|

市場調査レポート

商品コード

1444520

e-ヘルス:市場シェア分析、業界動向と統計、成長予測(2024~2029年)EHealth - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| e-ヘルス:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

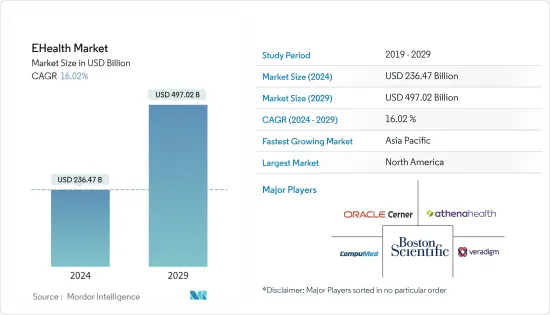

e-ヘルス市場規模は2024年に2,364億7,000万米ドルと推定され、2029年までに4,970億2,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に16.02%のCAGRで成長します。

COVID-19は、隔離期間中のCOVID-19の接触追跡や相談のための遠隔医療やその他のe-ヘルスソリューションの市場関係者による発売の増加により、e-ヘルス市場に影響を与えています。たとえば、2022年6月に国際医療情報学ジャーナルに掲載された記事によると、2021年1月25日から2月22日にかけて日本のヘルスケア提供者を対象に実施されたオンライン調査では、医療提供機関の73.3%が電子医療記録を使用し、 EMRの57.8%は、他の病院との地域医療情報の共有(22.0%)、オンラインでの医療保険請求の報告(27.5%)、および院内システムのメンテナンス(61.5%)の実施に役立つ外部ネットワークに接続していました。したがって、パンデミック中にe-ヘルスの使用がピークに達しました。 e-ヘルス市場は、COVID-19による導入の増加により成長しており、予測期間中に大幅な成長率を記録すると予想されています。

e-ヘルス市場の成長を促進する要因には、IoTと技術革新の成長、モバイルテクノロジーとインターネットへの選好の高まり、国民の健康管理に対する需要の高まりが含まれます。たとえば、2022年 8月にDigital Healthに掲載された記事によると、サウジアラビア全土の多数のヘルスケア施設におけるデジタルヘルスへの移行は、デジタルヘルス指標を利用して評価されました。民間ヘルスケア施設のデジタル変革スコアの合計は、導入率が高いため、政府病院よりも高いことが観察されました。したがって、民間ヘルスケア施設全体でのデジタル医療システムの普及が進んでいることにより、予測期間中に市場の成長が高まると予想されます。

モバイルテクノロジーとインターネットに対する嗜好の高まりに対する政府の取り組みも、市場の成長を促進すると予想されます。たとえば、2022年5月、イスラエルは、HMO、病院、研究機関を含むヘルスケア機関が、この分野の新興企業との共同研究開発プロジェクトに必要なデジタルインフラストラクチャを開発できるようにする新しいデジタルヘルスイニシアチブとして、3,000万米ドルで19件のイニシアチブを承認しました。ヘルスケアの。

e-ヘルスソリューションの技術進歩、製品の発売、市場関係者によるパートナーシップは、予測期間中に市場の成長を推進すると予想されます。たとえば、2022年 5月、ブラジルのデジタルヘルス企業Memedは、患者がMemedの電子処方箋から直接オンラインで薬を購入できる一連のデジタル統合ケア経路を開始しました。さらに、2022年 1月に、Visionflexはオーストラリアのクラウドベースの電子医療記録および診療管理システムのプロバイダーであるMediRecordsと提携しました。この提携は、Visionflexのビデオ会議プラットフォームであるVisionと、MediRecordsのクラウドベースの電子医療記録および診療管理ソフトウェアプラットフォームを統合することを目的としています。

したがって、調査対象の市場は、市場関係者によるe-ヘルスソリューションの拡大のための発売、パートナーシップ、資金調達の増加などの要因により、分析期間中に成長が見られると予想されます。しかし、データセキュリティに対する懸念、新興市場における償還ポリシーの欠如、新興市場におけるe-ヘルスのための適切なインフラストラクチャの欠如が、市場の成長を抑制すると推定されています。

e-ヘルス市場の動向

電子処方箋セグメントは、予測期間中にかなりの市場シェアを保持すると予想される

電子処方箋または電子処方箋は、医師やその他の医療従事者が、書面による処方箋を使用する代わりに、電子形式で処方箋を作成して参加薬局に送信できるようにするテクノロジーフレームワークです。

このセグメントは、処方箋ミスの最小化、コスト削減、市場プレーヤーによる技術の進歩と発売の増加による電子処方箋の需要の高まりにより、予測期間中に成長すると予想されています。たとえば、2022年12月に英国の医学雑誌に掲載された論文によると、日本の老人ホームの高齢者の間では、薬物有害事象や投薬ミスがよく見られるといいます。規制薬物の乱用の削減と医療過誤の削減への注目の高まりにより、予測期間中に電子処方システムの導入が加速すると予想されます。

さらに、電子処方箋の有用性の向上につながる政府の取り組みの高まりが、この分野の成長を大きく加速させています。たとえば、2022年 8月に日本の厚生労働省は、電子処方箋プロジェクトのパイロットサイトを4か所選択しました。これは、2023年1月に全国で電子処方箋が正式に開始されることに先立って行われました。さらに、2021年9月には首相がインドでプラダン・マントリ・デジタル・ヘルス・ミッションを展開しました。これは、全国的なヘルスケア行為をデジタル化し、国全体のデジタル医療エコシステムを構築し、患者が医療記録を保存、アクセス、共有することに同意できるようにすることを目的としていました。

さらに、電子処方箋ソリューションの拡大に向けた市場関係者による戦略的取り組みが、この分野の成長を促進すると予想されます。たとえば、2023年1月、カタールを拠点とするヘルステックスタートアップのAt Home Docは、カタール開発銀行(QDB)やその他のエンジェル投資家の支援を受け、エラジ・グループの投資部門タワソル・ホールディングスが主導するプレシリーズA資金で190万米ドルを調達しました。 2022年 6月、ハマドメディカルコーポレーション(HMC)とプライマリヘルスケアコーポレーション(PHCC)は、カタールでより良い結果をもたらすために、Cernerが管理するテクノロジーを採用すると発表しました。この資金は、国内の電子処方箋ソリューションを強化するために活用されます。

したがって、市場セグメントは、上記の要因により、予測期間中に大幅な成長を遂げると予想されます。

北米地域は大きな市場シェアを保持しており、予測期間中同じ傾向に従うと予想されます

よく発達し技術的に進歩したヘルスケアシステムに支えられ、患者のケアとニーズへの注目が高まっていること、より効果的なデータ管理システムに対する需要の高まり、そしてこの地域でのパートナーシップ、買収、製品発売の増加が、成長を促進すると予想されています。この地域のe-ヘルス市場のトップ。

国立保健統計センターの2021年の推定によると、米国の勤務医の89.9%がEMR/EHRシステムを使用し、72.3%が認定されたEMR/EHRシステムを使用しました。この地域でのEMRの普及率の高さにより、予測期間中にe-ヘルスソリューションの有用性が促進されると予測されます。

さらに、この地域での電子健康ソリューションの発売、パートナーシップ、導入の増加により、市場の成長が促進されると予想されます。たとえば、2022年 3月、Cantata Health Solutionsは、Village NetworkがArize電子健康記録(EHR)を導入して、その優れた構成、結果ベースのレポート、モバイルアクセス機能を活用すると報告しました。 2022年 5月、Cantata Health Solutionsはニューメキシコ州のMental Health Resources(MHR)によってテクノロジーパートナーとして選ばれ、Arize電子健康記録(EHR)ソリューションを導入する予定です。

さらに、2021年 10月に、Allscriptsヘルスケア LLCは、人工知能を活用して患者ケアを改善し、ヘルスケア業務の効率を向上させるガイド付きスケジューリングを開始しました。 2021年 2月、Northern Inyoヘルスケア DistrictはCerner Corporationと協力して、電子医療記録(EHR)を変革しました。この連携には、北インヨヘルスケア地区が、医師、看護師、臨床医が地区の複数のオフィス間でデータを共有できるようにサポートする最新の電子システムへの移行が含まれていました。このような協力は、予測期間中にこの地域でのe-ヘルスの導入の増加に貢献します。

e-ヘルス業界の概要

e-ヘルス市場は、世界的および地域的に事業を展開する複数の企業が存在するため、本質的に細分化されています。競合情勢には、大手または重要な市場シェアを持つ数社の国際企業および地元企業の分析が含まれます。主要な市場プレーヤーには、Boston Scientific Corporation、Veradigm LLC、Oracle Cerner、Athenahealth Inc.、GEヘルスケア、CompuMed Inc.、Epic Systems Corporation、Optum Health、Siemens Healthineers、Koninklijke Philips NV、およびeClinicalWorksなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- IoTと技術革新の成長

- モバイルテクノロジーとインターネットへの関心の高まり

- 人口の健康管理に対する需要の高まり

- 市場抑制要因

- データセキュリティに関する懸念

- 新興市場における償還ポリシーの欠如

- 新興市場におけるe-ヘルスのための適切なインフラストラクチャの欠如

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- コンポーネント別

- 電子健康記録

- 電子処方箋

- 臨床意思決定支援システム

- 遠隔医療

- その他のコンポーネント

- サービスタイプ別

- モニタリングサービス

- 診断サービス

- 治療およびその他のサービス

- エンドユーザー別

- 病院

- 保険会社

- その他のエンドユーザー

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Veradigm LLC

- athenahealth Inc.

- Boston Scientific Corporation

- Oracle Cerner

- CompuMed Inc.

- GE Healthcare

- eClinicalWorks

- Epic Systems Corporation

- Optum Health

- Siemens Healthineers

- Koninklijke Philips NV

第7章 市場機会と将来の動向

The EHealth Market size is estimated at USD 236.47 billion in 2024, and is expected to reach USD 497.02 billion by 2029, growing at a CAGR of 16.02% during the forecast period (2024-2029).

COVID-19 has impacted the eHealth market owing to market players' increased launches of telemedicine and other eHealth solutions for COVID-19 contact tracing and consultations during the isolation period. For instance, according to an article published in the International Journal of Medical Informatics in June 2022, an online survey of Japanese healthcare providers carried out from January 25 to February 22, 2021, reported that 73.3% of care delivery institutions used electronic medical records and 57.8% of the EMRs were connected to an external network that helps in sharing the regional health information with other hospitals (22.0%), report online medical insurance claims (27.5%), and conduct intrahospital system maintenance (61.5%). Hence, the use of e-health was at its peak during the pandemic. The eHealth market is growing due to its increasing adoption because of COVID-19 and is expected to register a significant growth rate during the forecast period.

The propelling factors for the growth of the e-health market include the growth in IoT and technological innovations, rising preference toward mobile technology and the internet, and rising demand for population health management. For instance, according to an article published in Digital Health in August 2022, the digital health transition in numerous healthcare facilities throughout Saudi Arabia was assessed utilizing digital health indicators. The total digital transformation score in private healthcare facilities was observed to be higher than in governmental hospitals due to greater implementation rates. Thus, the high adoption of digital health systems across private healthcare facilities is expected to increase market growth over the forecast period.

The government initiatives for the rising preference toward mobile technology and the internet are also expected to propel market growth. For instance, in May 2022, Israel approved 19 initiatives for USD 30 million for a new digital health initiative enabling healthcare institutions, including HMOs, hospitals, and institutes, to develop the digital infrastructure needed for collaborative R&D projects with start-ups in the field of healthcare.

The technological advancement in e-health solutions, product launches, and partnerships by market players is expected to propel market growth during the forecast period. For instance, in May 2022, Brazil's digital health company, Memed, launched a set of digitally integrated care pathways that allow patients to purchase medication online directly from a Memed e-prescription. Furthermore, in January 2022, Visionflex partnered with MediRecords, Australia's cloud-based electronic medical record and practice management systems provider. The partnership is aimed to integrate Visionflex's video conferencing platform, Vision, with MediRecords' cloud-based electronic health record and practice management software platforms.

Therefore, the studied market is anticipated to witness growth over the analysis period due to the factors such as rising launches, partnerships, and fundraising for the expansions of eHealth solutions by market players. However, the concerns over data security, the lack of reimbursement policies in emerging markets, and the lack of proper infrastructure for eHealth in emerging markets are estimated to restrain the market growth.

eHealth Market Trends

e-Prescribing Segment is Expected to Hold a Significant Market Share Over The Forecast Period

E-prescribing or electronic prescribing is a technology framework that allows physicians and other medical practitioners to write and send prescriptions to a participating pharmacy in an electronic format instead of using written prescriptions.

The segment is expected to grow during the forecast period owing to the rising demand for e-prescriptions due to the minimization of prescription errors, cost reduction, and increasing technological advancements and launches by market players. For instance, according to an article published in the British medical journal in December 2022, adverse drug events and medication errors are common among the aging population in nursing homes in Japan. The rising focus on reducing the abuse of controlled substances and increasing focus on reducing medical errors will accelerate the adoption of an e-prescribing system in the forecast period.

