|

市場調査レポート

商品コード

1693871

欧州のチーズ:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Europe Cheese - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のチーズ:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 201 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

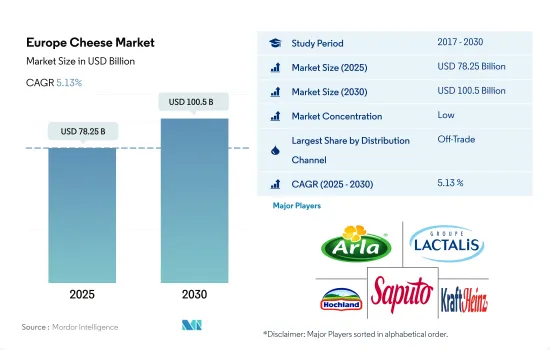

欧州のチーズ市場規模は2025年に782億5,000万米ドルと推定・予測され、2030年には1,005億米ドルに達し、市場推定・予測期間(2025~2030年)のCAGRは5.13%で成長すると予測されます。

スーパーマーケットとハイパーマーケットの存在感の高まりが欧州の小売業を促進

- オフチャネルの高い市場シェアは、主にハイパーマーケット/スーパーマーケットが牽引しています。戦略的な製品ポジショニング、チーズ製品専用の棚スペース、世界ブランドとともに地元ブランドの入手可能性などが、これらのチャネルを通じたチーズ販売を促進する主要因です。欧州では、スーパーマーケット/ハイパーマーケットが2022年のチーズ販売額の58.45%を占めています。

- 主要スーパーマーケットとハイパーマーケットチェーンは、最大市場をカバーするため、地域内のさまざまな場所に店舗網を構築しています。同市場で確認されている主要事業者には、Metro Group、Ahold Delhaize、Fidesco、AmazonFresh、Walmart、Tesco、REWE Group、Kaufland、Aldiなどがあります。ドイツ、フランス、英国は、この地域で最も多くのスーパーマーケットとハイパーマーケットを展開しています。2022年には、3カ国合計で欧州のスーパーマーケットとハイパーマーケットを通じたチーズ数量全体の36.29%のシェアを獲得しました。

- 現代の消費者は多忙なライフスタイルのため、食料品のオンライン購入を好むため、オンラインチャネルが最も急成長する流通チャネルになると予測されます。インターネットユーザーの増加に伴い、オンラインチーズ・ショップの数が増加しているため、予測期間中、天然・チーズのオンライン販売が促進されると予想されます。2022年には、インターネットにアクセスできる世帯のシェアは、2011年の72%から93%に増加しました。オランダ、フランス、英国、ドイツ、イタリアはインターネット利用者の普及率が高い国です。主要オンラインチーズ小売業者には、FROMAGES.COM、The East London Cheese Board、La Gourmeta、Love Cheese、Italia Regina、Frank and Salなどがあります。オンラインチャネルの販売額は、2023~2029年にかけてCAGR 5.15%を記録すると予測されます。

ドイツ、フランス、イタリアが牽引する爆発的なチーズ消費が成長の原動力

- チーズは伝統的に、現地の生乳要件を満たした後のEU産生乳の優先的な販売先と見なされてきました。チーズ部門は2022年に11.20%の市場数量シェアを獲得し、2017~2022年までの販売数量成長率は8.46%でした。チーズは、イタリア料理、英国料理、ドイツ料理、ギリシャ料理、フランス料理などの欧州料理に欠かせないものです。

- ドイツ、フランス、イタリアはチーズ消費量の多い国であり、2022年には同地域のチーズ消費量全体の39.53%を占めています。イタリアでは400種類以上のチーズが生産されています。モッツァレラ、パルメザン、ペコリーノはイタリアの郷土料理でよく使われるチーズです。ピッツァ、バルサミコ・ディ・モデナ、リゾット、トルテッリーニ、ポレンタ、ペストは、トッピングまたはフィリングとしてチーズを使用する主要なイタリア料理です。

- フランス人の平均年間チーズ消費量が26.5kgであることも、チーズの存在感を高めています。実際、ほぼ40%の人が毎日チーズを消費し、95%以上の人が普段の食生活にチーズを取り込んでいます。英国では、チーズのような付加価値の高い乳製品の消費が伸びています。これは、農場から出荷される生乳を使用する加工業者に影響を与えています。2019年、チーズに使われる生乳の量は10億9,000万リットル増加しました。

- スーパーマーケット/ハイパーマーケットは、欧州におけるチーズの主要な流通チャネルとして認識されています。このセグメントは2022年に数量全体の44.33%のシェアを獲得しました。チーズのオントレード消費は、マクドナルド、KFC、タコベル、サブウェイ、バーガーキングといった大手ファーストフードブランドの存在によって牽引されています。フランスを拠点とするファストフードレストランチェーンのバーガーキングは、フランス全土に480店舗以上を展開しています。オンチャネルでの数量は、2023~2029年にCAGR 0.73%を記録すると予測されています。

欧州のチーズ市場動向

欧州の様々な文化圏におけるチーズ消費の増加が、チーズの高い需要と消費の一因となっています。

- 2022年のチーズの一人当たり消費量は、2021年と比較して3%増加しました。欧州の人々は少なくとも7,000年前からチーズを食べています。チーズは、イタリア料理、英国料理、ドイツ料理、ギリシャ料理、フランス料理などの欧州料理に欠かせないものです。欧州連合(EU)では年間約900万トンのチーズが消費されています。パスタ、ピザ、サンドイッチ、ハンバーガーなど、欧州料理のさまざまな料理はチーズなしには成立しないです。2021年8月に実施された消費者調査によると、調査対象者1,554人のうち71%が定期的にチーズを食べていることが明らかになりました。

- 消費されるチーズの多くも欧州で生産されており、主にフランス、イタリア、ドイツ、オランダで生産されています。これらの国々は、2022年にこの地域で消費されるチーズ全体の39.53%を占めています。チーズはその多様な風味と社会的側面から、フランス人の間で高く評価されています。実際、ほぼ40%の人々が毎日チーズを消費しており、95%以上が普段の食生活にチーズを取り入れています。フランス人の平均年間消費量が26.5kgであることも、チーズの存在感を高めています。

- 各国の消費パターンは大きく異なります。イタリアのチーズ生産者は、約400種類のチーズを生産しています。イタリアの郷土料理では、モッツァレラチーズ、パルメザンチーズ、ペコリーノチーズがよく使われます。ピッツァ、バルサミコ・ディ・モデナ、リゾット、トルテッリーニ、ポレンタ、ペストは、トッピングやフィリングとしてチーズを使った主要イタリア料理です。牛乳から作られるチーズは、どの地域でも最も好まれています。例えば、フランスには1,000種類ものチーズが存在するが、中でもラクレットチーズ、クリーミーなカマンベールチーズ、エメンタールチーズなどは、牛乳から作られるチーズとして消費量が多いです。

欧州のチーズ産業概要

欧州のチーズ市場は細分化されており、上位5社で13.04%を占めています。この市場の主要企業は、Arla Foods amba、Groupe Lactalis、Hochland Holding GmbH & Co. KG、Saputo Inc.、The Kraft Heinz Companyなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 一人当たり消費量

- 原料/商品生産量

- チーズ

- 規制の枠組み

- フランス

- ドイツ

- イタリア

- 英国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 製品タイプ

- 天然チーズ

- プロセスチーズ

- 流通チャネル

- オフトレード

- サブ流通チャネル別

- コンビニエンスストア

- オンライン小売

- 専門店

- スーパーマーケットとハイパーマーケット

- その他(倉庫クラブ、ガソリンスタンドなど)

- オントレード

- オフトレード

- 国名

- ベルギー

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- トルコ

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Arla Foods amba

- Bel Group

- Egidio Galbani SRL

- Granarolo SpA

- Groupe Lactalis

- Groupe Sodiaal

- Hochland Holding GmbH & Co. KG

- Kingcott Dairy

- Koninklijke ERU Kaasfabriek BV

- Saputo Inc.

- Savencia Fromage & Dairy

- The Kraft Heinz Company

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 50000735

The Europe Cheese Market size is estimated at 78.25 billion USD in 2025, and is expected to reach 100.5 billion USD by 2030, growing at a CAGR of 5.13% during the forecast period (2025-2030).

Greater presence of supermarket and hypermarket is promoting the retailing segment in europe

- The high market share of off-trade channels is primarily driven by hypermarkets/supermarkets. Strategic product positioning, dedicated shelf space for cheese products, and the availability of local brands, along with global brands, are key factors driving cheese sales through these channels. In Europe, supermarkets/hypermarkets covered 58.45% of cheese sales, in terms of value, in 2022.

- Key supermarket and hypermarket chains have established a network of stores in different locations across the region to cover the maximum market. Some of the major operators identified in the market include Metro Group, Ahold Delhaize, Fidesco, AmazonFresh, Walmart, Tesco, REWE Group, Kaufland, and Aldi. Germany, France, and the United Kingdom hold the largest number of supermarket and hypermarket stores in the region. In 2022, three countries collectively acquired a 36.29% share in the overall cheese sales volume through supermarkets and hypermarkets in Europe.

- The online channel is projected to be the fastest-growing distribution channel as modern consumers prefer online grocery purchases due to their busy lifestyles. The increasing number of online cheese shops in response to the rising number of internet users is anticipated to drive online sales of natural cheese during the forecast period. In 2022, the share of households with internet access was recorded as 93%, up from 72% in 2011. Netherlands, France, the United Kingdom, Germany, and Italy are the countries with high penetration of internet users. Key online cheese retailers include FROMAGES.COM, The East London Cheese Board, La Gourmeta, Love Cheese, Italia Regina, and Frank and Sal. The online channel sales value is anticipated to register a CAGR of 5.15% during 2023-2029.

Explosive cheese consumption led by Germany, France, and Italy is fueling the growth

- Cheese has traditionally been considered the preferred outlet for milk from the European Union after local fresh-milk requirements have been met. The cheese segment acquired a market volume share of 11.20% in 2022, with a volume sales growth of 8.46% from 2017 to 2022. Cheese is an integral part of European cuisines like Italian, British, German, Greek, and French.

- Germany, France, and Italy are highly cheese-consuming countries and collectively covered 39.53% volume of the overall cheese consumed in the region in 2022. More than 400 types of cheeses are produced in Italy. Mozzarella, parmesan, and Pecorino are commonly used cheeses in regional Italian cuisines. Pizza, Balsamic di Modena, Risotto, Tortellini, Polenta, and Pesto are key Italian dishes featuring cheese either as a topping or filling.

- The fact that an average French individual consumes 26.5 kilograms of cheese per year adds to its prominence. In fact, almost 40% of people consume cheese every day, and over 95% have included it in their regular diet. The consumption of value-added dairy products like cheese is growing in the United Kingdom. This has influenced processors using raw milk delivered off farms. In 2019, the volume of raw milk going into cheese rose by 1.09 billion liters.

- Supermarkets/hypermarkets are identified as major distribution channels for cheese in Europe. The segment acquired a 44.33% share of the overall sales volume in 2022. On-trade consumption of cheese is driven by the presence of leading fast-food brands such as McDonald's, KFC, Taco Bell, Subway, and Burger King. Burger King, a France-based fast-food restaurant chain, has more than 480 stores across France. Volume sales across on-trade channels are projected to register a CAGR of 0.73% during 2023-2029.

Europe Cheese Market Trends

The increased cheese consumption in Europe across various European cultures contributes to its high demand and consumption

- The per capita consumption of cheese increased by 3% in 2022 compared to 2021. Europeans have been eating cheese for at least 7,000 years. Cheese is an integral part of European cuisines like Italian, British, German, Greek, and French. Approximately nine million metric tons of cheese are consumed annually in the European Union. Different dishes in European cuisine, including pasta, pizza, sandwiches, and burgers, are incomplete without cheeses. A consumer study conducted in August 2021 revealed that 71% of respondents among the 1,554 surveyed population eat cheese regularly.

- Much of the cheese consumed is also produced in Europe, mainly in France, Italy, Germany, and the Netherlands. These countries collectively covered 39.53% volume of the overall cheese consumed in the region in 2022. Cheese is highly valued among French people due to its diverse flavor and the social aspect it offers. In fact, almost 40% of people consume cheese every day, and over 95% have included it in their regular diet. The fact that an average French individual consumes 26.5 kilograms of cheese per year adds to its prominence.

- The consumption patterns of various nations vary significantly. Italian producers of cheeses have around 400 different varieties. Regional Italian cuisines frequently use mozzarella, parmesan, and pecorino cheeses. Pizza, Balsamic di Modena, Risotto, Tortellini, Polenta, and Pesto are key Italian dishes featuring cheese either as a topping or filling. Cheese made from cow milk is most preferred across the regions. For instance, among the 1,000 types of cheeses that exist in France, Raclette cheese, creamy Camembert, and Emmental, among others, are highly consumed ones that are made from cow's milk.

Europe Cheese Industry Overview

The Europe Cheese Market is fragmented, with the top five companies occupying 13.04%. The major players in this market are Arla Foods amba, Groupe Lactalis, Hochland Holding GmbH & Co. KG, Saputo Inc. and The Kraft Heinz Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Per Capita Consumption

- 4.2 Raw Material/commodity Production

- 4.2.1 Cheese

- 4.3 Regulatory Framework

- 4.3.1 France

- 4.3.2 Germany

- 4.3.3 Italy

- 4.3.4 United Kingdom

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Product Type

- 5.1.1 Natural Cheese

- 5.1.2 Processed Cheese

- 5.2 Distribution Channel

- 5.2.1 Off-Trade

- 5.2.1.1 By Sub Distribution Channels

- 5.2.1.1.1 Convenience Stores

- 5.2.1.1.2 Online Retail

- 5.2.1.1.3 Specialist Retailers

- 5.2.1.1.4 Supermarkets and Hypermarkets

- 5.2.1.1.5 Others (Warehouse clubs, gas stations, etc.)

- 5.2.2 On-Trade

- 5.2.1 Off-Trade

- 5.3 Country

- 5.3.1 Belgium

- 5.3.2 France

- 5.3.3 Germany

- 5.3.4 Italy

- 5.3.5 Netherlands

- 5.3.6 Russia

- 5.3.7 Spain

- 5.3.8 Turkey

- 5.3.9 United Kingdom

- 5.3.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Arla Foods amba

- 6.4.2 Bel Group

- 6.4.3 Egidio Galbani SRL

- 6.4.4 Granarolo SpA

- 6.4.5 Groupe Lactalis

- 6.4.6 Groupe Sodiaal

- 6.4.7 Hochland Holding GmbH & Co. KG

- 6.4.8 Kingcott Dairy

- 6.4.9 Koninklijke ERU Kaasfabriek BV

- 6.4.10 Saputo Inc.

- 6.4.11 Savencia Fromage & Dairy

- 6.4.12 The Kraft Heinz Company

7 KEY STRATEGIC QUESTIONS FOR DAIRY AND DAIRY ALTERNATIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms