|

市場調査レポート

商品コード

1685686

農業用キレート化合物:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Agricultural Chelates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 農業用キレート化合物:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

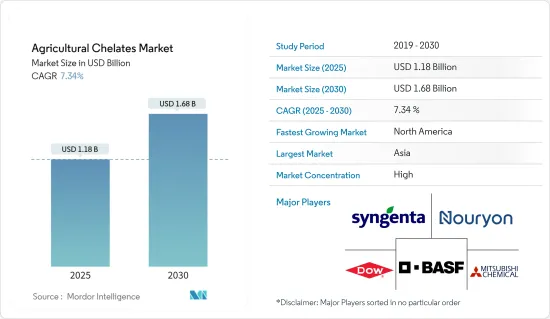

農業用キレート化合物の市場規模は2025年に11億8,000万米ドルと予測され、予測期間(2025年~2030年)のCAGRは7.34%で、2030年には16億8,000万米ドルに達すると予測されます。

主なハイライト

- 気候条件の変化、耕地の減少、世界人口の急速な拡大により、食糧安全保障に対する懸念が高まっています。米国農務省(USDA)が実施した2022年農業センサスでは、米国(U.S.)の農場数が200万を割り込んだことが明らかになりました。具体的には、2022年の米国における農家数は190万戸で、2017年の国勢調査の数字から7%減少しました。さらに、国勢調査は米国の農地総面積が2.2%減少し、2022年には8億8,000万エーカーになることを強調しています。こうした開発を踏まえると、適切な農業投入による生産性の向上が不可欠となっています。その結果、世界の食糧需要を満たすために作物の収量を向上させるため、農業におけるキレート剤の採用が顕著に急増しています。キレート剤は、植物の栄養素の取り込みを促進し、特定の栄養素をより利用しやすくします。これにより、植物の成長と開発が改善され、最終的に作物の収量と品質が向上します。

- 独立研究所の分析によると、英国の小麦作物では窒素が10%、リンが25%欠乏していることが、何千もの土壌サンプルから明らかになっています。キレート化は、溶液と土壌の両方における不要な反応から微量栄養素を保護するメカニズムとして機能します。Fe、Cu、Mn、Znなどの微量栄養素の生物学的利用能を高めることで、キレート肥料は商業作物生産の生産性と収益性を高める上で極めて重要な役割を果たします。特に、pHが6.5を超える土壌や低微量栄養素ストレス下にある土壌では、キレート肥料は標準的な微量栄養素と比較して、商業的収量を増加させる優れた能力を実証しています。

- 持続可能な農業の機運が高まり、合成キレート剤が環境に与える影響に対する意識が高まる中、生分解性の代替品を模索する動きが顕著になっています。こうした状況を踏まえ、各社はこの需要の高まりに対応すべく戦略的なポジショニングをとり、市場での存在感を高めています。

農業用キレート化合物市場の動向

農業におけるEDTA選好の高まり

- エチレンジアミン四酢酸(EDTA)は、農業における主要な合成キレート剤として頭角を現し、土壌および葉面栄養剤の両方に広く使用されています。土壌pHが6.0前後であれば、EDTAは露地施肥でその有効性を発揮します。この適応性の高さが、EDTAの市場における主導的地位を確固たるものにしています。

- EDTAキレートは、鉄(Fe)、マンガン(Mn)、銅(Cu)、亜鉛(Zn)などの必須微量元素を土壌から直接植物の根に移行させる効率に優れているため、従来の無機物よりも好まれている。インド土壌科学研究所(Indian Institute of Soil Science)は、微量栄養素の欠乏が蔓延しているという懸念すべき動向を強調しています。インドの土壌における平均欠乏率は、亜鉛が43.0%、鉄が12.1%、銅が5.4%、マンガンが5.6%、ホウ素が18.3%です。憂慮すべきことに、酸性土壌では亜鉛とリン酸が、半乾燥地域では亜鉛と鉄が欠乏しており、将来の作付体系に潜在的な課題があることを示しています。重要な微量栄養素である亜鉛は、植物ホルモンのバランスを維持し、成長を促進するために不可欠です。有機キレート亜鉛源、特にZn-EDTA(Znを12%含む)は、無機代替品よりも優れているとみなされることが多いです。例えば、トウモロコシや豆類などの作物にZn-EDTAキレート肥料を施用する場合、農家は従来の硫酸亜鉛(ZnSO4)の半分の量で済みます。さらに、EDTAキレートは価格が安いだけでなく、現在入手可能な他の多くの市販農業用キレートよりも入手しやすいという利点もあります。

