|

市場調査レポート

商品コード

1444505

ECGテレメトリー装置:市場シェア分析、業界動向と統計、成長予測(2024~2029年)ECG Telemetry Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ECGテレメトリー装置:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

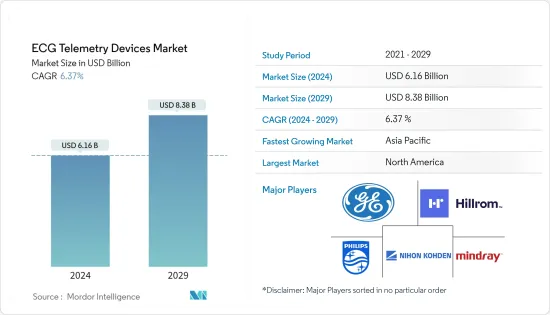

ECG(心電図)テレメトリー装置の市場規模は、2024年に61億6,000万米ドルと推定され、2029年までに83億8,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に6.37%のCAGRで成長します。

COVID-19のパンデミックは市場の成長に大きな影響を与えています。COVID-19のパンデミックの発生により、緊急でない予定された訪問や入院が中止される全国的なロックダウンが生じ、その結果、心疾患患者の診断が遅れました。たとえば、2022年 2月にNature Medicineに掲載された記事によると、COVID-19感染者は、心不全、血栓塞栓性疾患、不整脈、心膜炎、心筋炎、虚血性および非虚血性心筋炎などの心血管疾患を患う可能性が高いことが観察されています。虚血性心疾患。したがって、CVD関連疾患の負担が大きいため、パンデミック中にECGGテレメトリー、ウェアラブル、患者監視デバイスの需要が高まりました。さらに、2021年8月にPLOS Oneに掲載された記事では、心血管転帰の調整後の発生率比が、新型コロナウイルス感染症以前と比較して、新型コロナウイルス感染症曝露後の期間でかなり大きかったことが示されました。このため、心臓発作のリスクを軽減するために心臓の状態を定期的に監視するデバイスの需要が高まっています。また、COVID-19の制限が緩和され、心臓サービスが再開され、患者の来院が増加したことにより、調査対象の市場は予測期間中に成長すると予想されます。

心血管疾患の有病率の増加、高齢者人口の増加、遠隔監視技術の技術進歩などの要因が市場の成長を押し上げています。たとえば、BHFの2022年のレポートによると、2021年には英国で760万人以上が心血管疾患を患っていました。したがって、心血管疾患とその有病率の高さにより、心臓の状態を定期的にモニタリングする需要が増加し、市場の成長を促進すると予想されます。

さらに、オーストラリア統計局の2022年 3月の最新情報によると、2020年から2021年のオーストラリアにおける心臓病の有病率は4.0%で、これは約100万人に相当します。また、同じ情報源によると、オーストラリアでは心臓病は年齢とともに増加し、45~54歳の2.3%から75歳以上の23.2%まで増加しており、この国で心臓病に最も罹患しているのは男性であるといいます。したがって、CVDの負担の増加は、高齢者人口の増加と相まって、予測期間中の市場の成長の主な促進要因になると予想されます。

さらに、人口における肥満、糖尿病、高血圧、高コレステロールの有病率の増加が市場の成長に貢献しています。たとえば、OECDが発表した2021年のデータによると、2030年までに米国の人口の約47%、メキシコの39%、カナダの35%が肥満に悩まされると予想されています。また、2022年の統計によると、 IDFの発表によると、世界中で20~79歳の成人約5億3,700万人が糖尿病を抱えており、この数は2030年までに6億4,300万人、2045年までに7億8,300万人に増加すると予測されています。したがって、糖尿病によって引き起こされる高血糖は、心臓や血管を制御する神経にダメージを与え、冠動脈疾患や脳卒中などのさまざまな心血管疾患を引き起こし、動脈が狭くなる可能性があります。これにより、心臓イベントモニタリングやその他の遠隔測定デバイスの需要がさらに増加し、市場の成長が促進されると予想されます。

