|

市場調査レポート

商品コード

1911802

フィリピンペットフード市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Philippines Pet Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| フィリピンペットフード市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 80 Pages

納期: 2~3営業日

|

概要

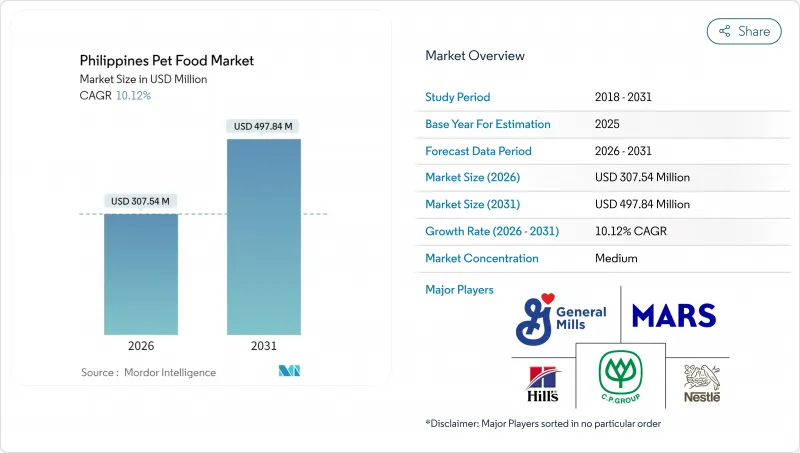

フィリピンのペットフード市場は、2025年に2億7,927万米ドルと評価され、2026年の3億754万米ドルから2031年までに4億9,784万米ドルに達すると予測されています。

予測期間(2026年~2031年)におけるCAGRは10.12%と見込まれています。

ペットの人間化が進み、電子商取引が急速に普及し、家畜飼料メーカーがペット栄養分野へ事業転換していることが、この成長を支えています。都市部の世帯では機能性ダイエットによるプレミアム需要が高まる一方、地方の飼い主は地元製造による価格競争力向上に伴い、食卓の残り物から経済的なドライフードへ移行しています。多国籍ブランドは全国的な小売業の近代化を活用していますが、ペソ相場の変動、動物産業局の長い認可手続き、偽造製品といった課題が短期的な成長を抑制しています。国内飼料メーカーが価格に敏感なセグメントを獲得し、世界の大手がフィリピンペットフード市場でのシェア維持に向け投資を深化させる中、競合環境は流動的な状態が続いています。

フィリピンペットフード市場の動向と洞察

ペットの人間化傾向とプレミアム栄養食品への支出増加

フィリピンのペットオーナーは動物を家族の一員として扱う傾向が強まっており、マース社の「世界のペット親調査」によれば、犬種ではシーズー(29%が希望)、猫種ではペルシャ(43%が希望)が選択を支配しており、実用目的よりも伴侶動物を好む傾向が反映されています。この人間化動向は、プロバイオティクス、オメガ3脂肪酸、専門的な獣医用食事など、機能性成分の需要を牽引しています。特に犬の飼い主の61%が、ペットを飼う主な利点としてストレス解消を挙げています。この変化はプレミアムポジショニングの機会を生み出していますが、価格感応度は依然として高く、犬の年間フード費用は平均340.59米ドルで、ベトナムに次いでアジアで2番目に低くなっています。

近代的な小売業態と電子商取引の拡大

近代的な小売形態の拡大はペットフードの入手可能性を根本的に変え、ロビンソンズ・リテール・ホールディングスは2025年にペット小売店の出店を加速させると同時に、商品品揃えの強化やグルーミングサービスの導入によりカテゴリー成長を推進しています。ランダーズ・スーパーストアなどの倉庫型会員制店舗は、2024年までに12店舗から17店舗へ拡大し、2027年まで年間7店舗の新規出店を長期計画として掲げています。この拡大により、大容量パック購入が可能となり、価格に敏感な消費者の単価コスト削減につながります。チャネルの多様化は、差別化されたポジショニングを求めるプレミアムブランドと、広範な市場アクセスを必要とするエコノミーブランドの両方に利益をもたらしますが、複数の接触点における規制順守はますます複雑化しています。

高い価格感応度と食卓の残り物による給餌

ペットの人間化が進む中でも、持続的な価格感応度の高さが市場のプレミアム化を制約しており、50%以上の動物が依然として食卓の残り物や廃棄物を与えられています。これにより、商業用ペットフードの普及が制限されています。消費者セグメンテーションでは、ペットを労働動物として扱う実用主義者、基本的なケアを提供する現実的な甘やかし派、感情的な絆を求める伴侶派、保険や医療を含む完全な家族待遇を提供する人間化派という4つの明確なタイプが明らかになりました。実用主義者と現実的なセグメントが優勢であるため、プレミアム価格への支払い意欲は限定的ですが、可処分所得の増加と中上位所得層への接近により、都市部市場では徐々にプレミアム化の機会が生まれています。

セグメント分析

食品製品は2025年に53.70%の市場シェアを占め、市場を独占しています。プレミアム化動向と衝動買い行動により、主食よりも価格に敏感でないおやつが牽引役となり、2031年までの年間平均成長率(CAGR)12.21%で最も急速に成長するセグメントとして浮上しています。ドライフードは保存性とコスト効率の高さから最大のサブセグメントシェアを維持し、一方ウェットフードは熱帯気候における猫の水分補給効果をフィリピン消費者が認識していることから、カテゴリー内で重要なシェアを占めています。

このセグメントの重要性は、ペットの健康維持における専門的でバランスの取れた栄養食の必須性に主に起因しており、ドライフードは利便性、長期保存性、コスト効率の高さから主要な消費形態となっています。このセグメントの強固な地位は、ペットオーナーの栄養意識の高まり、プレミアム動向の増加、ペットを家族の一員として扱う傾向によってさらに強化されています。多様なブランド・製品の入手可能性と給餌の利便性が相まって、フィリピンではペットフードが飼い主の優先選択肢となっています。

フィリピンペットフード市場レポートは、ペットフード製品(フード、ペット用栄養補助食品/サプリメント、ペット用おやつなど)、ペットの種類(猫、犬など)、流通チャネル(コンビニエンスストア、オンラインチャネル、専門店、スーパーマーケット/ハイパーマーケットなど)別に分類されています。市場予測は、金額(米ドル)および数量(メトリックトン)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

- 調査手法

第2章 レポート提供

第3章 エグゼクティブサマリー主要な調査結果

第4章 主要業界動向

- ペットの飼育数

- 猫

- 犬

- その他のペット

- ペット関連支出

- 消費者の動向

第5章 供給と生産の動向

- 貿易分析

- 原料動向

- バリューチェーン及び流通チャネル分析

- 規制の枠組み

- 市場促進要因

- ペットの人間化傾向の高まりとプレミアム栄養食品への支出増加

- 近代的な小売業と電子商取引の拡大

- 犬と猫の飼育頭数の増加

- 飼料メーカーによる遊休設備のペットフードラインへの転換

- 獣医療の遠隔診療とペット保険の急増

- 免税店や倉庫型会員制店舗での大容量パッケージ商品の入手可能性

- 市場抑制要因

- 価格に対する高い敏感さと残飯の与餌

- 輸入依存と為替・物流の変動性

- 動物産業局における製品登録手続きの長期化

- 偽造品や並行輸入品による信頼の低下

第6章 市場規模と成長予測(価値と数量)

- ペットフード製品

- フード

- 製品別

- ドライペットフード

- ペット用ドライフード別

- キブル

- その他のドライペットフード

- ペット用ドライフード別

- ウェットペットフード

- ドライペットフード

- 製品別

- ペット用栄養補助食品/サプリメント

- 製品別

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質およびペプチド

- ビタミン・ミネラル

- その他の栄養補助食品

- 製品別

- ペット用おやつ

- 製品別

- カリカリおやつ

- デンタルおやつ

- フリーズドライ・ジャーキーおやつ

- ソフト&チューイおやつ

- その他のおやつ

- 製品別

- ペット用医療用フード

- 製品別

- 糖尿病

- 消化器系サポート

- 口腔ケア用フード

- 腎臓用

- 尿路疾患

- 肥満用ダイエットフード

- 皮膚用ダイエットフード

- その他の獣医用ダイエットフード

- 製品別

- フード

- ペット

- 猫

- 犬

- その他のペット

- 流通チャネル

- コンビニエンスストア

- オンラインチャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他の販売チャネル

第7章 競合情勢

- 主要な戦略的動きs

- 市場シェア分析

- Brand Positioning Matrix

- Market Claim Analysis

- 企業概況

- 企業プロファイル.

- Mars, Incorporated

- Nestle(Purina)

- Colgate-Palmolive Company(Hill's Pet Nutrition, Inc.)

- General Mills Inc.

- Schell & Kampeter, Inc.(Diamond Pet Foods)

- ADM

- Virbac

- Charoen Pokphand Group.

- EBOS Group Limited

- DoggyMan H.A.Co.,Ltd.

- San Miguel Foods Inc.

- Pet Plus Global Marketing Corp.

- Consumer Care Products Inc.

- Pet Discount Inc.

- Universal Robina Corp.(TopBreed)