米国のセンサ- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

United States Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 192 Pages

- 納期

- 2~3営業日

- 商品コード

- 1694045

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

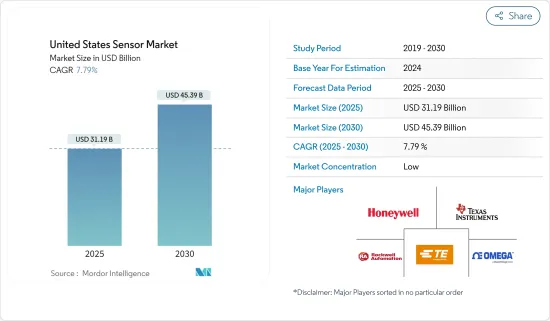

米国のセンサ市場規模は2025年に311億9,000万米ドルと推定され、市場推定・予測期間(2025~2030年)のCAGRは7.79%で、2030年には453億9,000万米ドルに達すると予測されています。

センサは、圧力、熱、光、動き、湿気など、物理的環境からのさまざまな入力を検出し、反応するように設計されています。その結果出力される信号は通常、センサが設置された場所で人間が読める形式で表示されるか、読み取りや追加処理を容易にするためにネットワーク経由で電子的に送信されます。

スマートフォンのナビゲーションシステムから運転支援システムに至るまで、インテリジェントなセンサ技術に対する需要の高まりは様々な産業で顕著です。センサは、技術セグメントで競合を維持する上で重要な役割を果たしています。モノのインターネット(IoT)、ウェアラブルヘルスモニタリングシステム、自動車の自動化といった大きな動向がこの需要を後押ししています。その結果、インテリジェントセンサがより身近なものとなり、さまざまな産業の企業が自動化、生産性、効率性、安全対策を強化できるようになりました。

センシング技術の進化は、プロセスオートメーションの進歩とともに明らかであり、より高性能で相互接続されたセンシングデバイスの開発につながっています。デジタル化へのシフトが加速するにつれ、プロセスの自動化、異常検知の改善、予知保全能力の向上に対する需要が高まり、センシング技術の大幅な普及を促しています。

継続的な技術進歩により、米国の自動車産業では、特に位置検出用途用の電子センサのニーズが高まっています。電動化や自律走行といった技術進歩に産業が注力していることが、センサの需要を高めています。さらに、自動車に位置センサを組み込む動向は、市場成長の有望な将来を示しています。

さらに、米国ではスマートビークルの市場が拡大し、自動車相手先商標製品メーカー(OEM)によるセンサの利用が拡大していることも、自動車セグメントでのセンサ需要を後押ししています。自動車産業におけるセンサ需要の増加は、自動車に特定のセンサの使用を義務付ける規制の施行によってさらに後押しされています。

センサの統合は産業オートメーションを強化する一方で、コスト増を伴うため、コスト重視の用途では制限要因になる可能性があります。さらに、新製品を生み出すための研究開発には高いコストがかかるため、特に資金不足の中小センサメーカーにとっては大きな課題となります。

米国のセンサ市場動向

リトラクタブルセーフティシリンジセグメントが予測期間中に大きな成長を遂げる見込み

- 化学センサは、特定の分析対象物に選択的かつ可逆的に反応し、総合的な組成分析を可能にする電気出力信号を提供する分析装置です。国内では汚染レベルが上昇しており、化学センサの需要が高まっています。多様なサンプル組成を分析する化学センサの用途が増加していることが、その採用を後押ししています。特筆すべきは、先進的直交変種を含む、低コストで携帯可能な化学センサの需要が急増していることであり、市場の成長を促進する重要な動向となっています。

- 産業開発は、発がん性、変異原性、一般的に有害な化学品を含む様々な有毒物質の生産に拍車をかけています。厳格な管理にもかかわらず、これらの物質は人間の健康を脅かし続けています。

- さらに、医療産業では、連続的なリアルタイムの生理学的・化学的データを提供し、涙、唾液、汗、間質液、ヒト揮発性物質などのヒト生体流体中の生化学マーカーを非侵襲的にモニタリングできる化学センサへの関心が高まっている

- 最近の進歩は、特に代謝物、タンパク質、化学品、細菌をモニタリングするための電気化学バイオセンサに集中しています。人体内の生物物理量を測定することは、医療や医療において重要な焦点となっています。スポーツ、医療、医療用途における重要なパラメータをモニターするために、多数の軟質、ウェアラブル、着脱可能なセンサが開発され、商品化されています。

- さらに、糖尿病罹患率の急増に伴い、各国政府は先進的な診断方法への投資を強化しており、医療における化学センサの普及に拍車をかけています。

- 2024年の全米糖尿病統計報告書によると、米国の成人3,840万人が糖尿病であることが明らかになりました。そのうち2,930万人が診断を受けており、970万人が未診断でした。特筆すべきは、アメリカ人口の29.2%、1,650万人が65歳以上の高齢者であったことです。さらに、毎年推定120万人のアメリカ人が糖尿病と診断されています。同国では毎年糖尿病患者が増加していることから、今後数年間は市場の成長に拍車がかかると予想されます。

予測期間中、北米が大きな市場シェアを占める見込み

- 民生用電子機器セグメントには、スマートフォン、ノートパソコン、タブレット、テレビ、ゲーム機、スマートホームデバイス、デジタルカメラなどが含まれます。スマートウェアラブルはこのセグメントに含まれないです。

- 携帯電話、ノートパソコン、ゲーム機、電子レンジ、冷蔵庫などの民生用電子機器製品の多くは、温度、近接、モーションセンサなどで動作します。これらの機器の需要が高いことが、市場成長の重要な要因となっています。

- 民生用電子機器製品のセンサは、スマートフォン、タブレット、ウェアラブル、ゲーム機、民生用電子機器製品など、幅広い民生用電子機器製品の機能性、使いやすさ、全体的な性能を向上させる上で重要な役割を果たしています。これらのセンサは、これらのデバイスが周囲の環境と相互作用することを可能にし、タッチセンシティブインターフェース、モーション検出、画像キャプチャ、環境モニタリングなどの機能を記載しています。

- センシングデバイスは、スマート構造の普及に伴い、より多くのスマートホーム用途で使用されるようになっています。センサの需要は、スマート民生用電子機器の普及、スマートホーム向けIoT機器、技術の進歩や革新により増加すると予想されます。さらに、ワイヤレス技術の利用が拡大し、スマート民生用電子機器市場を後押ししていることから、センサの新たな市場機会が開かれると予想されます。

- 例えば、消費者技術協会(CTA)によると、米国では、スマートホームデバイスの販売による総収入は、2018年の197億米ドルに対し、2023年には235億米ドルに達すると推定されています。スマート技術市場では、省エネ民生用電子機器の需要が高まり、用途付きセンサの需要が増加すると予測されています。

- スマート民生用電子機器の採用は、センサ技術、AI、ビッグデータ分析、IoT対応機器によって促進されます。予測によると、2024年の米国における民生用電子機器製品の小売売上高は5,120億米ドルに達します。2023年には、OLEDテレビが23億米ドルを、携帯ゲーム機が15億米ドルの売上を見込んでいます。

米国のセンサ産業概要

米国のセンサ市場はセグメント化されており、センサ産業における著名メーカーの存在感が増していることから、予測期間中に競争企業間の敵対関係が激化すると予想されます。Texas Instruments Incorporated、TE Connectivity Ltd、Omega Engineering Inc、Honeywell International Inc、Rockwell Automation Incなど、市場の既存企業が市場全体に大きな影響を与えています。