さらに、遠隔監視技術における技術進歩の高まりにより、企業が遠隔測定装置や遠隔患者監視装置を製造する機会が生まれています。これにより、市場での製品の入手可能性が高まり、市場の成長が促進されると予想されます。たとえば、ロイヤルフィリップスは2022年 1月に、分散型臨床試験で使用する初の家庭用 12誘導心電図(ECG)ソリューションを導入しました。また、2021年 7月に、アボットは挿入可能な心臓モニター(ICM)であるJot Dxを米国で発売しました。この技術により、患者の不整脈の遠隔検出と診断精度の向上が可能になります。

したがって、上記の要因により、調査対象の市場は予測期間中に成長すると予想されます。ただし、デバイスの高コストとさまざまな国の複雑な償還政策により、予測期間中の市場の成長が妨げられると予想されます。

ECGテレメトリー装置の市場動向

植込み型ループレコーダーセグメントは、予測期間中に主要な市場シェアを保持すると予想されます

植込み型ループレコーダーセグメントは、心疾患の有病率の増加、心臓モニタリング装置の最近の技術進歩、遠隔患者モニタリングの需要の増加などの要因により、予測期間中にECGテレメトリー装置市場で大幅な成長が見込まれると予想されています。植込み型ループレコーダー(ILP)は心臓イベントレコーダーとも呼ばれ、心臓のリズムを最長3年間継続的に記録する心臓監視装置の一種です。また、医師が遠隔から心拍を監視することも可能になります。 2021年12月にCardiovascular Diagnosis and Therapy(CDT)に掲載された論文によると、ILPは、生命を脅かす心臓病のリスクがある症候性CHD患者の良性および悪性不整脈の同定と分類に重要な補助診断価値を提供することが観察されています。イベント。また、同じ情報源によると、特に短期のホルターモニタリングでは十分な診断の確実性が得られない場合、中期または長期の不整脈モニタリングが必要な、何らかの複雑性のCHD患者では、ILR移植を検討すべきです。これにより、幅広い心血管疾患に苦しむ患者への植込み型ループレコーダーの採用が増加し、この部門の成長が促進されると予想されます。

さらに、新しい償還政策のイントロダクションよる患者間の遠隔患者モニタリング(RPM)の採用の増加や、提携、買収などのさまざまなビジネス戦略の採用の増加も、ILPの需要を増加させると予想されています。たとえば、2021年 1月、CMSは2021年の医師料金表を修正し、遠隔患者モニタリング(RPM)の償還基準を引き上げました。これは、心臓モニタリングにRPMが広く採用され、それによって埋め込み型ループレコーダーの需要が増加していることを示しています。また、AHAによると、最近の臨床ガイドラインでは、脳卒中患者と非脳卒中患者の両方で心房細動検出のための遠隔患者モニタリングの使用を強く推奨しており、これにより植込み型ループレコーダーの需要がさらに増加し、市場の成長を促進しています。さらに、2021年 1月、ボストンサイエンティフィックはPreventice Solutionsを9億2,500万米ドルで買収しました。この買収により、ボストンは中核となる心調律管理と電気生理学の事業部門を拡大しました。したがって、上記の要因により、調査対象セグメントは予測期間中に成長すると予想されます。

北米は予測期間中にかなりの市場シェアを保持すると予想される

予測期間中、北米が市場を独占すると予想されます。市場の成長の要因としては、国民の心臓血管への負担の増加、償還政策に伴う高額なヘルスケア費、そしてこの地域におけるECGテレメトリー装置の需要と採用の増加が挙げられます。

心血管疾患の有病率の増加が、この地域におけるECGテレメトリー装置の需要を促進する主な要因です。たとえば、AHAが2021年6月に発表した統計によると、2021年のカナダの心不全有病率は1.5%から1.9%でした。同じ情報源によると、推定では、カナダの成人は1億3,000万人以上です。米国では、2035年までに何らかの心臓病が発生すると予想されています。また、CDCが発表した2022年のデータによると、心臓病は米国の主な死因であり、米国では毎年約805,000人が死亡しています。心臓発作を起こしています。したがって、人口における心不全症例の数が多いと、心房細動や不整脈のリスクが高まるため、心臓へのさらなるリスクを防ぐために心拍数と酸素飽和度を定期的にモニタリングする必要があり、そのためECGテレメトリー装置の需要が高まっています。さらに、2021年 7月にInternational Journal of Strokeに掲載された調査結果によると、米国では2050年までに約600万人から1,200万人が、2060年までに1,790万人が心房細動に苦しむと予想されています。、心血管関連の健康上の問題による国民の負担の増加が予想されており、患者パラメータ監視装置だけでなく定期的な心臓監視の需要も高まることが予想されます。これにより、予測期間中の市場の成長が促進されると予想されます。

