|

|

市場調査レポート

商品コード

1444032

臨床意思決定支援システム: 市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Clinical Decision Support Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 臨床意思決定支援システム: 市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

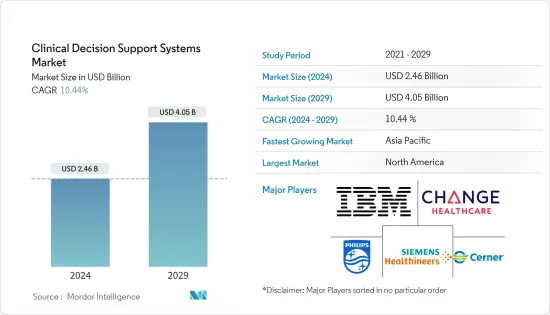

臨床意思決定支援システム市場規模は、2024年に24億6,000万米ドルと推定され、2029年には40億5,000万米ドルに達すると予測され、予測期間(2024~2029年)のCAGRは10.44%で成長する見込みです。

COVID-19が大流行するなか、各国の医療システムはオンライン・サービスに大きく依存していました。ヘルスケアの専門家たちは、バーチャルな情報源を通じて患者の診察を受けていました。これは主に、パンデミックの初期段階で各国政府が厳しい封鎖規制を課したためです。さらに、世界中でCOVID-19が大流行したため、臨床判断支援システムは患者のリソースやサービスを支援する上で重要な役割を果たしました。例えば、2021年3月に発表されたPlos One誌の論文では、COVID-19のリアルタイムの臨床診断のための意思決定支援ツールの開発は、患者のトリアージを支援し、リスクのある患者にリソースを割り当てる上で極めて重要であると述べられています。いくつかの国ではオンラインサービスの提供が増加しており、これが市場を押し上げています。さらに、さまざまな市場企業がCOVID-19データと洞察の管理のための臨床意思決定支援システムを発売しました。例えば、2022年5月、Epocratesは、臨床意思決定支援ガイドラインのライブラリを拡張するために、最新の更新を組み込んだ革新的な長いCOVID-19ツールを発売しました。このように、臨床意思決定支援システムの導入と発売の増加は、パンデミックの間に市場の成長を後押ししました。

医療費削減に対する需要の高まり、ケアの質の向上に対するニーズ、病院におけるヘルスケアITの技術的進歩は、臨床意思決定支援システム(CDSS)市場の成長を後押しすると思われる主な要因です。さらに、経済協力開発機構(OECD)の調査報告書によると、2021年の1人当たりの平均医療費は、ドイツで約7,382.6米ドル、ノルウェーで7,064.8米ドル、スウェーデンで6,262.3米ドルでした。したがって、医療費の高さも市場の成長に寄与すると予想されます。

2022年11月に発表されたScience directの研究によると、ハイブリッド最適化学習アルゴリズムは、精度、感度、特異度の指標を有していました。その結果、提案されたモデルは社会不安障害の診断に極めて適切であり、他の研究結果と一致していることが明らかになった。臨床意思決定支援システムのこのような効率性は、市場の成長に寄与すると予想されます。

さらに、老年人口の増加も市場の成長に寄与すると予想されます。2022年10月に発表されたWHOのデータによると、60歳以上の人口は2030年には14億人に増加し、2050年には21億人に達すると予測されています。2022年の国連報告書では、65歳以上の人口に占める割合が2022年の10%から2050年には16%に上昇すると予測されています。慢性疾患を発症しやすく、疾病予防のために定期的な健康診断や治療を必要とする老年人口は、高度な臨床意思決定支援システムの需要を促進し、市場の成長に貢献すると予想されます。

さらに、臨床意思決定支援システム開発のための共同研究やパートナーシップなどのイニシアチブの増加が、市場の成長に寄与すると期待されています。例えば、2021年6月、グーグル・クラウドは全国病院チェーンのHCAヘルスケアと複数年契約を締結し、臨床意思決定を改善するためにカスタマイズされたヘルスケアアルゴリズムを作成しました。

このように、医療費の増加や臨床意思決定支援システムの市場開拓に向けた取り組みの増加は、市場の成長に寄与すると期待されています。しかし、CDSSは開発の初期段階にあるため、システムに対する信頼の欠如、熟練労働者の不足、不必要な診断検査をCDSSから提案されることなどが市場開拓の妨げとなっています。

CDSS市場の動向

予測期間中、クラウドベースのセグメントが大きな市場シェアを占める見込み

ヘルスケア支出の増加とクラウドコンピューティングの採用が、クラウドベースセグメントの市場拡大の主な要因となっています。欧州地域の各国政府は、ヘルスケアにおける情報技術の成長を支援する取り組みを進めています。例えば、英国政府は2021年2月、完全に接続されたクラウド主導の医療サービスを採用するイニシアチブを開始しました。このイニシアチブの下、200万を超える国民保健サービス(NHS)のメールボックスがマイクロソフトのAzure Cloudに移行されました。これにより、NHSの組織や部門を超えたスタッフ間の円滑で効率的なコミュニケーションが可能になり、情報へのアクセスも改善されます。これにより、英国における(ヘルスケア情報技術)HCIT変更管理サービスの利用が増加し、市場の成長が促進されます。

さらに、臨床意思決定支援システム(CDSS)のローカルナレッジマネジメントでは、大規模な処理能力とストレージ容量が必要となる場合があり、運用コストが高くなる可能性があります。対照的に、クラウドベースのアプリケーションは遠隔地のサーバーで運用されるため、実行する際にユーザーの端末に大量の計算能力や大容量のストレージを必要としないです。

クラウドベースのアプリケーションはウェブブラウザに依存しないため、ウェブベースのアプリケーションよりも本質的に安全です。クラウドベースの臨床判断支援システムでは、処理装置は遠隔地のサーバーにホストされ、そのサーバーは世界中の複数のデータセンターに配置できるため、サイバー攻撃に対する脆弱性が低くなります。クラウド技術を利用できるようになったことで、クラウドベースのCDSSの利用が予測期間中に増加すると予想されます。

予測期間中、北米が市場で大きなシェアを占める見込み

北米の臨床意思決定支援システム(CDSS)市場は、CDSSの技術的進歩、患者の高い認知度、ヘルスケアITソリューションへの投資の増加によって牽引されています。

また、北米におけるヘルスケア支援のための政府からの資金援助が増加していることも、米国における市場成長の要因となっています。例えば、米国議会予算局(2021年)は、過去数十年間で、国立衛生研究所(NIH)に対する連邦政府の資金は総額7,000億米ドルを超えたと発表しています。

さらに、様々な市場プレーヤーがこの地域でますます先進的な製品を発売していることも、市場の成長に寄与すると期待されています。例えば、2021年8月、First Databank, Inc.は、ラスベガスで開催された2021 HIMSS Global conference and exhibitionにおいて、FDB CDS Analyticsを発表しました。このソリューションにより、ヘルスケアプロバイダー組織は、電子カルテにおける臨床意思決定支援を容易に特定、監視、カスタマイズできるようになります。

同様に、2021年6月、カナダのヘルスケア企業Pathwayは、プロバイダーにエビデンスに基づく臨床支援を提供し、その最初の資金調達ラウンドで130万米ドルを調達しました。この資金調達により、同社は臨床意思決定支援システムを強化し、最終的にヘルスケアの効率を高めることを目指しました。

投資の増加、CDSSの立ち上げ、医療への高額な資金提供など、こうした要因が北米におけるCDSS市場の予測期間中の成長を促進する可能性があります。

CDSS産業の概要

臨床意思決定支援システム市場には、国際的、地域的、ローカルに多様化したプレーヤーが存在します。しかし、一部の国際的な大手企業が、そのブランドイメージと市場リーチにより市場を独占しています。市場は細分化され、競争が激しいです。主な市場プレーヤーには、シーメンスヘルスケア、Koninklijke Philips NV、IBM、Cerner Corporation、Change Healthcareなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 病院におけるヘルスケアITの技術進歩

- ヘルスケア支出削減に対する需要の高まり

- 医療の質向上とヒューマンエラー削減の必要性

- 市場抑制要因

- クラウドベースのCDSSに関するプライバシーとデータセキュリティの懸念

- 熟練した専門家の不足

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- モデル別

- 知識型CDSS

- 非知識型CDSS

- 提供形態別

- クラウドベース

- オンプレミス

- コンポーネント別

- ハードウェア

- ソフトウェア

- サービス

- 製品別

- 統合型CDSS

- スタンドアロンCDSS

- 用途別

- 医療診断

- アラートとリマインダー

- 処方決定サポート

- 情報検索

- その他の用途

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Cerner Corporation

- Epic Systems Corporation

- IBM

- Change Healthcare

- Medical Information Technology Inc.

