|

市場調査レポート

商品コード

1637761

次世代ストレージ:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Next-generation Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 次世代ストレージ:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

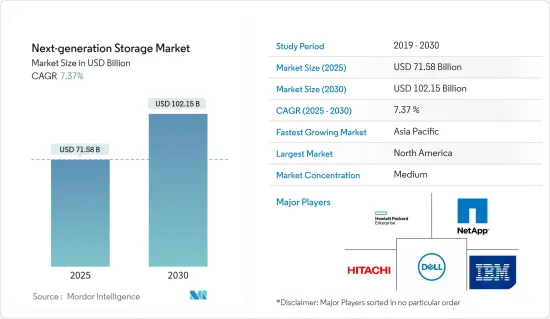

次世代ストレージの市場規模は2025年に715億8,000万米ドルと推計され、予測期間(2025~2030年)のCAGRは7.37%で、2030年には1,021億5,000万米ドルに達すると予測されます。

デジタル社会の急速な発展に伴い、モバイルサービス、ビッグデータ、クラウド・コンピューティング、ソーシャル・ネットワーキング・アプリケーションの開発が加速しています。次世代ストレージ技術は、IT企業、自動車会社、データセンターなど、さまざまなエンドユーザー業界のデータ保存を支援する製品やソリューションの高度なポートフォリオを扱う。ファイルサイズの増大や大量の非構造化データ、ビッグデータにより、IT企業はデータ管理で多くの問題に直面しています。

主なハイライト

- 従来のデータストレージ技術では、大量の日常データを処理できないです。次世代データストレージ・インフラは、増大するデータストレージ需要に対応するため、信頼性が高く、高速で、コスト効率の高いソリューションを提供します。

- さらに、次世代ストレージ技術市場は、ビッグデータストレージ、エンタープライズ・データストレージ、その他のクラウドベースのサービスなど、幅広い用途で情報技術分野に進出しています。ストレージとその対処方法は、トップラインとボトムラインに大きな影響を与える可能性があります。IT組織は、安全なストレージへの投資から、ビジネスに利益をもたらす新技術への投資へと、より積極的に移行することが期待されています。

- 2023年4月、バストデータはヒューレット・パッカード・エンタープライズ(HPE)がバストデータの主要なファイルソフトウェアプラットフォームを新しいHPE GreenLake for File Storageサービスに組み込んだと発表しました。新しいHPE GreenLakefor File Storageにバストデータ独自の革新的なスケールアウトソフトウェアアーキテクチャを活用することで、企業顧客は非構造化データを大規模なパフォーマンスで管理し、より迅速なデータ洞察を実現することができます。

- しかし、クラウドベースのストレージには、設定ミス、不十分なデータガバナンス、不十分なアクセス制御など、多くのセキュリティ上の問題があります。このようなクラウドストレージのセキュリティ問題は、企業データを権限のない第三者に公開する可能性があり、市場成長の抑制要因となっています。

- COVID-19の大流行は、次世代ストレージ市場、特にクラウドストレージで使用されるソリューションにプラスの影響を与えました。ストレージ・ベンダーは、COVID-19コロナウイルスの大流行中、研究者、企業、在宅勤務ユーザー、パートナー企業のビジネス運営や遠隔作業を支援するため、自社のハードウェアやソフトウェア技術の一部を無料で提供していました。

次世代ストレージ市場動向

ダイレクト・アタッチドストレージ(DAS)が著しい成長を遂げる

- ダイレクト・アタッチドストレージ(DAS)は、ネットワークを介してコンピュータに接続される他のストレージ・システムとは異なり、PCやサーバーなどのコンピュータに直接接続される最も古く、最もオーソドックスなデータストレージ・システムです。

- DASは、多くの組織のストレージ戦略において重要な役割を果たす他のストレージシステムと比較して、高性能、セットアップとコンフィギュレーションの容易さ、データへの高速アクセス、低コストといった特定の利点を提供します。

- DASは、サーバーがデータを読み書きするためにネットワークを横断する必要がないため、ネットワークストレージよりも優れたパフォーマンスをユーザーに提供できます。このため、多くの組織が高いパフォーマンスを必要とするアプリケーションにDASを利用しています。DASはまた、ネットワーク・ベースのストレージ・システムよりも複雑ではないため、導入や保守が容易で、コストも抑えられます。

- さらに、仮想化技術の進歩は、特に市場のハイパーコンバージドインフラ(HCI)システムにおいて、DASに新たな息吹を吹き込んでいます。HCIシステムは複数のサーバーとDASストレージ・ノードで構成され、ストレージは論理リソース・プールに集約されるため、従来のDASよりも柔軟なストレージ・ソリューションを提供します。