- 市場の有力企業は、農業用に調整された幅広いEDTA製品を展示しています。例えばCorteva社は、VersenolとCrop Maxというブランド名でEDTAキレート剤を提供しており、いずれも農業界で高い需要があります。EDTAは栄養剤としての用途だけでなく、水銀、カドミウム、鉛などの重金属で汚染された土壌を無害化する能力もあり、市場の拡大に拍車をかけています。しかし、EDTAにも課題がないわけではないです。多くの合成薬剤と同様、EDTAは高コスト、限定的な生分解性、潜在的な二次汚染リスクといった問題に取り組んでいます。これらの課題は、このセグメントの成長軌道を阻害する可能性があります。

アジア太平洋が市場を独占

- アジア太平洋では、中国、インド、日本、オーストラリアが農業用キレート剤の市場需要をリードしています。オーストラリア政府によると、アルカリ性土壌はオーストラリアの土地の約24%を占めており、特に西部地域ではpHレベルが4~8.5となっています。その結果、オーストラリアでは、農業の生産性向上を妨げる微量元素の欠乏を背景に、キレート剤の需要が増加しています。

- 世界最大の人口を抱える中国は、最も広大な農業施設も擁しています。人口が急増し、食糧需要が高まる中、中国の農家はより高い作物収量を達成する必要に迫られています。しかし、中国のさまざまな地域では、石灰質土壌における微量栄養素の欠乏に悩まされています。このような課題に対処するため、中国は北京の非営利環境保護団体が主導する包括的な土壌センサスに取り組んでおり、2025年の完了を目指しています。この土壌調査から得られる知見は、土壌の欠乏を明らかにし、同国でのキレート剤の売上を押し上げる可能性があります。

- 微量栄養素の欠乏は、タイをはじめとするコメ生産国の生産性を損なっています。ある独自の研究では、主要な微量栄養素(Fe、Mn、Zn、Cu)が極めて重要であることが特定され、それらの欠乏は米粒の収量を24.12%~46.46%も減少させる可能性があることが明らかになりました。しかし、DTPAを適用すれば、これらの微量栄養素の添加により、収量を大幅に向上させることができます。

農業用キレート化合物産業の概要

世界の農業用キレート化合物市場は統合されており、BASF SE、三菱化学、Syngenta Ag、Dow Inc、Nouryon Chemicals Holding B.Vなどの大手企業が大きなシェアを占めています。これらの企業の市場シェアが大きいのは、高度に多様化した製品ポートフォリオと、レビュー期間中の買収や提携に起因しています。これらの企業はまた、地理的プレゼンスを拡大するため、研究開発や製品イノベーションにも注力しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 農作物の高収量化に対する需要

- 微量栄養素中毒におけるキレートの応用

- 土壌における微量栄養素の欠乏

- 市場抑制要因

- 生分解性キレート化合物の貧弱な製品提供

- 合成キレート剤の使用に対する規制の高まり

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- 合成

- EDTA

- EDDHA

- DTPA

- IDHA

- その他の合成タイプ

- 有機

- リンゴ硫酸塩

- アミノ酸

- ヘプタグルコン酸塩

- その他の有機タイプ

- 合成

- 用途

- 土壌

- 葉面散布

- 施肥

- その他の用途

- 作物タイプ

- 穀物

- 豆類および油糧種子

- 商業作物

- 果物および野菜

- 芝・観葉植物

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他の北米地域

- 欧州

- スペイン

- 英国

- フランス

- ドイツ

- ロシア

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- アフリカ

- 南アフリカ

- その他のアフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Nouryon Chemicals Holding B.V

- Shandong Iro Chelating Chemical Co. Ltd

- Ava Chemicals Private Limited

- Protex International

- Innospec Inc.

