|

市場調査レポート

商品コード

1851235

自動気泡コンクリート(AAC):市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Autoclaved Aerated Concrete (AAC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動気泡コンクリート(AAC):市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

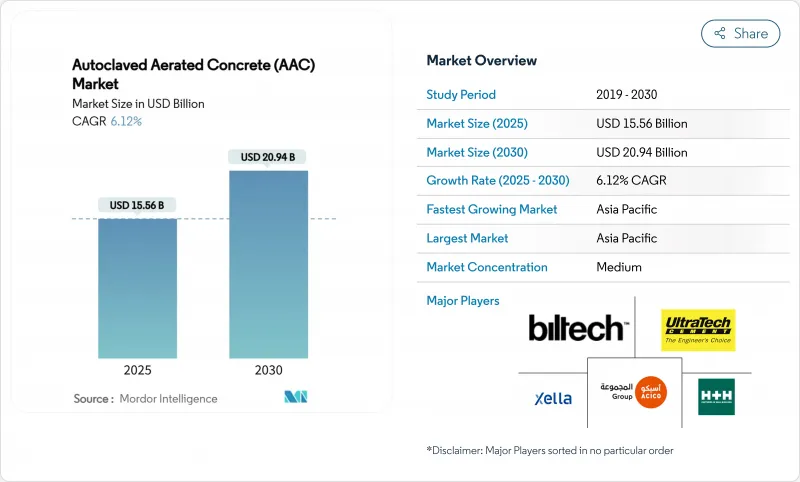

2025年のオートクレーブド・エアレーテッド・コンクリート市場規模は155億6,000万米ドルと推計され、予測期間(2025~2030年)のCAGRは6.12%で、2030年には209億4,000万米ドルに達すると予測されます。

成長の原動力となっているのは、グリーンビルディングの義務化、耐震構造に対する需要の高まり、モジュール建築の急速な普及などであり、これらすべてがAACの軽量でエネルギー効率の高い特性を際立たせています。伝統的な石積みの主流は依然としてブロックだが、プレハブ化によってプロジェクトのスケジュールが見直されるにつれて、パネルも勢いを増しています。アジア太平洋は都市化とインフラ整備を背景に世界需要の半分近くを占め、北米と欧州は厳しいエネルギー規制と耐震規制を背景にしています。メーカーは、需要の急増に対応し、コスト構造を改善し、地域のサプライチェーンを強化するために、生産能力を拡大し、工場を自動化しています。

世界の自動気泡コンクリート(AAC)市場の動向と洞察

新築・改築工事の需要拡大

新興経済国での住宅および商業施設の着工急増により、基礎荷重を低減し、プロジェクトサイクルを短縮する軽量素材が不可欠となっています。AACは自重を30~40%削減し、基礎のスリム化と床から床への素早い移動を可能にします。インドでは住宅建設が盛んで、国内メーカーのBigBloc Construction社は、都市部の住宅認可の増加に対応するため、生産能力を拡大しています。AACの精密なブロックは、構造ラインを改修することなく改修を合理化できるため、改修計画もAACを好んでいます。4時間耐火性能は商業施設の改修におけるコンプライアンスを高め、その防カビマトリックスは湿気の多い気候でアピールします。これらの要因が、自動気泡コンクリート市場の持続的成長を支えています。

厳しいグリーンビルディング規制とLEEDの採用

具現化炭素の抑制を目的とした政策は、世界中で材料の選択を変えています。米国政府は持続可能な材料ベンチマークのために1億6,000万米ドルの資金を提供し、AACの導入を明確に奨励しています。EPA(米国環境保護庁)の2024年低炭素ラベルは、メーカーに気候変動に対する優位性を定量化する明確なルートを提供し、公共プロジェクトの入札スコアを向上させています。H+H UKは、EUの脱炭素化目標に沿って、2050年までにネット・ゼロの運営を目標としています。厚さ200mmでR値1.43のAACは、10~20%の運用エネルギー削減を実現し、リサイクル・フライアッシュを組み込んでいるため、サーキュラー・エコノミーの基準を満たしています。

高い初期費用と粘土・コンクリートブロックの比較

建設業者がライフサイクルの節約よりも購入価格を優先する場合、割高な価格設定という認識がAACの普及を妨げています。しかし、インドの主要都市では最近、伝統的な赤レンガの価格がAACより約20%高くなり、購入者はより軽量な代替品に流れるようになりました。2025年の関税引き上げで鉄鋼は10~25%、コンクリートは3~7%上昇し、AACのコスト差は縮小しました。地域によっては限られた工場しかないため、納入価格が15~20%上昇します。30%のエネルギー代削減と労働力の削減を強調する教育キャンペーンは、総所有コストに重点を置いた調達決定を徐々に見直しつつあります。

