感圧接着剤(PSA):市場シェア分析、産業動向、成長予測(2025~2030年)

Pressure Sensitive Adhesives (PSA) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1637794

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

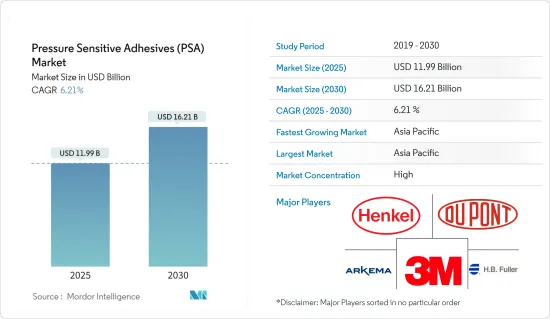

感圧接着剤(PSA)の市場規模は2025年に119億9,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは6.21%で、2030年には162億1,000万米ドルに達すると予測されます。

COVID-19の発生により、2020年には世界中で全国的な封鎖、製造活動やサプライチェーンの混乱、生産停止が発生し、市場にマイナスの影響を与えました。しかし、2021年には状況が回復し始め、市場の成長軌道が回復しました。

主なハイライト

- 市場を牽引している主な要因は、低コストでフレキシブルなパッケージングの開発が進んでいることと、硬化時間が短い感圧接着剤(PSA)の使用が増加していることです。

- その反面、VOC排出に関する厳しい環境規制や、UV硬化型接着剤のような代替品の使用増加が市場成長の妨げになると予想されます。

- テープ分野は市場を独占しており、予測期間中も成長が見込まれています。これは、包装、医療、輸送などのエンドユーザー産業が成長しているためです。

- バイオベースの感圧接着剤(PSA)の採用や、ナノテクノロジーをベースとした機能性感圧接着剤(PSA)の開発は、今後のチャンスとなりそうです。

- アジア太平洋地域が世界市場を独占し、中国やインドなどの国による消費が最も多いです。

感圧接着剤(PSA)の市場動向

包装産業が市場を独占

- 接着剤は、製品パッケージが消費者に届くまで無傷であることを保証します。パッケージング業務では、複数の新製品や製品の急増に伴い、ますます複雑化するパッケージング需要に対応するため、信頼性の高い接着剤が必要とされています。

- 感圧接着剤(PSA)は、特に包装業界にいくつかの利点を提供します:

- 迅速なリワーク:再加工や再包装はコストを増加させます。PSAは、製品が規格に適合し、棚に並べられるようにするタイムリーな方法を提供します。感圧接着剤(PSA)はスティックのりよりも安全で、従来のテープよりも目立たないです。スティックのりとは異なり、感圧接着剤(PSA)は塗布時に熱を必要としません。熱がないため火傷の心配がなく、工場で働く人々の安全性が向上します。さらに、PSAはパッケージンググラフィックの邪魔にならず、ブランドイメージを損なうことなく必要な粘着力を提供します。感圧接着剤(PSA)は、ブランドのインパクトを維持し、最大化する、目立ちにくいパッケージングソリューションです。

- 即時接着:感圧接着剤(PSA)を塗布すると、硬化するまで待つ必要がないため、時間の節約になります。感圧接着剤(PSA)を塗布すると、接着と同時に基材が圧縮されます。瞬時に接着できるため、処理速度が向上し、生産性も向上します。

- ブランドイメージの維持ブランドイメージはパッケージの外観に大きく依存します。PSAは、パッケージングにダメージを与えたり、残留物を残したりすることなく、きれいに剥がせる接着剤を提供します。ブランドイメージの維持は、消費者へのアピールにつながります。

- さらに、ここ数年、パッケージング業界は、製造業や産業部門がフレキシブル・パッケージングに適応する転換期を迎えています。

- 軽量で扱いやすく、場所をとらず、保存期間が長く、輸送が容易で、破損しにくく、印刷適性に優れているなどの利点があるため、パッケージングが普及しました。

- eコマース、eリテール、食品のオンライン注文や宅配サービスの増加傾向に伴い、包装材料、特に軟包装の需要が増加しており、予測期間中にUV硬化型接着剤の需要を牽引する可能性が高いです。ドイツでは、2022年に紙包装産業が以前に比べて大きく成長しました。

- インド包装産業協会(PIAI)によると、インドの包装産業は予測期間中に22%の成長が見込まれています。さらに、インドの包装市場は2025年までに2,048億1,000万米ドルに達すると予想されています。

- 軟包装は、低所得の南米、アフリカ、アジア太平洋諸国の食品包装用途で使用されています。新興国では軟包装の人気と需要が高まっており、継続的な景気拡大と飲食品産業の加速が需要を支えています。

- ドイツでは2022年に紙製包装産業が大きく成長したが、これはさまざまなエンドユーザー産業向けの非化石ベースの包装に対する需要が増加しているためです。

- このような要因により、予測期間中、感圧接着剤(PSA)市場の需要は増加すると思われます。

アジア太平洋地域が市場を独占する見込み

- 世界需要の40%以上を占めるアジア太平洋地域は、感圧接着剤(PSA)にとって最も有望な市場であり、近いうちに支配することになると思われます。この支配は、同地域のテープやラベルの需要拡大に起因しています。

- 中国、インド、日本、韓国は、感圧接着剤(PSA)の需要の80%以上を占めています。

- 中国は粘着製品(テープ、ラベルなど)の主要輸出国のひとつです。多くの顧客にとって重要なのは、製品の品質、ベンダーが提供する製品群、接着剤の使用量と無駄の削減です。従って、現在、感圧接着剤(PSA)の中国市場は国際的なプレーヤーが支配しています。同じ要因が、国内の主要市場シェアを獲得するために研究開発に投資する地元メーカーを後押ししています。

- 中国は、一人当たり所得の増加とeコマース大手の台頭により、世界最大のパッケージング消費国となっています。インドプラスチック工業協会によると、インドの包装産業は世界第5位で、年間約22~25%の成長率を示しています。高度に熟練した労働力と安価な人件費により、包装・加工食品のコストは欧州よりも40%低く抑えることができます。人口の増加と包装需要の増加が市場を牽引すると予想されます。

- さらに、中国の包装産業は、経済の拡大と購買力の高い中間層の台頭により、近年一貫して急成長を遂げています。食品包装は包装業界の主要企業であり、中国における市場シェアの約60%を占めています。Interpakによると、中国の食品包装カテゴリーでは、包装総量は2023年に4,470億個に達すると予想されており、包装業界からの感圧接着剤(PSA)に対する需要の増加を示しています。

- インドの感圧接着剤(PSA)市場は高い成長率が見込まれます。その用途は、透明ラベルやフィルムラベル、FMCG(Fast-Moving Consumer Goods)メーカー向けのシュリンクラップラベル、フレキシブルラベル、マルチカラーラップアラウンドラベルで増加しました。感圧接着剤(PSA)市場はまだ初期の成長段階にあり、将来の成長展望はより高いです。

- アジア太平洋の大きな成長と相まって、大きな市場規模が感圧接着剤(PSA)市場の拡大に寄与しています。

感圧接着剤(PSA)産業の概要

感圧接着剤(PSA)市場は統合されています。主要企業7社で60%近くを占めています。主要企業(順不同)には、3M、Arkema、DuPont、HB Fuller、Henkel AG &Co.KGaAです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 低コストフレキシブルパッケージングの開発増加

- 硬化時間が短いPSAの使用増加

- その他の促進要因

- 抑制要因

- VOC排出に関する厳しい環境規制

- UV硬化型接着剤のような代替品の使用増加

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- テクノロジー別

- 水性

- 溶剤系

- ホットメルト

- 放射線

- 樹脂別

- アクリル

- シリコーン

- エラストマー

- その他の樹脂

- 用途別

- テープ

- ラベル

- グラフィック

- その他の用途

- エンドユーザー産業別

- 包装

- 木工・建具

- 医療

- 商業グラフィック

- 運輸

- エレクトロニクス

- その他エンドユーザー産業

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋地域

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Arkema Group(Bostik SA)

- Ashland Inc.

- Avery Dennison Corp.

- DuPont

- Franklin International

- H.B. Fuller Co.

- Helmitin Adhesives

- Henkel AG & Co. KGaA

- Huntsman Corporation

- Illinois Tool Works Inc.

- Jowat AG

- Mapei SPA

- Master Bond

- Pidilite Industries Ltd

- Sika AG

- Tesa SE(A Beiersdorf Company)

- Wacker Chemie AG

第7章 市場機会と今後の動向

- バイオベースの感圧接着剤(PSA)の採用

- ナノテクノロジーに基づく機能性感圧接着剤(PSA)の開発

目次

The Pressure Sensitive Adhesives Market size is estimated at USD 11.99 billion in 2025, and is expected to reach USD 16.21 billion by 2030, at a CAGR of 6.21% during the forecast period (2025-2030).

Due to the COVID-19 outbreak, nationwide lockdowns worldwide, disruption in manufacturing activities and supply chains, and production halts negatively impacted the market in 2020. However, the conditions started recovering in 2021, restoring the market's growth trajectory.

Key Highlights

- The major factor driving the market studied is the increasing development of low-cost, flexible packaging and increasing usage of pressure-sensitive adhesives because of lesser curing time.

- On the flip side, stringent environmental regulations regarding VOC emissions and increasing usage of substitutes like UV-cured adhesives are expected to hinder the studied market's growth.

- The tapes segment dominated the market and is expected to grow during the forecast period. It is owing to the growing end-user industries, such as packaging, medical, and transportation.

- Adopting bio-based pressure-sensitive adhesives and developing nanotechnology-based functional pressure-sensitive adhesives is likely an opportunity in the future.

- Asia-Pacific dominated the global market, with the largest consumption from countries such as China and India.

Pressure Sensitive Adhesives Market Trends

Packaging Industry to Dominate the Market

- Adhesives ensure the product packaging remains intact until it reaches the consumer. Packaging operations require a reliable adhesive to meet the increasingly complex packaging demands as there is an increase in several new products and product proliferation.

- Pressure-sensitive adhesives (PSAs) specifically offer several advantages for the packaging industry:

- Quick reworks: Reworking or repackaging increases costs. PSAs offer a timely way to make products compliant and shelf-ready. Pressure-sensitive adhesives are safer than glue sticks and more discrete than traditional tape. Unlike glue sticks, pressure-sensitive adhesives do not require heat during application. The absence of heat eliminates burns and increases safety among plant workers. Additionally, PSAs are less intrusive on packaging graphics, providing the required adhesion without sacrificing the brand image. Pressure-sensitive adhesives are less visible packaging solutions that preserve and maximize the brand's impact.

- Instant bond: Applying pressure-sensitive adhesives is time-saving, as waiting until they cure is unnecessary. When applied, they compress the substrate right when adhesion occurs. Instant bonding increases the processing speed, as well as improves production.

- Maintaining brand image: Brand image relies heavily on the packaging appearance. PSAs provide a bond that removes cleanly without damaging the packaging or leaving behind residue. Preserving brand image adds to your consumer appeal.

- Furthermore, in the last few years, the packaging industry is experiencing a transition where the manufacturing and industrial sector is adapting to flexible packaging.

- The benefits, such as being lightweight, easy to handle, less space-consuming, longer shelf life, easy transit, damage resistance, and better printability, made packaging popular.

- With the growing trend of e-commerce, e-retail, and online food orders and delivery services, the demand for packaging materials, especially flexible packaging, is increasing, likely to drive the demand for UV-curable adhesives during the forecast period. In Germany, the paper packaging industry grew significantly in 2022 compared to previous years.

- According to the Packaging Industry Association of India (PIAI), the Indian packaging industry is expected to grow at 22% during the forecast period. Moreover, the Indian packaging market is expected to reach USD 204.81 billion by 2025.

- Flexible packaging is used in food packaging applications in low-income South America, Africa, and Asia-Pacific countries. The popularity and demand for flexible packaging are rising in emerging economies, and the demand is supported by continued economic expansion and an acceleration in the food and beverage industry.

- The paper packaging industry grew significantly in Germany in 2022 because of the increasing demand for non-fossil-based packaging for different end-user industries.

- Such factors will likely increase the demand for the pressure-sensitive adhesives market over the forecast period.

Asia-Pacific Region is Expected to Dominate the Market

- With over 40% of the global demand, Asia-Pacific is the most promising market for pressure-sensitive adhesives, which will likely dominate soon. This domination can be attributed to the region's growing demand for tapes and labels.

- China, India, Japan, and South Korea account for over 80% of the demand for pressure-sensitive adhesives.

- China is one of the major exporters of adhesive products (tapes, labels, etc.). The factors concerning most of its customers are the product quality, the product range offered by the vendor, and reducing the dosage and wastage of adhesives. Therefore, international players currently dominate the Chinese market for pressure-sensitive adhesives. The same factor encourages local producers to invest in R&D to acquire a major national market share.

- China is the world's largest packaging consumer globally, owing to growing per capita income and rising e-commerce giants. India's packaging industry is the fifth-largest globally, growing at about 22-25% per year, according to the Plastics Industry Association of India. Packaging and processing food costs can be 40% lower than in Europe because of highly skilled labor and cheap labor costs. The growing population and increasing demand for packaging are expected to drive the market.

- Furthermore, the Chinese packaging industry grew rapidly and consistently in recent years, owing to the expanding economy and rising middle class with greater purchasing power. Food packaging is a major player in the packaging industry, accounting for roughly 60% of the total market share in China. According to Interpak, in China, in the foodstuff packaging category, total packaging is expected to reach 447 billion units in 2023, indicating an increased demand for pressure-sensitive adhesives from the packaging industry.

- The pressure-sensitive adhesives market in India is expected to grow at a higher rate. Its usage increased with transparent and film labels, shrink-wrap labels for fast-moving consumer goods (FMCG) manufacturers, flexible labels, and multicolor wrap-around labels. The pressure-sensitive adhesives market is still in its early growth stage, with a higher scope of growth in the future.

- The large market size, coupled with the huge growth of Asia-Pacific, is instrumental in expanding the pressure-sensitive adhesives market.

Pressure Sensitive Adhesives Industry Overview

The pressure-sensitive adhesives market is consolidated. The top seven players account for almost 60%. The major companies (not in any particular order) include 3M, Arkema, DuPont, HB Fuller, and Henkel AG & Co. KGaA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Development of Low-cost Flexible Packaging

- 4.1.2 Increasing Usage of PSA Because of Lesser Curing Time

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations Regarding VOC Emissions

- 4.2.2 Increasing Usage of Subsitutes like UV Cured Adhesives

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Technology

- 5.1.1 Water-based

- 5.1.2 Solvent-based

- 5.1.3 Hot Melt

- 5.1.4 Radiation

- 5.2 Resin

- 5.2.1 Acrylics

- 5.2.2 Silicones

- 5.2.3 Elastomers

- 5.2.4 Other Resins

- 5.3 Application

- 5.3.1 Tapes

- 5.3.2 Labels

- 5.3.3 Graphics

- 5.3.4 Other Applications

- 5.4 End-user Industry

- 5.4.1 Packaging

- 5.4.2 Woodworking and Joinery

- 5.4.3 Medical

- 5.4.4 Commercial Graphics

- 5.4.5 Transportation

- 5.4.6 Electronics

- 5.4.7 Other End-user Industries

- 5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema Group (Bostik SA)

- 6.4.3 Ashland Inc.

- 6.4.4 Avery Dennison Corp.

- 6.4.5 DuPont

- 6.4.6 Franklin International

- 6.4.7 H.B. Fuller Co.

- 6.4.8 Helmitin Adhesives

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Huntsman Corporation

- 6.4.11 Illinois Tool Works Inc.

- 6.4.12 Jowat AG

- 6.4.13 Mapei SPA

- 6.4.14 Master Bond

- 6.4.15 Pidilite Industries Ltd

- 6.4.16 Sika AG

- 6.4.17 Tesa SE (A Beiersdorf Company)

- 6.4.18 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Adoption of Bio-based Pressure Sensitive Adhesives

- 7.2 Development of Nanotechnology based Functional Pressure Sensitive Adhesives

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日