|

|

市場調査レポート

商品コード

1637897

政府機関向けクラウド-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Government Cloud - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 政府機関向けクラウド-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

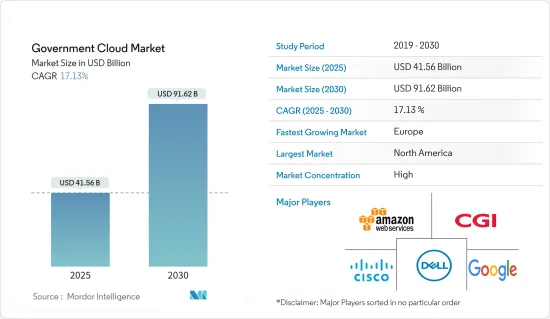

政府機関向けクラウドの市場規模は、2025年に415億6,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは17.13%で、2030年には916億2,000万米ドルに達すると予測されます。

政府機関向けクラウドとは、政府機関向けに明確に構築された仮想化とクラウドコンピューティングシステムを指します。この世界のプログラムは、世界の連邦政府の運用、財務、戦略、ITの目標をサポートするクラウドソリューションの特定と開発を目的としています。

主要ハイライト

- 国勢調査データの増加(人口の絶え間ない増加)、新たな施策やイニシアティブ、他地域との協力、新規事業の急増によるGDPの増加などにより、政府のデータ生成量は増加しています。物理的なハードウェアベースのレガシーシステムは非効率的で、スペースが足りなくなる可能性もあります。そのため、政府のクラウドが必要とされています。

- さらに、政府はクラウド機能を活用することで、より迅速でスケーラブルな市民向けアプリケーションやサービスを生み出すことができます。行政機関は、クラウドネイティブのセキュリティサービスを利用することで、セキュリティの向上、配備の近代化と安全性の確保、クラウドネイティブの自動スケーリング機能による高い耐障害性の実現が可能になります。

- 国や地域の法律、施策、戦術に基づいて、多くの国で政府クラウドが台頭しています。例えば、米国のGovCloudイニシアチブは、特にセキュリティに重点を置き、確立された標準に従ってクラウドコンピューティングシステムの採用を支援しています。このプログラムでは、連邦クラウドコンピューティング戦略やNISTクラウドコンピューティング技術ロードマップなど、いくつかのガイドラインが作成されています。

- 各地域の政府施策が市場の大きな抑制要因となっています。EU、米国、シンガポール、インドの政府は、政府機関のデータを現地のデータセンターに保存することを義務付けています。このような規制は、現地の参入企業には恩恵があるが、世界企業にはさらなる財政的負担を強いています。

- COVID-19の発生により、政府機関がリモートワークアクセスを導入したり、さまざまな国でロックダウンが実施される中でセキュリティ問題に対する意識が高まったりしているため、クラウドベースのサービスやツールの適応が進んでおり、政府機関向けクラウド市場は大きな成長が見込まれています。

政府機関向けクラウド市場の動向

より大きなクラウドストレージ機能へのニーズが成長に寄与

- あらゆる種類のデジタルデータは、世界規模で常に劇的に増加しています。このようなデータを効果的に管理することが世界各国の政府に求められており、イノベーションを促進し、国民の福祉と幸福のための規定を整備する政府の能力が課題となっています。Global Datasphereによると、2025年までに175ゼタバイトのデジタルデータが存在するといいます。政府機関は大量のデータを作成しており、クラウドベースのストレージに対する需要が高まっている

- クラウドストレージのニーズと採用率は、あらゆる政府部門における低コストのデータバックアップ、ストレージ、保護のニーズの高まりや、モバイル技術の利用増加によって生成されるデータを管理する要件の高まりによって、有利になっています。

- さらに、銀行産業ではデータ漏洩の件数が増加しているため、政府系銀行はクラウドストレージを採用しています。クラウドストレージは、銀行自体またはサードパーティが管理・所有する場所にデータを保存できるため、エンドユーザーのセキュリティが向上します。予測される期間中、クラウドストレージの採用が進むと予想されます。

- クラウドソリューション市場の参入企業は現在、大量のデータが生成されるため、データを保存し処理する安価な方法を開発する必要に迫られています。例えば、Tata Communicationsは昨年7月、インド当局が要求する銀行、企業、産業セグメントのデータプライバシー、保護コンプライアンス、セキュリティ基準を満たすためにカスタマイズ型コミュニティクラウドプラットフォーム「IZOTM Financial Cloud」を発表しました。

欧州が最大の成長を遂げる

- 欧州委員会は2012年、初のクラウドコンピューティング戦略を発表しました。その目的は、経済のあらゆる領域でクラウドコンピューティングの利用を加速し、拡大することでした。現在、欧州大陸の企業の36%がクラウドサービスを利用しており2、2020年のクラウド直接投資額は推定540億ユーロ(5兆6,360億米ドル)で、来年には倍増すると予想されています。