Furthermore, the rising government initiatives leading to an increase in the utility of e-prescription are significantly adding to the segment's growth. For instance, in August 2022, the Japanese Ministry of Health, Labour, and Welfare selected four pilot sites for its electronic prescription project. This came ahead of the formal launch of e-prescriptions across the country in January 2023. Furthermore, in September 2021, the Prime Minister rolled out the Pradhan Mantri Digital Health Mission in India. It aimed to digitalize healthcare practices nationwide, creating a country-wide digital health ecosystem and enabling patients to store, access, and consent to share health records.

Moreover, the strategic initiatives by market players for expansions of e-prescription solutions are expected to propel the segment's growth. For instance, in January 2023, the Qatar-based HealthTech startup At Home Doc raised USD 1.9 million in Pre-Series A funding led by Elaj Group's investment arm Tawasol Holdings, endorsed by Qatar Development Bank (QDB) and other angel investors. In June 2022, the Hamad Medical Corporation (HMC) and Primary Health Care Corporation (PHCC) announced adopting Cerner-managed technology to deliver better outcomes in Qatar. The funding will be utilized to enhance electronic prescription solutions in the country.

Thus, the market segment is expected to witness significant growth during the forecast period due to the abovementioned factors.

The North American Region Holds the Significant Market Share and is Expected to Follow the Same Trend Over the Forecast Period

The rising focus on patient care and need, supported by the well-developed and technologically advanced healthcare system, the increasing demand for more effective data management systems, and increasing partnerships, acquisitions, and product launches in the region, is expected to drive the growth of the eHealth market in the region.

According to the National Center for Health Statistics 2021 estimates, 89.9% of office-based physicians in the United States used any EMR/EHR system, and 72.3% used a certified EMR/EHR system. The high adoption of EMRs in the region is projected to propel the utility of eHealth solutions during the forecast period.

Furthermore, the rising launches, partnerships, and increasing adoption of electronic health solutions in the region are expected to propel the market growth. For instance, in March 2022, Cantata Health Solutions reported that the Village Network would deploy its Arize Electronic Health Record (EHR) to leverage its superior configuration, outcomes-based reporting, and mobile access capabilities. In May 2022, Cantata Health Solutions was selected by Mental Health Resources (MHR) in New Mexico as its technology partner and will deploy the Arize Electronic Health Record (EHR) solution.

Additionally, in October 2021, Allscripts Healthcare LLC launched guided scheduling by leveraging artificial intelligence to improve patient care and increase healthcare operational efficiencies. In February 2021, Northern Inyo Healthcare District collaborated with Cerner Corporation to transform its Electronic Health Record (EHR). The collaboration involved Northern Inyo Healthcare District moving to an updated electronic system that supports physicians, nurses, and clinicians to share data across the District's multiple offices. Such collaborations will contribute to the rising adoption of eHealth in the region during the forecast period.

eHealth Industry Overview

The eHealth market is fragmented in nature due to the presence of several companies operating globally as well as regionally. The competitive landscape includes an analysis of a few international and local companies with major or significant market shares. Some of the key market players are Boston Scientific Corporation, Veradigm LLC, Oracle Cerner, Athenahealth Inc., GE Healthcare, CompuMed Inc., Epic Systems Corporation, Optum Health, Siemens Healthineers, and Koninklijke Philips NV, and eClinicalWorks.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in IoT and Technological Innovations

- 4.2.2 Rising Preference Toward Mobile Technology and Internet

- 4.2.3 Rising Demand for Population Health Management

- 4.3 Market Restraints

- 4.3.1 Concerns over Data Security

- 4.3.2 Lack of Reimbursement Policies in the Emerging Markets

- 4.3.3 Lack of Proper Infrastructure for eHealth in Emerging Markets

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Component

- 5.1.1 Electronic Health Records

- 5.1.2 e-Prescribing

- 5.1.3 Clinical Decision Support Systems

- 5.1.4 Telemedicine

- 5.1.5 Other Components

- 5.2 By Type of Service

- 5.2.1 Monitoring Service

- 5.2.2 Diagnosis Service

- 5.2.3 Therapeutic and Other Services

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Insurance Companies

- 5.3.3 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Veradigm LLC

- 6.1.2 athenahealth Inc.

- 6.1.3 Boston Scientific Corporation

- 6.1.4 Oracle Cerner

- 6.1.5 CompuMed Inc.

- 6.1.6 GE Healthcare

- 6.1.7 eClinicalWorks

- 6.1.8 Epic Systems Corporation

- 6.1.9 Optum Health

- 6.1.10 Siemens Healthineers

- 6.1.11 Koninklijke Philips NV