|

市場調査レポート

商品コード

1685876

エチルベンゼン- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Ethylbenzene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| エチルベンゼン- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

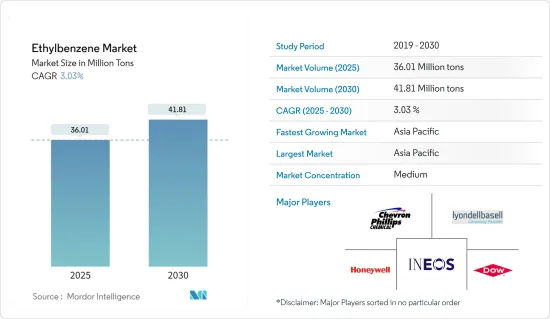

エチルベンゼンの市場規模は2025年に3,601万トンと推定され、予測期間(2025年~2030年)のCAGRは3.03%で、2030年には4,181万トンに達すると予測されます。

市場は2020年にCOVID-19によってマイナスの影響を受けました。しかし、2021年~22年には市場は大きく回復し、建設や自動車製造の活動によって、自動車ダッシュボード、外装パネル、スチレン-アクリルエマルション、塗料・コーティング用溶剤・試薬など、エチルベンゼン系ポリマーやその他の製品の需要が復活しました。パンデミック(世界的大流行)により、食品業界やeコマース業界からのパッケージング需要が増加し、市場調査を行いました。

主なハイライト

- 様々なエンドユーザー産業からのスチレン需要の増加と、天然ガス回収におけるエチルベンゼンの使用量の増加が市場の成長を牽引すると予想されます。

- 一方、エチルベンゼンの使用に関する厳しい規則が市場の成長を鈍らせる可能性が高いです。

- 塗料やコーティング剤、接着剤、洗浄剤など、さまざまな製品の生産における溶剤や試薬としてのエチルベンゼンの用途は、市場に新たな成長機会をもたらす可能性が高いです。

- アジア太平洋地域が世界市場を席巻し、中国や韓国などの国々が最大の消費国となっています。

エチルベンゼン市場の動向

スチレン生産が市場を独占

- スチレンの生産はエチルベンゼン市場の需要にプラスの影響を与えると思われます。スチレンは、アクリロニトリル-ブタジエン-スチレン、ポリスチレン、スチレン-ブタジエンエラストマーとラテックス、スチレン-アクリロニトリル樹脂、不飽和ポリエステルなど、いくつかの工業用ポリマーの前駆体です。

- 前述のスチレン系ポリマー、エラストマー、樹脂は、エレクトロニクス、包装、農業、石油化学、建築など、さまざまなエンドユーザー産業で幅広い用途を見出しています。ポリスチレンは、使い捨て用品、包装、低価格の消費者向け製品に主に使用されています。

- 世界銀行によると、2021年のスチレン系ポリマーの輸出上位国はオランダ(6億2,010万910米ドル)、トルコ(2億9,183万2,220米ドル)、ベルギー(2億4,861万9,880米ドル)、ギリシャ(2億4,847万1,970米ドル)でした。

- OECによると、2022年9月の中国のスチレン系ポリマー輸出は7,390万米ドルでした。2021年9月から2022年9月の間に、中国のスチレン系ポリマーの輸出は5,200万米ドルから7,390万米ドルに2,190万米ドル(42.1%)増加しました。

- 世界銀行によると、米国のスチレン系ポリマー(膨張性ポリスチレン)の一次形態の輸出は1億9,868万6,760米ドル、数量は97,729,500Kgでした。

- インドにおける環状炭化水素スチレンの輸入量は2021-22年度で907.04キロトンであり、国内の需要増に伴い消費量は増加すると思われます。

- スチレンの需要はゴムタイヤの需要増により継続的に伸びています。European Rubber Journalの年次世界セクター調査によると、中国の主要サプライヤーの売上高は2021年に前年比30%増の15億6,100万米ドルに達しました。来年はさらに増加すると予想されています。