- 欧州全域で革新的かつ主権的なエッジとクラウド技術の採用を維持するためには、エッジとクラウド設備の密度を高める必要があるため、欧州市場はクラウドネイティブ5Gを採用し、産業ローカル5Gネットワークを実現することを計画しています。これは、ネットワーク機器プロバイダーの国際競合とIT・通信事業者の世界のフットプリントを活用し、モバイルネットワークを広く分散したクラウドエッジノードの世界ネットワークに変えるためです。

- さらに、欧州連合(EU)は今後7年間で100億ユーロ(104億4,000万米ドル)を投資し、Amazon、Google、Alibabaといった多国籍企業に対抗しうる国内クラウドコンピューティング市場の創設を計画しています。これらの要因は、予測期間中に政府クラウド市場を押し上げると考えられます。

- 遠隔地のエンドポイントからユーザーログ、施策、システムに関する膨大な市民データにアクセスするために、さまざまな産業セグメントで政府機関向けクラウドが広く採用されていることは、この地域全体の市場成長を促進する主要要因の1つです。

政府機関向けクラウド産業概要

官公庁向けクラウド市場は、Microsoft、Oracle NEC、IBM、Googleなどの大手企業が官公庁向けにクラウドソリューションとサービスを提供しており、市場は集中しています。既存ベンダーが強固な骨格を築いているため、同市場への参入障壁は高いです。

テランガナ州政府は、情報技術(IT)ワークロードをクラウドに移行して電子統治計画を加速し、33の部局と289の組織を通じてより迅速で信頼性の高い市民サービスを提供するとともに、高い運用効率とITコストの削減を実現することを決定しました。

2022年1月、Dellの技術は、アプリケーションとデータが存在する場所を問わず一貫したエクスペリエンスを提供するマルチクラウド機能を導入し、ポートフォリオの拡大とともにマルチクラウドへの旅を加速させました。また、デルのインフラのセキュリティ、サポート、予測可能なコストと組み合わせた適切なクラウド環境の選択を支援する新しいオファーとリソースを提供し、開発者の運用(DevOps)のサポートも拡大しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月間のアナリストサポート

目次

第1章 イントロダクション

- 研究の定義と前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターファイブフォース

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 市場力学

第6章 市場促進要因

- 大容量ストレージへのニーズが市場の需要を牽引

- データの透明性へのニーズが市場を拡大

第7章 市場抑制要因

- クラウドコンピューティングのスキルギャップが市場成長の妨げに

第8章 市場セグメンテーション

- 導入モデル別

- パブリッククラウド

- プライベートクラウド

- ハイブリッドクラウド

- デリバリーモード別

- インフラアズ・アサービス

- プラフォーム・アズ・アサービス

- サービス型ソフトウェア

- 用途別

- サーバーとストレージ

- ディザスタリカバリ/データバックアップ

- セキュリティとコンプライアンス

- 分析

- コンテンツ管理

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第9章 競合情勢

- 企業プロファイル

- Amazon Web Services Inc.

- CGI Inc.

- Cisco Systems Inc.

- Dell Inc.

- Google Inc.

- IBM Corporation

- Microsoft Corporation

- NetApp Inc.

- Oracle Corporation

- Rackspace Inc.

- Salesforce.com Inc.

- VMWare Inc.

第10章 投資分析

第11章 市場機会と今後の動向

The Government Cloud Market size is estimated at USD 41.56 billion in 2025, and is expected to reach USD 91.62 billion by 2030, at a CAGR of 17.13% during the forecast period (2025-2030).

Government cloud refers to virtualization and cloud computing systems explicitly created for governmental entities. This global program aims to identify and develop cloud solutions supporting global federal governments' operational, financial, strategic, and IT goals.

Key Highlights

- Government data generation is increasing due to growing census data (constant population growth), new policies and initiatives, cooperation with other regions, and increased GDP due to the mushrooming of new businesses. Physical hardware-based legacy systems are inefficient and may run out of room. Government cloud is therefore required.

- Moreover, governments may create more swiftly and scalable applications and services for citizens by utilizing cloud capabilities. Agencies can use cloud-native security services to improve security, modernize and secure their deployment, and achieve higher resilience through cloud-native auto-scaling capabilities.

- Based on their national and local laws, policies, and tactics, government clouds are emerging in numerous nations. For instance, the GovCloud initiative in the US supports the adoption of cloud computing systems following established standards, with a particular emphasis on security. This program has produced several guidelines, including the Federal Cloud Computing Strategy and the NIST Cloud Computing Technology Roadmap.

- Government policies across different regions have been a major restraining factor for the market. The governments in the EU, US, Singapore, and India have mandated that the data from government agencies be saved in local data centers. These regulations have benefitted the local players but have exerted additional financial strain on global companies.

- With the outbreak of COVID-19, the government cloud market is expected to witness significant growth as cloud-based services and tools are increasingly adapted due to government organizations deploying remote work access and rising awareness of security issues amid lockdowns in various countries.