セグメント分析

ブロックは2024年の売上高の54.78%を占め、数十年にわたる請負業者の慣れと幅広い流通網を反映しています。これと並行して、建築業者がプレハブ外壁に軸足を移していることから、パネルは2030年まで7.81%のCAGRを記録します。パネル・ブームは、建設業界の工業化推進を体現しています。工場でカットされたモジュールが現場ですぐに使える状態で届くため、廃棄物が減り、スケジュールが短縮されます。高層住宅にパネルが好まれるのは、継ぎ目が少ないため、熱外皮が密になり、侵入ロスが少なくなるからです。

特に、労働力が豊富で現場技術が優位を占める市場では、低層住宅の中心は依然としてブロック・セグメントです。しかし、パネルの技術革新はとどまるところを知らないです。補強された壁パネルが耐荷重責務を担うようになり、熱伝導率0.11 W/mKの屋根モジュールがゼロ・エネルギー建築の目標を達成しています。自動化された製材ラインとロボットハンドリングがパネル製造コストを削減し、オートクレーブド・アエロテッド・コンクリート(AAC)市場の、職人的なブロック敷設から工業的なパネル組み立てへのシフトを支えています。

地域分析

アジア太平洋地域は2024年の世界売上高の46.78%を占め、2030年までのCAGRは7.28%で加速しています。中国とインドが需要の中心であり、住宅メガプロジェクトと国家インフラパイプラインが牽引しています。低炭素建築法に対する政府の優遇措置は、AACへの仕様をさらに傾ける。日本と韓国は耐震安全性のためにAACを採用し、オーストラリアは家庭用エネルギー基準で着実な普及を維持しています。アジア太平洋地域の原材料自給率の高さとオートメーション化の進展が単価競争力を維持し、アジア太平洋地域の優位性を確固たるものにしています。

北米では、米国西部における山火事への耐性要件と、気候帯を超えた建築外皮の厳格化によって、AAC使用のルネッサンスが起きています。EPA(米国環境保護庁)の低排出炭素ラベルは公共調達を促進し、カナダのエネルギー基準改正はその勢いを加速させています。メキシコの住宅刺激策はこの地域の状況を補完し、自動気泡コンクリート市場の堅調な軌道をもたらします。

欧州の成熟した状況は、厳格な炭素目標の恩恵を受けている:ドイツと英国は積極的に建物を改修し、北欧市場はゼロエネルギーに近い基準に向かっています。EUのグリーンディール融資は、プラントのアップグレードや新設ラインを支援します。中欧と東欧では、活況を呈するロジスティクスとデータセンター建設が耐火性と熱効率の高いシェルを求めているため、ホワイトスペースが成長しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 新築・改築需要の拡大

- 厳しいグリーンビルディング規制とLEEDの採用

- 低炭素材料に対する政府のインセンティブ

- モジュラー式オフサイト建築の普及

- 耐震軽量ブロックの需要

- 市場抑制要因

- 粘土・コンクリートブロックに比べ初期費用が高め

- 耐荷重用途における構造的限界

- アルミニウム粉末発泡剤の供給と価格の変動性

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- 製品タイプ別

- ブロック

- パネル

- リンテル

- タイル

- その他(Uブロック、フロア/ルーフエレメント)

- 工法別

- 現場石工

- プレハブ/モジュール

- 用途別

- 住宅用

- 商業用

- インダストリアル

- その他の用途(道路、ユーティリティエンクロージャ、防音壁)

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリアおよびニュージーランド

- ASEAN

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- ポーランド

- オランダ

- ルーマニア

- チェコ共和国

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- イスラエル

- カタール

- 南アフリカ

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- ACICO Group

- AERCON AAC

- Asahi Kasei Corporation

- Bauroc AS

- Biltech Building Elements Limited

- BirlaNu Limited

- Eastland Building Materials Co., Ltd

- Eco Green

- Ecostone AAC

- H+H UK Limited

- JK Lakshmi Cement Ltd.

- Renacon

- SOLBET

- Starken AAC Sdn Bhd

- STT Turk Gazbeton

- Thomas Armstrong(Concrete Blocks)Ltd

- UAL Industries Limited

- UltraTech Cement Ltd.

- Xella International