- 一般的にDASは、SASやSATAなどの高速コンピュータ・バス・インターフェースの利点と、システムのRAMやプロセッサにデータが近い位置にあることから、直接接続されるコンピュータ・システムに高いストレージ性能を提供します。

- 2022年5月、TerraMasterは大容量のデータを保存する中央ロケーションを必要とする顧客向けに、新しい8ベイDAS(Direct Attached Storage)アプライアンスをリリースしました。NASとは異なり、DASはPCやその他のデバイスに直接接続されたケーブルを介してローカルで使用されます。新しいTerraMaster D8-332は、最大160TBの容量を持つ業務用RAIDストレージです。

- DASの一般的な用途の一つはデータセンターです。ウェブホスティングのようなアプリケーションではDASが使用され、顧客は専用のストレージデバイスを専用サーバーに接続することを望みます。DASはまた、オペレーティングシステムやハイパーバイザーを起動するためのストレージとしても、データユースセンターで一般的に利用されています。

北米が最大の市場シェアを占める

- 北米の次世代ストレージ市場は、世界ベンダーと消費者の地域集中が進んでいるため、高い成長率を示すと思われます。

- 米国は、世界的に見てもデータセンターのトップ市場の1つです。また、グーグルは2022年4月、全国のデータセンターとオフィスに95億米ドルを投資する計画を発表しました。この巨大企業は、ジョージア州、テキサス州、ニューヨーク州、カリフォルニア州など、米国の各州に14のデータセンターを建設・拡張する予定です。このようなデータセンターへの投資の増加は、市場にも大きな成長機会をもたらしています。

- さらに、データを多用するモノのインターネット(IoT)機器は、次世代ストレージのもう一つの新興市場を構成しています。これらのアプリケーションは主に広範囲に及ぶ。ファクトリー4.0の形をした産業オートメーションは、その1つのセグメントです。しかし、IoTにはウェアラブル、ヘルスケア、航空、さらにスマートホーム、スマートファーム、スマートメーター、スマート物流など、スマートから始まるあらゆるものが含まれます。

- スタンフォード大学とアバストの調査によると、北米地域の家庭は世界で最もIoTデバイスの設置密度が高いです。特に、同地域の家庭の66%が少なくとも1台のIoTデバイスを所有しています。さらに、北米の家庭の25%は3台以上のデバイスを所有しています。

- さらに、インターネットトラフィックとユーザー生成データの増加が市場成長に寄与しており、北米はIPトラフィック量が最も多いです。CISCOによると、同地域のIPトラフィックは2022年までに月間108.4EBに達するといいます。

- エリクソンのレポートによると、北米におけるスマートフォン1台当たりの月間モバイルデータ使用量の平均は、2028年に55GBに達する見込みです。改善された5Gネットワークと無制限のデータプランは、この地域でより多くの5G加入者を引き付けると思われます。動画ベースのアプリ、仮想現実/拡張現実、ゲームは膨大なデータトラフィックを生み出します。2028年には、北米の5G契約数は世界の90%を上回り、全地域の中で最も高くなると同社は予測しています。

次世代ストレージ業界の概要

次世代ストレージ市場は半固体化しており、いくつかの主要企業で構成されています。市場シェアの面では、現在、少数の主要企業が市場を独占しています。しかし、メモリパッケージング技術の革新に伴い、多くの企業が新興国の未開拓の新市場で存在感を高めています。

- 2023年5月- ネットアップは、新しい最新のブロックストレージ製品と、ランサムウェア攻撃からの復旧におけるネットアップのクラス最高の能力を強調する保証を発表しました。ネットアップはこの発表を通じて、IT予算の制限、ITの複雑化、持続可能性に対する緊急性の高まり、サイバー脅威の継続的な急増など、お客様の重要な課題に対応することを目指します。

- 2023年4月- ピュアストレージは、次世代の統合ブロック・ファイルストレージ・サービスを発表しました。この新しいストレージ・サービスは、単一の世界・リソース・プールからネイティブ・ブロック・サービスとファイル・サービスへのアクセスを提供します。ユニファイドストレージ・アーキテクチャーは、ブロックストレージとファイルストレージのフォーマットをサポートし、企業がさまざまな方法でデータを保存・閲覧できるようにします。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19の業界への影響評価

- 技術スナップショット

- 磁気ストレージ

- ソリッド・ステートストレージ

- ソフトウェア定義ストレージ(SDS)

