|

市場調査レポート

商品コード

1432803

リスク分析:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Risk Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| リスク分析:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

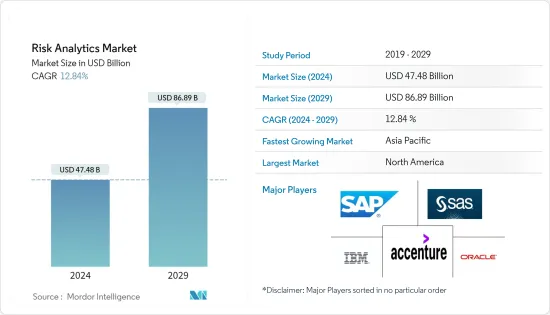

リスク分析市場規模は2024年に474億8,000万米ドルと推定され、2029年には868億9,000万米ドルに達し、市場推計・予測期間(2024-2029年)のCAGRは12.84%で成長すると予測されます。

リスク分析ソリューションは、ヒューマンエラー、システム障害(ソフトウェア、ハードウェア、ネットワークなどに関連する可能性がある)、不正サイバー犯罪などの内部要因によって発生する可能性のあるオペレーショナルリスクへの対処と保護を支援します。

主なハイライト

- 現在、リスク分析技術により、リスク管理者はこれまで以上に確実にリスクを測定・予測できるようになっています。企業はリスク分析を活用して、さまざまなセキュリティ・データ・ソースから裏付けとなる情報を収集し、サイバーリスクの定量化、セキュリティ運用の自動化、インテリジェンス主導の意思決定を行っています。さらに組織は、PCI-DSSやNISTサイバーセキュリティフレームワークなどの義務付けやガイダンスによって、サイバー観点からの規制圧力が高まっているのを目の当たりにしています。

- 様々なエンドユーザ業界において、大量の構造化データおよび非構造化データの利用が増加しているため、データを脅威から管理・保護するためのリスク分析に対する需要が高まっています。例えば、シーゲイト・テクノロジーPLCによると、世界のデータ量は2020年には47ゼタバイト、2025年には163ゼタバイトに増加すると予想されています。

- さらに、クラウド・コンピューティングは、過去40年間の他のどのコンピューティング革命よりも驚くべきソフトウェア革命を推進しています。ロケーションベースのリスク分析が進歩するにつれ、旧来のサーバーベースのシステムではなく、クラウドベースのテクノロジーを使って構築・提供できるようになるのは当然のことです。現在、クラウドを通じて利用可能なリスク評価・蓄積プラットフォームがいくつかあります。セキュリティに対するルールベースのアプローチは、それが脅威の検知、調査、対応のいずれに適用されるものであっても、アカウントの漏洩や悪意のある内部関係者を含む高度なサイバー脅威にもはや追いつくことはできないです。

- 銀行・金融サービス・保険(BFSI)セクターにおけるリスク分析の需要は、モバイルバンキングサービスの利用増加とデータ量の増加によっても高まっています。リスク・アナリティクスを適用することで、データを1つの包括的な視点にまとめ、必要不可欠なデータを収集し、活用できる知見を生み出すことができます。さらに、世界中の物流企業にとって、コロナウイルス感染症の国際的な蔓延によってもたらされた事業の混乱やサプライチェーンの問題に効率的に対処するためにも、リスク・アナリティクスは不可欠です。

- さらに、COVID-19と闘うために、主にヘルスケア分野で新しいアナリティクス・ソリューションを提供する企業もあります。臨床検査は臨床判断のかなりの割合を左右し、一般的でリスクの高い状態の患者のケアを改善する上で不可欠な役割を果たしています。例えば、LabCorpはInsight Analyticsレポートを発表し、プロバイダー組織が様々な高リスクの健康状態に対して、個人レベルでも集団レベルでも改善されたケアを提供していることを支援しています。

リスク分析市場の動向

BFSIはリスク・アナリティクス・ソリューションの大幅な導入が見込まれる

- 世界中の銀行は、銀行・金融業界を取り巻くリスクの増大に対処するため、より合理的なアプローチが必要であることを認識し、リスク分析の重要性を理解しています。

- リスク分析によって、銀行や金融機関はリスク管理に対する「サイロ」アプローチから脱却し、企業全体のリスクを包括的に捉えることができるようになります。例えば、オペレーショナル・リスク管理(ORM)では、監視が必要な取引件数が飛躍的に増加しているため、現行の銀行インフラに対する圧力が高まり、リスク・アナリティクス市場が活性化しています。

- 金融機関は、事業を成長させながら不正行為を減らし、厳しい規制遵守要件を満たすという強いプレッシャーにさらされています。さらに、新規口座詐欺と口座乗っ取りは、現在金融機関が課題としている詐欺の上位2種類です。リスク・アナリティクス・ソリューションは、AIの一種である機械学習ベースのリスク分析を用いて、オンラインおよびモバイル・チャネルにおけるこれらの不正行為やその他の不正行為から保護します。

- データ分析は、銀行が危険から身を守るために様々な方法で利用することができます。例えば、顧客分析は、信用リスク管理のために、信用力に応じて顧客を分類するために使用することができます。そのような顧客は期日通りに支払いを行うことが期待できるため、そうすることで個人はクレジット商品のターゲット市場を選ぶことができ、債務不履行リスクへのエクスポージャーを下げることができます。世界・アソシエーション・オブ・リスク・プロフェッショナルによると、資本市場、銀行、保険セクターは、リスク情報テクノロジーとサービスに960億米ドルを費やすと推定されています。

- さらに、グラント・ソントンの調査研究によると、回答者の85%が、銀行のデータおよびリスク情報管理イニシアチブは、その潜在能力をフルに発揮するためにさらなる効率化が必要であると考えています。さらに、82%の回答者は、自行のリスク分析と測定についても同じことを述べています。したがって、このような動向がBFSI業界におけるリスク分析ソリューションの必要性を後押ししています。

北米が大きなシェアを占める見込み

- 北米が最も高い市場シェアを占めると予想され、米国が市場をリードしています。同地域の優位性は、エンドユーザー業界におけるリスク分析ソリューションの採用が増加していること、大企業の存在感が大きいこと、低コストの地域で事業を展開する他の企業との競争により早期の技術導入が推進されていることによる。

- さらに、各業界でクラウドコンピューティングが採用されていることも、市場の成長を後押ししています。ヘルスケア情報システム(HIS)を差し迫ったサイバーセキュリティリスクから保護するという課題は、クラウドコンピューティングの採用と絡み合っています。HISのデータとリソースは、リモートアクセス、意思決定、緊急時、その他ヘルスケア関連の観点から、他のシステムと本質的に共有されています。

- さらに、米国ではパンデミックの年に、電子メールのハッキング事件、マルウェア攻撃、EHRへの不正アクセスなど、28件のデータ漏洩事件が報告されている(出典:米国保健社会福祉省)。医療ヘルスケア分野では、クラウド・コンピューティングはスケーラブルで経済的であるため、即効性のある救済策と考えられています。

- 米国のヘルスケア・インフラは、予測分析の領域で前向きな動向を経験しています。過去数年間で、ヘルスケア企業の経営幹部の40%以上が、データ量が50%増加したと報告していることが調査で明らかになっています。データセットが大きくなり、取り扱いが難しくなるにつれ、医療システムや支払機関は予測分析をますます採用するようになっています。

- さらに、この地域にはリスク分析ベンダーが強力な足場を築いており、市場の成長に寄与しています。その中には、IBM Corporation、Oracle Corporation、SAS Institute Inc.、AxiomSL Ltd.などが含まれます。

リスク分析業界の概要

リスク分析市場は、特に企業レベルでの導入において大手ベンダーが大きなシェアを占めており、比較的統合された市場です。また、大企業は革新的で高品質なサービスをエンドユーザーに提供できるため、この市場を独占しています。IBM Corporation、SAP SE、SAS Institute Inc.、Oracle Corporation、Accenture PLC、Adenza Group Inc.

2023年11月、SaaS(Software-as-a-Service)リスク分析サプライヤーであるRenew Risk社と、再生可能エネルギー・プロジェクト向けの著名な保険会社であるGCube Insurance社は、戦略的提携を発表しました。GCubeの洋上風力発電の顧客はこのパートナーシップから大きな恩恵を受け、洋上風力発電のリスク分析とモデリングの能力を強化します。GCubeは、洋上風力ポートフォリオ向けに調整されたRenew Riskの先進的な災害リスクモデルを活用することで、この契約から利益を得る。

2023年9月、コーポレート・リスク・ソリューション、ポートフォリオ構築ツール、ファクター・リスク・モデルの世界的サプライヤーであるAxiomaは、Jacobi Inc.との新たな提携を発表しました。サンフランシスコを拠点とするジャコビ社のテクノロジーは、ダイナミックな顧客エンゲージメントを可能にし、投資業務を最適化し、マルチアセット・ポートフォリオの構築とメンテナンスを簡素化します。このワークフロー一体型のソリューションにより、投資マネジャーは、株式ポートフォリオやマルチアセットクラス・ポートフォリオのファクター・ベースの分解に必要な時系列データやポイント・イン・タイムのリスク・データに容易にアクセスできるようになります。

2022年10月、世界トップクラスの投資銀行、証券、投資運用会社であるゴールドマン・サックス・グループと、革新的なリスク、分析、インデックス・ソリューションのリーディング・プロバイダーであるQontigoは、パートナーシップの拡大を発表しました。Qontigoは、モジュール式データ管理・分析ソリューションの集合体であるGoldman Sachs Financial Cloud for Data、および市場をリードするデータ、分析、市場インサイト、トレーディング・ソリューションを機関投資家に提供する同社のデジタル・プラットフォームであるGoldman Sachs Marqueeを通じて、Axioma Portfolio OptimizeおよびAxioma Equity Factor Risk Modelsを利用できるようになります。

2022年9月、キャメロット・マネジメント・コンサルタンツと、サプライチェーン・インサイトとリスク・アナリティクスの著名なプロバイダーであるエバーストリーム・アナリティクスとの間で、共同提携が開始されました。この提携は、エバーストリーム社の優れたリスク評価とAIを駆使したアナリティクスを、キャメロット社の比類のない戦略的プロセス設計と組織的知識と組み合わせることで、高パフォーマンスでコンプライアンスに準拠したレジリエントなバリューチェーンを構築するものです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 市場の定義と範囲

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 市場促進要因

- ビジネス・プロセスの複雑化

- 世界な規制フレームワークと政府政策

- 市場抑制要因

- 高い導入コストと運用コスト

- 複雑な規制遵守が市場成長の妨げになる可能性

- COVID-19の市場全体への影響

第5章 市場セグメンテーション

- 構成別

- ソリューション

- サービス別

- 展開別

- オンプレミス

- クラウド

- 業界別

- BFSI

- ヘルスケア

- 小売

- 製造業

- その他エンドユーザー別(ITおよびテレコム)

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他のMEA

- 北米

第6章 競合情勢

- 企業プロファイル

- IBM Corporation

- Oracle Corporation

- SAP SE

- SAS Institute Inc.

- Moody's Analytics Inc.

- OneSpan Inc.

- Capgemini SE

- Accenture PLC

- Risk Edge Solutions

- Adenza Group Inc.(AxiomSL Ltd.)

- Provenir Inc.

第7章 投資分析

第8章 市場機会と今後の動向

The Risk Analytics Market size is estimated at USD 47.48 billion in 2024, and is expected to reach USD 86.89 billion by 2029, growing at a CAGR of 12.84% during the forecast period (2024-2029).

Risk analytics solutions help organizations deal with and protect against operational risks, which can arise due to internal factors, such as human errors, failures of systems (which can be related to software, hardware, network, etc.), and fraud cybercrime.

Key Highlights

- Currently, risk analytics techniques are enabling risk managers to measure and predict risk with more certainty than ever before. Organizations are leveraging risk analytics to gather supporting information through various security data sources to quantify their cyber risks, automate their security operations, and make intelligence-driven decisions. Additionally, organizations are witnessing increased regulatory pressure from the cyber perspective with mandates and guidance, such as the PCI-DSS and NIST Cybersecurity Framework.

- The increased usage of large amounts of structured and unstructured data in the various end-user industries boosts the demand for risk analytics to manage and save data from threats. For instance, According to Seagate Technology PLC, the global volume of data is expected to increase to 47 zettabytes and 163 zettabytes in 2020 and 2025.

- Moreover, cloud computing is driving a software revolution astonishingly as any other computing revolution of the past 40 years. As analytics for location-based risk advance, it is only sensible that they can be built and delivered using cloud-based technology rather than older server-based systems. There are several risk assessment and accumulation platforms available now through the cloud. Rules-based approaches to security, whether they are applied to threat detection, investigation, or response, can no longer keep pace with advanced cyber threats, including account compromise and malicious insiders.

- The demand for risk analytics in the banking, financial services, and insurance (BFSI) sector is also fueled by the increased use of mobile banking services and the rising volume of data. Risk analytics can be applied to combine the data into a single, comprehensive perspective, collect essential data, and produce insights that can be put to use. In addition, risk analytics are critical for logistics firms worldwide to efficiently address business disruptions and supply chain issues brought on by the spread of the coronavirus disease internationally.

- Furthermore, players cater to provide new analytics solutions, majorly in the healthcare sector, to combat COVID-19. Laboratory testing influences a significant percentage of clinical decisions and plays an essential role in improving care for patients with common, high-risk conditions. For example, LabCorp launched Insight Analytics reports that support provider organizations are delivering improved care, both individually and on a population level, for a range of high-risk health conditions.

Risk Analytics Market Trends

BFSI is Expected to Witness Huge Adoption of Risk Analytics Solutions

- Banks across the world are realizing that they need a more rational approach to managing a growing plethora of risks enveloping the banking and financial industries' landscape, and they have now understood the significance of risk analytics.

- Risk analytics enables banks and financial institutions to move away from the 'silo' approach to risk management and move toward the comprehensive view of enterprise-wide risks. For instance, in operational risk management (ORM), the number of transactions that need to be monitored is growing exponentially, thus implying pressure on the current banking infrastructure and enabling the market for risk analytics.

- Financial Organizations are under intense pressure to reduce fraud and meet strict regulatory compliance requirements while growing their business. Moreover, New Account Fraud and Account Takeover are the top two types of fraud challenging financial institutions today. Risk analytics solutions protect against these and other fraudulent activities across online and mobile channels, using machine learning-based risk analysis, a form of AI.

- Data analytics can be used in a variety of ways by banks to protect themselves from danger. Customer analytics, for instance, can be used to categorize customers according to their creditworthiness for credit risk management. Because one can rely on those customers to make payments on time, doing so lets individuals choose a target market for credit products and lowers exposure to default risk. According to the Global Association of Risk Professionals, it is estimated that capital markets, banking, and insurance sectors are likely to spend USD 96 billion on risk information technologies and services.

- Additionally, the Grant Thornton survey study identified that 85% of respondents believed that their bank's data and risk information management initiatives need additional efficiencies to realize their full potential. Furthermore, 82% had indicated the same for their institution's risk analytics and measurements. Hence, such trends drive the need for risk analytics solutions in the BFSI industry.

North America is Expected to Hold a Significant Share

- North America is expected to hold the highest market share, with the United States leading the market. The dominance of the region is due to its increasing adoption of risk analytics solutions among end-user industries, a significant presence of large enterprises, and drive for early technological adoption owing to competition from other businesses operating in low-cost regions.

- Moreover, adopting cloud computing across industries is driving market growth. The task of protecting Healthcare Information Systems (HIS) from immediate cyber security risks has been intertwined with cloud computing adoption. The data and resources of HISs are inherently shared with other systems for remote access, decision-making, emergency, and other healthcare-related perspectives.

- Additionally, there have been 28 data breach incidents reported during the pandemic year in the United States, including email hacking incidents, malware attacks, and unauthorized access to EHRs (source the US Department of Health & Human Services). In the medical healthcare sector, cloud computing is considered to be an immediate remedy because it is scalable as well as economical.