- したがって、前述の要因は今後数年間、市場に大きな影響を与えると予想される

アジア太平洋地域が市場を独占する

- アジア太平洋地域が世界市場シェアを独占しています。中国、インド、日本などの国々では、建設業や包装業が成長し、塗料やコーティング剤、染料、香料、インク、合成ゴムなどの溶剤や試薬としての用途が増加しているため、この地域ではエチルベンゼンの使用量が増加しています。

- エチルベンゼンは主にスチレンの生産に使用され、さらに加工されてポリスチレンとなり、包装用製品の主原料となります。インド・ブランド・エクイティ財団によると、インドは世界市場において包装資材の主要輸出国として台頭してきています。インドからの包装資材の輸出は、2018-19年の8億4,400万米ドルから2021-22年には11億1,900万米ドルに増加しました。このような国内の包装需要の増加が、調査対象市場の需要を刺激しています。

- 公共インフラ、再生可能エネルギー、インフラ、商業プロジェクトに対する投資の増加に伴い、建設部門は今後数年間緩やかなペースで成長を記録すると予想され、それによって消費者と投資家の信頼がともに向上し、ひいては予測期間中にエチルベンゼンの需要を刺激します。

- 中国国家統計局によると、2021年の中国の建設企業の付加価値額は前年比2.1%増の8兆138億人民元(1兆2,484億2,000万米ドル)であり、これにより建設産業からの塗料・コーティング剤とエチルベンゼン系ポリマーの需要が高まり、ひいては研究市場の需要を刺激しています。

- 自動車用軽量材料の需要は、電気自動車セグメントからの需要増加により、この期間に増加しています。アクリロニトリル-ブタジエン-スチレンなどを含むエチルベンゼン系ポリマーは、ダッシュボード、外装パネル、バンパーなど、さまざまな自動車外装・内装部品の製造に使用されています。

- 2021年に中国で販売された乗用車は2,148万1,537台で、2020年の2,017万7,731台に比べ約6%増加しており、ダッシュボードなどの自動車部品の製造に使用される原材料の需要急増につながり、調査対象市場の需要にプラスの影響を与えました。

- インドの乗用車市場は、2020-21年度の243万3,473台に対し、2021-22年度の推定販売台数は308万2,279台と、27%という驚異的な伸びを示しました。

- 電子情報技術産業協会(JEITA)によると、デジタル化の進展が需要を押し上げ、輸出が拡大するなか、日本の電子・IT企業の2021年の世界生産額は前年比8%増の37兆3,000億円に達しました。このようなエレクトロニクス分野の成長は、今後数年間のエチルベンゼン市場の需要を高めると思われます。

- したがって、前述の要因は今後数年間、市場に大きな影響を与えると予想されます。

エチルベンゼン産業の概要

エチルベンゼン市場は、その性質上、部分的に断片化されています。主要企業には、LyondellBasell Industries Holdings B.V.、INEOS、Honeywell International Inc、Chevron Phillips Chemical Company LLC、Dowなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- スチレン需要の増加

- 天然ガス回収における使用の増加

- 抑制要因

- エチルベンゼンの使用に関する厳しい規制

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 技術スナップショット

- 生産プロセス

- 貿易分析

- 価格指数

- 規制政策分析

第5章 市場セグメンテーション

- 用途

- スチレン

- アクリロニトリル-ブタジエン-スチレン

- スチレン-アクリロニトリル樹脂

- スチレンブタジエンエラストマーとラテックス

- 不飽和ポリエステル樹脂

- ガソリン

- ジエチルベンゼン

- 天然ガス

- 塗料

- アスファルトとナフサ

- スチレン

- エンドユーザー産業

- 包装

- エレクトロニクス

- 建設

- 農業

- 自動車

- その他のエンドユーザー産業

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Carbon Holdings Limited(Cairo)

- Changzhou Dohow Chemical Co. Ltd

- Chevron Phillips Chemical Company LLC

- Cos-Mar Company

- Dow

- Guangdong Wengjiang Chemical Reagent Co., Ltd.

- Honeywell International Inc

- INEOS

- J&K Scientific Ltd.

