|

市場調査レポート

商品コード

1693967

アジア太平洋のクロスラミネートティンバー:市場シェア分析、産業動向、成長予測(2025年~2030年)Asia-Pacific Cross-Laminated Timber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋のクロスラミネートティンバー:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

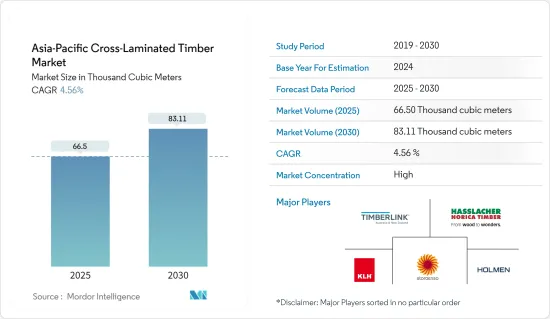

アジア太平洋のクロスラミネートティンバー(CLT)市場規模は、2025年には6万6,500立方メートルと推定・予測され、2030年には8万3,110立方メートルに達すると予測され、予測期間(2025~2030年)のCAGRは4.56%です。

アジア太平洋のクロスラミネートティンバー市場はCOVID-19の悪影響を受けました。厳しい封鎖措置が実施されたため、産業活動は停止しました。しかし、規制解除後は順調に回復しています。産業活動の成長はアジア太平洋のクロスラミネートティンバー市場にプラスの動向をもたらしました。

主要ハイライト

- 短期的には、同地域の商業セクタの成長が市場成長の主要因となっています。

- しかし、材料の吸湿関連リスクは、予測期間中に対象産業の成長を抑制すると予想される主要因です。

- クロスラミネートティンバーをベースとしたカーボンネガティブな未来は、近い将来、世界市場に有利な成長機会を生み出す可能性が高いです。

- 中国は、様々な用途のために国全体でこの材料がかなり消費されているため、この地域で最も成長している市場として浮上しました。

アジア太平洋のクロスラミネートティンバー市場動向

市場を独占する非住宅用途セグメント

- ホテル、オフィス、レストランなどの商業ビルでは、梁、支持構造、家具、床、壁、天井など様々な部分にクロスラミネートティンバーが使用され、部屋に美観を与えています。

- クロス・ラミネーテッドティンバー(CLT)は、その高い強度対重量比、簡単な施工、美的特徴は言うに及ばず、比較的二酸化炭素排出量が少ないことから、建築物建設において鉄骨/コンクリートに代わる革新的な材料として登場しました。

- クロスラミネートティンバーは最近、アジア太平洋の様々な機関で使用されています。例えばオーストラリアでは、今年9月にニューカッスル大学の新校舎にクロスラミネートティンバーが採用されることが決まりました。このプロジェクトには約5,800万豪ドル(約3,725万米ドル)が投じられ、ニューサウスウェールズ州セントラルコーストで建設される初の大量木材を使用した建物となります。

- 今年、シンガポールはアジアで最も著名なマスティンバー・ビル、南洋理工大学(NTU)の南洋ビジネススクール用ガイアビルの建設に投資しました。このプロジェクトは伊東豊雄建築設計事務所が主導したもので、NTUのスポーツホール「ザ・ウェーブ」に続き、NTUキャンパスで2番目にマスティンバーを使用した建物です。

- また、フィリピンのマクタン国際空港は、アジアで初めてグルラムのみで屋根を構成した空港です。グルラム(クロスラミネートティンバー)とは、個々の木材を組み合わせて作られる構造材です。この木材は高い耐久性と耐湿性を持ち、一般的にメラミンやポリウレタン樹脂と呼ばれる産業用接着剤で結合することで、大きなピースやユニークな形態を簡単に作ることができます。

- そのため、商業ビルの建設が増加するにつれて、壁、屋根、床、天井の需要も大幅に増加しており、アジア太平洋諸国におけるクロスラミネートティンバーの大きな市場を形成しています。

市場を独占する中国

- 中国は世界最大の木材輸入国です。中国経済が急速な発展を続ける中、木材セクタも変貌を遂げ、近代化が進んでいます。さらに、中国木材・木材製品協会によれば、中国は世界最大の木材・木材製品消費国であり、輸入木材(RWE)3億1,000万m3を含む年間5億7,000万m3の木材を消費しています。

- 2022年、中国は停滞していた不動産開発を復活させ、デベロッパーの資金不足からの回復を支援するため、いくつかのイニシアチブを開始しました。しかし、年末の新たな調査によると、国内の行き詰まったプロジェクトのうち、完全に建設が再開されたのはわずか21%に過ぎなかりました。

- 中国政府は、経済成長全体を押し上げるため、国内の建設セクタ全体への投資促進に注力しています。例えば、インフラ建設への融資を増やすための最近の動きには、施策銀行の融資比率を1,200億米ドル引き上げることが含まれています。政府はまた、地方政府がインフラ建設資金を調達するための特別公債枠のうち、最大約2,200億米ドルを地方政府が使用できるようにすることも検討しています。

- 建設産業の付加価値は2023年に6%成長し、8兆7,500億人民元(1兆2,000億米ドル)に達すると予想されます。業務用不動産建設はインフラプロジェクトの着工に伴い成長が見込まれるが、住宅建設は2023年にはほとんど伸びないと予測されます。

- 2023年8月、3つの学校と1つの病院プロジェクトの建設が新たな段階に入りました。北京は3つの学校と1つの病院を建設することで、新エリアを援助しています。

- これらの施策が、予測期間中、国内の建設産業を牽引すると予想されます。このため、建設産業で研究される市場の需要に拍車がかかりそうです。政府はまた、COVID-19からの回復後、国の経済的影響から立ち直るために、建設部門、より具体的にはインフラ部門における活動を後押ししたいと考えています。

- したがって、前述の要因は、予測期間中に同国で調査された市場の需要に影響を与えると予想されます。

アジア太平洋のクロスラミネートティンバー産業概要

アジア太平洋のクロスラミネートティンバー市場は、少数の主要企業が市場をリードしており、統合された性質を持っています。主要企業(順不同)には、Stora Enso、Timberlink Australia & New Zealand、KLH Massivholz GmbH、HASSLACHER Holding GmbH、Holmenが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 地域における商業セクタの成長

- その他の伝統的木質材料に対するクロスラミネートティンバーの人気の高まり

- 抑制要因

- 材料の吸湿に関するリスク

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- 接着剤による接着

- 機械的固定

- 用途

- 住宅用

- 非住宅用

- 業務用

- 工業/施設

- その他

- 地域

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- AGROP NOVA a.s.

- HASSLACHER Holding GmbH

- Holmen

- KLH Massivholz GmbH

- Mercer International Inc.

- SCHILLIGER HOLZ AG

- SEIHOKU CORPORATION

- Stora Enso

- Timberlink Australia & New Zealand

- XLam Australia Pty Ltd

第7章 市場機会と今後の動向

- クロスラミネートティンバーによるカーボンネガティブな未来

The Asia-Pacific Cross-Laminated Timber Market size is estimated at 66.50 thousand cubic meters in 2025, and is expected to reach 83.11 thousand cubic meters by 2030, at a CAGR of 4.56% during the forecast period (2025-2030).

The Asia-Pacific cross-laminated timber market was negatively impacted by COVID-19. The implementation of stringent lockdown measures led to a halt of industrial operations. However, the sector has been recovering well since restrictions were lifted. The growth in industrial activities registered a positive trend for the cross-laminated timber market in the Asia-Pacific region.

Key Highlights

- Over the short term, growing commercial sectors in the region are the major factor driving the growth of the market studied.

- However, moisture absorption-related risks of the material are the key factors anticipated to restrain the growth of the target industry over the forecast period.

- Nevertheless, the carbon-negative future based on cross-laminated timber is likely to create lucrative growth opportunities for the global market soon.

- China emerged as the largest growing market for cross-laminated timber in the region owing to considerable consumption of the material across the country for various applications.

Asia-Pacific Cross-Laminated Timber Market Trends

Non-Residential Application Segment to Dominate the Market

- In commercial buildings such as hotels, offices, and restaurants, cross-laminated timber is used in various parts, including beams, support structures, furniture, floors., walls, ceilings, and other such areas, giving the rooms an aesthetic appearance.

- Cross-laminated timber (CLT) has emerged as an innovative alternative material to steel/concrete in building construction, given its relatively low carbon footprint, not to mention its high strength-to-weight ratio, simple installation, and aesthetic features.

- Cross-laminated timber has recently been used in various institutions in the Asia-Pacific. For instance, in Australia, the University of Newcastle's new building was set to be made using cross-laminated timber in September this year. The project cost around AUD 58 million (~ USD 37.25 million) and would be the first mass timber building constructed on the NSW Central Coast.

- This year, Singapore made an investment in the construction of Asia's most prominent mass timber building: the Gaia building for the Nanyang Business School at Nanyang Technological University (NTU). This project has been led by Toyo Ito & Associates, and is the second building on the NTU campus to use mass timber, following NTU's 'The Wave' sports hall.

- The Mactan International Airport in the Philippines is Asia's first airport with a roof structure composed entirely of glulam. Glulam (Glued Laminated Wood) is a structural material produced from the union of individual wood segments. This wood has high durability and humidity resistance, making it easy to make big pieces and unique shapes when binding with industrial adhesives commonly known as melamine or polyurethane resin.

- Therefore, with such a rise in the construction of commercial buildings, the demand for walls, roofs, floors, and ceilings has also increased substantially, thus creating a significant market for cross-laminated timber in the Asia-Pacific countries.

China to Dominate the Market

- China operates as the world's largest importer of timber. As China's economy continues to develop rapidly, the timber sector is also in a state of transformation and modernization. Furthermore, as per the Chinese Timber and Wood Products Association, China is the world's biggest consumer of timber and timber products, with an annual consumption of 570 million m3 of timber, including 310 million m3 of imported timber (RWE).

- In 2022, China launched several initiatives to revive stalled property developments and help developers recover from a funding shortage. Still, at year-end, a new survey showed that only 21% of the country's stalled projects had completely resumed construction.

- The Chinese government is focusing on boosting investments across the construction sector in the country to boost overall economic growth. For instance, recent moves to increase financing for infrastructure construction include a USD 120 billion increase in the lending ratio of policy banks. The government is also considering allowing local governments to spend up to about USD 220 billion of the special bond quota through which local governments fund infrastructure construction.

- The value-added of the construction industry is expected to grow by 6% in 2023, reaching CNY 8.75 trillion (USD 1.2 Trillion). The growth of commercial property construction is expected to increase, with infrastructure projects starting, while residential property construction is projected to show little growth in 2023.

- In August 2023, the construction of 3 schools and one hospital project entered a new phase. Beijing is aiding the new area by building three schools and one hospital.

- These policies are expected to drive the nation's construction industry over the forecast period. This will likely spur the demand for the market studied in the construction industry. The government is also looking forward to boosting activities in the construction sector, more specifically in the infrastructure sector, after the recovery from COVID-19 to bounce back from the country's economic impact.

- Thus, the aforementioned factors are expected to impact the market's demand studied in the country during the forecast period.

Asia-Pacific Cross-Laminated Timber Industry Overview

The Asia Pacific cross-laminated timber (CLT) market is consolidated in nature, with few key players leading the studied market. The major players (not in any particular order) include Stora Enso, Timberlink Australia & New Zealand, KLH Massivholz GmbH, HASSLACHER Holding GmbH, and Holmen.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Commercial Sector in the Region

- 4.1.2 Increasing Popularity of Cross-Laminated Timber Over other Traditional Wood Materials

- 4.2 Restraints

- 4.2.1 Moisture Absorption Related Risks of the Material

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Adhesive Bonded

- 5.1.2 Mechanically Fastened

- 5.2 Application

- 5.2.1 Residential

- 5.2.2 Non-Residential

- 5.2.2.1 Commercial

- 5.2.2.2 Industrial/Institutional

- 5.2.2.3 Other Applications

- 5.3 Geography

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 South Korea

- 5.3.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AGROP NOVA a.s.

- 6.4.2 HASSLACHER Holding GmbH

- 6.4.3 Holmen

- 6.4.4 KLH Massivholz GmbH

- 6.4.5 Mercer International Inc.

- 6.4.6 SCHILLIGER HOLZ AG

- 6.4.7 SEIHOKU CORPORATION

- 6.4.8 Stora Enso

- 6.4.9 Timberlink Australia & New Zealand

- 6.4.10 XLam Australia Pty Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Carbon-negative Future Based on Cross-laminated Timber