|

市場調査レポート

商品コード

1693440

小麦種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Wheat Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 小麦種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 399 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

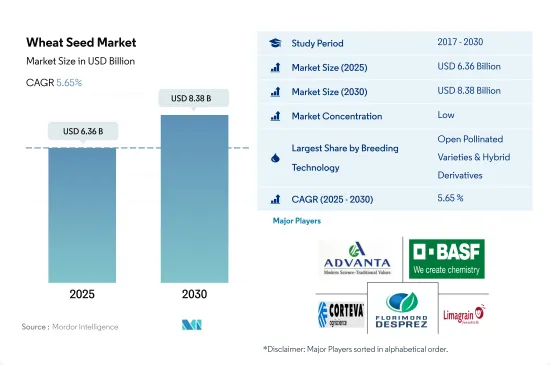

小麦種子市場規模は2025年に63億6,000万米ドルと予測され、2030年には83億8,000万米ドルに達し、予測期間中(2025~2030年)にCAGR 5.65%で成長すると予測されています。

開放受粉品種が世界の小麦種子市場を独占

- 世界全体では、2022年には、開放受粉品種とハイブリッド派生品種が小麦種子市場の9%を占めました。OPVは自家受粉であり、開放受粉種子品種は低コストであるため、世界中で栽培に多く使用されているからです。2022年には、北米が小麦の栽培に開放受粉品種とハイブリッド派生品種を使用する最大の地域であり、世界の小麦種子市場の25%を占めました。これは、世界におけるOPVの手頃な価格と入手可能性の高さに関連しています。

- ブラジルとスペインは、世界のOPV小麦種子市場で最も急成長している国です。両国は、農家からの需要と国際市場からの小麦需要の増加により、予測期間中に10.7%と8.4%のCAGRで推移すると予測されています。

- 世界全体では、ハイブリッド種子は2022年の小麦種子市場全体のわずか5%を占めるに過ぎなかったが、高収量で投入効率の高い種子品種に対する需要の増加により、2030年までに58%増加すると予測されます。ハイブリッド種子は1ヘクタール当たりの収量を40%向上させることができるため、アジア太平洋地域におけるハイブリッド種子分野の成長に貢献します。2022年、ハイブリッド種子のうち、非遺伝子組み換え小麦種子は世界の小麦種子市場の約95.4%を占め、遺伝子組み換え種子は世界のハイブリッド小麦種子市場の4.5%を占める。最近、2022年にアルゼンチンとブラジルが遺伝子組み換え小麦(HB4)の干ばつ耐性品種の栽培を承認しました。

- 開放受粉品種は肥料や農薬などの投入が少なくて済み、低所得農家にとってより手頃な価格であることから、予測期間中のOPV小麦種子市場のCAGRは5.6%と予測されます。

小麦の高い消費需要と低投資が市場成長の要因

- 2022年、小麦種子市場は世界の種子市場価値の8.2%を占めました。小麦種子市場価値は2017年から2022年の間に57.8%増加しました。欧州は世界最大の小麦生産国でした。世界の小麦種子市場の45.3%のシェアを占めました。フランス、ドイツ、英国、ウクライナ、ロシアがこの地域で最大のシェアを占め、2022年には合わせて世界の小麦種子市場の30.1%を占めました。

- 2022年、米国は、ハイブリッド種子よりも開放受粉種子品種が多く使用されるため、より高い種子貯蔵と高いROIにより、世界の小麦種子市場の20.3%の市場シェアを占めました。

- 南米のハイブリッド小麦種子市場は、栽培面積の増加と小麦の世界の需要により、予測期間中にCAGR 9.9%で成長すると予測されます。南米の小麦栽培面積は、世界の需要を満たすために小麦を大量生産するためにより多くのOPVが使用されたため、2017年から2022年の間に22%以上増加しました。

- 南米の生産者は、ウクライナ・ロシア戦争による生産と需要の不足を補うため、より多くの小麦を栽培すると推定されます。アルゼンチンは南米の主要な小麦生産・輸出国で、2022年には世界輸出の約7%を占める。

- 小麦におけるOPVの使用率は、ハイブリッドよりも手ごろで、次の作期まで保存できることから高いです。したがって、ハイブリッド種子に比べてOPV種子の価格が低いため、生産者は種子への投資が少なくて済み、ROIが高くなります。