- LyondellBasell Industries Holdings B.V.

- LLC'Gazprom neftekhim Salavat'

- PJSC "Nizhnekamskneftekhim"

- ROSNEFT

- Shanghai Myrell Chemical Technology Co., Ltd.

- Sibur-Khimprom CJSC

- TCI Chemicals(India)Pvt. Ltd.

- Versalis S.p.A.

- Westlake Chemical Corporation

第7章 市場機会と今後の動向

- 溶媒や試薬としての用途の拡大

The Ethylbenzene Market size is estimated at 36.01 million tons in 2025, and is expected to reach 41.81 million tons by 2030, at a CAGR of 3.03% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2020. However, the market recovered significantly in the 2021-22 period, and the construction and automotive manufacturing activities have reinstated the demand for ethylbenzene-based polymer and other products, including automotive dashboards, exterior panels, styrene-acrylic emulsions, solvents and reagents for paints and coatings, and others. The pandemic had increased the demand for packaging from the food and e-commerce industries, thereby stimulating the demand for the market studied.

Key Highlights

- The increasing demand for styrene from various end-user industries and the increasing usage of ethylbenzene in the recovery of natural gas are expected to drive the market's growth.

- On the other hand, strict rules about using ethylbenzene are likely to slow the growth of the market that was studied.

- Ethylbenzene application as a solvent and reagent in the production of various products, such as paints and coatings, adhesives, and cleaning materials, will likely provide new growth opportunities for the market.

- Asia-Pacific dominated the market across the world, with the largest consumption coming from countries such as China and South Korea.

Ethylbenzene Market Trends

Styrene Production to Dominate the Market

- Styrene production will have a positive influence on ethylbenzene market demand. Styrene is a precursor to several industrial polymers, including acrylonitrile-butadiene-styrene, polystyrene, styrene-butadiene elastomers and latex, styrene-acrylonitrile resins, and unsaturated polyester.

- The aforementioned styrene-based polymers, elastomers, and resins find a wide range of applications in various end-user industries, such as electronics, packaging, agriculture, petrochemicals, and construction. Polystyrene is majorly used in disposables, packaging, and low-cost consumer products.

- According to World Bank, in 2021, the top exporters of styrene polymers were the Netherlands (USD 620,100.91 thousand), Turkey (USD 291,832.22 thousand), Belgium (USD 248,619.88 thousand), and Greece (USD 248,471.97 thousand).

- According to OEC, in September 2022 China's styrene polymers exports accounted for USD 73.9 million. Between September 2021 and September 2022 the exports of China's styrene polymers have increased by USD 21.9 million (42.1%) from USD 52 million to USD 73.9 million.

- According to the World Bank, United States exports of styrene polymers (expansible polystyrene) in primary forms was USD 198,686.76 thousand and a quantity of 97,729,500 Kg.

- The cyclic hydrocarbon styrene imports in India stood at 907.04 kilotons in FY2021-22, and the consumption is likely to increase as per the rising demand in the country.

- The demand for styrene is continuously growing due to an increased demand for rubber tires. According to the European Rubber Journal's annual global sector survey, sales among leading Chinese suppliers increased by 30% year-on-year in 2021 to reach USD 1,561 million. It is further expected to increase in the upcoming year

- Therefore, the aforementioned factors are expected to significantly impact the market in the coming years

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominated the global market share. With growing construction and packaging industries and increasing applications as solvents and reagents in paints and coatings, dyes, perfumes, inks, and synthetic rubber in countries such as China, India, and Japan, the usage of ethylbenzene has been increasing in the region.

- Ethylbenzene is mainly used for the production of styrene, which further gets processed to form polystyrene, a major raw material for packaging products. According to the India Brand Equity Foundation, India is emerging as a key exporter of packaging materials in the global market. The export of packaging materials from India grew to USD 1,119 million in 2021-22 from USD 844 million in 2018-19. This increase in the demand for packaging within the country is stimulating the demand for the market studied.