Government Cloud Market Trends

Need for Greater Cloud Storage Capabilities to witness growth

- Digital data of all kinds are constantly growing dramatically on a global scale. The requirement for governments worldwide to manage such data effectively is posing challenges to their capacity to foster innovation and make provisions for the welfare and happiness of their citizens. According to Global Datasphere, 175 zettabytes of digital data will exist by 2025. Government agencies are producing large amounts of data, increasing the demand for cloud-based storage.

- The need for and adoption rate of cloud storage are favored by the rise in the need for low-cost data backup, storage, and protection across all government sectors, as well as the requirement to manage the data produced by the increased use of mobile technologies.

- Additionally, due to the growing number of data breaches in the banking industry, government banks are adopting cloud storage, which enables them to save data in a location that is either maintained and owned by the bank itself or by a third party, improving end-user security. Over the projected period, this is anticipated to enhance the adoption of cloud storage.

- Players in the cloud solutions market are currently compelled to develop inexpensive ways to store and handle the data due to the volume of data produced. The government cloud market will grow due to these factors in the future; for instance, In July last year, Tata Communications launched 'IZOTM Financial Cloud,' a community cloud platform tailored to fulfill Indian authorities' demanding data privacy, protection compliance, and security criteria for the banking, enterprises, and industries sectors.

Europea to Witness the Highest Growth

- The European Commission unveiled its first cloud computing strategy in 2012. The goal of the process was to accelerate and broaden the usage of cloud computing in all spheres of the economy. Currently, 36% of the continent's companies use cloud services2, for an estimated €54 billion (USD 5636 Billion) of direct cloud spending in 2020, which is expected to double by next year.

- As the Increased density of edge and cloud facilities is needed to sustain the adoption of innovative and sovereign edge and cloud technologies across the continent, the European market is planning to adopt cloud native 5G and enable industrial local 5G networks, leveraging the global competitiveness of its network equipment providers and the worldwide footprint of its telecommunication operators to transform the mobile network into a global network of widely distributed cloud-edge nodes.

- Moreover, the European Union plans to invest EUR 10 billion(USD 10.44 Billion) over the next seven years to create a domestic cloud computing market that could compete with multinational companies like Amazon, Google, and Alibaba. These factors will boost the government cloud market during the forecast period.

- The widespread adoption of government cloud across various industrial verticals for accessing the excessive amount of citizen data regarding user logs, policies, and systems from remote endpoints is one of the key factors driving the market growth across the region.

Government Cloud Industry Overview

The market for government cloud is concentrated with major giants, such as Microsoft, Oracle NEC, IBM, and Google, providing cloud solutions and services for the government. This market's entry barrier is high since the existing vendors have a strong foothold.

In September 2022 - Amazon Web Services Inc announced that it has joined the government of Telangana for the project to transform its citizen service delivery by advancing its cloud adoption framework as the Telangana state government has decided to migrate its information technology (IT) workloads to the cloud to accelerate its eGovernance plans, and deliver faster and more reliable citizen services through its 33 departments and 289 organizations while achieving high-operational efficiency and reduced IT costs.

In January 2022 - Dell technologies sped Journey to Multi-Cloud with Portfolio Expansion with introduced multi-cloud capabilities that offer a consistent experience wherever applications and data reside, along with also expanding support for developer operations (DevOps) with new offers and resources to help choose the right cloud environment combined with the security, support and predictable cost of Dell infrastructure.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Definitions and Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter Five Forces

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

6 Market Drivers

- 6.1 Need for Greater Storage Capabilities is Driving the Market Demand

- 6.2 Need for Data Transparency are Expanding the Market

7 Market Restraints

- 7.1 Cloud Computing Skills Gap is Hindering the Market Growth

8 MARKET SEGMENTATION

- 8.1 By Deployment model

- 8.1.1 Public Cloud

- 8.1.2 Private Cloud

- 8.1.3 Hybrid Cloud

- 8.2 By Delivery Mode

- 8.2.1 Infrastructure-as-a-Service

- 8.2.2 Pltaform-as-a-Service

- 8.2.3 Software-as-a-Service

- 8.3 By Application

- 8.3.1 Server and Storage

- 8.3.2 Disaster Recovery/Data Backup

- 8.3.3 Security and Compliance

- 8.3.4 Analytics

- 8.3.5 Content Management

- 8.4 By Geography

- 8.4.1 North America

- 8.4.2 Europe

- 8.4.3 Asia Pacific

- 8.4.4 Latin America

- 8.4.5 Middle East and Africa

9 COMPETITIVE LANDSCAPE

- 9.1 Company Profiles

- 9.1.1 Amazon Web Services Inc.

- 9.1.2 CGI Inc.

- 9.1.3 Cisco Systems Inc.

- 9.1.4 Dell Inc.

- 9.1.5 Google Inc.

- 9.1.6 IBM Corporation

- 9.1.7 Microsoft Corporation

- 9.1.8 NetApp Inc.

- 9.1.9 Oracle Corporation

- 9.1.10 Rackspace Inc.

- 9.1.11 Salesforce.com Inc.

- 9.1.12 VMWare Inc.