- このように、小麦の高い消費量と低い投資額は、予測期間中に小麦セグメントの成長をCAGR 5.6%で押し上げる可能性が高いです。

世界の小麦種子市場動向

主食としての消費者とバイオ燃料を生産する加工産業からの需要により栽培面積が増加

- 世界的に小麦は主に温帯地域と亜熱帯地域で主食として栽培されています。アジア太平洋の小麦栽培面積は世界最大であり、2022年には約9,600万ヘクタールとなります。アジア太平洋における小麦栽培の主要国はインドと中国で、2022年におけるアジア太平洋の小麦栽培面積の32.7%と24.4%を占めています。欧州地域は小麦の栽培面積が2番目に大きく、良好な気候条件のため2022年には約7,030万ヘクタールとなります。同市場では、消費者や加工産業からの需要の増加が見込まれています。ロシアでは、2022年の収穫面積は2,810万ヘクタールで、2017年から2.3%増加しました。このように、小麦の作付面積の増加が市場の成長を後押ししています。国内需要と製粉用の工業用小麦需要(澱粉とバイオエタノールを含む)は、2021年と比較して2022年は2.8%増加しました。この需要により、予測期間中の同地域の小麦作付面積は増加すると予想されます。

- 北米は世界第3位の小麦生産国で、2022年の世界の小麦生産量の約11.3%を占めています。米国は、2022年に約1,510万ヘクタールの小麦を生産する同地域の主要生産国です。同国における小麦需要の増大は、予測期間中の小麦作付面積全体を牽引すると予想されます。

- 小麦は多くの国の主食であるため需要の増加、高収量品種の入手可能性の増加、非公開会社によるストレス耐性品種や耐病性品種の研究の増加は、世界的に小麦の栽培面積を増加させ、予測期間中の小麦種子需要を増加させると予想されます。

耐病性と幅広い適応性形質への需要の高まりが収量を押し上げ、市場成長を牽引

- 小麦は、主に温帯地域や亜熱帯地域で主食作物として栽培されている主要な穀物です。人気の高い形質は、病害抵抗性、幅広い適応性、その他(宿根耐性や品質属性を含む)です。

- 収量に大きな損失をもたらす一般的な病害は、さび病、フザリウム菌核病、セプトリア葉枯病、縞さび病、斑点病、褐斑病、うどんこ病です。これらの病害に耐性を持つ品種への需要は、生産者の導入拡大につながると予想されます。さらに、小麦はインドで最も重要かつ栽培されている食用穀物のひとつです。同国で最も人気のある作物の形質には、耐病性、耐宿主性、幅広い適応性、粒の大きさ、粒の色などの品質属性が含まれます。さび病や鈍性スマット病は50%以上の収量低下を引き起こすため、耐病性種子品種に対する需要は大きいです。例えば、2021年にはBASF SEがハイブリッド小麦用のIdeltis種子ブランドを開発し、高い収量と品質などの特徴を提供しています。

- 欧州では、Syngenta、Groupe Limagrain、KWS SAATなどの企業が、SY Insitor、Graham、LG Typhoon、LG Princeなどの病害虫抵抗性小麦品種を提供し、セプトリア、さび病、OWBM(Orange Wheat Blossom Midge)などの病害による収量減に対処しています。さらに2021年には、バイエルとRAGT Semencesは、最新の育種手法、高性能な種子製品システム、高度なデジタルソリューションを用いてハイブリッド小麦種子を開発するパートナーシップ契約を締結しました。吸汁性病害虫の蔓延や、短期間での高収量に対する需要の高まりが、予測期間中に改良種子品種の需要を高めています。

小麦種子産業の概要

小麦種子市場は断片化されており、上位5社で21.58%を占めています。この市場の主要企業は以下の通りです。 Advanta Seeds-UPL, BASF SE, Corteva Agriscience, Florimond Desprez and Groupe Limagrain(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 栽培面積

- 最も人気のある形質

- 育種技術

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非遺伝子組み換え雑種

- 遺伝子組み換え雑種

- その他の形質

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 地域

- アフリカ

- 育種技術別

- 国別

- エジプト

- エチオピア

- ケニア

- ナイジェリア

- 南アフリカ

- タンザニア

- その他のアフリカ

- アジア太平洋

- 育種技術別

- 国別

- オーストラリア

- バングラデシュ

- 中国

- インド

- 日本

- ミャンマー

- パキスタン

- タイ

- その他アジア太平洋地域

- 欧州

- 育種技術別

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ポーランド

- ルーマニア

- ロシア

- スペイン

- トルコ

- ウクライナ

- 英国

- その他欧州

- 中東

- 育種技術別

- 国別

- イラン

- サウジアラビア

- その他中東

- 北米

- 飼育技術別

- 国別

- カナダ

- メキシコ

- 米国

- その他北米

- 南米

- 育種技術別

- 国別

- アルゼンチン

- ブラジル

- その他南米地域

- アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- BASF SE

- Corteva Agriscience

- Florimond Desprez

- Groupe Limagrain

- Hefei Fengle Seed Industry Co. Ltd

- Kaveri Seeds

- KWS SAAT SE & Co. KGaA

- RAGT Group

- Seed Co. Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92502

The Wheat Seed Market size is estimated at 6.36 billion USD in 2025, and is expected to reach 8.38 billion USD by 2030, growing at a CAGR of 5.65% during the forecast period (2025-2030).