- クラウドストレージ

- ユニファイドストレージ

- その他のストレージ技術

第5章 市場力学

- 市場促進要因

- デジタルデータ量の増加

- ソリッドステート・デバイスの採用増加

- スマートフォン、ノートパソコン、タブレットの普及拡大

- 市場抑制要因

- クラウドおよびサーバーベースのサービスにおけるデータセキュリティの欠如

第6章 市場セグメンテーション

- ストレージシステム別

- ダイレクト・アタッチドストレージ(DAS)

- ネットワーク接続型ストレージ(NAS)

- ストレージ・エリア・ネットワーク(SAN)

- ストレージアーキテクチャ別

- ファイル・オブジェクト・ベースストレージ(FOBS)

- ブロックストレージ

- エンドユーザー業界別

- BFSI

- 小売

- ITおよび電気通信

- ヘルスケア

- メディア・エンターテイメント

- その他エンドユーザー産業

- 地域別

- 北米

- 欧州

- アジア太平洋

- 世界のその他の地域

第7章 競合情勢

- 企業プロファイル

- Dell Inc.

- Hewlett Packard Enterprise Company

- NetApp Inc.

- Hitachi Ltd

- IBM Corporation

- Toshiba Corp.

- Pure Storage Inc.

- DataDirect Networks.

- Scality Inc.

- Fujitsu Ltd.

- Netgear Inc.

第8章 投資分析

第9章 市場の将来

The Next-generation Storage Market size is estimated at USD 71.58 billion in 2025, and is expected to reach USD 102.15 billion by 2030, at a CAGR of 7.37% during the forecast period (2025-2030).

With the sizeable and exponential growth in the digital world, there has been an accelerating development in mobile services, Big Data, cloud computing, and social networking applications. Next-generation storage technology deals with an advanced portfolio of products and solutions, which help store data across various end-user industries, including IT firms, automotive companies, and data centers. With the increasing file sizes and a massive amount of unstructured and Big Data, IT companies face plenty of problems while dealing with data management.

Key Highlights

- Conventional data storage technologies cannot handle a large amount of everyday data. The next-generation data storage infrastructure offers a reliable, faster, and cost-effective solution to meet the growing data storage demands.

- Further, the next-generation storage technology market is moving into the information technology sector, with an extensive range of applications across Big Data storage, enterprise data storage, and other cloud-based services. Storage and how it is addressed can significantly impact the top and bottom lines. IT organizations are expected to be more willing to move from making a safe storage investment to investing in new technologies that can benefit the business.

- In April 2023, VAST Data announced that Hewlett Packard Enterprise (HPE) had incorporated VAST Data's leading file software platform into the new HPE GreenLake for File Storage service. By leveraging VAST's unique and innovative scale-out software architecture for the new HPE GreenLakefor File Storage, enterprise customers can manage unstructured data with massive performance and achieve faster data insights.

- However, many security issues are associated with cloud-based storage, such as misconfiguration, insufficient data governance, and poor access controls, among others. Such cloud storage security issues that can expose enterprise data to unauthorized parties can act as a restraint on market growth.

- The COVID-19 pandemic outbreak positively impacted the next-generation storage market, especially solutions used in cloud storage. Storage vendors were making some of their hardware and software technology available for free to help researchers, businesses, work-from-home users, and partners run their businesses and work remotely during the COVID-19 coronavirus pandemic.

Next-generation Storage Market Trends

Direct Attached Storage (DAS) to Witness Significant Growth

- Direct Attached Storage (DAS) is the oldest and most conventional data storage system connected directly to a computer, such as a PC or server, unlike other storage systems connected to a computer over a network.

- DAS offers specific benefits compared to other storage systems that play an essential role in many organizations' storage strategies: high performance, easiness during the setup and configuration, fast access to data, and low cost.

- DAS can provide users with better performance than network storage because the server does not have to traverse the network to read or write data. For this reason, many organizations utilize his DAS for applications that require high performance. DAS is also less complex than network-based storage systems, making them easier to implement and maintain and less expensive.

- Moreover, growing advances in virtualization technology are breathing new life into DAS, especially in the market's hyper-converged infrastructures (HCI) systems. The HCI system consists of multiple servers and DAS storage nodes, and the storage is aggregated into logical resource pools, providing a more flexible storage solution than traditional DAS.

- Generally, DAS offers high storage performance to the computer system it is directly attached to, owing to the advantage of fast computer bus interfaces, such as SAS and SATA, and the close location of data to the system's RAM and processor.

- In May 2022, TerraMaster recently released a new 8-bay Direct Attached Storage (DAS) appliance for customers who need a central location to store large amounts of data. Unlike NAS, DAS is used locally via a cable connected directly to a PC or other device. The new TerraMaster D8-332 is professional RAID storage with up to 160TB capacity.

- One common application of DAS is in data centers. Applications like web hosting use DAS, where customers want their private storage devices connected to their dedicated server. DAS is also commonly utilized in data use centers as storage for booting operating systems and hypervisors.

North America Occupies the Largest Market Share

- The country's next-generation storage market will witness a high growth rate due to the increasing regional concentration of global vendors and consumers.

- The United States remains one of the top markets for data centers globally. Also, in April 2022, Google announced plans to invest USD 9.5 billion in data centers and offices nationwide. The tech giant will be building or expanding 14 data centers in the US states like Georgia, Texas, New York, and California, among others. Such increasing investments in data centers are also creating considerable growth opportunities for the market.

- Moreover, the data-heavy Internet of Things (IoT) devices constitute another emerging market for next-generation storage. These applications primarily cover a wide range. Industrial automation in the form of Factory 4.0 is one segment. Still, the IoT also includes wearables, healthcare, aviation, plus about anything that begins with smart, such as smart homes, smart farms, smart metering, and smart logistics, among others.

- According to a Stanford University and Avast study, homes in the North American region have the highest density of IoT devices installed worldwide. Notably, 66% of households in the region have at least one of her IoT devices. Additionally, 25% of North American homes have three or more devices.

- Additionally, increasing Internet traffic and user-generated data contribute to the market growth, with North America having the highest volume of IP traffic. According to CISCO, IP traffic in the region will reach 108.4 EB per month by 2022.

- According to Ericsson's report, the average monthly mobile data usage per smartphone is likely to reach 55 GB in 2028 in North America. The improved 5G network and unlimited data plans will attract more 5G subscribers in the region. Video-based apps, virtual/augmented reality, and gaming generate huge data traffic. In 2028, the company predicts that 5G subscriptions in North America will be more than 90%world's, the highest among all regions.

Next-generation Storage Industry Overview

The next-generation storage market is semi-consolidated and consists of some major players. In terms of market share, few of the key players currently dominate the market. However, with innovation in memory packaging technology, many companies are increasing their market presence across untapped new markets of emerging economies.

- May 2023 - NetApp announced a new modern block storage offering and a guarantee highlighting NetApp's best-in-class ability to recover from ransomware attacks. Through this launch, the company aims to address critical customer challenges, including restricted IT budgets, increasing IT complexity, increased urgency around sustainability, and the continued exponential growth of cyber threats.

- April 2023 - Pure Storage Inc. announced introducing a next-generation unified block and file storage service. This new storage service provides access to native block and file services from a single, global pool of resources. A unified storage architecture supports block and file storage formats, allowing organizations to store and view data in various ways.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of COVID-19 Impact on the Industry

- 4.4 Technology Snapshot

- 4.4.1 Magnetic Storage

- 4.4.2 Solid State Storage

- 4.4.3 Software Defined Storage (SDS)

- 4.4.4 Cloud Storage

- 4.4.5 Unified Storage

- 4.4.6 Other Storage Technologies

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Volume of Digital Data

- 5.1.2 Rising Adoption of Solid-state Devices

- 5.1.3 Increasing Proliferation of Smartphones, Laptops, and Tablets

- 5.2 Market Restraints

- 5.2.1 Lack of Data Security in Cloud- and Server-based Services

6 MARKET SEGMENTATION

- 6.1 Storage System

- 6.1.1 Direct Attached Storage (DAS)

- 6.1.2 Network Attached Storage (NAS)

- 6.1.3 Storage Area Network (SAN)

- 6.2 Storage Architecture

- 6.2.1 File and Object-based Storage (FOBS)

- 6.2.2 Block Storage

- 6.3 End User Industry

- 6.3.1 BFSI

- 6.3.2 Retail

- 6.3.3 IT and Telecom

- 6.3.4 Healthcare

- 6.3.5 Media and Entertainment

- 6.3.6 Other End-user Industries

- 6.4 Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia Pacific

- 6.4.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Dell Inc.

- 7.1.2 Hewlett Packard Enterprise Company

- 7.1.3 NetApp Inc.

- 7.1.4 Hitachi Ltd

- 7.1.5 IBM Corporation

- 7.1.6 Toshiba Corp.

- 7.1.7 Pure Storage Inc.

- 7.1.8 DataDirect Networks.

- 7.1.9 Scality Inc.

- 7.1.10 Fujitsu Ltd.

- 7.1.11 Netgear Inc.