- Koninklijke Philips NV

- Siemens Healthcare

- Allscripts Healthcare Solutions Inc.

- Wolters Kluwer NV

- Mckesson Corporation

- Zynx Health Inc.

- Elsevier

- NextGen Healthcare Inc.

- Agfa-Gevaert Group

- Athenahealth Inc.

- VisualDx

第7章 市場機会と今後の動向

The Clinical Decision Support Systems Market size is estimated at USD 2.46 billion in 2024, and is expected to reach USD 4.05 billion by 2029, growing at a CAGR of 10.44% during the forecast period (2024-2029).

Amid the COVID-19 pandemic, the health systems of countries were majorly dependent on online services. Healthcare professionals were taking up a consultation with the patients through virtual sources. This was mainly due to the strict lockdown regulations imposed by various governments during the initial stages of the pandemic. Moreover, due to the COVID-19 outbreak across the world, clinical decision support systems played a vital role in assisting patient resources and services. For instance, the Journal Plos One article published in March 2021 mentioned that the development of decision support tools for real-time clinical diagnosis of COVID-19 is of prime importance of assist patient triage and allocating resources for patients at risk. Several countries are increasingly providing online services, which is boosting the market. Additionally, various market players launched clinical decision support systems for the management of COVID-19 data and insights. For instance, in May 2022, Epocrates launched an innovative long COVID-19 tool that incorporates late-breaking updates to expand the library of clinical decision support guidelines. Thus the increased adoption and launches of clinical decision support systems boosted the growth of the market during the pandemic.

The rising demand for reducing healthcare expenditure, the need for improvement in the quality of care, and technological advancements in healthcare IT in hospitals are the major factors that are likely to boost the growth of the clinical decision support systems (CDSS) market. Furthermore, according to the Organization for Economic Co-operation and Development (OECD) Survey Report, in 2021, the average per capita health expenditure was about USD 7,382.6 in Germany, USD 7,064.8 in Norway, and USD 6,262.3 in Sweden. Thus, the high healthcare expenditure is also expected to contribute to the growth of the market.

According to the Science direct study published in November 2022, the hybrid optimization learning algorithm had accuracy, sensitivity, and specificity metrics. The results revealed that the proposed model was quite appropriate for social anxiety disorder diagnosis and in line with the findings of other studies. Such efficiency of clinical decision support systems is expected to contribute to the growth of the market.

Additionally, the rising geriatric population is also expected to contribute to the growth of the market. According to the WHO data published in October 2022, the population aged 60 years and over will increase to 1.4 billion in 2030 and is expected to reach 2.1 billion by 2050. The UN report in 2022 mentioned that the share of the population aged 65 years or over is projected to rise from 10% in 2022 to 16% in 2050. The geriatric population who are vulnerable to developing chronic diseases and needs regular health checks and treatments for the prevention of diseases is expected to drive the demand for advanced clinical decision support systems, thereby contributing to the growth of the market.

Moreover, increasing initiatives such as collaborations and partnerships to develop clinical decision support systems are expected to contribute to the growth of the market. For instance, in June 2021, Google cloud entered into a multi-year agreement with the national hospital chain HCA healthcare to create customized healthcare algorithms to improve clinical decision-making.

Thus, the increasing healthcare expenditure and increasing initiatives for the development of clinical decision support systems are expected to contribute to the growth of the market. However, lack of trust in the systems, as CDSS are in the initial stages of development, lack of skilled labor, and suggestions from CDSS for unnecessary diagnostic testing hinder the market growth.

CDSS Market Trends

The Cloud-based Segment is Expected to Hold a Major Market Share Over the Forecast Period

The increasing healthcare expenditure and adoption of cloud computing are the major drivers for the expansion of the cloud-based segment of the market. The government in various countries in the European region are taking initiatives to support the growth of information technology in healthcare. For instance, in February 2021, the UK government launched an initiative to adopt a fully connected cloud-driven health service. Under this initiative, over two million National Health Services (NHS) mailboxes were moved to Microsoft's Azure Cloud. This will enable smoother and more efficient communication between staff across NHS organizations and departments and provide improved access to information. This will increase the usage of (Healthcare Information Technology) HCIT Change Management services in the United Kingdom and boost the market's growth.

Furthermore, local knowledge management of clinical decision support systems (CDSS) may require extensive processing power and storage capacity, which can result in high operating costs. In contrast, cloud-based applications are operated on remote servers, and executing them does not require a large amount of computational power or large storage space in the user's device.

Cloud-based applications do not depend on web browsers, which makes them inherently safer than web-based applications. In a cloud-based clinical decision support system, processing units are hosted on remote servers, which can be located in multiple data centers across the world, making them less vulnerable to cyberattacks. The increasing availability of cloud technology, owing to its benefit, is expected to drive the usage of cloud-based CDSS over the forecast period.

North America is Expected to Hold a Significant Share in the Market During the Forecast Period

The clinical decision support systems (CDSS) market in North America is driven due to the rise in the technological advancement in CDSS, the high awareness among patients, and rising investments in healthcare IT solutions in the region.

Also, the increasing funding from the government in North America for supporting healthcare is an attributing factor to the growth of the market in the United States. For instance, the Congressional Budget Office,2021, published that in the past few decades, federal funding for the National Institute of Health (NIH) has totaled over USD 700 billion.

Additionally, the increasingly advanced product launches in this region by various market players are also expected to contribute to the growth of the market. For instance, in August 2021, First Databank, Inc launched the FDB CDS Analytics, during the 2021 HIMSS Global conference and exhibition in Las Vegas. The solution enables healthcare provider organizations to easily identify, monitor, and customize clinical decision support in their electronic health record.

Similarly, in June 2021, a Canadian Healthcare company Pathway which offers, evidence-based clinical support to providers, raised USD 1.3 million in its first round of financing. With this financing, the company aimed to enhance clinical decision support systems which eventually increase healthcare efficiency.

These factors such as increasing investments, CDSS launches, and high funding for healthcare, may fuel the growth of the CDSS market over the forecast period in North America.

CDSS Industry Overview

The clinical decision support systems market has the presence of well-diversified international, regional, and local players. However, some big international players dominate the market, owing to their brand image and market reach. The market is fragmented and competitive in nature. some of the major market players include Siemens Healthcare, Koninklijke Philips NV, IBM, Cerner Corporation, Change Healthcare and Others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Technological Advancement in Healthcare IT in Hospitals

- 4.2.2 Rising Demand to Reduce Healthcare Expenditure

- 4.2.3 Need for Improvement in Quality of Care and Reducing Human Errors

- 4.3 Market Restraints

- 4.3.1 Privacy and Data Security Concerns Related to Cloud-based CDSS

- 4.3.2 Lack of Skilled Professionals

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Model

- 5.1.1 Knowledge-based CDSS

- 5.1.2 Non-knowledge CDSS

- 5.2 By Mode of Delivery

- 5.2.1 Cloud-based

- 5.2.2 On-premise

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.2 Software

- 5.3.3 Services

- 5.4 By Product

- 5.4.1 Integrated CDSS

- 5.4.2 Standalone CDSS

- 5.5 By Application

- 5.5.1 Medical Diagnosis

- 5.5.2 Alerts and Reminders

- 5.5.3 Prescription Decision Support

- 5.5.4 Information Retrieval

- 5.5.5 Other Applications

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Cerner Corporation

- 6.1.2 Epic Systems Corporation

- 6.1.3 IBM

- 6.1.4 Change Healthcare

- 6.1.5 Medical Information Technology Inc.

- 6.1.6 Koninklijke Philips NV

- 6.1.7 Siemens Healthcare

- 6.1.8 Allscripts Healthcare Solutions Inc.

- 6.1.9 Wolters Kluwer NV

- 6.1.10 Mckesson Corporation

- 6.1.11 Zynx Health Inc.

- 6.1.12 Elsevier

- 6.1.13 NextGen Healthcare Inc.

- 6.1.14 Agfa-Gevaert Group

- 6.1.15 Athenahealth Inc.

- 6.1.16 VisualDx