2024年2月-STMicroelectronicsは、市場をリードする2.3kの解像度を誇るオールインワンの直接飛行時間(dToF)3D LiDARモジュールを発表しました。さらに同社は、世界最小の50万画素間接飛行時間(iToF)センサの早期設計成功を発表しました。VL53L9は、新しい直接ToF 三次元LiDARデバイスで、最大2.3kゾーンの解像度を記載しています。市場で他に類を見ないデュアルスキャンフラッド照明を特徴とするこのLiDARは、2D赤外線(IR)画像と3D深度マップ情報を同時に取得しながら、小さな物体やエッジを検出することができます。

2024年1月-amsオスラムは、サンフランシスコで開催されたPhotonics Westにおいて、Mira製品ファミリーの最新製品であるMira016 CMOSイメージセンサの展示を発表しました。Mira016は、コンパクトな1.8 mm x 1.8 mm包装の裏面照射型(BSI)ダブルスタックセンサで、400 x 400ピクセルの解像度を誇ります。フル解像度、90fpsで20mWの消費電力で動作し、近赤外でも高い量子効率を実現し、低消費電力で高性能を発揮します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 産業バリューチェーン/サプライチェーン分析

第5章 市場力学

- 市場の促進要因

- IoTとコネクテッドデバイスに対する需要の高まり

- 自動車産業における先進的センサ技術の採用増加

- 市場抑制要因

- 初期コストの高さ

第6章 市場セグメンテーション

- 製品タイプ別

- 圧力

- レベル

- フロー

- 近接

- 環境

- ケミカル

- 慣性

- 磁気

- ホール効果センサ

- その他の磁気センサ

- 位置センサ

- 電流センサ

- その他

- 動作モード別

- 光学式

- 電気抵抗

- バイオセンサ

- ピエゾ抵抗

- 画像

- 容量性

- 圧電

- ライダー

- レーダー

- その他の動作モード

- エンドユーザー産業別

- 自動車

- 民生用電子機器

- エネルギー

- 産業・その他

- 医療福祉

- 建設・農業・鉱業

- 航空宇宙

- ロボット工学

第7章 競合情勢

- 企業プロファイル

- Texas Instruments Incorporated

- TE Connectivity Ltd

- Omega Engineering Inc.

- Honeywell International Inc.

- Rockwell Automation Inc.

- Siemens AG

- STMicroelectronics Inc.

- AMS Osram AG

- NXP Semiconductors NV

- Infineon Technologies AG

- Bosch Sensortec GmbH

- Sick AG

- ABB Limited

- Omron Corporation

- Allegro MicroSystems Inc

第8章 市場展望

目次

The United States Sensor Market size is estimated at USD 31.19 billion in 2025, and is expected to reach USD 45.39 billion by 2030, at a CAGR of 7.79% during the forecast period (2025-2030).

A sensor is designed to detect and react to various inputs from the physical environment, such as pressure, heat, light, motion, and moisture. The resulting output typically consists of a signal that can be displayed in a human-readable format at the sensor's location or transmitted electronically over a network for easy reading or additional processing.

The increasing demand for intelligent sensor technology is evident in various industries, from smartphone navigation systems to driver-assistance systems. Sensors are playing a vital role in staying competitive in the technology sector. Major trends like the Internet of Things (IoT), wearable health monitoring systems, and vehicle automation drive this demand. Consequently, intelligent sensors are now more accessible, enabling businesses in various industries to enhance automation, productivity, efficiency, and safety measures.

The evolution of sensing technology is apparent with advancements in process automation, leading to the development of more capable and interconnected sensing devices. As the shift toward digitalization speeds up, there is a growing demand for increased process automation, improved anomaly detection, and predictive maintenance capabilities, prompting a significant uptake of sensing technology.

Due to ongoing technological advancements, the automotive industry in the United States is experiencing a growing need for electronic sensors, especially for position-sensing applications. The industry's focus on technical progress, such as electrification and autonomous driving, has increased the demand for sensors. Additionally, the trend of incorporating position sensors into vehicles demonstrates a promising future for the market's growth.

