payment method in the UK last year was debit cards which accounted for 45 % and 28 % respectively of all payments made at POS terminals according to statistics from Worldplay.

Europe is Expected to Hold Significant Share in the Contactless Payment Terminals Market

- The European region is expected to hold a significant market share over the upcoming period, owing to the changing payment landscape for various reasons: changing consumer habits, regulatory developments, innovation, and the COVID-19 pandemic. Moreover, the broader adoption of contactless payment terminals in different end-user industries is witnessing significant growth, further driving the market in the coming years.

- In Europe, consumers' wearable devices for payments continue to take off as they grate this relatively new payment method into their daily lives. For example, a ring, a wearable device, a bracelet, or a smartwatch, has Near-field Communication (NFC) capabilities. There exists 'active' and 'passive' wearables. The transaction which can be authorized by entering the PIN code on the payment terminal, just as with a plastic card, if you have your passive wristwatch that is like a ring. When you wear an active watch, such as a smartwatch, the PIN is inserted on your device itself and payments can be made using one tap.

- Additionally, amidst the COVID-19 situation, contactless card limits across Europe grew substantially as contactless payments were promoted across the continent. More and more consumers in the region are moving toward contactless payments after the pandemic, which is further expected to drive the market.

- In addition, continuous product innovation by market vendors in the region is expected to drive the market over the forecast period. For instance, in May last year, PayPal Holdings Inc. launched Tap to Pay with Zettle by PayPal for small businesses in the United Kingdom. The new function will enable individual sellers and small businesses to accept contactless in-person payments directly on Android mobile devices without additional hardware and fees.

Contactless Payment Terminals Industry Overview

The contactless payment terminals market is consolidated because only some players have a significant market share. Moreover, consumers' need for more awareness toward contactless cards and concern over security issues make market entry challenging for new players. Some of the key players in the market include Thales Group, OTI, VeriFone Systems Inc., Hewlett Packard, and Ingenico Group SA.

- December 2023: Mastercard leads the charge in transforming Nigeria's payment landscape as it unveils its contactless payment solutions. The solution will empower businesses to accept card payments quickly and cost-effectively, using a tap on the phone, QR Pay by link, and Payment link on their smartphones. Contactless payments make the checkout experience faster and more convenient for all parties involved. With a contactless payment system, customers can skip paying by cash or swiping their cards and inputting their PIN. They can tap the card against the terminal or mobile phone, making transactions smoother.

- October 2023: Softpay and Dotykacka Collaborate to Introduce Tap-to-phone Payment Solution In the Czech Republic and Slovakia utilizing Nexi as Acquirer. Tap-to-phone technology provider SoftPay has announced a strategic partnership with multifunctional POS system solution provider Dotykacka to meet the growing demand for contactless payment acceptance in the Czech Republic and Slovakia.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of COVID-19 impact on the industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Reduction in Queuing Time and Quicker Checkout Time

- 5.1.2 Convenience and Ease Associated with Contactless Payments

- 5.2 Market Restraints

- 5.2.1 Security Concerns Regarding Digital Payment

6 MARKET SEGMENTATION

- 6.1 Technology

- 6.1.1 Bluetooth

- 6.1.2 Infrared

- 6.1.3 Carrier-based

- 6.1.4 Wi-Fi

- 6.1.5 Other Technologies

- 6.2 Payment Mode

- 6.2.1 Account-based

- 6.2.2 Credit/Debit Card

- 6.2.3 Stored Value

- 6.2.4 Smart Card

- 6.2.5 Other Payment Modes

- 6.3 Device

- 6.3.1 Integrated POS

- 6.3.2 mPOS

- 6.3.3 PDA

- 6.3.4 Unattended Terminal

- 6.3.5 Contactless Reader

- 6.3.6 Other Devices

- 6.4 End-user Industry

- 6.4.1 Retail

- 6.4.2 Transportation

- 6.4.3 Banking

- 6.4.4 Government

- 6.4.5 Healthcare

- 6.4.6 Other End-user Industries

- 6.5 Geography

- 6.5.1 North America

- 6.5.1.1 United States

- 6.5.1.2 Canada

- 6.5.2 Europe

- 6.5.2.1 United Kingdom

- 6.5.2.2 Germany

- 6.5.2.3 France

- 6.5.2.4 Rest of Europe

- 6.5.3 Asia Pacific

- 6.5.3.1 China

- 6.5.3.2 Japan

- 6.5.3.3 India

- 6.5.3.4 Rest of Asia- Pacific

- 6.5.4 Latin America

- 6.5.4.1 Brazil

- 6.5.4.2 Argentina

- 6.5.4.3 Mexico

- 6.5.4.4 Rest of Latin America

- 6.5.5 Middle-East and Africa

- 6.5.5.1 United Arab Emirates

- 6.5.5.2 Saudi Arabia

- 6.5.5.3 South Africa

- 6.5.5.4 Rest of Middle-East and Africa

- 6.5.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Thales Group

- 7.1.2 On Track Innovation LTD. (OTI)

- 7.1.3 VeriFone Inc.

- 7.1.4 Hewlett Packard Enterprise Development LP

- 7.1.5 Ingenico Group SA

- 7.1.6 Visiontek Products LLC

- 7.1.7 PayPal Holdings Inc.

- 7.1.8 Castles Technologies

- 7.1.9 ID Tech Solutions

- 7.1.10 NEC Corporation