- With increasing investments in public infrastructure, renewable energy, infrastructure, and commercial projects, the construction sector is expected to record growth at a moderate pace over the next few years, thereby improving both consumer and investor confidence and, in turn, stimulating the demand for ethylbenzene over the forecast period.

- According to the National Bureau of Statistics of China, in 2021, the value added of construction enterprises in China was CNY 8,013.8 billion (USD 1,248.42 billion), up by 2.1 percent over the previous year, thereby enhancing the demand for paints and coatings and ethylbenzene-based polymers from the construction industry, which in turn stimulates the demand for the studied market.

- The demand for lightweight automotive materials has increased during this period, owing to the increased demand from the electric vehicle segment. Ethylbenzene-based polymers, including acrylonitrile-butadiene-styrene and others, are used for manufacturing various automotive exterior and interior parts, including dashboards, exterior panels, bumpers, and others.

- In 2021, around 2,14,81,537 passenger cars were sold in China compared to 2,01,77,731 passenger cars sold in 2020, witnessing an increase of about 6%, thus leading to a surge in the demand for raw materials used to produce automotive parts such as dashboards, among others, which in turn positively impacted the demand for the market studied.

- The Indian passenger vehicle market saw a staggering 27% growth, as the sales estimated for FY2021-22 are 30,82,279, compared to 24,33,473 in FY 2020-21.

- According to the Japan Electronics and Information Technology Industries Association (JEITA), with the advance of digitalization boosting demand and expanding exports, global production by Japanese electronics and IT companies grew by 8% year on year in 2021, reaching JPY 37,300 billion. This growth in the electronics segment will enhance the demand for the ethylbenzene market in the coming years.

- Therefore, the aforementioned factors are expected to have a significant impact on the market in the coming years.

Ethylbenzene Industry Overview

The ethylbenzene market is partially fragmented in nature. The major companies include LyondellBasell Industries Holdings B.V., INEOS, Honeywell International Inc, Chevron Phillips Chemical Company LLC, and Dow, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Styrene

- 4.1.2 Increasing Use in Recovery of Natural Gas

- 4.2 Restraints

- 4.2.1 Strict Regulations on the Use of Ethylbenzene

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Technological Snapshot

- 4.5.1 Production Process

- 4.6 Trade Analysis

- 4.7 Price Index

- 4.8 Regulatory Policy Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Styrene

- 5.1.1.1 Acrylonitrile-Butadiene-Styrene

- 5.1.1.2 Styrene-Acrylonitrile Resins

- 5.1.1.3 Styrene-Butadiene Elastomers and Latex

- 5.1.1.4 Unsaturated Polyester Resins

- 5.1.2 Gasoline

- 5.1.3 Diethylbenzene

- 5.1.4 Natural Gas

- 5.1.5 Paint

- 5.1.6 Asphalt and Naphtha

- 5.1.1 Styrene

- 5.2 End-user Industry

- 5.2.1 Packaging

- 5.2.2 Electronics

- 5.2.3 Construction

- 5.2.4 Agriculture

- 5.2.5 Automotive

- 5.2.6 Other End-User Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Carbon Holdings Limited (Cairo)

- 6.4.2 Changzhou Dohow Chemical Co. Ltd

- 6.4.3 Chevron Phillips Chemical Company LLC

- 6.4.4 Cos-Mar Company

- 6.4.5 Dow

- 6.4.6 Guangdong Wengjiang Chemical Reagent Co., Ltd.

- 6.4.7 Honeywell International Inc

- 6.4.8 INEOS

- 6.4.9 J&K Scientific Ltd.

- 6.4.10 LyondellBasell Industries Holdings B.V.

- 6.4.11 LLC 'Gazprom neftekhim Salavat'

- 6.4.12 PJSC "Nizhnekamskneftekhim"

- 6.4.13 ROSNEFT

- 6.4.14 Shanghai Myrell Chemical Technology Co., Ltd.

- 6.4.15 Sibur-Khimprom CJSC

- 6.4.16 TCI Chemicals (India) Pvt. Ltd.

- 6.4.17 Versalis S.p.A.

- 6.4.18 Westlake Chemical Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing use in applications as solvent and reagents