|

市場調査レポート

商品コード

1939123

チタン合金:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Titanium Alloy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| チタン合金:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

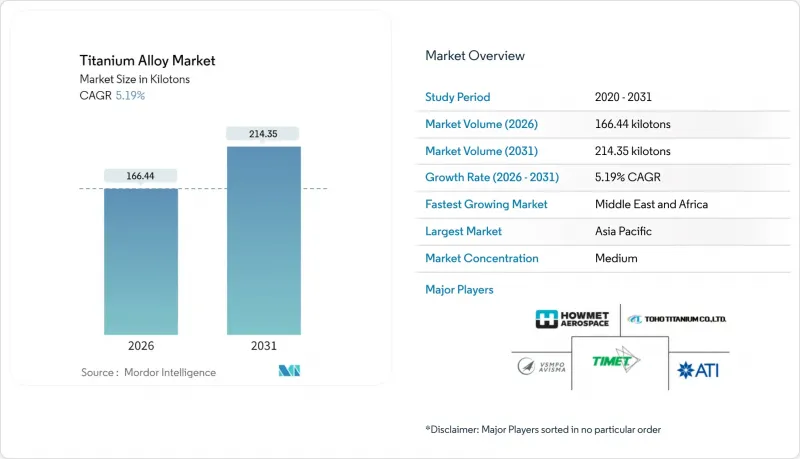

チタン合金市場は、2025年の158.23キロトンから2026年には166.44キロトンへ成長し、2026年から2031年にかけてCAGR5.19%で推移し、2031年までに214.35キロトンに達すると予測されています。

ボーイング社およびエアバス社における継続的な受注残、防衛調達サイクルの回復、ならびに拡大する医療用インプラント顧客基盤が需要を支えています。持続的な成長は、チタニウムの高い強度重量比、耐食性、生体適合性といった特性に依存しており、これらの特性は重要な用途において依然として高い製造コストを上回っています。生産者は供給ボトルネックを緩和するため、水素補助還元法や積層造形技術などを通じて溶解能力を増強しており、顧客は地政学的リスクを軽減するために調達先の多様化を進めています。コスト削減イノベーションと燃費効率の高い航空機に対する規制強化が、チタニウム合金市場の成長ストーリーをさらに強化しています。

世界のチタン合金市場の動向と洞察

航空宇宙・防衛分野における機体需要の拡大

15,000機を超える民間航空機の受注により、チタンは構造部品、着陸装置、エンジン部品に確実に採用されています。軽量化は燃料節約に直結するためです。ATI社は2025年第1四半期の収益の66%を航空宇宙・防衛分野から得ており、エアバス社とは5年間で10億米ドル規模の供給契約を締結しました。ハウメット・エアロスペース社は、エンジン需要の急増により、2024年第3四半期に民間航空宇宙分野の売上高が17%増加しました。現在、ジェットエンジンの重量に占めるチタンの割合は15~25%に達しており、防衛プログラムではステルス性と耐久性を考慮してこの合金が指定されています。ロシア産原料からの脱却に向けた多様化が進み、日本や中東のサプライヤーとの新たな提携が促進されており、チタン合金市場の生産再編が強化されています。

軍事用地上車両の軽量化プログラム

防衛計画担当者は、防護性能を損なうことなく航続距離と積載量を向上させるため、装甲・駆動系・サスペンションにおいて鋼鉄からチタニウムへの切り替えを加速しています。米国防総省がIperionX社に授与した4,710万米ドルの契約は、安全かつ低コストなチタン生産能力の確保に向けた国家的な取り組みを裏付けています。材料仕様を調和させるNATO規格は国境を越えた需要を拡大し、実戦データでは鋼鉄部品をチタン部品に置き換えた場合、15~20%の燃料節約効果が確認されています。先進的な製造技術により部品点数が削減され、配備車両群の保守負担が軽減されることで、チタン合金市場の長期的な成長が促進されています。

高コスト生産と複雑な冶金技術

従来のクロール法では1トンあたり11~13MWhを消費するため、チタニウムはアルミニウムの3~4倍、鋼鉄の10~15倍のコストがかかります。反応性冶金学では不活性雰囲気と特殊切削油が必要であり、下流工程の機械加工における生産性を阻害しています。水素補助還元プロセスは低温化を可能としますが、まだ商業化前段階です。東京大学のイットリウム反応による酸素除去技術はコスト削減の可能性を秘めていますが、産業規模での実用化には数年を要します。新プロセスが成熟するまでは、高い転換コストがチタン合金市場の潜在的可能性を制限しています。