Open pollinated varieties dominated the global wheat seed market

- Globally, in 2022, open pollinated varieties and hybrid derivatives accounted for 9% of the wheat seed market, as it is largely used for cultivation across the globe due to OPV being self-pollinated and the lower cost of open-pollinated seed varieties. In 2022, North America was the largest region using open-pollinated varieties and hybrid derivatives for the cultivation of wheat, accounting for 25% of the global wheat seed market. This is associated with the affordability and high availability of OPVs in the world.

- Brazil and Spain are the fastest-growing countries in the global OPV wheat seed market. Both countries are projected to register a CAGR of 10.7% and 8.4% during the forecast period due to the demand from farmers and the increase in the demand for wheat from international markets.

- Globally, hybrids accounted for only 5% of the total wheat seed market in 2022, which is projected to increase by 58% by 2030 due to the increase in the demand for high-yielding and input-efficient seed varieties. Hybrid seeds can produce a 40% higher yield per hectare, which will help in the growth of the hybrid seed segment in Asia-Pacific. In 2022, among hybrids, non-transgenic wheat seeds accounted for about 95.4% of the global wheat seed market, whereas transgenic seeds accounted for 4.5% of the global hybrid wheat seed market. Recently, in 2022, Argentina and Brazil approved the cultivation of transgenic wheat (HB4) drought-tolerant varieties.

- Open pollinated varieties require fewer inputs, such as fertilizers and pesticides, and they are more affordable for low-income farmers, which is projected to drive the OPV wheat seed market during the forecast period with a CAGR of 5.6%.

High consumption demand of wheat and lower investment are factors driving the market growth

- In 2022, wheat seed market accounted for 8.2% of the global seed market value. The wheat seed market value increased by 57.8% between 2017 and 2022. Europe was the largest wheat producer globally. It accounted for a 45.3% share of the global wheat seed market. France, Germany, the United Kingdom, Ukraine, and Russia held the largest share in the region, together accounted for 30.1% of the global wheat seed market in 2022.

- In 2022, the United States held a market share of 20.3% of the global wheat seed market due to higher seed storage and high ROI, as open-pollinated seed varieties are used more than hybrid seeds.

- The South American hybrid wheat seed market is anticipated to grow at a CAGR of 9.9% during the forecast period due to the increased cultivation area and the global demand for wheat. The wheat cultivation area in South America increased by more than 22% between 2017 and 2022 as more OPVs were used to produce wheat in large quantities to meet the global demand.

- South American growers are estimated to cultivate more wheat to compensate for the deficit in production and demand due to the Ukraine-Russia war. Argentina is the primary South American producer and exporter of wheat, accounting for about 7% of the global exports in 2022.

- The usage of OPVs in wheat is higher as they are more affordable than hybrids and can be saved for the next crop season. Thus, growers can have a higher ROI as less investment is required for seeds due to the lower price of OPVs than hybrid seeds.

- Thus, the high consumption of wheat and lower investment are likely to boost the wheat segment's growth during the forecast period at a CAGR of 5.6%.

Global Wheat Seed Market Trends

The demand from consumers as a staple food and processing industries to produce biofuel led to an increase in the area under cultivation

- Globally, wheat is cultivated mainly in temperate regions and subtropical regions as a staple food. Asia-Pacific has the largest area under wheat cultivation in the world, with about 96.0 million hectares in 2022. The major countries for wheat cultivation in Asia-Pacific are India and China, which accounted for 32.7% and 24.4% of the total acreage under wheat in Asia-Pacific in 2022. The European region has the second largest area under wheat cultivation, with about 70.3 million hectares in 2022 due to the favorable climatic conditions. The demand from consumers and processing industries is expected to increase in the market. In Russia, the area harvested was 28.1 million hectares in 2022, which increased by 2.3% since 2017. Thus, an increase in the acreage under wheat is fueling the growth of the market. The domestic demand and industrial wheat demand for flour milling (including starch and bio-ethanol) was 2.8% higher in 2022 compared to 2021. This demand is anticipated to drive wheat acreage in the region during the forecast period.

- North America is the third-largest producer of wheat in the world, which accounted for about 11.3% of the global wheat production in 2022. The United States is the major producer of wheat in the region with about 15.1 million hectares in 2022. The growing demand for wheat in the country is anticipated to drive the overall wheat acreage during the forecast period.

- The increase in the demand as it is the staple food of many countries, an increase in the availability of high-yielding varieties, and the increase in research on stress-tolerant and disease-resistant varieties by private companies are expected to increase the area under cultivation of wheat globally, thereby increasing the demand for wheat seeds during the forecast period.

