|

市場調査レポート

商品コード

1444514

芝生および観賞用投入材:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Turf & Ornamental Inputs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 芝生および観賞用投入材:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

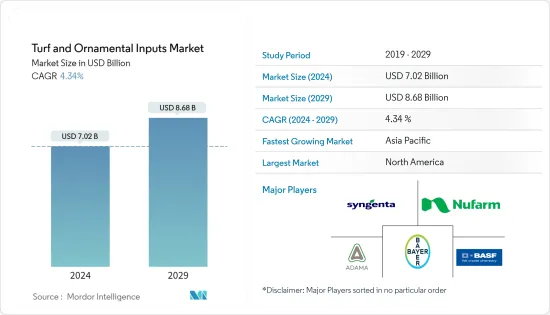

芝生および観賞用投入材の市場規模は、2024年に70億2,000万米ドルと推定され、2029年までに86億8,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に4.34%のCAGRで成長します。

主なハイライト

- 芝生および観賞用投入材は、植物の成長と保護に必要な肥料、殺虫剤、その他の成長調節剤です。特に芝生や観賞用の化学物質投入産業は、作物配合の動向や環境規制の変化と相まって堅調な成長を遂げ、長年にわたって変革を続けてきました。

- 人口の増加、耕作可能な土地の減少、食糧安全保障、農業生産性の向上の必要性は、より高い農業生産高への需要を促進する重要な要因であり、その結果、世界中で作物保護産業の成長が促進されています。特に灌漑投入量が少なくて済む状況では、芝草の色と品質が着色剤によって最適化されます。定期的に処理することで競技面が改善され、芝刈りの必要性が減り、極度に乾燥した条件下ではオーバーシードの代わりに使用できます。

- 地方自治体や州政府が水制限を法的に定めている状況では、着色剤が便利なツールとなります。土壌界面活性剤は、処理される土壌の湿潤、再湿潤、および浸透速度に有利な影響を与えることにより、自然に乾燥しやすい土壌に存在する作物および草の生理学的ストレスを軽減することを目的としています。

芝生および観賞用投入材市場の動向

ゴルフコースとスポーツフィールドの開発が進む

芝生および観賞用投入材は、ゴルフコースやスポーツ場の芝生の維持に重要な役割を果たします。ゴルフコースの芝生は、雑草や昆虫を防除し、窒素施肥などの栄養素を導入するために、グリーンキーパーによって注意深く維持されています。コースを魅力的で優れたプレーコンディションに保つには、適切かつスケジュールどおりに施肥することが必要です。芝草は、成長を促進し、重要な栄養素を供給する肥料の結果、より強く、より弾力性のあるものになります。肥料を使用することで健全な芝生を維持したり、枯れたり休眠した芝生を復活させたりすることができます。

Golf Around the World 2021によると、206か国に38,081のゴルフコースがありました。ゴルフは米国で人気のスポーツであり、現在国内には15,000以上のゴルフコースがあります。フロリダは退職者(ゴルフをよくする傾向がある)に人気の目的地であり、一年中ゴルフをするのに最適な気候を備えています。フロリダに次いでゴルフコースが最も多い州は、ニューヨーク、カリフォルニア、テキサス、オハイオ、ミシガンです。

市場には他にも多くの肥料の混合物や組み合わせがありますが、リン、カリウム、窒素が肥料の維持に使用される3つの主要な肥料であり、その中で窒素が最も重要なものです。これら3つの栄養素のN(窒素)が葉や茎の健全な成長を促します。これにより、春から夏にかけて最高の太くて強い草を育てることができます。メンテナンスの手間がかからないエリアでは、単一の窒素源で芝生のニーズを満たすことができます。しかし、芝生、ゴルフコース、運動場などの需要がより大きい場合は、さまざまな供給源、高分子着色剤、界面活性剤の組み合わせが必要です。

北米が市場を独占

北米は現在、芝生および観賞用投入材の世界最大の市場であり、米国、カナダ、メキシコなどの国々が、管理された持続可能な芝生の成長のためにスポーツフィールドを大規模に採用していることを示しています。さらに、所得の増加と都市化により、国民は芝生の芝生の維持に積極的に支出を増やしています。

労働統計局の調査によると、2020年の芝生の維持にかかる年間支出は2018年の113.61ドルから115.07ドルに増加しました。米国では、新世代の肥料はその外観と価値を高めるために着色されています。たとえば、Sun Chemicalという会社は、肥料用の幅広い着色剤を複数のシステムで提供しています。高い着色力によりコストの削減が期待される一方、耐光性特性により表面および塊状肥料の着色に対する紫外線に耐えられることが期待されます。

レジャー用の芝生と芝生は、米国で最も栽培されている作物の1つです。これらのレジャー用の芝生や芝生は、住宅所有者や商業施設が魅力を抑えるために景観を整えるために主に好まれています。北米の人々は、水の保全に役立つとして、在来の草に移行しつつあります。たとえば、テキサス州では、バッファローグラス、ブルーグラマ、サンダーターフなどの在来草が他の草や芝の品種に取って代わりつつあります。この要因により、今後数年間で肥料やその他の化学物質の需要がさらに高まることが予想されます。

芝生および観賞用投入材業界の概要

芝生および観賞用投入材市場は、世界市場の大部分を占める大手企業によって高度に統合されています。主要なプレーヤーは、BASF SE、Bayer CropScience AG、Syngenta、Nufarm Limited、およびAdama Limitedです。新製品のイノベーション、パートナーシップ、買収は、世界中の市場の大手企業が採用する主要戦略です。イノベーションと拡張に加えて、研究開発への投資と新しい製品ポートフォリオの開発は、今後数年間で重要な戦略となる可能性があります。これらの著名な企業は、世界中で新たなイノベーションと拡張を実現するために戦略的コラボレーションを考え出しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 芝草タイプ

- バミューダグラス

- シバ草

- ブルーケンタッキーグラス

- ライグラス

- トールフェスク

- その他

- 観賞用草タイプ

- フェザーヨシ草

- ファウンテングラス

- 紫アワ

- ラヴェンナグラス

- 光ファイバーグラス

- その他

- 合成化学物質投入材

- 農薬

- 肥料

- 植物成長調節剤

- その他

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米

- 欧州

- スペイン

- 英国

- フランス

- ドイツ

- デンマーク

- イタリア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- タイ

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- アフリカ

- 南アフリカ

- その他アフリカ

- 北米

第6章 競合情勢

- 市場シェア分析

- 最も採用されている戦略

- 企業プロファイル

- Adama Agricultural Solutions

- American Vanguard Corporation

- BASF SE

- Bayer Crop Sciences

- Chemisco Division of United Industries Corp.

- Chemtura Agro Solutions

- DowDuPont

- FMC Corporation

- Gowan International

- Koch Agronomic Services LLC

- Monsanto Company

- Nufarm Ltd

- Precision Laboratories

- Syngenta AG

第7章 市場機会と将来の動向

The Turf & Ornamental Inputs Market size is estimated at USD 7.02 billion in 2024, and is expected to reach USD 8.68 billion by 2029, growing at a CAGR of 4.34% during the forecast period (2024-2029).

Key Highlights

- Turf and Ornamentals chemicals are Fertilizers, Pesticides, and other growth regulators that are required in the growth and protection of plants. The chemical input industry particularly for turf and ornamental has been transforming over the years, with robust growth coupled with changing crop mix trends and environmental regulations.

- Growing population, declining arable land, food security, and the need for augmented agricultural productivity are the significant factors driving the demand for higher agricultural output, thus augmenting the growth of the crop protection industry, globally. Turfgrass color and quality are optimized by colorants, particularly in situations where less irrigation input is needed. Regular treatments will enhance playing surfaces, lessen the need for mowing, and under extremely dry conditions, they can be used in place of overseeding.

- In situations where municipal and state governments have legislated water restrictions, colorants offer a useful tool. By favorably influencing the wetting, rewetting, and infiltration rates of the soils treated, soil surfactants are intended to lessen crop and grass physiological stresses present in naturally drought-prone soils.

Turf & Ornamental Chemical Input Market Trends

Increasing Development of the Golf Courses and Sports Field

Turf and Ornamental chemicals input play an important role in the maintenance of the turf grasses of Golf courses and sports fields. Golf course turf grass is carefully maintained by a greenskeeper to control weeds, and insects and to introduce nutrients, such as nitrogen fertilization. Fertilizing properly and on schedule is necessary to keep the course attractive and in outstanding playing condition. Turf grass will become stronger and more resilient as a result of fertilizer, which promotes growth and supplies vital nutrients. With the use of fertilizer, healthy turf can be maintained, or dying or dormant turf can be revived.

According to the Golf Around the World 2021, there were 38,081 golf courses in 206 different countries. Golf is a popular sport in the United States, in which there are currently over 15,000 golf courses in the country. Florida is a popular destination for retirees (who tend to play a lot of golf) and it has a great climate for playing year-round. After Florida, the states with the most golf courses are New York, California, Texas, Ohio, and Michigan.

Although there are many other mixtures and combinations of fertilizers on the market, phosphorus, potassium, and nitrogen are the three major fertilizers used for their maintenance, out of which nitrogen is the most essential one. These three nutrients' N (nitrogen) promotes healthy leaf and stem growth. This helps grow the best thick and strong grass throughout the spring and summer months. In low-maintenance areas a single source of nitrogen may meet the needs of the turf. But where demands are greater as for lawns, golf courses and athletic fields, combinations of different sources, polymeric colorants and surfactants are necessary.

North America Dominates the Market

North America is currently the largest market for Turf & Ornamental Chemical Input in the world, with countries, like the United States, Canada, and Mexico, demonstrating massive adoption of sports fields for controlled and sustainable turf plant growth. Moreover, due to the increasing incomes and urbanization, the people in the country are willing to spend more on the maintenance of turf grasses in the lawns.

According to a study by the Bureau of labor statistics, in 2020, the annual spending on the maintenance of lawns increased from USD 113.61 in 2018 to USD 115.07. In the United States, the new generation fertilizer is colored to enhance its appearance and value. For instance, a company, Sun Chemical, provides a wide range of colorants for fertilizers in multiple systems. The high tinting strength is expected to reduce one's costs, while light fastness properties are expected to stand up to UV rays for surface and mass fertilizer coloration.

Leisure turf and lawns are among the most grown crops in the United States. These leisure turfs and lawns are mostly preferred by house owners and commercial places for landscaping to curb the appeal. People in North America are shifting to native grasses as they help in water conservation. For instance, in Texas, native grasses, such as buffalo grass, blue grama, and thunder turf, have been replacing other grass and turf varieties. This factor is further expected to boost the demand for fertilizers and othert chemical inputs during the coming years.

Turf & Ornamental Chemical Input Industry Overview

The Turf & Ornamental Chemical Input Market is highly consolidated with the leading companies occupying the majority of the global market. The major players are BASF SE, Bayer CropScience AG, Syngenta, Nufarm Limited, and Adama Limited. New product innovation, partnerships, and acquisitions are the major strategies adopted by the leading companies in the market across the globe. Along with innovations and expansions, investments in R&D and developing novel product portfolios will likely be crucial strategies in the coming years. These prominent companies are coming up with strategic collaborations to fetch new innovations and expansions around the globe.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forcess Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type of Turf Grass

- 5.1.1 Bermuda Grass

- 5.1.2 Zoysia Grass

- 5.1.3 Blue Kentucky Grass

- 5.1.4 Rye Grass

- 5.1.5 Tall Fescue

- 5.1.6 Others

- 5.2 Type of Ornamental Grass

- 5.2.1 Feather Reed Grass

- 5.2.2 Fountain Grass

- 5.2.3 Purple Millet

- 5.2.4 Ravenna Grass

- 5.2.5 Fibre Optic Grass

- 5.2.6 Others

- 5.3 Synthetic Chemical Inputs

- 5.3.1 Pesticides

- 5.3.2 Fertilizers

- 5.3.3 Plant Growth Regulators

- 5.3.4 Others

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Spain

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Germany

- 5.4.2.5 Denmark

- 5.4.2.6 Italy

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Thailand

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share Analysis

- 6.2 Most Adopted Strategies

- 6.3 Company Profiles

- 6.3.1 Adama Agricultural Solutions

- 6.3.2 American Vanguard Corporation

- 6.3.3 BASF SE

- 6.3.4 Bayer Crop Sciences

- 6.3.5 Chemisco Division of United Industries Corp.

- 6.3.6 Chemtura Agro Solutions

- 6.3.7 DowDuPont

- 6.3.8 FMC Corporation

- 6.3.9 Gowan International

- 6.3.10 Koch Agronomic Services LLC

- 6.3.11 Monsanto Company

- 6.3.12 Nufarm Ltd

- 6.3.13 Precision Laboratories

- 6.3.14 Syngenta AG