セグメント分析

ベータ合金は2031年までにCAGR6.02%で推移すると予測される一方、アルファーベータ系グレードは2025年にチタン合金市場シェアの51.12%を占めました。Ti-5553は優れた鋳造性を示し、主翼貫通部や着陸装置構造に不可欠な高強度重量比を実現します。ジルコニウムとハフニウムを組み込んだ高エントロピー金属間化合物の調査により、8%の塑性ひずみで1.5GPaの降伏強度を達成し、極超音速用途の選択肢を拡大しています。

進行中の積層造形技術の導入により、ニアネットシェイプ生産が可能となり、調達から飛行までの比率を最大60%削減するとともに、タービンブレードの複雑な冷却通路構造を支えています。ベータ系合金のチタン合金市場規模は、粉末微粒化能力と重要飛行機器の認証試験における相乗効果に支えられ、この10年を全体の約25%で締めくくる見込みです。500℃以上の高温環境向けアルファ合金およびニアアルファ合金への並行的な関心は、ガスタービンや宇宙推進分野での需要を維持しています。メーカーが真空アーク再溶解パラメータを標準化するにつれ、合金組成が安定化し、航空宇宙・防衛主要メーカーの信頼性が向上しています。

本チタン合金レポートは、微細構造(αおよび近α、αーβ、β)、エンドユーザー産業(航空宇宙、自動車・造船、化学処理、発電・海水淡水化、医療・歯科インプラント、その他エンドユーザー産業)、地域(アジア太平洋、北米、欧州、南米、中東・アフリカ)別に分類されています。市場予測は数量(キロトン)単位で提供されます。

地域別分析

2025年、アジア太平洋地域はチタン合金市場の41.02%を占め、中国が世界の金属生産量の60%を占めることがその基盤となっています。しかしながら、同地域の航空宇宙分野における認証の遅れが、高付加価値のジェット機プログラムへの即時参入を妨げています。インドはHALおよびDRDOと連携し、国産スポンジチタンの生産能力拡大に取り組んでおります。一方、オーストラリアの鉱山企業は、バリューチェーン上流での利益確保を目指し、下流の合金製造分野への進出を進めております。これらの取り組みは、品質面の課題が残るもの、総生産量の堅調な増加を支えるものとなっております。

中東・アフリカ地域はCAGR5.85%で拡大しており、サウジアラビアの460億米ドル規模の鉱業戦略の恩恵を受けています。同戦略は2030年までに鉱業のGDPシェアを750億米ドルに引き上げ、同王国を中立的なチタン供給国とすることを目指しています。北米ではスポンジ生産量が最小限であるにもかかわらず、消費量は高水準を維持しています。ノースカロライナ州カンバーランド郡では、水素補助還元法による国内生産能力再構築のため8億6,700万米ドルの工場を確保し、フル稼働時には年間1万トンの供給が可能となる見込みです。カナダでは、ケベック州の水力発電を利用したイルメナイト事業が、低炭素スポンジへの垂直統合を模索しています。

大西洋を隔てた欧州では、OEM各社が制裁順守と生産継続の両立に苦慮し、カザフスタンや日本のサプライヤーとの合弁事業が協議されています。EUの重要原材料法により、ノルウェーとスペインにおけるスポンジプロジェクトの許可手続きが迅速化されました。南米は依然として主に原料鉱石の輸出地域ですが、ブラジルの国営開発銀行は、既存のイルメナイト鉱山近隣における下流合金プラントへの共同融資に関心を示しています。全体として、供給基盤の変容がチタン合金市場の再構築を継続的に進めています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3か月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 航空宇宙・防衛分野における機体需要の拡大

- 軍事用地上車両の軽量化プログラム

- 医療・歯科インプラント処置の拡大

- 積層造形技術による新規グレードの開拓

- 新興水素経済における熱交換器の需要

- 市場抑制要因

- 高コストな生産と複雑な冶金技術

- 世界のスポンジ生産能力の制約

- ロシア産原料への地政学的依存

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 微細構造別

- アルファおよびニアアルファ

- アルファーベータ

- ベータ

- エンドユーザー業界別

- 航空宇宙

- 自動車および造船

- 化学処理

- 電力・海水淡水化

- 医療・歯科用インプラント

- その他のエンドユーザー産業(石油・ガスなど)

- 地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ロシア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)**/順位分析

- 企業プロファイル

- ATI

- Alleima

- AMG

- BAOTI Group Co.,Ltd.

- Corporation VSMPO-AVISMA

- CRS Holdings, LLC

- Daido Steel Co., Ltd.

- Hermith GmbH

- Howmet Aerospace

- KOBE STEEL, LTD.

- OSAKA Titanium Technologies Co.,Ltd.

- Perryman Company

- PJSC VSMPO-AVISMA Corporation

- TIMET(Precision Castparts Corp.)

- Toho Titanium Co., Ltd.

- Weber Metals(OTTO FUCHS Kommanditgesellschaft)

- Western Superconducting Technologies Co., Ltd