- Syngenta Ag

- Mitsubishi Group(Mitsubishi Chemical Corporation)

- Dow Inc

第7章 市場機会と今後の動向

The Agricultural Chelates Market size is estimated at USD 1.18 billion in 2025, and is expected to reach USD 1.68 billion by 2030, at a CAGR of 7.34% during the forecast period (2025-2030).

Key Highlights

- Concerns over food security are rising due to changing climate conditions, diminishing arable land, and a swiftly expanding global population. The 2022 Census of Agriculture, conducted by the United States Department of Agriculture (USDA), revealed that the number of farms in the United States (U.S.) has dipped below 2 million. Specifically, in 2022, the U.S. counted 1.9 Million farms, marking a 7% decrease from the figures in the 2017 Census. Additionally, the Census highlighted a 2.2% reduction in total U.S. farmland, bringing it down to 880 million acres in 2022. Given these developments, boosting productivity through appropriate agricultural inputs has become imperative. Consequently, there's been a notable surge in the adoption of chelating agents in agriculture, to enhance crop yields to satisfy global food requirements. Chelating agents facilitate plants' uptake of nutrients, making certain nutrients more accessible. This leads to improved plant growth and development, ultimately enhancing crop yield and quality.

- Independent laboratory analyses highlight troubling trends, includes wheat crops in the UK are experiencing a 10% nitrogen deficiency and a 25% phosphorus deficiency, as evidenced by thousands of soil samples. Chelation serves as a protective mechanism, shielding micronutrients from unwanted reactions in both solutions and soil. By boosting the bioavailability of micronutrients like Fe, Cu, Mn, and Zn, chelated fertilizers play a pivotal role in enhancing the productivity and profitability of commercial crop production. Notably, in soils with a pH exceeding 6.5 or those under low-micronutrient stress, chelated fertilizers have demonstrated a superior capacity to boost commercial yields compared to standard micronutrients.

- With the rising momentum of sustainable farming and growing awareness about the environmental repercussions of synthetic chelating agents, there's a marked pivot towards exploring biodegradable alternatives. In light of this, companies are strategically positioning themselves to meet this evolving demand, thereby strengthening their market presence.

Agricultural Chelates Market Trends

Increasing Preference for EDTA in Agriculture

- Ethylenediaminetetraacetic acid (EDTA) has emerged as the premier synthetic chelating agent in agriculture, widely employed for both soil and foliar nutrient applications. At soil pH levels around 6.0, EDTA demonstrates its efficacy in open-field fertigation. This adaptability plays a pivotal role in cementing EDTA's leading market position.

- EDTA chelates are preferred over conventional inorganic sources due to their superior efficiency in transferring essential trace elements such as iron (Fe), manganese (Mn), copper (Cu), and zinc (Zn)-from the soil directly to plant roots. The Indian Institute of Soil Science highlights a concerning trend of micronutrient deficiencies are widespread, with average deficiencies in Indian soils being 43.0% for Zinc, 12.1% for Iron, 5.4% for Copper, 5.6% for Manganese, and 18.3% for Boron. Alarmingly, the combined deficiency of Zn and B in acidic soils, and Zn and Fe in semi-arid regions, signals potential challenges for future cropping systems. Zinc, a crucial micronutrient, is essential for maintaining plant hormone balance and fostering growth. Organic chelated zinc sources, particularly Zn-EDTA (which contains 12% Zn), are frequently regarded as superior to their inorganic alternatives. For instance, when treating crops like corn and beans, the application of Zn-EDTA chelate fertilizer allows farmers to use only half the quantity compared to traditional zinc sulfate (ZnSO4). Additionally, EDTA chelates not only come at a lower price point but also boast greater accessibility than numerous other commercial agricultural chelates available today.

- Prominent players in the market showcase a wide array of EDTA products tailored for agricultural use. Corteva, for instance, offers its EDTA chelating agents under the brand names Versenol and Crop Max, both of which are in high demand within the agricultural community. Beyond its nutrient application, EDTA's ability to detoxify soils contaminated with heavy metals like mercury, cadmium, and lead further fuels its market expansion. However, EDTA isn't without its challenges. Like many synthetic agents, it grapples with issues such as high costs, limited biodegradability, and potential secondary pollution risks. These challenges could hinder the segment's growth trajectory.

Asia-Pacific Dominates the Market

- In the Asia-Pacific region, China, India, Japan, and Australia lead in market demand for agricultural chelates. According to the Australian Government, alkaline soils account for about 24% of Australia's land, particularly in the western regions, where pH levels range from 4 to 8.5. As a result, Australia is experiencing an increasing demand for chelating agents, driven by trace element deficiencies that impede agricultural productivity growth.

- China, home to the world's largest population, also hosts some of the most expansive agricultural facilities. With its population surging and food demand rising, Chinese farmers are under pressure to achieve higher crop yields. Yet, various regions in China grapple with micronutrient deficiencies in their calcareous soils. To address these challenges, China is undertaking a comprehensive soil census, led by a nonprofit environmental organization from Beijing, with an anticipated completion in 2025. Insights from this soil survey are poised to illuminate soil deficiencies, potentially boosting chelate sales in the nation.

- Micronutrient deficiencies are currently undermining productivity in rice-growing nations, notably Thailand. An independent study identified key micronutrients (Fe, Mn, Zn, and Cu) as pivotal, revealing their deficiency could slash rice grain yields by a staggering 24.12%-46.46%. However, with the application of DTPA, these yields can be significantly bolstered through the addition of these micronutrients.

Agricultural Chelates Industry Overview

The global agricultural chelates market is consolidated, with the major players in the market including BASF SE, Mitsubishi Chemical Corporation, Syngenta Ag, Dow Inc, Nouryon Chemicals Holding B.V, etc holding a significant share of the market. The significant market share of these players can be attributed to a highly diversified product portfolio and acquisitions and partnerships during the review period. These players also focus on R&D and product innovations to widen their geographical presence.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand For Higher Crop Yields

- 4.2.2 Application of Chelates in Micronutrient Intoxication

- 4.2.3 Micronutrient Deficiency In Soil

- 4.3 Market Restraints

- 4.3.1 Poor Product Offering in Biodegradable Chelates

- 4.3.2 Rising Regulation on Use of Synthetic Chelating Agents

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Synthetic

- 5.1.1.1 EDTA

- 5.1.1.2 EDDHA

- 5.1.1.3 DTPA

- 5.1.1.4 IDHA

- 5.1.1.5 Other Synthetic Types

- 5.1.2 Organic

- 5.1.2.1 LingoSulphates

- 5.1.2.2 Aminoacids

- 5.1.2.3 Heptagluconates

- 5.1.2.4 Other Organic Types

- 5.1.1 Synthetic

- 5.2 Application

- 5.2.1 Soil

- 5.2.2 Foliar

- 5.2.3 Fertigation

- 5.2.4 Other Applications

- 5.3 Crop Type

- 5.3.1 Grains and Cereals

- 5.3.2 Pulses and Oilseeds

- 5.3.3 Commercial Crops

- 5.3.4 Fruits and Vegetables

- 5.3.5 Turf and Ornamentals

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Spain

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Germany

- 5.4.2.5 Russia

- 5.4.2.6 Italy

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Nouryon Chemicals Holding B.V

- 6.3.2 Shandong Iro Chelating Chemical Co. Ltd

- 6.3.3 Ava Chemicals Private Limited

- 6.3.4 Protex International

- 6.3.5 Innospec Inc.

- 6.3.6 Syngenta Ag

- 6.3.7 Mitsubishi Group (Mitsubishi Chemical Corporation)

- 6.3.8 Dow Inc