世界の鉄骨形鋼市場:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Global Steel Sections - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693695

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

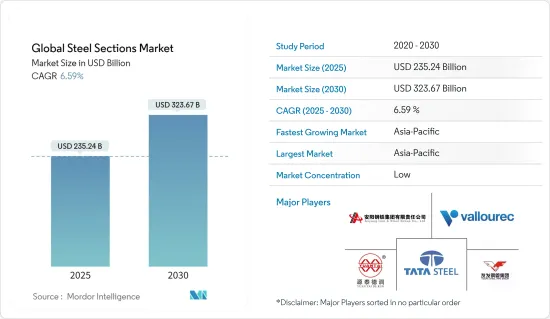

世界の鉄骨形鋼市場規模は、2025年に2,352億4,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは6.59%で、2030年には3,236億7,000万米ドルに達すると予測されています。

主なハイライト

- すべての鉄鋼生産国が加盟する世界鉄鋼協会(World Steel Association)によると、世界の鉄鋼需要は2024年に1.9%成長する見込みです。世界鉄鋼協会の短期予測によると、2024年の需要は1,849.1トンまで増加します。2022年の粗鋼需要は1,831.5トンで、2021年比で4.3%減少すると予測していました。

- 市場開拓の主な要因としては、建設業界からの需要増加、インフラ整備の進展、産業化の進展などが挙げられます。鉄骨形鋼は建設プロジェクトに不可欠な要素であり、建設業界の成長が鉄骨形鋼の需要を牽引すると予想されます。

- 世界各国政府は、道路、橋梁、鉄道などのインフラ開発プロジェクトに多額の投資を行っており、これが鉄骨形鋼の需要を押し上げる可能性が高いです。2023年6月現在、アジア太平洋地域の道路建設プロジェクトへの投資額は2兆3,000億米ドルを超えています。このようなプロジェクトでは、欧州が第2位で、投資額は約7億米ドルでした。

- 2023年の世界の粗鋼生産量は前年比横ばいの18億8,820万トンで、2022年の18億8,870万トンを上回りました。ただし、2023年12月の世界の粗鋼生産量は1億3,570万トンと、前年同期の1億4,330万トンから5.3%減少しました。

- 市場は、原料価格の変動、貿易保護主義、環境規制などの課題に直面しています。環境規制は鉄鋼生産コストを上昇させ、これは鋼材価格の上昇を通じて消費者に転嫁される可能性があります。

世界の鋼材市場動向

地域別では、アジア太平洋地域がより多くの機会で市場をリードする見込み

- アジア太平洋は、いくつかの要因により、鉄骨形鋼の最大の市場です。この地域は、世界的に最も急速に経済成長している地域の一つであり、建設、インフラ、製造業における鋼材需要の急増につながっています。いくつかの情報源によると、この地域の市場は2024年に3.5%から4.0%の成長が予測されています。

- 中国は世界有数の鉄鋼メーカーとなりました。2021年の鉄鋼生産量は9億4,300万トンで、世界総生産量17億5,000万トンの54%を占める。

- 中国の鉄鋼生産の大部分(約85%)は、高炉プロセスによる高炉で行われています。電気炉(EAF)は約15%に過ぎず、鉄スクラップを使用するはるかに「クリーン」なプロセスです。

- 中国の鉄スクラップ供給と国内電力価格は、今後数年間、世界のEAF生産の重要な触媒となる可能性が高いです。中国以外では、EAF生産量が全体の生産量に占める割合がはるかに大きく、北米が約70%、欧州が40%を占めています。気候変動目標を達成するため、世界中でEAFの増産と、よりクリーンなプロセスの開発が推進されています。

- 2022年9月、中国政府は現地製造業のデジタル化と反合法化を加速させる最新の開発計画を発表しました。この動きは、スマート製造業、特に自動車、石油化学、家電、医療機器などの主要産業に利益をもたらします。インテリジェント製造装置産業の規模は3兆人民元近くに達し、市場需要の50%以上を満たしています。

- 2026年以降、中国にあるBMWの自動車工場はHBISグリーン・スチールの使用を開始する予定です。HBISグリーン・スチールは、再生可能な電力でEAFにより生産され、CO2排出量を約95%削減します。この方法により、BMWはサプライチェーン側から年間約23万トンのCO2排出を削減することができます。HBISは、2050年までにカーボンニュートラルを達成するという目標を発表した翌年の2022年3月に、「低炭素開発技術ロードマップ」を発表しました。HBISは、2025年のピーク時から炭素排出量を10%、2030年には30%削減し、2050年にカーボンニュートラルを達成するため、「6つの技術的道筋を模索し、2つの管理プラットフォームを構築する」としています。

住宅セグメントは今後数年で勢いを増すと予想される

- 可処分所得の増加と建築・建設プロジェクトの技術進歩により、鉄骨形鋼市場は今後数年間で安定した成長が見込まれます。市場を牽引する主な要因の1つは、プレハブ部品を使用した先進的な建設手法の採用を奨励することを目的とした建設指標の開発です。

- 鉄骨形鋼は、長距離をまたぐためのエレガントでコスト効率の高い方法を提供します。鉄鋼スパンを延長することで、柱のない開放的な大空間の内部空間を作り出すことができ、現在では多くの顧客が15メートル以上の柱グリッド間隔を要求しています。平屋建ての建物では、圧延梁は50メートル以上の明確なスパンを提供します。

- スチールは、色、テクスチャー、形状の面で、建築家により自由なデザインを提供します。その強度、耐久性、美しさ、精密さ、可鍛性により、建築家はアイデアを探求し、革新的なソリューションを開発するための幅広いパラメーターを得ることができます。スチールの長いスパン能力は、中間柱や耐力壁のない大きなオープンスペースを生み出します。

世界の鉄骨形鋼産業概要

鉄骨形鋼市場は断片化されており、世界の企業だけでなく、地元や地域の企業も複数存在しています。主な企業には、Tata Steel、Vallourec、Yuantai Derun Group、Anyang Steel Group、Youfa Steel Pipe Groupなどがあります。市場は、サプライチェーンの制約や消費者の需要の変化により、多くの変化を経験しています。各社は生産能力の増強と技術進歩による製品の品質向上に取り組んでいます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学

- 現在の市場シナリオ

- 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- バリューチェーン/サプライチェーン分析

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 鉄骨形鋼の技術的進歩

- 各鋼材の生産と需要に関する洞察

- 鉄骨形鋼市場の価格分析

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 製品タイプ別

- 重量構造用鋼

- 軽量構造用鋼

- 鉄筋

- エンドユーザー産業別

- 住宅

- 製造業

- 航空宇宙・自動車

- 電力・公益事業

- 建設

- 石油・ガス

- その他エンドユーザー産業

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- ラテンアメリカ

- ブラジル

- アルゼンチン

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- 企業プロファイル

- Tata Steel

- Vallourec

- Yuantai Derun Group

- Anyang Steel Group

- Youfa Steel Pipe Group

- ArcelorMittal SA

- POSCO Holdings Inc.

- Baoshan Iron & Steel Co. Ltd

- Nippon Steel Corp.

- Nucor Corp.

- Ansteel Group

- Hyundai Steel*

第7章 市場の将来

第8章 付録

目次

The Global Steel Sections Market size is estimated at USD 235.24 billion in 2025, and is expected to reach USD 323.67 billion by 2030, at a CAGR of 6.59% during the forecast period (2025-2030).

Key Highlights

- According to the World Steel Association, a body with membership in every steel-producing country, the demand for steel worldwide is expected to grow by 1.9% in 2024. Based on its short-range forecast, the World Steel Association reported that demand will rise to 1,849.1 mt by 2024. It had projected that the demand for crude steel would reach 1,831.5 mt in 2022, down by 4.3% compared to 2021.

- Some of the key factors driving the market's growth include increasing demand from the construction industry, rising infrastructure development, and growing industrialization. Steel sections are an essential component of construction projects, and the growth of the construction industry is expected to drive the demand for steel sections.

- Governments worldwide are investing heavily in infrastructure development projects, such as roads, bridges, and railways, which will likely boost the demand for steel sections. As of June 2023, Asia-Pacific accounted for more than USD 2.3 trillion of investments in road construction projects. In such projects, Europe ranked second, with investments amounting to around USD 700 million.

- Compared to the previous year, crude steel production worldwide remained unchanged in 2023, with an output of 1,888.2 million ton over 1,888.7 million ton in 2022. However, in December 2023, crude steel production worldwide decreased by 5.3% to 135.7 million ton compared to 143.3 million ton in the same period of the previous year.

- The market is facing some challenges, such as volatility in raw material prices, trade protectionism, and environmental regulations. Environmental regulations are increasing the cost of steel production, which can be passed on to consumers through higher prices for steel sections.

Global Steel Sections Market Trends

By Region, Asia-Pacific is Expected to Lead the Market with More Opportunities

- Asia-Pacific is the largest market for steel sections due to several factors. The region has some of the fastest-growing economies globally, leading to a surge in demand for steel in the construction, infrastructure, and manufacturing industries. According to some sources, the regional market is projected to grow between 3.5% and 4.0% in 2024.

- China has become the world's dominant steel manufacturer. The country produced 943 million metric ton of steel in 2021, 54% of the global total of 1.75 billion metric ton.

- Most (about 85%) of China's steel production is done in blast furnaces using the BOF process. Only about 15% is electric-arc furnace (EAF), the far "cleaner" process that uses scrap steel.

- The country's scrap steel supply and domestic power pricing will likely become key catalysts of EAF production worldwide in the coming years. Outside of China, EAF production accounts for a far greater proportion of the overall output, with North America at about 70% and Europe at 40%. There is a push to build more EAF and develop even cleaner processes to meet climate goals across the world.

- In September 2022, the Chinese government announced its latest development plan to accelerate the digitalization and antilegalization of the local manufacturing industry. This move benefits the smart manufacturing industry, especially key industries like automobiles, petrochemicals, home appliances, and medical devices. The scale of the intelligent manufacturing equipment industry has reached almost CNY 3 trillion, satisfying more than 50% of market demand.

- From 2026, BMW's car plants in China will begin to use HBIS green steel, which is produced via EAF with renewable-source electricity, with CO2 emissions cut by about 95%. This method will allow BMW to remove about 230,000 ton of CO2 emissions per year from the supply chain side. HBIS launched its Low Carbon Development Technology Roadmap in March 2022, a year after it announced the goal of achieving carbon neutrality by 2050. It said it would "explore six technology paths and build two management platforms" to cut carbon emissions by 10% from the peak in 2025 and by 30% in 2030 and achieve carbon neutrality in 2050.

The Residential Segment is Expected to Gain Momentum in the Coming Years

- The steel sections market is expected to grow steadily in the coming years due to rising disposable incomes and technological advancements in building and construction projects. One of the major factors driving the market is the development of a construction index that aims to encourage the adoption of advanced construction methods using prefabricated components.

- Steel sections provide an elegant, cost-effective method of spanning long distances. Extended steel spans can create large, open-plan, column-free internal spaces, with many clients now demanding column grid spacing over 15 meters. In single-story buildings, rolled beams provide clear spans of over 50 meters.

- Steel offers architects more design freedom in terms of color, texture, and shape. Its strength, durability, beauty, precision, and malleability give architects broader parameters to explore ideas and develop innovative solutions. Steel's long-spanning ability gives rise to large open spaces free of intermediate columns or load-bearing walls.

Global Steel Sections Industry Overview

The steel sections market is fragmented, with the presence of several local and regional players, as well as global players. Some of the major players include Tata Steel, Vallourec, Yuantai Derun Group, Anyang Steel Group, and Youfa Steel Pipe Group. The market is going through many changes due to supply chain constraints and a shift in demand among consumers. Companies are working on increasing their production capacities and improving the quality of products through technological advancements.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Market Overview

- 4.3 Market Dynamics

- 4.3.1 Drivers

- 4.3.2 Restraints

- 4.3.3 Opportunities

- 4.4 Value Chain/Supply Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Technological Advancements in Steel Sections

- 4.7 Insights on Production and Demand for Different Steel Sections

- 4.8 Pricing Analysis of the Steel Sections Market

- 4.9 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Product Type

- 5.1.1 Heavy Structural Steel

- 5.1.2 Light Structural Steel

- 5.1.3 Rebar

- 5.2 By End-user Industry

- 5.2.1 Residential

- 5.2.2 Manufacturing

- 5.2.3 Aerospace and Automotive

- 5.2.4 Power and Utilities

- 5.2.5 Construction

- 5.2.6 Oil and Gas

- 5.2.7 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Overview

- 6.2 Company Profiles

- 6.2.1 Tata Steel

- 6.2.2 Vallourec

- 6.2.3 Yuantai Derun Group

- 6.2.4 Anyang Steel Group

- 6.2.5 Youfa Steel Pipe Group

- 6.2.6 ArcelorMittal SA

- 6.2.7 POSCO Holdings Inc.

- 6.2.8 Baoshan Iron & Steel Co. Ltd

- 6.2.9 Nippon Steel Corp.

- 6.2.10 Nucor Corp.

- 6.2.11 Ansteel Group

- 6.2.12 Hyundai Steel*

7 FUTURE OF THE MARKET

8 APPENDIX

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日