|

市場調査レポート

商品コード

1694017

乗員用酸素システム- 市場シェア分析、産業動向・統計、成長予測(2025~2030年)Crew Oxygen Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 乗員用酸素システム- 市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 121 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

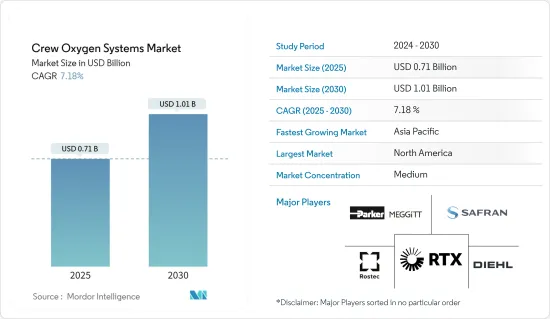

乗員用酸素システム市場規模は2025年に7億1,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは7.18%で、2030年には10億1,000万米ドルに達すると予測されます。

主要ハイライト

- 世界中の民間航空宇宙産業の急成長は、乗務員酸素システム市場に影響を与える主要因です。大手航空会社による航空機フリート拡大イニシアティブ、民間航空需要の高まり、軍用機近代化プロジェクトは、総じて乗員用酸素システムの需要拡大に寄与しています。航空旅客輸送量の増加は、市場の需要を満たすために世界中でより多くの航空機発注につながっています。その結果、客室乗務員の体力が向上し、最終的に乗務員用酸素システムの需要が大幅に増加することになります。

- さらに、世界中の国防軍が航空技術の進歩を優先しているため、軍用エンドユーザーが需要に影響を与えています。洗練された酸素システムの必要性は、長時間の飛行や高高度での運用を伴う軍事戦略の進化によってもたらされます。

- 米連邦航空局(FAA)や欧州連合航空安全機関(EASA)が定めるような国際的な航空安全基準は、乗員用酸素システムの需要に大きく影響しています。これらの安全基準やコンプライアンスは、安全認証要件を含み、進化する厳しい規制状況に貢献しており、重要な航空機部品の設計、開発、承認プロセスを直接形作っています。その一方で、酸素システムの開発に関連する高コストが市場成長の妨げとなっています。

乗員用酸素システム市場動向

予測期間中は酸素貯蔵システムが市場を独占

- 酸素貯蔵システムは、純粋な酸素の供給を貯蔵または生成し、その酸素を調整し、必要に応じて希釈し、乗員または乗客に分配するように設計されています。航空機タイプや役割に応じて、酸素システムは通常の運航に使用されることもあれば、特定の状況下で補助酸素を供給するために使用されることもあり、また煙、火災、煙、加圧喪失時に緊急用酸素を供給するために使用されることもあります。

- 補助酸素または緊急用酸素システムの提供と使用に関する規制は、国際民間航空機関(ICAO)の標準と推奨プラクティス(SARPS)が提供するガイダンスに基づいています。この規則では、加圧航空機と非加圧航空機を区別し、さらに飛行を行う高度に応じた具体的な要件を定めています。例えば、2022年6月、ディール・アビエーションは旅客機搭載用の非常用酸素供給装置を独自に製造しました。

- さらに、2023年には、BoeingとAirbusの合計で、2022年の480機と663機に対し、528機と735機が納入されました。A320の公式生産速度は月産45機で、2021年末からこの水準を維持しています。平均すると、2022年の43機に対し、2023年は月48機のA320を納入しました。従って、航空機納入の増加は、予測期間中の市場の推進力を生み出すと考えられます。

予測期間中、北米が市場で最も高いシェアを占める

- 北米が乗員用酸素システム市場で最も高いシェアを占めているのは、米国の高い航空需要、大規模な航空機保有台数、国防費への多額の投資によるものです。米国運輸省(DoT)は、2022年の航空旅客数が約8億5,400万人を超えると発表しました。Boeingは米国有数の航空機サプライヤーであり、乗務員関連の酸素システムに大きな需要を生み出しています。米国の航空産業はパイロット不足という課題に直面しています。しかし、これは航空セグメントにおける成長と開発の機会をもたらしています。米国では旅行需要が高いため、より多くのパイロットが必要とされています。航空機の新規発注が行われるたびに、それに対応する酸素システムの需要も発生します。

- 米国では2017~2022年にかけて合計1,500機以上の新型旅客機が納入され、2023~2029年にかけてはさらに2,000機以上の新型ジェット機が納入される見込みです。Carleton Technologies Inc.、Collins Aerospace、Safran Aerosystemsは、米国におけるBoeingB737とB787航空機向け酸素システムの主要サプライヤーです。米国は2022年の北米における航空旅客輸送量の80%を占めています。そのため、予測期間中、米国は他の北米諸国に比べ、新規航空機納入の需要が最も高くなると予想されます。航空会社は増大する航空需要に対応するために航空機の規模を拡大しようとしており、乗員用酸素システムの大きな需要を生み出す可能性があります。

- さらに、一般航空セグメントでは、相手先商標製品メーカー(OEM)が技術革新を重視し、新製品を発売しています。例えば、2023年には米国のAeroxがターボプロップや小型ジェット機関連の航空機用酸素システムを提供しました。これらのソリューションは、携帯用酸素システム、緊急降下装置、各種酸素システム付属品で構成されています。このことも、同国の一般航空セクタにおける酸素システムの成長を助けると期待されています。

乗員用酸素システム産業概要

乗員用酸素システム市場は、市場において重要なシェアを持つ少数のローカルと世界参入企業が存在するため、その性質上、半固体化しています。以下のような主要な航空宇宙参入企業The Boeing Company, Bombardier Inc., and Airbus SE shape market dynamics through their aircraft production and technology integration initiatives.

乗員用酸素システム市場の主要市場参入企業には、RTX Corporation、Safran、Parker-Meggitt(Parker Hannifin Corporation)、Rostec、Diehl Stiftung & Co.KGなどです。さらに、主要OEMは、軽量で先進的酸素システムを開発するために研究開発に高度に投資しています。このような成長動向は、拡大する世界の航空機をサポートする信頼性の高い先進的な酸素システムに対する莫大な需要を浮き彫りにしています。例えば、2023年6月、サフランはAir Liquideと独占交渉に入り、Air Liquideのアドバンスド技術の航空用酸素・窒素事業を買収すると発表しました。この買収プロジェクトは、サフラン・エアロシステムズの製品群、特に機内酸素発生システム(OBOGS)を補完するもので、サフランはシステムインテグレーションを通じてリーディング参入企業になることができます。乗員用酸素システム市場は半固定的な構造を示しており、市場シェアを大幅に握る一部のローカル・参入企業と世界の参入企業が支配的な存在感を示しているのが特徴です。Boeing社、ボンバルディア社、AirbusSEを含む主要な航空宇宙産業のリーダーは、航空機の生産と技術統合イニシアチブへの影響力ある貢献を通じて、市場力学の形成に極めて重要な役割を果たしています。

乗員用酸素システム市場の参入企業は、RTX Corporation、Safran、Parker-Meggitt(Parker Hannifin Corporation)、Rostec、Dehl Stiftung & Co.KGです。これらの主要市場参入企業は、革新と研究開発へのコミットメントを示し、軽量で高度に先進的な酸素システムの創造に多大な投資を行っています。このような技術進歩への継続的な重点の置き方は、拡大する世界の航空機のニーズに対応する信頼性の高い最先端の酸素システムへの大きな需要を裏付けています。

この成長動向は、主要な相手先商標製品製造業者(OEM)が最先端の酸素システムの製造を目指した研究開発に積極的に取り組んでいることを示しています。サフランが2023年6月に発表した、Air Liquide Advanced Technologiesの航空用酸素・窒素事業の買収に関するAir Liquide社との独占交渉はその一例です。この戦略的買収プロジェクトは、サフラン・エアロシステムズの目標、特に機内酸素発生システム(OBOGS)セグメントの製品ラインナップの強化に合致しています。この取り組みを通じて、サフランはシステムインテグレーションの強みを生かし、市場におけるリーディング参入企業としての地位を確立することを目指しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場の促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 用途

- 民間航空

- 軍用機

- 一般航空

- コンポーネント

- 酸素マスク

- 酸素貯蔵システム

- 酸素供給システム

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Cobham Limited

- Safran

- RTX Corporation

- Parker-Meggitt(Parker Hannifin Corporation)

- Rostec

- Aeromedix, LLC

- Aviation Oxygen Etc.

- Aerox Aviation Oxygen Systems, LLC

- Precise Flight, Inc.

- PFW Aerospace GmbH

- Caeli Nova

- Diehl Stiftung & Co. KG

第7章 市場機会と今後の動向

The Crew Oxygen Systems Market size is estimated at USD 0.71 billion in 2025, and is expected to reach USD 1.01 billion by 2030, at a CAGR of 7.18% during the forecast period (2025-2030).

Key Highlights

- The rapid growth of the commercial aerospace industry across the globe is a key factor influencing the crew oxygen systems market. Aircraft fleet expansion initiatives by major airlines, the rising demand for commercial aviation, and military aircraft modernization projects collectively contribute to increased demand for crew oxygen systems. The increase in air passenger traffic is leading to more aircraft orders around the world to meet market demand. This, in turn, leads to increased cabin crew strength, thus ultimately leading to a significant rise in demand for crew oxygen systems.

- Moreover, the military end users influence the demand as defense forces worldwide prioritize advancements in aviation technology. The need for sophisticated oxygen systems is driven by evolving military strategies that involve extended flight durations and operations at high altitudes.

- International aviation safety standards, such as those set by the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA), significantly influence the demand for crew oxygen systems. These safety standards and compliances, which include safety certification requirements and contribute to an evolving stringent regulatory landscape, directly shape the design, development, and approval processes of critical aircraft components. On the other hand, the high cost associated with the development of oxygen systems hinders the market growth.

Crew Oxygen Systems Market Trends

Oxygen Storage Systems Dominates the Market During the Forecast Period

- Oxygen storage systems are designed to store or generate a supply of pure oxygen and to regulate, dilute as required, and then distribute that oxygen to crew or passengers. Depending upon the type and the role of the aircraft concerned, an oxygen system may be used for normal operations, to provide supplemental oxygen for specific situations, or to provide emergency oxygen in the event of smoke, fire, fumes, or loss of pressurization.

- Regulations for the provision and use of supplemental or emergency oxygen systems are based on the guidance provided by the International Civil Aviation Organization (ICAO) Standards and Recommended Practices (SARPS). The regulations differentiate between pressurized and non-pressurized aircraft and then provide specific requirements based on the altitude at which the flight is to be conducted. For instance, in June 2022, Diehl Aviation built its own emergency oxygen supply generator for onboard passenger aircraft.

- Furthermore, in 2023, in total, Boeing and Airbus delivered 528 and 735 aircraft compared to 480 and 663, respectively, in 2022. The official A320 production rate is 45 aircraft per month and has remained at this level since the end of 2021. On average, the company delivered 48 A320s per month in 2023 compared to 43 in 2022. Thus, an increase in aircraft deliveries will create the market to propel during the forecast period.

North America Holds Highest Shares in the Market During the Forecast Period

- North America holds the highest shares in the crew oxygen systems market, owing to the high demand for air travel in the US, large fleet size, and significant investments in defense spending. The US Department of Transportation (DoT) announced that the air passenger traffic number in 2022 crossed around 854 million. Boeing is among the leading aircraft suppliers in the United States and is responsible for creating significant demand for crew-related oxygen systems. The US airline industry is facing a challenge with the pilot shortage. However, this presents an opportunity for growth and development in the aviation sector. The high demand for travel in the US has created a need for more pilots. Whenever new orders for aircraft are placed, the corresponding demand for oxygen systems is also generated.

- A total of 1500+ new passenger aircraft were delivered in the United States between 2017 and 2022, and a further 2000+ new jets are expected to be delivered to the region during 2023-2029. Carleton Technologies Inc., Collins Aerospace, and Safran Aerosystems were major suppliers of oxygen systems in the United States for Boeing B737 and B787 aircraft. The United States accounted for 80% of the total air passenger traffic in North America in 2022. Therefore, the United States is expected to generate the highest demand for new aircraft deliveries compared to other North American countries over the forecast period. Airlines are looking to expand their fleet size to cater to the growing demand for air travel, which may generate significant demand for crew oxygen systems.

- Furthermore, in the general aviation sector, original equipment manufacturers (OEMs) have emphasized on innovation and launched new products. For instance, in 2023, Aerox, a US-based company, offered aircraft oxygen systems related to turboprop and light jets. These solutions consist of portable oxygen systems, emergency descent gear, and various oxygen system accessories. This is also expected to aid the growth of oxygen systems in the country's general aviation sector.

Crew Oxygen Systems Industry Overview

The crew oxygen systems market is semi-consolidated in nature due to the presence of a few local and global players holding significant shares in the market. The key aerospace players such as The Boeing Company, Bombardier Inc., and Airbus SE shape market dynamics through their aircraft production and technology integration initiatives.

The key market players in the crew oxygen systems market include RTX Corporation, Safran, Parker-Meggitt (Parker Hannifin Corporation), Rostec, and Diehl Stiftung & Co. KG. Furthermore, key OEMs highly invest in research and development to develop lightweight and highly advanced oxygen systems. This growth trend highlights the huge demand for reliable and advanced oxygen systems to support the expanding global fleet. For instance, in June 2023, Safran announced that it had entered into exclusive negotiations with Air Liquide to acquire the aeronautical oxygen and nitrogen activities of Air Liquide's advanced Technologies. This acquisition project would complement Safran Aerosystems' product range especially on-board oxygen generation systems (OBOGS) will enable Safran to become a leading player through systems integration.The crew oxygen systems market exhibits a semi-consolidated structure, characterized by the dominant presence of a select number of local and global players holding substantial market shares. Key aerospace industry leaders, including The Boeing Company, Bombardier Inc., and Airbus SE, play pivotal roles in shaping market dynamics through their influential contributions to aircraft production and technology integration initiatives.

Prominent participants in the crew oxygen systems market comprise RTX Corporation, Safran, Parker-Meggitt (Parker Hannifin Corporation), Rostec, and Diehl Stiftung & Co. KG. These key market players demonstrate a commitment to innovation and research and development, investing significantly in the creation of lightweight and highly advanced oxygen systems. This ongoing emphasis on technological advancement underscores the substantial demand for dependable and cutting-edge oxygen systems to cater to the needs of the expanding global fleet.

This growth trend shows that key original equipment manufacturers (OEMs) are actively engaged in research and development endeavors aimed at producing state-of-the-art oxygen systems. An exemplary instance is the announcement made by Safran in June 2023, revealing exclusive negotiations with Air Liquide to acquire the aeronautical oxygen and nitrogen activities of Air Liquide Advanced Technologies. This strategic acquisition project aligns with Safran Aerosystems' objectives, particularly in enhancing its product range, specifically in the domain of onboard oxygen generation systems (OBOGS). Through this initiative, Safran aims to establish itself as a leading player in the market, leveraging its prowess in systems integration.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porters' Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Commercial Aviation

- 5.1.2 Military Aviation

- 5.1.3 General Aviation

- 5.2 Component

- 5.2.1 Oxygen Mask

- 5.2.2 Oxygen storage system

- 5.2.3 Oxygen Delivery system

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Cobham Limited

- 6.2.2 Safran

- 6.2.3 RTX Corporation

- 6.2.4 Parker-Meggitt (Parker Hannifin Corporation)

- 6.2.5 Rostec

- 6.2.6 Aeromedix, LLC

- 6.2.7 Aviation Oxygen Etc.

- 6.2.8 Aerox Aviation Oxygen Systems, LLC

- 6.2.9 Precise Flight, Inc.

- 6.2.10 PFW Aerospace GmbH

- 6.2.11 Caeli Nova

- 6.2.12 Diehl Stiftung & Co. KG