さらに、患者監視装置の技術進歩と、心血管疾患患者を支援する製品を開発・発売している地域の主要企業の存在により、予測期間中の市場の成長が拡大すると予想されます。たとえば、2021年 7月に、アボットは挿入可能な心臓モニター(ICM)であるJot Dxを米国で発売しました。これにより、患者の不整脈の遠隔検出と診断精度の向上が可能になります。また、Jot Dxは、患者がICMに接続し、接続を維持できるようにするための1対1のトレーニングと指導を提供するパーソナライズされたサービスであるSyncUPによってサポートされています。同様に、2021年 7月に米国食品医薬品局は、メドトロニックの2つのAccuRhythm人工知能(AI)アルゴリズムをLINQ II挿入型心臓モニター(ICM)で使用することを承認しました。したがって、上記の要因により、調査対象の市場は予測期間中に成長すると予想されます。

ECGテレメトリー装置業界の概要

ECGテレメトリー装置市場は本質的に細分化されており、複数の企業が市場で好成績を収めています。ただし、一部の企業はこの市場に最も貢献し、特定の地域を支配しています。製品開発への注目の高まりとヘルスケアにおけるテクノロジーの利用の増加により、将来的にはより多くの中小企業が市場に参入すると予想されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 心血管疾患の有病率と発生率の増加

- 高齢者人口の増加

- 遠隔監視技術の技術進歩

- 市場抑制要因

- デバイスのコストが高い

- 複雑な償還ポリシー

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品別

- イベントモニタリングとモバイル心臓テレメトリ

- 埋め込み型ループレコーダー

- その他の製品

- 用途別

- 不整脈

- 心筋虚血と心筋梗塞

- ペースメーカーの監視

- その他の用途

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Aerotel Medical Systems Ltd

- BioTelemetry Inc.

- GE Healthcare(GE Company)

- Medtronic Inc.

- iRhythm Technologies Inc.

- Nihon Kohden Corporation

- Philips Healthcare

- Medicalgorithmics SA

- Preventice Solutions Inc.

- Hill-Rom Services Inc.(Welch Allyn)

- BIOTRONIK

- Boston Scientific Corporation

第7章 市場機会と将来の動向

The ECG Telemetry Devices Market size is estimated at USD 6.16 billion in 2024, and is expected to reach USD 8.38 billion by 2029, growing at a CAGR of 6.37% during the forecast period (2024-2029).

The COVID-19 pandemic has significantly impacted market growth. The onset of the COVID-19 pandemic caused a nationwide lockdown with the suspension of non-urgent scheduled visits and hospitalizations, which resulted in the delayed diagnosis of patients with cardiac disorders. For instance, from an article published in Nature Medicine in February 2022, it has been observed that people with COVID-19 are more likely to have cardiovascular diseases such as heart failure, thromboembolic diseases, dysrhythmias, pericarditis, myocarditis, and ischemic and non-ischemic heart disease. Thus, the high burden of CVD-related diseases raised the demand for ECG telemetry, wearables, and patient monitoring devices during the pandemic. Moreover, an article published in PLOS One in August 2021 showed that the adjusted incident rate ratios for cardiovascular outcomes were considerably greater in the post-COVID-19 exposure period as compared to the pre-COVID-19 period. This raises the demand for devices that regularly monitors heart conditions to reduce the risk of a heart attack. Also, with the relaxed COVID-19 restrictions, resumed cardiac services, and increased patient visits, the studied market is expected to grow over the forecast period.

Factors such as the increasing prevalence of cardiovascular diseases, the growing geriatric population, and technological advancements in remote monitoring technologies are boosting market growth. For instance, as per BHF's 2022 report, more than 7.6 million people were living with cardiovascular diseases in the United Kingdom in 2021. Hence, cardiovascular diseases and their high prevalence is expected to increase the demand for regular monitoring of heart condition, propelling market growth.

