|

|

市場調査レポート

商品コード

1693813

タンタルコンデンサ-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Tantalum Capacitors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| タンタルコンデンサ-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 103 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

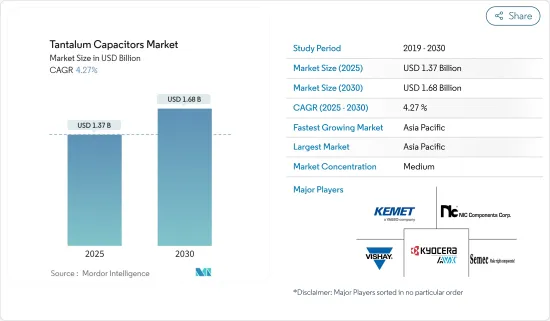

タンタルコンデンサ市場規模は、2025年に13億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.27%で、2030年には16億8,000万米ドルに達すると予測されます。

タンタルコンデンサは、陽極にタンタル金属を使用した電解コンデンサです。タンタルコンデンサは分極コンデンサで、より高い周波数特性と反発特性を持っています。同じ静電容量のアルミ電解コンデンサよりも小さいです。タンタルコンデンサの定格電圧範囲は、2Vから500V以上と幅広いです。

主要ハイライト

- タンタルコンデンサは、医療機器、民生用電子機器、自動車、産業用など複数の最終用途で使用されています。タンタルコンデンサは、PC、ノートPC、医療機器、オーディオアンプ、自動車回路、スマートフォン、デジタルカメラ、ポータブルメディア参入企業、その他の表面実装デバイス(SMD)など、様々な電子機器用途で一般的に使用されています。

- 2023年11月のTME Electronic Componentsによると、タンタルコンデンサは非常に多くの利点を誇っているため、さまざまな用途に使用できます。また、アルミ電解コンデンサやMLCCの置き換えやサポートにも使用できます。タンタルコンデンサの本質的な特徴の一つは、広い温度範囲にわたってパラメータが安定していることであり、静電容量は-55℃から125℃の温度範囲で安定しています。

- タンタルコンデンサは老朽化しないため、長年にわたりパラメータを保持します。タンタルコンデンサはまた、高い体積効率を特徴としています。例えば、標準的なSMDアルミ電解コンデンサの体積効率は11.8μFV/mm3であるのに対し、タンタルコンデンサは63μFV/mm3以上の効率を達成しています。

- タンタルコンデンサの主原料であるタンタル鉱石の価格変動により、市場は大きな課題に直面する可能性があります。タンタルコンデンサの価格は、地政学的緊張、複数の産業からの需要の変化、サプライチェーンの混乱、原料調達に関する特定の法律や規制など、さまざまな要因に基づいて変動する可能性があります。

- 同市場は、民生用電子機器部門の拡大、電子ガジェット市場の進展、5Gのような先端技術の普及拡大が原動力となって継続的な成長を遂げています。加えて、自動車産業の電気自動車への移行とIoTデバイスの台頭が市場の成長にさらに貢献しています。メーカーがより小型で効率的なコンデンサの開発に注力する中、継続的な技術革新と各産業における電子統合の高まりに後押しされ、市場は持続的な成長を遂げる構えです。

タンタルコンデンサ市場動向

コンシューマーエレクトロニクス部門が大きな成長を牽引

- タンタルコンデンサは、スマートフォンを含む様々な民生用電子機器に一般的に使用されています。これらのコンデンサは、スマートフォンのGSM用パワーアンプ(PA)の電源ラインに接続されるコンデンサとして使用されることが多いです。タンタルコンデンサはサイズが小さいため、スマートフォンのようなフットプリントの小さいアプリケーションでの使用に適しています。

- Ericssonによると、世界のスマートフォン契約数は2022年に66億を超えました。2028年には78億に達すると予想されています。スマートフォンのモバイルネットワーク契約数が最も多い国は、米国、中国、インドです。このようなスマートフォンの大幅な増加は、市場を牽引すると考えられます。

- タンタルコンデンサは、ノートパソコンやその他の電子機器にも使われています。例えば、ノートパソコン、特にマザーボードの電源フィルターには、1個あたり約1グラムのタンタルが使用されていることが調査によって実証されました。これは、タンタルコンデンサがMLCCコンデンサよりも高い静電容量値を提供し、マイクロフォニック効果を示さないためで、平坦またはコンパクトな設計のデバイスにとって魅力的な選択肢となっています。

- 5Gに対応したスマートフォンが普及し、ウェアラブルデバイスのような機器の多機能化・小型化が進む中、電子回路の小型化・高密度化のニーズが高まっています。さらに、5Gの急速な普及に伴い、タンタルコンデンサへのニーズも高まっています。固体コンデンサを湿式タンタルコンデンサに置き換えることは、近いうちに機会をもたらすと考えられます。

- GSMA Intelligenceが最近発表したデータによると、5G接続は2029年までに全モバイル接続の半分以上(51%)を占めるようになります。この割合は10年後までには56%までさらに増加し、5Gが接続性の主要技術として確固たるものになると予想されています。この数字は、2023年末までに16億接続、2030年までに55億接続に達すると予想されています。タンタルコンデンサはネットワーク機器の効率的な機能をサポートし、データ伝送の速度を高め、接続性を強化し、最終的にタンタルコンデンサ市場の成長を促進します。

アジア太平洋が著しい成長を遂げる

- アジア太平洋がよりクリーンなエネルギー源への移行を受け入れ、二酸化炭素排出量の削減に努める中、電気自動車の需要が増加しています。その結果、これらの自動車に電力を供給するためのタンタルコンデンサへのニーズが高まっています。電気自動車のバッテリーにおいて、タンタルコンデンサはエネルギー効率を改善し、バッテリーの寿命を延ばし、全体的な性能を向上させる上で非常に重要です。

- さらに、スマートフォンやその他のモバイル機器などの民生用電子機器は、アジア太平洋におけるタンタルコンデンサのさらなる需要を牽引しています。消費者がより小さく、より軽く、より強力なデバイスを求めているため、メーカーはこれらの要件を満たすためにタンタルコンデンサに目を向けています。

- アジア太平洋における5G技術の展開は、通信インフラにおけるタンタルコンデンサの需要を煽っています。タンタルコンデンサは、効率的な電力管理、フィルタリング、信号調整を促進することで、5G基地局、アンテナ、その他の通信機器において重要な役割を果たしています。

- 次世代通信ネットワークの建設が進む中、メイン回路基板とGaN RFパワーアンプの両方にまたがるこの用途でのタンタルコンデンサの利用が急増する見込みです。

タンタルコンデンサ産業概要

タンタルコンデンサ市場は、世界市場の大手ベンダーによって半固定化されています。主要企業は、市場シェアを向上させ、市場での収益性を高めるために、買収や提携など様々な戦略に取り組んでいます。市場の主要企業には、Vishay Intertechnology Inc.、Kemet Corporation(YAGEO Corporation)、NIC Components Corp.、KYOCERA AVX Components Corporation、Semec Technology Company Limitedなどが含まれます。

- 2024年3月、KEMETは、軍事性能仕様書MIL-PRF-32,700/2の要件を満たす全く新しいT581ポリマータンタル表面実装コンデンサを発表しました。この発売は、ポリマータンタル表面実装コンデンサの市場導入を意味し、新しい仕様を満たす最初のコンデンサとなります。これによりKEMETは、防衛・航空宇宙セグメントの高信頼性アプリケーション市場における主要企業としての地位をさらに強固なものにします。

- 2023年11月、Vishay Intertechnology Inc.は、Nexperia BVとの間で、Nexperiaの英国におけるウエハー製造工場と事業を現金約1億7,700万米ドルで買収する最終契約を締結したと発表した(売却後の調整を条件とする)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- バリューチェーン分析

- 市場のマクロ経済動向評価

第5章 市場力学

- 市場の促進要因

- デバイスの小型化への注目の高まり

- 自動車エレクトロニクスの台頭

- 市場抑制要因

- タンタル鉱石価格の変動

第6章 市場セグメンテーション

- 用途別

- 医療機器

- 民生用電子機器

- 自動車

- 産業用

- その他

- 地域別

- 南北アメリカ

- 欧州、中東・アフリカ

- アジア

- オーストラリアとニュージーランド

- 日本

- 韓国

第7章 競合情勢

- 企業プロファイル

- Vishay Intertechnology Inc.

- Kemet Corporation(YAGEO Corporation)

- NIC Components Corp.

- KYOCERA AVX Components Corporation(KYOCERA CORPORATION)

- Semec Technology Company Limited

- Samsung Electro-Mechanics

- Exxelia Group

- Abracon LLC

- Panasonic Corporation

- NTE Electronics Inc.

第8章 投資分析

第9章 市場の将来展望

The Tantalum Capacitors Market size is estimated at USD 1.37 billion in 2025, and is expected to reach USD 1.68 billion by 2030, at a CAGR of 4.27% during the forecast period (2025-2030).

Tantalum capacitors are electrolytic capacitors that use tantalum metal for the anode. They are polarized capacitors with higher frequency and resilience characteristics. They are smaller than aluminum electrolytic capacitors of the same capacitance. The voltage range rating for tantalum capacitors varies from 2 V to more than 500 V.

Key Highlights

- Tantalum capacitors are used across multiple end-user applications such as medical devices, consumer electronics, automotive, and industrial. Tantalum capacitors are commonly used in various electronic applications, including PCs, laptops, medical devices, audio amplifiers, automotive circuitry, smartphones, digital cameras, portable media players, and other surface-mounted devices (SMD).

- According to TME Electronic Components, in November 2023, tantalum capacitors boast a significant number of advantages and thus can be used in many different applications. They can also be used to replace or support aluminum electrolytic capacitors and MLCCs. One of the essential features of tantalum capacitors is their stability of parameters over a wide range of temperatures - capacitance is stable in temperature ranges from -55°C to 125°C.

- Tantalum capacitors do not age, so they retain their parameters for many years. Tantalum capacitors also feature high volumetric efficiency. For instance, standard SMD aluminum electrolytic capacitors have a volumetric efficiency of 11.8 µFV/mm3, whereas tantalum capacitors attain an efficiency of 63 µFV/mm3 and above.

- The market may face a significant challenge due to the fluctuating prices of tantalum ore, the primary raw material used to produce tantalum capacitors. The prices of tantalum capacitors are subject to change based on various factors, including geopolitical tensions, demand changes from multiple industries, disruption in the supply chain, and specific laws and regulations on the sourcing of material.

- The market is experiencing continued growth driven by the expanding consumer electronics sector, the advancing market for electronic gadgets, and the growing prevalence of advanced technologies like 5G. In addition, the automotive industry's transition toward electric vehicles and the rise of IoT devices further contribute to the market's growth. As manufacturers focus on developing smaller, efficient capacitors, the market is poised for sustained growth, pushed by ongoing technological innovations and rising electronic integration across industries.

Tantalum Capacitors Market Trends

Consumer Electronics Segment to Witness Major Growth

- Tantalum capacitors are commonly used in various consumer electronic devices, including smartphones. These capacitors are often used as the capacitors connected to the power line of the Power Amplifier (PA) for GSM on smartphones. Tantalum capacitors are small in size, making them suitable for use in small-footprint applications like smartphones.

- According to Ericsson, the global number of smartphone subscriptions reached over 6.6 billion in 2022. It is expected to hit 7.8 billion by 2028. The countries with the most smartphone mobile network subscriptions are the United States, China, and India. Such a huge rise in smartphones would drive the market.

- Tantalum capacitors are also used in laptops and other electronic devices. For example, researchers demonstrated that about 1 gram of tantalum is used per unit in laptops, specifically in motherboard power supply filters. This is because tantalum capacitors offer higher capacitance values than MLCC capacitors and display no microphonic effect, making them an attractive option for devices with flat or compact designs.

- With smartphones supporting 5G becoming more widespread and devices like wearable devices becoming increasingly multifunctional and compact, the need for smaller, higher-density electronic circuitry is increasing. Moreover, as 5G is rapidly growing, the need for a tantalum capacitor increases. Replacing solid capacitors with wet tantalum capacitors will likely present an opportunity soon.

- According to recent data released by GSMA Intelligence, 5G connections will account for more than half (51%) of all mobile connections by 2029. This percentage is expected to increase further to 56% by the end of the decade, solidifying 5G as the leading technology for connectivity. This number is anticipated to reach 1.6 billion connections by the end of 2023 and 5.5 billion by 2030. The tantalum capacitors support the effective functioning of network equipment, enhancing the speed of data transmission and strengthening connectivity, ultimately propelling the growth of the tantalum capacitors market.

Asia-Pacific to Witness Significant Growth

- As the Asia-Pacific region embraces the transition towards cleaner energy sources and strives to reduce carbon emissions, the demand for electric vehicles has increased. Consequently, there is an increased need for tantalum capacitors to power these vehicles. In electric vehicle batteries, tantalum capacitors are crucial in improving energy efficiency, extending battery life, and enhancing overall performance.

- Additionally, consumer electronics such as smartphones and other mobile devices drive further demand for tantalum capacitors in Asia-Pacific. As consumers demand smaller, lighter, and more powerful devices, manufacturers turn to tantalum capacitors to meet these requirements.

- The deployment of 5G technology in the Asia-Pacific region has fueled the demand for tantalum capacitors in telecommunication infrastructure. Tantalum capacitors play a vital role in 5G base stations, antennas, and other telecommunications equipment by facilitating efficient power management, filtering, and signal conditioning.

- With the ongoing construction of the next generation of telecom networks, there is poised to be a surge in the utilization of tantalum capacitors in this application, spanning both the main circuit boards and the GaN RF power amplifier.

Tantalum Capacitors Industry Overview

The tantalum capacitors market is semi-consolidated due to large vendors in the global market. The key players are involved in various strategies, such as acquisitions and partnerships, to improve their market share and enhance their profitability in the market. The key players in the market include Vishay Intertechnology Inc., Kemet Corporation (YAGEO Corporation), NIC Components Corp., KYOCERA AVX Components Corporation (KYOCERA CORPORATION), Semec Technology Company Limited.

- In March 2024, Kemet introduced the brand-new T581 polymer tantalum surface-mount capacitors that satisfy the requirements of Military Performance Specification Sheets MIL-PRF-32700/2. This launch signifies the introduction of polymer tantalum surface-mount capacitors to the market, making them the first to meet the new specifications. This further solidifies KEMET's position as a key firm in the defense and aerospace high-reliability application market.

- In November 2023, Vishay Intertechnology Inc. announced that it entered a definitive agreement with Nexperia BV to purchase Nexperia's wafer fabrication plant and operations in the United Kingdom for approximately USD 177 million in cash (subject to customary post-sale adjustments).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3 Value Chain Analysis

- 4.4 Assessment of Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Focus on Miniaturization of Devices

- 5.1.2 Rising In-vehicle Electronics

- 5.2 Market Restrains

- 5.2.1 Fluctuations in the Price of Tantalum ore

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Medical Devices

- 6.1.2 Consumer Electronics

- 6.1.3 Automotive

- 6.1.4 Industrial

- 6.1.5 Other Applications

- 6.2 By Geography

- 6.2.1 Americas

- 6.2.2 Europe, Middle East and Africa

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Japan

- 6.2.6 South Korea

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Vishay Intertechnology Inc.

- 7.1.2 Kemet Corporation (YAGEO Corporation)

- 7.1.3 NIC Components Corp.

- 7.1.4 KYOCERA AVX Components Corporation (KYOCERA CORPORATION)

- 7.1.5 Semec Technology Company Limited

- 7.1.6 Samsung Electro-Mechanics

- 7.1.7 Exxelia Group

- 7.1.8 Abracon LLC

- 7.1.9 Panasonic Corporation

- 7.1.10 NTE Electronics Inc.