|

市場調査レポート

商品コード

1850068

自動車用レインセンサー:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Automotive Rain Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動車用レインセンサー:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月25日

発行: Mordor Intelligence

ページ情報: 英文 116 Pages

納期: 2~3営業日

|

概要

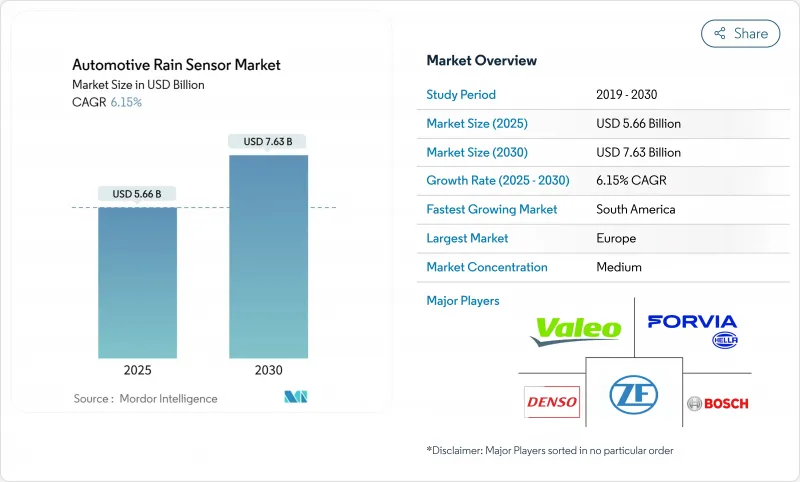

自動車用レインセンサー市場は現在、2025年に56億6,000万米ドルに達し、CAGR 6.15%を反映して2030年にはおよそ76億3,000万米ドルに達すると予測されています。

着実な電動化、レベル2+のドライバー・アシスタンス採用の増加、規制の勢いにより、レイン・センサーは快適な付加物から安全上重要な知覚入力へとシフトし続けています。ADAS機能のバンドル化、半導体の小型化、サブスクリプション対応のソフトウェアスタックにより、対応可能なベースが拡大する一方、コストダウンのMEMS技術革新により、ボリュームセグメントへのアクセスが拡大しています。チップメーカーとのサプライヤー間競争の激化も、ハードウェアのマージンを圧縮しているが、統合された光学、静電容量、湿度モジュールによる機能アップグレードを加速させています。これらの力を総合すると、OEMが集中型の無線アップデート可能な領域を中心に車両電気アーキテクチャを再構築するにつれて、自動車用レインセンサー市場は複数年にわたる変革の軌道を維持することになります。

世界の自動車用レインセンサー市場の動向と洞察

ADAS普及率の上昇により、多機能環境センシングが必須化

レベル2+およびレベル3の知覚スタックは、カメラレンズやLiDARウィンドウをクリアに保つために正確な雨滴、光、霧のデータを必要とし、センサーを快適性のための余分なものから中核的な安全イネーブラーへと作り変えています。欧州のOEMプログラムでは、光学式レインセンサーと湿度・光チャンネルを1枚のPCBで組み合わせ、ハーネスの軽量化と統合診断を実現しています。また、北米のトラックメーカーは、自動緊急ブレーキの稼働時間を延長するために、前方視界クラスターに雨検知を組み込んでいます。高解像度のCCDアレイは液滴の分類を改善し、ワイパー速度、アダプティブ・ヘッドライト、デフォッガー・ロジックを1つの制御ループで調整するフュージョン・ソフトウェアに供給します。その結果、調達チームは現在、ワイパーの待ち時間だけでなく、レーダーとカメラの相乗効果指標をベンチマークとして性能を評価するようになり、マルチセンサーの勝利はTier 1の収益パイプラインにとって極めて重要なものとなっています。

電化と高電圧アーキテクチャが採用を加速

400Vと800Vで動作するEプラットフォームは、信号処理ASICとレーザートリミングされたVCSELエミッタに安定した電力ヘッドルームを提供し、高湿度の過渡現象下では12Vの同等品よりも優れています。中央演算ドメインは、セキュアなCAN-FDリンクを介して生の液滴ベクトルをゾーンコントローラに取り込み、機械学習モデルがワイプのタイミングを改良し、ブレードの寿命を延ばし、空調負荷を削減します。無線ファームウェアのリリースにより、OEMは検出しきい値を繰り返し研ぎ澄ますことができ、予知保全アラートと連動した従量課金の収益層が開かれます。そのため、電池式ブランドは、レインセンサーをパッシブなガラスアクセサリーとしてではなく、窓の曇り止めサイクルを最大6%削減するエネルギー管理資産として販売しています。

エントリーレベルA/Bセグメント車の高い価格感応度

インド、ASEANの一部、およびラテンアメリカのコスト主導型プラットフォームは、インストルメントパネルのエレクトロニクス・スタック全体に75米ドル以下を割り当てており、25~30米ドルのレインセンサー・モジュールのための余裕はわずかです。インドの国産部品規制は、ローカライズされていないPCBAの輸入関税を増幅させ、ティア1の収益性を圧迫し、取得率を鈍らせる。OEMは、統合MEMSの価格が15米ドルを下回るまで、4m車以下の車種では手動可変間欠ワイパーに頼る。現地でのガラス接合パートナーシップを確保しているサプライヤーは、運賃サーチャージを削減することができるが、現在のところ、少量の受注がそのようなCAPEXの支出を妨げています。

セグメント分析

乗用車向け自動車用レインセンサー市場規模は2024年に71.23%のシェアを獲得し、2030年までのCAGRは6.55%と堅調に推移すると予想されます。セダン・プログラムはトリム・ライン全体で一貫した装着率を維持しているが、ハッチバックは依然として上位車種への価格傾斜が続いています。小型商用バンのフリートは、ドライバーの注意散漫と保険金請求を最小限に抑えるために自動ワイピングを指定するようになったが、中型トラックは後付けが複雑なため遅れています。需要調整では、SUVの構成比が10ポイント上昇するごとに、システム平均のBOM上限が4米ドル上昇し、ティア1のマージン維持を支えています。予測期間中、SUVはフロントガラスの面積が大きいため、静電容量式アレイの液滴ノイズが大きくなり、豪雨でも感度精度を+-2ml維持できる光学アーキテクチャーをOEMが好む傾向が続きます。

乗用車のリフレッシュサイクルは、高回転の小型商用車フリートと比較して、遅いが安定した台数増加をもたらします。テレマティクスを調査しているフリートオペレーターは、予測拭き取りアナリティクスが有効化されると、フロントガラスの修理請求が7%減少し、ビジネスケースが強化されると報告しています。全体として、SUVの普及により、自動車用レインセンサー市場は機能豊富なパッケージに偏っており、大量生産されるハッチバック車の低マージンとのバランスが保たれています。

光学CCD/CMOSデバイスは、S/N比の高さが実証され、2024年の売上高の81.64%を占める。光コントローラーASICの上位5製品はすでにシリコンリビジョンB以降であるため、コストカーブは平坦化し、MEMS参入企業は価格対性能で優位に立てる。静電容量式/MEMSベースのデバイスは、ガラス結合の公差を回避できるため、CAGRが8.83%に達します。赤外線反射ハイブリッドは、単価は高いもの、-25 °C以下の氷結防止性能を必要とするニッチなプログラムを取り込みます。

戦略ロードマップによると、MEMSサプライヤーは環境光センサーとIRプロキシミティを共有ダイスペースにバンドルし、PCBフットプリントを35%削減しています。逆に、光学業界の既存企業は、AIの最先端推論コアを内蔵することで、自己較正可能な液滴認識を可能にし、スペックリーダーシップを維持することで、生産量を確保しています。光学はプレミアムとシビアデューティのニッチを維持し、MEMSは民主化を推進します。

地域分析

欧州のシェア37.84%は、UNECEの厳格な視認性基準や、雨光と湿度の融合に2点の安全ポイントを与える2025 NCAPの採点を反映しており、Bセグメントハッチバック以上の車種にセンサーの装着が義務付けられています。南米大陸の確立されたプレミアム・ミックスも、利益率の高い光学アレイの優位性を確実なものにしています。サンパウロにあるブラジルの量販OEMハブが牽引する南米は、CAGR 10.33%で最も急速に成長しています。エントリーSUVからコンパクトSUVへの消費者のアップグレードは、自動ワイピングのためのBOMに余裕をもたらし、電子コンテンツの現地化を促進する連邦政府のインセンティブは、マナウス近郊のセンサーハウジング成形ベンチャーに拍車をかける。

アジア太平洋は微妙な動きを見せる。中国の新車評価プログラムでは、2027年から自動視界管理が評価され、すでに年間2,500万台の規模を誇る製造拠点内での安定した出荷が見込まれます。インドとASEANの一部では、輸入電子機器への課税がコストを押し上げています。とはいえ、EVの普及により、レインセンサーは再び重要性を増している:タイやインドネシアに輸出されている中国製の1万5,000米ドル以下のマイクロEVには、右ハンドルへの適合を容易にする基本的な静電容量式センサーが搭載されています。したがって、アジア太平洋地域は依然として最大の成長地域であると同時に、最も細分化された戦場でもあります。

北米の普及は目覚ましいというよりむしろ着実であるが、平均取引価格が高いため、主流のピックアップやSUVに複雑なセンサー融合パッケージが搭載されています。無線更新の文化は、フロントガラスの予知保全のためのサブスクリプション・モデルを生み出し、ハードウェアのコモディティ化を和らげる経常収益を生み出します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ADASの普及率の上昇により、多機能環境センサー(雨、光、霧)が必須に

- 電動化と高電圧オンボードアーキテクチャにより、ソリッドステート光学雨量センサーの採用が加速

- 自動ワイパーシステムに対する規制の推進

- 中型車における快適性と利便性の機能に対する消費者の需要の高まり

- フロントガラスのヘッドアップディスプレイ(HUD)モジュールの統合には清浄度センシングが必要(報告不足)

- 自動車の無線アップデートは、サブスクリプションベースのワイパー自動化を通じて新たな収益を生み出す(報告不足)

- 市場抑制要因

- エントリーレベルのA/Bセグメント車における高い価格感度により、インドとASEANにおけるセンサーの取り付け率が制限される

- 車載グレードのフォトダイオードとVCSELの不足

- フロントガラスの設計の不均一性により光学的結合が複雑化し、検証コストが上昇する(報告不足)

- カメラのみのADASスタックとの競合により、ソフトウェア定義の雨滴検知が期待される(あまり報道されていない)

- バリューチェーン/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力/消費者

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 車両タイプ別

- 乗用車

- ハッチバック

- セダン

- SUVとクロスオーバー

- 商用車

- 小型商用車(LCV)

- 中型および大型商用車

- 乗用車

- 技術別

- 光学式(CCD/CMOS)

- 赤外線反射

- 静電容量式/MEMSベース

- 販売チャネル別

- OEMインストール

- アフターマーケットの改造

- 用途別

- 自動ワイパー制御

- 雨量・光量・湿度の統合センサー

- ADASセンサーフュージョンモジュール

- 地域別

- 北米

- 米国

- カナダ

- その他北米地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- トルコ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- HELLA GmbH & Co. KGaA

- Valeo SA

- DENSO Corporation

- ZF Friedrichshafen AG

- Robert Bosch GmbH

- STMicroelectronics N.V.

- Analog Devices Inc.

- ams-OSRAM AG

- onsemi

- Hamamatsu Photonics K.K.

- Sensata Technologies Inc.

- Melexis NV

- Texas Instruments Inc.

- Panasonic Holdings Corp.