Additionally, according to the March 2022 update of the Australian Bureau of Statistics, the prevalence of heart disease in Australia was 4.0% in 2020-2021, which equates to about 1 million people. Also, as per the same source, in Australia, heart disease increased with age, from 2.3% of people aged 45-54 years through to 23.2% of people aged 75 years and over, with males being the most affected by it in the country. Hence, the rising burden of CVDs, coupled with the increasing geriatric population, is expected to be the major driving factor for the growth of the market over the forecast period.

Furthermore, the increasing prevalence of obesity, diabetes, hypertension, and high cholesterol among the population is contributing to market growth. For instance, according to the 2021 data published by the OECD, about 47% of the population in the United States, 39% in Mexico, and 35% in Canada are expected to suffer from obesity by 2030. Also, according to the 2022 statistics published by IDF, about 537 million adults aged between 20-79 years were living with diabetes globally, and this number is projected to increase to 643 million and 783 million by 2030 and 2045, respectively. Therefore, high blood sugar caused by diabetes can damage the nerves that control the heart and blood vessels, leading to a variety of cardiovascular diseases like coronary artery disease and stroke, which can narrow the arteries. This is further expected to increase the demand for cardiac event monitoring and other telemetry devices, hence boosting market growth.

Moreover, the growing technological advancements in remote monitoring technologies are creating opportunities for companies to manufacture telemetry and remote patient monitoring devices. This increases the availability of products in the market, which is anticipated to fuel market growth. For instance, in January 2022, Royal Phillips introduced the first at-home 12-lead electrocardiogram (ECG) solution for use in decentralized clinical trials. Also, in July 2021, Abbott launched Jot Dx, an insertable cardiac monitor (ICM), in the United States. This technology allows for remote detection and improved diagnostic accuracy of cardiac arrhythmia in patients.

Therefore, owing to the above-mentioned factors, the studied market is expected to grow over the forecast period. However, the high cost of the devices and complex reimbursement policies in various countries are expected to impede the growth of the market over the forecast period.

ECG Telemetry Devices Market Trends

The Implantable Loop Recorder Segment is Expected to Hold a Major Market Share Over the Forecast Period

The implantable loop recorder segment is expected to witness significant growth in the ECG telemetry devices market over the forecast period owing to factors such as the growing prevalence of cardiac disorders, recent technological advancements in cardiac monitoring devices, and increasing demand for remote patient monitoring. An implantable loop recorder (ILP), also called a cardiac event recorder, is a type of heart-monitoring device that constantly records the heart rhythm for up to three years. It also allows doctors to remotely monitor the heartbeat. According to an article published in Cardiovascular Diagnosis and Therapy (CDT) in December 2021, it has been observed that ILP offers a significant supplemental diagnostic value for the identification and classification of benign and malignant arrhythmias in symptomatic CHD patients at risk of life-threatening cardiac events. Also, as per the same source, ILR implantation should be considered in patients with CHD of any complexity who need medium or long-term arrhythmia monitoring, especially if short-term Holter monitoring is unable to provide adequate diagnostic certainty. This is anticipated to increase the adoption of implantable loop recorders in patients suffering from a wide range of cardiovascular diseases, hence bolstering the segment's growth.

Furthermore, the increasing adoption of remote patient monitoring (RPM) among patients due to the introduction of new reimbursement policies and the rising adoption of various business strategies such as collaborations, acquisitions, and others are also expected to increase the demand for ILP, hence boosting market growth. For instance, in January 2021, the CMS amended the 2021 Physician Fee Schedule to increase the reimbursement criteria for remote patient monitoring (RPM). This indicates wider adoption of RPM for cardiac monitoring, thereby increasing the demand for implantable loop recorders. Also, as per the AHA, recent clinical guidelines strongly recommend the use of remote patient monitoring for atrial fibrillation detection in both stroke and non-stroke patients, thereby further increasing the demand for implantable loop recorders, hence boosting the market growth. Moreover, in January 2021, Boston Scientific acquired Preventice Solutions for USD 925 million. With this acquisition, Boston expanded its business segment of core cardiac rhythm management and electrophysiology. Therefore, owing to the abovementioned factors, the studied segment is expected to grow over the forecast period.

North America is Expected to Hold Significant Market Share Over the Forecast Period

North America is expected to dominate the market over the forecast period. The factors attributed to the market's growth are the rising cardiovascular burden among the population, high healthcare expenditure along with reimbursement policies, and rising demand and adoption for ECG telemetry devices in the region.

The increasing prevalence of cardiovascular diseases is the key factor driving the demand for ECG telemetry devices in the region. For instance, according to the statistics published by the AHA in June 2021, the prevalence rate of heart failure in Canada was between 1.5% to 1.9% in 2021. As per the same source, in an estimate, more than 130 million adults in the United States are expected to have some type of heart disease by 2035. Also, according to the 2022 data published by the CDC, heart disease is the leading cause of death in the United States, and every year, about 805,000 people in the United States have a heart attack. Thus, the high number of heart failure cases among the population increases the risk of atrial fibrillation and cardiac arrhythmias, which requires regular monitoring of the heart rate and oxygen saturation to prevent further risk to the heart, hence propelling the demand for ECG telemetry devices. Additionally, as per a research study published in the International Journal of Stroke in July 2021, it has been observed that about 6-12 million people in the United States are expected to suffer from atrial fibrillation by 2050 and 17.9 million people by 2060. Thus, the expected increase in the burden of cardiovascular-related health problems among the population is anticipated to fuel the demand for regular heart monitoring as well as a patient-parameters monitoring device. This is expected to propel the market's growth over the forecast period.

Furthermore, the technological advancements in patient monitoring devices, as well as the presence of key players in the region that are developing and launching products for helping patients with cardiovascular diseases, are expected to augment the market's growth over the forecast period. For instance, in July 2021, Abbott launched Jot Dx, an insertable cardiac monitor (ICM), in the United States. It allows remote detection and improved diagnostic accuracy of cardiac arrhythmia in patients. Also, Jot Dx is supported by SyncUP, a personalized service that offers one-on-one training and instruction to help patients become connected and stay connected to their ICM. Similarly, in July 2021, the US Food and Drug Administration approved Medtronic's two AccuRhythm artificial intelligence (AI) algorithms for use with the LINQ II insertable cardiac monitor (ICM). Therefore, owing to the abovementioned factors, the studied market is expected to grow over the forecast period.

ECG Telemetry Devices Industry Overview

The ECG telemetry devices market is fragmented in nature, and multiple companies are performing well in the market. However, some of the companies are contributing the most to this market and dominating certain geographies. With the rising focus on product development and the increasing usage of technology in healthcare, more small and mid-sized companies are expected to enter the market in the future. Some of the companies that are currently dominating the market are Aerotel Medical Systems Ltd, BioTelemetry Inc., GE Healthcare (GE Company), Medtronic Inc., iRhythm Technologies Inc., Nihon Kohden Corporation, Philips Healthcare, Medicalgorithmics SA, Preventice Solutions Inc., and Hill-Rom Services Inc. (Welch Allyn).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence and Incidence of Cardiovascular Diseases

- 4.2.2 Growing Geriatric Population

- 4.2.3 Technological Advancements in Remote Monitoring Technologies

- 4.3 Market Restraints

- 4.3.1 High Cost of Devices

- 4.3.2 Complex Reimbursement Policies

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Product

- 5.1.1 Event Monitoring and Mobile Cardiac Telemetry

- 5.1.2 Implantable Loop Recorders

- 5.1.3 Other Products

- 5.2 By Application

- 5.2.1 Arrhythmias

- 5.2.2 Myocardial Ischemia and Infarction

- 5.2.3 Pacemaker Monitoring

- 5.2.4 Other Applications

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Aerotel Medical Systems Ltd

- 6.1.2 BioTelemetry Inc.

- 6.1.3 GE Healthcare (GE Company)

- 6.1.4 Medtronic Inc.

- 6.1.5 iRhythm Technologies Inc.

- 6.1.6 Nihon Kohden Corporation

- 6.1.7 Philips Healthcare

- 6.1.8 Medicalgorithmics SA

- 6.1.9 Preventice Solutions Inc.

- 6.1.10 Hill-Rom Services Inc. (Welch Allyn)

- 6.1.11 BIOTRONIK

- 6.1.12 Boston Scientific Corporation