北米のスタンドアップパウチ包装:市場シェア分析、産業動向、成長予測(2025~2030年)

North America Stand-Up Pouch Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693971

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

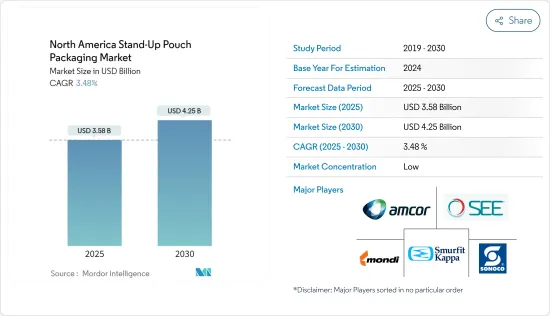

北米のスタンドアップパウチ包装市場規模は、2025年に35億8,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは3.48%で、2030年には42億5,000万米ドルに達すると予測されます。

市場規模では、2025年の269億9,000万個から2030年には314億9,000万個になると予測され、予測期間(2025~2030年)のCAGRは3.13%です。

標準、無菌、レトルトなどのスタンドアップパウチ包装製品が市場調査の対象です。スタンドアップパウチ包装は、出荷や輸送中に理想的な保護バリアを提供し、湿気や汚れなどの外部要素が品目に接触するのを防ぎます。

主要ハイライト

- 地域全体の冷凍包装産業の成長は、市場にプラスの影響を与えると予想されます。包装食品と飲食品の需要増加、RTE(Ready-to-Eat)食品の需要増加、使用の利便性、パウチの費用対効果が市場成長を支える主要因です。

- さらに、外出先でのスナックに対するニーズの高まりが、顧客に利便性を提供する再閉鎖可能なスタンドアップパウチの需要につながっています。さらに、消費者のライフスタイルや食の嗜好の変化、食品技術の変化が市場の需要をさらに押し上げています。

- 環境問題に対する消費者の関心の高まり、ダイナミックな規制基準、プラスチックベースの包装製品を生分解性材料に置き換えることからなる持続可能性への継続的な推進、最先端のリサイクル施設の不足による不十分なリサイクル率が、市場の成長に課題を与えています。

- 急速に変化する市場要件に対応するため、包装機械の技術革新が進んでいるが、従来の機械を使用している包装メーカーは、現在の市場要件の増大する作業負荷に対応するための十分な設備が整っていないため、これが課題となります。参入企業は、変化する市場ニーズに対応するために新しいツール、スペアパーツ、ソフトウェアに投資するか、新しい機械に切り替える必要があります。

- COVID-19後のパンデミックは、飲食品や製薬産業からの需要の増加に助けられ、包装需要の急増をもたらしました。

北米のスタンドアップパウチ包装市場動向

スタンダードパウチタイプセグメントが大きな市場シェアを占める見込み

- ベビーフードや液体包装(茶、コーヒー、ジュース)を含むスタンダードパウチは、飲食品産業で広く使用されています。自然の特性や香りを余すところなく保存できる包装された生鮮食品に対する消費者の期待が、スタンダードパウチの利用を後押ししています。

- スタンダードスタンドアップパウチは、エンドユーザー産業の需要が急増しており、メーカーに革新的なソリューションへの努力を促しています。この情勢はダイナミックな戦略によって特徴付けられ、各社は競合を維持するために協業、拡大、買収、製品発売などのアプローチを採用しています。

- 米国農務省海外農業局によると、米国の2022/2023会計年度のコーヒー消費量は60キログラム袋で2,630万袋を超えました。これは、2020/2021会計年度の米国におけるコーヒー消費量(60キログラム入り2,594万袋)からわずかに増加したものです。

- コーヒー消費量の増加に伴い、コーヒーを封入し流通させるための包装ソリューションに対する需要も高まると考えられます。スタンダードスタンドアップパウチは、利便性、保護、視認性を提供する、人気のある汎用性の高い包装オプションです。コーヒーの消費量が増加するにつれて、これらのパウチの需要も増加する可能性があります。

- コーヒー市場は競争が激しく、各ブランドは差別化を図るために包装を利用することが多いです。スタンドアップパウチは、ブランディング、ラベリング、マーケティングメッセージのための十分なスペースを記載しています。コーヒーの消費量が増加するにつれ、企業は商品が棚で目立つような包装に投資するようになり、スタンドアップパウチの需要が高まる可能性があります。

大幅な成長が期待されるカナダ

- カナダにおけるスタンドアップパウチの需要増加の主要原動力は、包装食品や加工食品への依存度が高いことです。トロント大学の報告によると、カナダの食料供給の約75%は加工食品によるものです。消費パターンの変化は、便利でサステイナブル包装ソリューションの必要性を強調し、カナダ市場でスタンドアップパウチが好まれる選択肢となっています。

- 食品産業は急速に拡大・変化しており、包装の選択肢を広げ、より生産性の高い方法を模索しています。さらに、Logos Pack、Omniplast、Canada Brown、Rootree、Grauman Packagingなど、より環境に優しくサステイナブル包装ソリューションが利用可能になるにつれて、包装の決定を再考する企業が増えています。

- カナダのペットフード産業は活況を呈しており、カナダ農業・農業食品省(AAFC)のデータによると、カナダにおけるペットフードの小売売上高はCAGRでさらに4.9%増加し、2025年までに53億カナダドル(2億2,000万米ドル)に達すると予想されています。ペットフード産業では、ドライフードやウェットフードの包装にスタンドアップパウチがよく使われています。ティアノッチとイージーオープン機能を備えたパウチは、ペットに食事を与える際の飼い主の利便性に応えます。

- この地域では、包装オプションに対する消費者の需要が高まり、食品、飲食品、製薬産業での採用が増加しています。また、医療への関心の高まりや環境規制により、軽量でバリア性の高い包装製品の使用が増加しています。リシーラブルの利点は、パーソナルケアや化粧品用途の成長を後押ししています。

- 拡大する外国人人口の存在と新製品を試したいという衝動も、レディミールの需要を後押ししています。この地域では、社会的・経済的パターンの変化により、惣菜を含む手早く簡単な食品へのニーズが高まっています。健康への関心が高まる中、消費者は植物性の惣菜にも注目しています。カナダ農業食糧省によると、カナダにおける植物性惣菜(食肉不使用)の小売売上高は2021年に1,910万米ドル、2022年には2,210万米ドルに達します。

- また、カナダ国内の様々なエンドユーザーにおける需要増加により、カナダ市場における企業プレゼンス拡大のための企業拡大、合併、買収も見られました。

北米のスタンドアップパウチ包装産業の概要

北米のスタンドアップパウチ包装市場はセグメント化されており、Amcor PLC、Mondi Group、Sealed Air Corporation、Sonoco Products Company、Smurfit Kappa Groupなどの大手企業が存在します。市場の参入企業は、製品提供を強化し、サステイナブル競争上の優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2023年7月-フルタマキOYJは米国テキサス州パリの施設に多額の投資を行うと発表しました。この投資は、製造能力の拡大と外部倉庫の統合から成る。生産資産への投資額は約3,000万米ドルで、倉庫と製造施設はリースとなります。これにより、北米事業部門の生産能力を増強し、フードサービス事業の成長をサポートする大きな機会がもたらされます。

- 2023年1月-グレンロイ社は、2年間の開発プロセスを経て、リサイクル可能なSTANDCAPがプラスチックリサイクル協会(APR)からクリティカルガイダンス認定を受けたと発表。硬質プラスチックやガラス瓶に代わる完全なエコフレンドリー代替品として、100%ポリエチレン製のリサイクル可能なSTANDCAPは、環境、消費者、ブランド、小売業者、食品の安全性にとって大きな勝利です。グレンロイは、同社のサステイナブル軟質包装オプションを強調することで、エコロジーの目標に貢献すると同時に、サステイナブルソリューションに対する市場の嗜好の高まりを利用し、長期的なビジネスの成長を促進します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業エコシステム分析

- 産業標準と規制

- スタンドアップパウチ市場における最近のイノベーション

- 比較分析:フラットパウチ包装とスタンドアップパウチ包装の比較

第5章 市場力学

- 市場の促進要因

- 北米での飲食品需要の拡大が見込まれ、市場成長に貢献

- 標準的なパウチは利便性が高く(ジッパー、スライダー、スパウトパックなどがある)、代替品に比べて材料量が少なくて済む

- 市場課題

- スタンドアップパウチを製造するための充填機の変更が、移行を難しくしている

第6章 市場セグメンテーション

- パックタイプ別

- スタンダード

- アセプティック

- レトルト

- その他のパックタイプ

- 材料タイプ別

- プラスチック(PE、PP、PVC、EVOH、バイオプラスチック)

- 金属/箔

- 紙

- エンドユーザー別

- 食品

- 飲料

- 医療医薬品

- ペットフード

- ホーム&パーソナルケア

- その他

- 国別

- 米国

- カナダ

第7章 競合情勢

- 企業プロファイル

- Amcor PLC

- Mondi Group

- Sealed Air Corporation

- Sonoco Products Company

- Smurfit Kappa Group

- ProAmpac LLC

- Clondalkin Group

- Huhtamaki Oyj

- Dazpak Flexible Packaging

- Glenroy Inc.

- PPC Flexible Packaging LLC

第8章 市場の将来

目次

The North America Stand-Up Pouch Packaging Market size is estimated at USD 3.58 billion in 2025, and is expected to reach USD 4.25 billion by 2030, at a CAGR of 3.48% during the forecast period (2025-2030). In terms of market size, the market is expected to grow from 26.99 billion units in 2025 to 31.49 billion units by 2030, at a CAGR of 3.13% during the forecast period (2025-2030).

Stand-up pouch packaging products such as Standard, Aseptic, and Retort are considered under the scope of the market study. Stand-up pouch packaging offers an ideal protective barrier during shipment and transit and prevents any external element, such as moisture and dirt, from coming into contact with the item.

Key Highlights

- The growth of the frozen packaged industry across the region is expected to impact the market positively. Rising demand for packaged food and beverages, increasing demand for Ready-to-Eat (RTE) food, convenience of use, and cost-effectiveness of pouches are primary factors supporting the market growth.

- In addition, the rise in the need for on-the-go snacks has led to the demand for re-closable stand-up pouches as they offer convenience to customers. In addition, the changing lifestyle and food preferences among consumers and changing food technology further boost the market's demand.

- The growing consumer attention to environmental concerns, dynamic regulatory standards, the ongoing drive for sustainability, which comprises replacing plastic-based packaging products with biodegradable materials, and inadequate recycling rates due to the lack of cutting-edge recycling facilities are challenging the market's growth.

- The ongoing technological changes in packaging machinery to cope with the rapidly changing market requirements will pose a challenge as packaging manufacturers using traditional machinery are not well equipped to take the increasing workload of current market requirements. Players must either invest in new tools, spare parts, and software to meet the changing market needs or switch to new machinery.

- The post-COVID-19 pandemic resulted in a surge in demand for packaging aided by the growing demand from the food and beverage and pharmaceutical industries, which will likely continue for the next few years.

North America Stand-Up Pouch Packaging Market Trends

Standard Pack Type Segment is Expected to Hold Significant Market Share

- Standard pouches, including baby food and liquid packaging (tea, coffee, and juices), are widely used in the food and beverage industry. Consumers' expectations for packaged fresh food to store all the natural properties and aromas drive the usage of standard pouches.

- The Standard Stand-up pouches are experiencing a surge in end-user industry demand, prompting manufacturers to strive for innovative solutions. The landscape is characterized by dynamic strategies, with companies adopting approaches such as collaboration, expansion, acquisition, and product launches to stay competitive.

- According to the USDA Foreign Agricultural Service, Coffee consumption in the United States amounted to over 26.3 million 60-kilogram bags in the 2022/2023 fiscal year. This is a slight increase from the total United States coffee consumption in the 2020/2021 fiscal year, which amounted to 25.94 million 60-kilogram bags.

- With increased coffee consumption, there is likely to be a higher demand for packaging solutions to contain and distribute the coffee. Standard Stand-up Pouches are a popular, versatile packaging option offering convenience, protection, and visibility. As coffee consumption rises, the demand for these pouches may also increase.

- The coffee market is highly competitive; brands often use packaging to differentiate themselves. Stand-up pouches provide ample space for branding, labeling, and marketing messages. As coffee consumption increases, companies will invest more in packaging that helps their products stand out on the shelves, which could boost the demand for stand-up pouches.

Canada Expected to Witness Significant Growth

- A key driving factor for the increased demand for stand-up pouches in Canada is the prevalent reliance on packaged and processed foods. University of Toronto's report indicated that approximately 75% of the nation's food supply comes from processed foods. The shift in consumption patterns underscores the need for convenient and sustainable packaging solutions, making stand-up pouches a preferred choice in the Canadian market.

- The food industry is expanding and changing swiftly, extending its packaging alternatives and looking for methods to be more productive. Additionally, more businesses, such as Logos Pack, Omniplast, Canada Brown, Rootree, and Grauman Packaging, are reconsidering their packaging decisions as more eco-friendly and sustainable packaging solutions become available.

- The pet food industry in Canada is booming, and as per Agriculture and Agri-Food Canada (AAFC) data, retail sales of pet food in Canada are expected to increase in CAGR by a further 4.9%, attaining CAD 5.3 billion (USD 0.22 billion) by 2025. In the pet food industry, stand-up pouches are a popular choice for packaging dry and wet pet food. Pouches with tear notches and easy-open features cater to the convenience of pet owners when serving their pets meals.

- The region is witnessing increased consumer demand for packaging options and rising adoption in the food, beverage, and pharmaceutical industries. Also, growing healthcare concerns and environmental regulations have increased the use of lightweight, high-barrier packaging products. The resealable benefit bolsters the growth of personal care and cosmetic applications.

- The existence of an expanding ex-pat population and the urge to try new products also drive the demand for ready meals. The region's need for quick and easy food, including prepared meals, is increasing due to shifting social and economic patterns. With rising health concerns, consumers are also focused on plant-based ready meals. According to Agriculture and Agri-Food Canada, the retail sales of plant-based ready meals (free from meat) in Canada were 19.1 million USD in 2021, reaching 22.1 million USD in 2022.

- The market also witnessed corporate expansions, mergers, and acquisitions to expand corporate presence in the Canadian market due to increased demand across various end-users in the country.

North America Stand-Up Pouch Packaging Industry Overview

The North America stand-up pouch packaging market is fragmented, with the precence of major players like Amcor PLC, Mondi Group, Sealed Air Corporation, Sonoco Products Company, and Smurfit Kappa Group. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- July 2023 - Huhtamaki OYJ announced a significant investment in its Paris, Texas, facility in the United States. The investment consists of an expansion of its manufacturing capacity as well as a consolidation of an external warehouse. The investment into production assets is approximately USD 30 million, and the warehouse and manufacturing facility will be leased. This brings significant opportunities to increase the North America business segment's capacity to support the growth of the food service business.

- January 2023- Glenroy Inc. announced that after a two-year development process, they received Critical Guidance Recognition from the Association of Plastic Recyclers (APR) for the recyclable STANDCAP. As a complete eco-friendly alternative to rigid plastic and glass bottles, the 100% Polyethylene recyclable STANDCAP is a major win for the environment, consumers, brands, retailers, and food safety. By emphasizing the company's sustainable, flexible packaging options, Glenroy contributes to ecological goals while also capitalizing on the growing market preference for sustainable solutions, driving business growth in the long term.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Ecosystem Analysis

- 4.4 Industry Standards and Regulations

- 4.5 Recent Innovations in the Stand-Up Pouch Market

- 4.6 Comparative Analysis: Flat Packaging vs Stand-Up Pouch Packaging

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Demand for Food and Beverage Expected to Grow in North America, thereby Contributing to the Market Growth

- 5.1.2 Standard Pouches Offer a High Level of Convenience (Available in Zipper, Slider, Spout Packs, Etc.) and Require Less Material Volumes as Compared to Alternative

- 5.2 Market Challenges

- 5.2.1 Filling Machinery Changes for Producing Stand-Up Pouches Make Transitions Difficult to Implement

6 MARKET SEGMENTATION

- 6.1 By Pack Type

- 6.1.1 Standard

- 6.1.2 Aseptic

- 6.1.3 Retort

- 6.1.4 Other Pack Types

- 6.2 By Material Type

- 6.2.1 Plastic (PE, PP, PVC, EVOH, Bio-Plastics)

- 6.2.2 Metal/Foil

- 6.2.3 Paper

- 6.3 By End User

- 6.3.1 Food

- 6.3.2 Beverages

- 6.3.3 Medical and Pharmaceutical

- 6.3.4 Pet Food

- 6.3.5 Home and Personal Care

- 6.3.6 Other End Users

- 6.4 By Country

- 6.4.1 United States

- 6.4.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor PLC

- 7.1.2 Mondi Group

- 7.1.3 Sealed Air Corporation

- 7.1.4 Sonoco Products Company

- 7.1.5 Smurfit Kappa Group

- 7.1.6 ProAmpac LLC

- 7.1.7 Clondalkin Group

- 7.1.8 Huhtamaki Oyj

- 7.1.9 Dazpak Flexible Packaging

- 7.1.10 Glenroy Inc.

- 7.1.11 PPC Flexible Packaging LLC

8 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日