Increasing demand for disease resistant and wider adaptability traits to boost the yield and drive the growth of market

- Wheat is the major grain crop cultivated mainly in temperate regions and subtropical regions as a staple food crop. The popular traits are disease resistance, wider adaptability, and others (including lodging tolerance and quality attributes).

- The common diseases that cause significant yield losses are rust, fusarium head blight, Septoria leaf blotch, stripe rust, spot blotch, tan spot, and powdery mildew. The demand for varieties with resistance to these diseases is expected to lead to higher adoption by growers. Furthermore, wheat is one of the most important and cultivated food grains in India. The most popular traits of the crop in the country include disease resistance, lodging tolerance, wider adaptability, and quality attributes such as grain size, grain color, and others. There is significant demand for disease-resistant seed varieties to resist rust and blunt smut traits as the diseases cause yield losses of more than 50%. For instance, in 2021, BASF SE developed the Ideltis seed brand for hybrid wheat, which provides characteristics such as high yield and quality.

- In Europe, companies such as Syngenta, Groupe Limagrain, and KWS SAAT are offering disease and pest-resistant wheat varieties such as SY Insitor, Graham, LG Typhoon, and LG Prince to address yield losses caused by diseases such as Septoria, rusts, OWBM (Orange Wheat Blossom Midge). Additionally, in 2021, Bayer and RAGT Semences signed a partnership agreement to develop hybrid wheat seeds using the latest breeding methodologies, high-performing seed product systems, and advanced digital solutions. The prevalence of sucking pests and diseases, as well as higher demand for higher yields in shorter periods, are increasing the demand for improved seed varieties during the forecast period.

Wheat Seed Industry Overview

The Wheat Seed Market is fragmented, with the top five companies occupying 21.58%. The major players in this market are Advanta Seeds - UPL, BASF SE, Corteva Agriscience, Florimond Desprez and Groupe Limagrain (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.2 Most Popular Traits

- 4.3 Breeding Techniques

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Other Traits

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Region

- 5.2.1 Africa

- 5.2.1.1 By Breeding Technology

- 5.2.1.2 By Country

- 5.2.1.2.1 Egypt

- 5.2.1.2.2 Ethiopia

- 5.2.1.2.3 Kenya

- 5.2.1.2.4 Nigeria

- 5.2.1.2.5 South Africa

- 5.2.1.2.6 Tanzania

- 5.2.1.2.7 Rest of Africa

- 5.2.2 Asia-Pacific

- 5.2.2.1 By Breeding Technology

- 5.2.2.2 By Country

- 5.2.2.2.1 Australia

- 5.2.2.2.2 Bangladesh

- 5.2.2.2.3 China

- 5.2.2.2.4 India

- 5.2.2.2.5 Japan

- 5.2.2.2.6 Myanmar

- 5.2.2.2.7 Pakistan

- 5.2.2.2.8 Thailand

- 5.2.2.2.9 Rest of Asia-Pacific

- 5.2.3 Europe

- 5.2.3.1 By Breeding Technology

- 5.2.3.2 By Country

- 5.2.3.2.1 France

- 5.2.3.2.2 Germany

- 5.2.3.2.3 Italy

- 5.2.3.2.4 Netherlands

- 5.2.3.2.5 Poland

- 5.2.3.2.6 Romania

- 5.2.3.2.7 Russia

- 5.2.3.2.8 Spain

- 5.2.3.2.9 Turkey

- 5.2.3.2.10 Ukraine

- 5.2.3.2.11 United Kingdom

- 5.2.3.2.12 Rest of Europe

- 5.2.4 Middle East

- 5.2.4.1 By Breeding Technology

- 5.2.4.2 By Country

- 5.2.4.2.1 Iran

- 5.2.4.2.2 Saudi Arabia

- 5.2.4.2.3 Rest of Middle East

- 5.2.5 North America

- 5.2.5.1 By Breeding Technology

- 5.2.5.2 By Country

- 5.2.5.2.1 Canada

- 5.2.5.2.2 Mexico

- 5.2.5.2.3 United States

- 5.2.5.2.4 Rest of North America

- 5.2.6 South America

- 5.2.6.1 By Breeding Technology

- 5.2.6.2 By Country

- 5.2.6.2.1 Argentina

- 5.2.6.2.2 Brazil

- 5.2.6.2.3 Rest of South America

- 5.2.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 BASF SE

- 6.4.3 Corteva Agriscience

- 6.4.4 Florimond Desprez

- 6.4.5 Groupe Limagrain

- 6.4.6 Hefei Fengle Seed Industry Co. Ltd

- 6.4.7 Kaveri Seeds

- 6.4.8 KWS SAAT SE & Co. KGaA

- 6.4.9 RAGT Group

- 6.4.10 Seed Co. Limited

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms