|

市場調査レポート

商品コード

1911772

中東衛星通信市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Middle East Satellite Communications - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東衛星通信市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 171 Pages

納期: 2~3営業日

|

概要

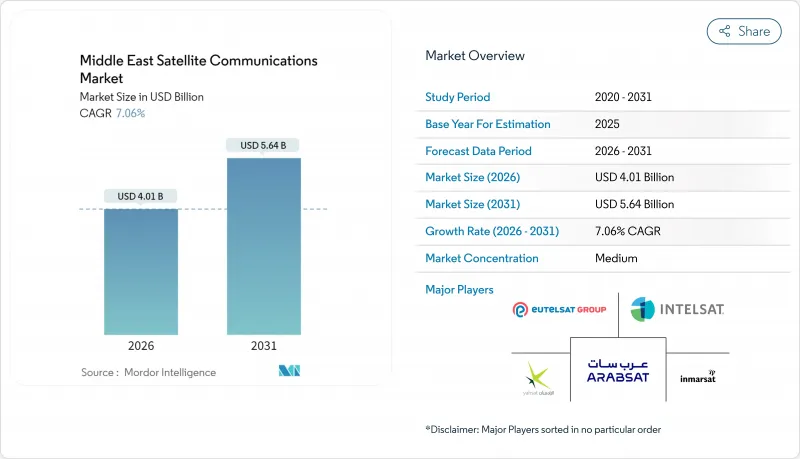

中東の衛星通信市場規模は、2026年には40億1,000万米ドルと推定されており、2025年の37億4,000万米ドルから成長が見込まれます。

2031年の予測では56億4,000万米ドルに達し、2026年から2031年にかけてCAGR7.06%で拡大する見通しです。

地政学的な複雑性、政府主導のブロードバンド義務化、ならびに油田、港湾、航空機におけるIoT導入の急増が相まって需要を拡大しております。事業者様は、帯域幅を大量に消費する企業および防衛分野のニーズに対応するため、高スループット衛星(HTS)への投資を優先しております。一方で、周波数調整の課題により新規打ち上げコストは上昇傾向にあります。競争上の優位性は、クラウドゲートウェイ、マネージド接続、エッジ分析機能を融合した垂直統合型サービスバンドルにますます依存しています。海上・航空機向け接続、5Gプライベートネットワークのバックホール、デバイス直結型(D2D)イニシアチブは、高収益ニッチ市場として台頭しており、中東衛星通信市場の次なる成長波を形成するでしょう。

中東衛星通信市場の動向と洞察

IoT対応油田設備の導入拡大

衛星接続センサー数千台が遠隔油井の圧力・流量・排出量を監視し、予知保全を可能にするとともに予期せぬ操業停止を低減しています。サウジアラムコのリアルタイム油井監視ネットワークは、光ファイバーが不可能な地域でエネルギー大手が宇宙通信を活用する好例です。Space42社のAIを活用した分析技術は採掘効率をさらに向上させ、Globalstar社のタンク監視ツールは湾岸地域のターミナルにおける供給中断を削減します。これらの導入は運用コストを削減し、中東衛星通信市場を持続させる継続的な帯域幅需要を生み出しています。

VSATベースの海上通信の急速な普及

ドバイ、ジェッダ、ドーハの主要港湾では船舶交通管理や貨物分析にVSATを活用しており、海運会社による船隊全体のアップグレードを推進しています。マーリンク社が地域事業者との間で締結した契約は、HTS容量が映像配信、IoTテレメトリー、乗組員福祉サービスを提供する実例を示しています。自律航行プラットフォームとの統合により、無人水上艇の規制面での進展に伴い新たな収益源が開拓されています。

周波数帯域の混雑と国境を越えた周波数紛争

衛星の急速な普及により干渉リスクが悪化し、ITUの調整手続きは対応に追われています。クワッドサット社とアラブサット社の周波数監視契約は拡大しており、自動化ツールの重要性が業界で認識されつつあります。しかしながら、未解決のCバンドおよびKuバンドの重複は打ち上げの遅延や保険料の上昇を招き、中東衛星通信市場に摩擦を生じさせています。

セグメント分析

地上設備は2025年、中東衛星通信市場で58.05%のシェアを維持しました。サウジアラビアとUAEにおけるテレポート、ゲートウェイ、VSATの展開が基盤となっています。しかしながら、サービス収益はハードウェアを上回る7.85%のCAGRで成長が見込まれており、管理型帯域幅パッケージ、クラウドゲートウェイ、衛星対応IoTプラットフォームが牽引役となっています。

サービス分野の成長は、ネットワーク管理の負担を軽減する従量課金モデルに対する企業の需要を反映しています。エスヘイルサット社とネクサット社のOSS/BSS提携は、自動化が運用コスト削減と導入促進に寄与する好例です。HTSペイロードの普及に伴い、事業者はサイバーセキュリティ、エッジ分析、SLAに基づく稼働時間保証をパッケージ化し、中東衛星通信市場における顧客の支出シェアを拡大しています。

2025年の中東衛星通信市場シェアにおいて、海上アプリケーションは40.30%を占めました。これはスエズ運河やホルムズ海峡を通る密集した航路が要因です。一方、航空機向け接続は8.22%という最速のCAGRを記録すると予測されています。航空会社が乗客のストリーミング需要を満たす競争を激化させ、防衛用UAV(無人航空機)艦隊が拡大しているためです。

地域航空会社は顧客体験の差別化を図るためKaバンド機内Wi-Fiを導入し、UAEの都市型航空モビリティ実証事業では指揮統制に低遅延衛星リンクを活用しています。陸上プラットフォームは油田SCADAバックアップや災害復旧ネットワークにおいて依然として重要であり、中東衛星通信市場を支える多様な需要基盤を強化しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- IoT対応油田設備の導入拡大

- VSATベースの海上通信接続の急速な普及

- ユニバーサルブロードバンド政府プログラム(サウジアラビア、アラブ首長国連邦)

- 民間衛星間データ中継ネットワークの成長

- 5Gプライベートネットワーク向け衛星バックホール需要の増加

- GCCコンソーシアムを通じた協力的な深宇宙探査ミッションの拡大

- 市場抑制要因

- 周波数帯域の混雑と国境を越えた周波数紛争

- HTS艦隊アップグレードの高額な設備投資費用

- 特定国に対する地政学的打ち上げサービス制限

- 地域における衛星通信グレード耐放射線性チップの不足

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- マクロ経済要因の影響

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- タイプ別

- 地上設備

- 衛星ゲートウェイ

- VSAT機器

- ネットワーク運用センター(NOC)

- 衛星ニュース収集(SNG)機器

- サービス

- 移動体衛星通信サービス(MSS)

- 地球観測サービス

- 地上設備

- プラットフォーム別

- 携帯型

- 陸上

- 海上

- 航空機搭載型

- 周波数帯別

- Lバンド

- Cバンド

- Kuバンド

- Kaバンド

- エンドユーザー業界別

- 海上

- 防衛・政府機関

- 企業向け

- メディアとエンターテイメント

- 石油・ガス

- その他のエンドユーザー業種

- 用途別

- 音声通信

- データ通信

- 放送

- リモートセンシング

- 国別

- サウジアラビア

- アラブ首長国連邦

- カタール

- オマーン

- クウェート

- トルコ

- その他中東

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Al Yah Satellite Communications Company PJSC(Yahsat)

- Inmarsat Global Limited(now Viasat Inc.)

- Arab Satellite Communications Organization

- Intelsat S.A.

- Eutelsat Communications S.A.

- SES S.A.

- Thuraya Telecommunications Company PJSC

- Gulfsat Communications Company K.S.C.C.

- Saudi Telecom Company(Saudi Telecom Co.)

- Etisalat and(Emirates Telecommunications Group Co. PJSC)

- Telesat Canada

- L3Harris Technologies Inc.

- Raytheon Technologies Corporation

- Kratos Defense and Security Solutions Inc.

- Cobham Limited

- Huawei Technologies Co. Ltd.

- Anuvu Operations LLC

- SatADSL S.A.

- OneWeb Holdings Ltd.

- Taqnia Space Co.