- The healthcare infrastructure in the United States is experiencing positive trends in the predictive analytics domain. Studies have shown that in the last few years, more than 40% of healthcare executives reported a 50% increase in data volume. As the data sets become bigger and more difficult to handle, health systems and payers increasingly adopt predictive analytics.

- Moreover, the region has a strong foothold of risk analytics vendors, which contributes to the growth of the market. Some of them include IBM Corporation, Oracle Corporation, SAS Institute Inc., and AxiomSL Ltd, among others.

Risk Analytics Industry Overview

The risk analytics market is a relatively consolidated market as the major vendors account for a significant share of the market, especially in the enterprise-level adoption. Additionally, large companies dominate this market owing to their ability to offer innovative and high-quality services to end-users on a different scale and with customization that suits their specific needs. IBM Corporation, SAP SE, SAS Institute Inc., Oracle Corporation, Accenture PLC and Adenza Group Inc. (previosuly AxiomSL Ltd.) are a few prominent players operating in the market.

In November 2023, Renew Risk, a Software-as-a-Service (SaaS) risk analytics supplier, and GCube Insurance, a prominent insurance company for renewable energy projects, announced a strategic partnership. GCube's offshore wind clients will significantly benefit from this partnership, strengthening the company's capacity for offshore wind risk analytics and modeling. GCube will benefit from this agreement by utilizing Renew Risk's advanced catastrophe risk models, which are tailored for offshore wind portfolios.

In September 2023, Axioma, a global supplier of corporate risk solutions, portfolio construction tools, and factor risk models, announced a new partnership with Jacobi Inc. The San Francisco-based company Jacobi's technology enables dynamic client engagement, optimizes investing operations, and simplifies multi-asset portfolio building and maintenance. With this single workflow-integrated solution, investment managers can readily access time series and point-in-time risk data for factor-based decomposition across equity and multi-asset class portfolios.

In October 2022, Goldman Sachs Group, Inc., a top global investment banking, securities, and investment management organization, and Qontigo, a leading innovative risk, analytics, and index solutions provider, announced an expanded partnership. Through Goldman Sachs Financial Cloud for Data, a collection of modular data management and analytics solutions, as well as Goldman Sachs Marquee, the company's digital platform that offers market-leading data, analytics, market insights, and trading solutions to institutional investors, Qontigo would now make the Axioma Portfolio Optimize and Axioma Equity Factor Risk Models available.

In September 2022, A collaborative alliance was launched between CAMELOT Management Consultants and Everstream Analytics, a prominent provider of supply chain insights and risk analytics. This partnership combines Everstream's superior risk ratings and AI-powered analytics with CAMELOT's unrivaled strategic process design and organizational knowledge to create high-performing, compliant, resilient value chains.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Scope

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Market Drivers

- 4.4.1 Growing Complexities across Business Processes

- 4.4.2 Global Regulatory Frameworks and Government Policies

- 4.5 Market Restraints

- 4.5.1 High Installation and Operational Costs

- 4.5.2 Complicated Regulatory Compliance might hinder the Market Growth

- 4.6 Impact of COVID-19 on Overall Market

5 MARKET SEGMENTATION

- 5.1 By Component

- 5.1.1 Solution

- 5.1.2 Service

- 5.2 By Deployment

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.3 By End-user Vertical

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 Retail

- 5.3.4 Manufacturing

- 5.3.5 Other End-user Verticals (IT and Telecom)

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 UK

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Mexico

- 5.4.4.3 Argentina

- 5.4.4.4 Rest of Latin America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 UAE

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of MEA

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles*

- 6.1.1 IBM Corporation

- 6.1.2 Oracle Corporation

- 6.1.3 SAP SE

- 6.1.4 SAS Institute Inc.

- 6.1.5 Moody's Analytics Inc.

- 6.1.6 OneSpan Inc.

- 6.1.7 Capgemini SE

- 6.1.8 Accenture PLC

- 6.1.9 Risk Edge Solutions

- 6.1.10 Adenza Group Inc. (AxiomSL Ltd.)

- 6.1.11 Provenir Inc.