Additionally, the increasing market for smart vehicles and the growing use of sensors by automotive original equipment manufacturers (OEMs) in the United States also drive the demand for sensors in the automotive sector. The rise in demand for sensors in the automotive industry is further bolstered by the enforcement of regulations requiring the use of specific sensors in vehicles.

While integrating sensors enhances industrial automation, it comes with an added cost that may be a limiting factor in cost-sensitive applications. Furthermore, the high costs associated with research and development for creating new products pose a significant challenge, especially for smaller sensor manufacturers that may lack funds.

United States Sensor Market Trends

Retractable Safety Syringes Segment Expected to Witness Significant Growth During the Forecast Period

- Chemical sensors are analyzers that respond selectively and reversibly to specific analytes, providing an electrical output signal that enables a comprehensive composition analysis. The country's escalating pollution levels have bolstered the demand for these sensors. Rising applications for chemical sensors in analyzing diverse sample compositions drive their adoption. Notably, the market is witnessing a surge in demand for low-cost, portable chemical sensors, including advanced orthogonal variants, underscoring a significant trend poised to propel the market's growth.

- Industrial development has spurred the production of various toxic materials, encompassing carcinogenic, mutagenic, and generally hazardous chemicals. Despite stringent management, these substances continue to endanger human health.

- Furthermore, the healthcare industry is increasingly interested in chemical sensors due to their capability to deliver continuous, real-time physiological and chemical data and non-invasive monitoring of biochemical markers in human biofluids such as tears, saliva, sweat, interstitial fluid, and human volatiles.

- Recent advancements have concentrated on electrochemical biosensors, particularly for monitoring metabolites, proteins, chemicals, and bacteria. Measuring biophysical quantities in the human body has been a significant focus in healthcare and medicine. Numerous flexible, wearable, and detachable sensors have been developed and commercialized to monitor critical parameters in sports, healthcare, and medical applications.

- Furthermore, as diabetes rates surge, the country's governments are ramping up investments in advanced diagnostic methods, fueling the uptake of chemical sensors in healthcare.

- The National Diabetes Statistics Report of 2024 revealed that 38.4 million adults in the United States had diabetes. Among them, 29.3 million had been diagnosed, while a concerning 9.7 million were undiagnosed. Notably, 29.2% of the American population, equating to 16.5 million seniors, were aged 65 and above. Furthermore, an estimated 1.2 million Americans are diagnosed with diabetes each year. The increasing number of diabetes patients in the country every year is expected to fuel the market's growth in the coming years.

North America Expected to Hold Significant Market Share During the Forecast Period

- The consumer electronics segment includes smartphones, laptops, tablets, televisions, gaming consoles, smart home devices, digital cameras, and others. Smart wearables are not considered in this segment.

- Most consumer electronics, such as mobile phones, laptops, game consoles, microwaves, and refrigerators, operate with temperature, proximity, motion sensors, etc. The high demand for these devices is a crucial factor contributing to the market's growth.

- Sensors in consumer electronics play a crucial role in improving the functionality, user-friendliness, and overall performance of a wide range of consumer electronic products, including smartphones, tablets, wearables, gaming consoles, home appliances, and others. These sensors enable these devices to interact with their surroundings and offer touch-sensitive interfaces, motion detection, image capture, environmental monitoring, and more capabilities.

- Sensing devices are used in more smart home applications as smart structures gain popularity. The demand for sensors is expected to increase due to the growing popularity of smart consumer electronics, IoT devices for smart homes, and technological advancements and innovations. Additionally, the growing use of wireless technologies, propelling the market for smart consumer electronics, is anticipated to open up new market opportunities for sensors.

- For instance, according to the Consumer Technology Association (CTA), in the United States, total revenue from the sales of smart home devices was estimated to reach USD 23.5 billion in 2023, compared to USD 19.7 billion in 2018. It is anticipated that the market for smart technology will witness rising demand for energy-saving appliances and increasing demand for sensors with applications.

- The adoption of smart home appliances will be fueled by sensor technology, AI, big data analytics, and IoT-enabled devices. Projections indicate that 2024 retail sales in the United States for consumer electronics will hit a significant USD 512 billion. In 2023, OLED TVs were on track to rake in USD 2.3 billion, while portable gaming consoles were eyeing a revenue of USD 1.5 billion.

United States Sensor Industry Overview

The United States Sensor market is fragmented, and the increasing presence of prominent manufacturers in the sensor industry is expected to intensify competitive rivalry during the forecast period. Market incumbents, such as Texas Instruments Incorporated, TE Connectivity Ltd, Omega Engineering Inc., Honeywell International Inc., Rockwell Automation Inc., etc., considerably influence the overall market.

February 2024 - STMicroelectronics introduced an all-in-one, direct Time-of-Flight (dToF) 3D LiDAR module boasting a market-leading 2.3k resolution. Additionally, the company has disclosed an early design win for the world's smallest 500k-pixel indirect Time-of-Flight (iToF) sensor. The VL53L9, a novel direct ToF 3D LiDAR device, offers a resolution of up to 2.3k zones. Featuring a dual scan flood illumination, which is unparalleled in the market, this LiDAR can detect small objects and edges while simultaneously capturing 2D infrared (IR) images and 3D depth map information.

January 2024 - ams OSRAM announced the showcase of the latest member of the Mira product family, the Mira016 CMOS image sensor, at Photonics West in San Francisco. The Mira016 boasts a resolution of 400 x 400 pixels for a backside illuminated (BSI) double-stack sensor that comes in a compact 1.8 mm x 1.8 mm package. It operates at a power of 20 mW at full resolution and 90 fps and also offers high quantum efficiency in the near-infrared, providing high performance with low power consumption.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain/Supply Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for IoT and Connected Devices

- 5.1.2 Increasing Adoption of Advanced Sensor Technologies in Automotive Industry

- 5.2 Market Restraints

- 5.2.1 High Initial Cost Involved

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Pressure

- 6.1.2 Level

- 6.1.3 Flow

- 6.1.4 Proximity

- 6.1.5 Environmental

- 6.1.6 Chemical

- 6.1.7 Inertial

- 6.1.8 Magnetic

- 6.1.8.1 Hall Effect Sensors

- 6.1.8.2 Other Magnetic Sensors

- 6.1.9 Position Sensors

- 6.1.10 Current Sensors

- 6.1.11 Other Types

- 6.2 By Mode of Operation

- 6.2.1 Optical

- 6.2.2 Electrical Resistance

- 6.2.3 Biosensor

- 6.2.4 Piezoresistive

- 6.2.5 Image

- 6.2.6 Capacitive

- 6.2.7 Piezoelectric

- 6.2.8 Lidar

- 6.2.9 Radar

- 6.2.10 Other Modes of Operation

- 6.3 By End-user Industry

- 6.3.1 Automotive

- 6.3.2 Consumer Electronics

- 6.3.3 Energy

- 6.3.4 Industrial and Other

- 6.3.5 Medical and Wellness

- 6.3.6 Construction, Agriculture and Mining

- 6.3.7 Aerospace

- 6.3.8 Robotics

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Texas Instruments Incorporated

- 7.1.2 TE Connectivity Ltd

- 7.1.3 Omega Engineering Inc.

- 7.1.4 Honeywell International Inc.

- 7.1.5 Rockwell Automation Inc.

- 7.1.6 Siemens AG

- 7.1.7 STMicroelectronics Inc.

- 7.1.8 AMS Osram AG

- 7.1.9 NXP Semiconductors NV

- 7.1.10 Infineon Technologies AG

- 7.1.11 Bosch Sensortec GmbH

- 7.1.12 Sick AG

- 7.1.13 ABB Limited

- 7.1.14 Omron Corporation

- 7.1.15 Allegro MicroSystems Inc

8 MARKET OUTLOOK

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 192 Pages

- 納期

- 2~3営業日