|

市場調査レポート

商品コード

1693673

中国の医薬品原薬(API)市場:シェア分析、産業動向、成長予測(2025年~2030年)China Active Pharmaceutical Ingredients (API) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国の医薬品原薬(API)市場:シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 80 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

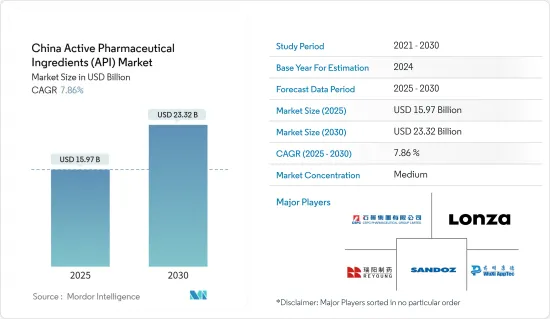

中国の医薬品原薬市場規模は2025年に159億7,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは7.86%で、2030年には233億2,000万米ドルに達すると予測されます。

同市場は、慢性疾患の有病率の増加、予測期間中の生物製剤とバイオシミラーの採用・承認の増加により成長が見込まれています。

中国では慢性疾患、感染症、遺伝性疾患の有病率や発症率が増加しており、効果的で安全な医薬品への需要が高まっています。そのため、さまざまな疾患に対する新薬開発のために、国全体で医薬品原薬に対するニーズが高まっています。このことが、予測期間中の医薬品原薬市場の成長をさらに促進すると予想されています。例えば、2022年3月にChinese Medical Journalに掲載された紙製によると、2022年に中国で新たにがんと診断された患者数は約482万人で、前年は450万人でした。このように、大腸がんを含むがん患者数の増加が予想されることから、治療用の新規薬剤の需要が高まります。このことが、予測期間中のAPI市場の成長を促進すると予想されます。

また、虚血性心疾患、脳卒中、アルツハイマー病などの認知症、慢性閉塞性肺疾患は、国民の障害調整生存年数の4大原因となっています。例えば、2023年6月にBMC Public Healthに掲載された紙製によると、2050年までに中国に住む約4,000万人がアルツハイマー病と関連する認知症に苦しむと予想されています。このように、予想される患者人口の増加は、新規生物学的薬剤の開発の必要性を高め、中国における医薬品原薬の需要を増加させると予想されます。

さらに、生物製剤やバイオシミラーの採用や承認が増加していることも、予測期間中の市場を牽引すると予想されます。世界の医療システムは、コストを削減し収益を上げる方法を積極的に模索しています。革新的な処方箋管理は、患者のケアを犠牲にすることなく処方箋価格を節約する方法を記載しています。専門医薬品は、コスト削減が大きな違いをもたらす顕著なセグメントの一つです。なぜなら、生物製剤のコストが高く、国の医薬品支出全体に不釣り合いな貢献をしているからです。したがって、より安価なバイオシミラーの使用は、患者の転帰を損なうことなく、薬剤費と生物製剤への支出を削減する機会を記載しています。

例えば、2023年10月にHealth Policy誌に掲載された紙製によると、2022年の中国では、がん治療のバイオシミラーのコストは基準薬のコストの69%から90%であり、その普及率は54%から83%に達しました。したがって、バイオシミラーの低コストと臨床上の利点は、その採用を増加させ、最終的に予測期間中の市場を牽引すると予想されます。同様に、2022年6月にBioengineered誌に掲載された紙製で、中国の研究者は、バイオシミラーモノクローナル抗体は中国における研究開発のホットスポットの1つであり、継続的な施策の改善とバイオシミラーの研究開発への関心の高まりがあると観察しています。

このように、バイオ医薬品市場の開拓により、中国におけるバイオシミラーの需要は徐々に拡大すると予想され、国家ガイドラインの改善により、様々な慢性疾患や感染症の治療への採用がさらに増加し、市場の成長に寄与しています。

したがって、慢性疾患の有病率の増加、生物製剤とバイオシミラーの採用・承認の増加といった前述の要因により、予測期間中に市場は成長すると予想されます。しかし、同国の医薬品承認に関する厳しい規制と薬価施策が、予測期間中の市場成長の妨げになると予想されます。

中国の医薬品原薬(API)市場動向

がん領域は高い年間成長率が見込まれる

がん患者の負担増は、中国における主要な医療問題の1つです。がんの罹患率は年齢とともに劇的に上昇するが、これは年齢とともに増加する特定のがんのリスクが蓄積するためと考えられます。したがって、がんの適切な管理が必要であり、それは先進医薬品によって可能となります。このように、様々な種類のがんを管理するための先端医薬品に対するニーズの高まりは、がん治療の最終製剤を製造するための医薬品原薬の需要に拍車をかけると予測されます。

中国ではがん患者の負担が大きいため、がん治療用の革新的な医薬品に対する需要が高まり、予測期間中に産業の拡大が加速すると予測されています。例えば、2023年1月にBMC Cancerに掲載された紙製によると、中国では過去3年間に4,16,371件の乳がんの新規患者が発生しています。このように、がんの有病率の高さは、がん治療用の新薬の需要を促進すると予想され、同国の市場成長を支える可能性が高いです。

さらに、同国では高齢者が増加しており、高齢者層におけるがんの負担が高いことから、予測期間中に同国の市場成長が促進されると予測されています。例えば、2022年12月にScience China Life Sciences Journalが発表した記事によると、中国では高齢者のがんの負担が高くなっています。2022年の高齢者における患者数は279万人で、全人口の55.8%を占めると推定されています。このように、中国の人口におけるがんの負担の増加は、がん管理のための新規薬剤治療に対する旺盛な需要を生み出し、ひいては産業の拡大に拍車をかけると予測されます。

また、さまざまながん治療の開発に注力する企業が増加していることも、医薬品原薬の需要を高め、市場の成長を後押ししています。例えば、2023年12月、AstraZenecaは中国のがん治療企業であるグラセルを12億米ドルで買収しました。この取引は、AstraZenecaの事業の約3分の1を占める中国でのがん研究・治療へのさらなる投資であり、中国での事業拡大を引き続き推進するものです。同様に、グレンマーク社は2024年1月、3Dメディシンズ社と江蘇アルファマブ・バイオファーマシューティカルズ社と提携し、各種がんの治療envafolimabを発売しました。この契約では、江蘇アルファマブがenvafolimabの製造者となります。

したがって、このような契約は予測期間中に産業の拡大に拍車をかけると予測されます。したがって、主要企業による買収や提携などの戦略的活動の増加も、予測期間中のセグメント収益を押し上げると予想されます。

したがって、上記の要因から、中国におけるがん患者の有病率の上昇と主要企業による戦略的活動の増加が予測期間中の市場を牽引すると予想されます。

ブランド医薬品セグメントが大きな市場シェアを占める見込み

ブランド医薬品は通常、特定期間の法的特許保護を受けた革新的な医薬品です。治験薬候補がすべての調査要件を満たすと、特定の疾患領域でブランドとして扱われます。このセグメントの成長は、主にブランド医薬品に対する需要の増加と、ブランド医薬品の製剤化に必要な医薬品原薬を製造するための強固な医薬品原薬製造施設によってもたらされます。さらに、同国における医薬品市場の成長と市場参入企業による様々な戦略的取り組みが、予測期間中のセグメント拡大を促進すると予測されています。

中国は世界の主要医薬品市場のひとつです。そのため、ほとんどの市場参入企業は、ビジネス機会を強化するために、中国と国際市場で製品を発売し、輸出しています。このため、承認、新発売、投資、事業拡大など、製薬企業が実施するさまざまな戦略的取り組みが、同国でのブランド医薬品製造のための医薬品原薬需要を促進すると予測されます。これは、予測期間中のセグメント拡大をサポートすると予測されます。例えば、2024年1月、バイオジェンとエーザイのLeqembiが中国の国家医薬品監督管理局から承認を取得しました。Leqembiはアルツハイマー病の治療に用いられる抗体ベースの治療です。中国がLeqembiを承認したのは米国、日本に続き3カ国目となります。このため、新製品の承認は同国におけるLeqembiの医薬品原薬製造の需要を促進し、予測期間中の市場成長を促進すると予想されます。同様に、世界の製薬企業の中国製薬市場への投資意欲の高まりは、新規治療法の開発に拍車をかけると予想され、その結果、調査期間中の同セグメントの取り込みを促進すると予測されます。例えば、2024年1月、Bayer AGとRTW Investments, LPは、中国のJi Xing Pharmaceuticals Limitedに3,500万米ドルと1億2,700万米ドルを投資しました。この投資は、中国における心血管薬と眼科薬の開発を加速させるために行われました。また、この投資によりBayerAGは中国市場におけるプレゼンスを強化することができました。このように、このような投資はブランド医薬品の開発に大きな期待を抱かせ、ひいては医薬品原薬の需要を促進するものと期待されています。

同セグメントはさらに、市場各社が医薬品原薬生産能力を育成するために行っているいくつかの取り組みからも恩恵を受けると予想されます。例えば、2022年9月、Asymchemは中国江蘇省泰興市に土地を譲渡し、化学原料、低分子医薬品原薬、医薬品の研究開発・生産施設を建設することで合意しました。このような事例により、同国における医薬品原薬製造能力が強化されることが予想され、予測期間中の同セグメントの市場成長に拍車がかかることが期待されます。

このように、上記の要因、ブランド製品に対する需要の増加、成長する医薬品市場、企業によるいくつかの戦略的イニシアティブは、予測期間中にセグメントの拡大を加速させると予想されます。

中国の医薬品原薬(API)産業概要

中国の医薬品原薬市場は比較的セグメント化されています。API市場では、複数のメーカーが提携、施設の拡大、医薬品の承認など様々な事業戦略を採用し、足跡の拡大に注力しています。主要市場参入企業には、CSPC Pharmaceutical Group Limited、WuXi AppTec(WuXi STA)、Lonzaなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場の促進要因

- 慢性疾患の有病率の増加

- 生物製剤とバイオシミラーの採用と承認の増加

- 市場抑制要因

- 薬価統制施策

- 医薬品原薬メーカー間の高い競合と厳しい規制

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- ビジネスモード別

- キャプティブAPI

- マーチャントAPI

- 合成タイプ別

- 合成

- バイオ

- 医薬品タイプ別

- ジェネリック

- ブランド

- 用途別

- 循環器

- 腫瘍学

- 呼吸器内科

- 神経学

- 整形外科

- 眼科

- その他

第6章 競合情勢

- 企業プロファイル

- Teva Pharmaceutical Industries Ltd

- Shenzhen Shengda Pharma Limited

- Jinzhou Pharmaceuticals

- WuXi AppTec

- Sandoz Group AG

- Pfizer Inc.

- Jinan Shengqi Pharmaceutical Co. Ltd

- Reyoung Pharmaceuticals

- Lonza

- CSPC Pharmaceutical Group Limited(Shijiazhuang Pharmaceutical Group Co. Ltd)

第7章 市場機会と今後の動向

The China Active Pharmaceutical Ingredients Market size is estimated at USD 15.97 billion in 2025, and is expected to reach USD 23.32 billion by 2030, at a CAGR of 7.86% during the forecast period (2025-2030).

The market is expected to grow due to the increasing prevalence of chronic disorders and the rising adoption and approval of biologics and biosimilars during the forecast period.

The increasing prevalence and incidence of chronic diseases, infectious diseases, and genetic disorders in China are driving the demand for effective and safe drugs. Thus, the need for active pharmaceutical ingredients across the country is increasing for the development of novel drugs for various diseases. This, in turn, is further expected to fuel the growth of the active pharmaceutical ingredients market during the forecast period. For instance, according to an article published in the Chinese Medical Journal in March 2022, it has been observed that about 4.82 million new cancer cases were diagnosed in China in 2022, compared to 4.5 million cases in the last year. Thus, the expected increase in the number of people who have cancer, including colorectal cancer, raises the demand for novel drugs for the treatment. This, in turn, is anticipated to propel the growth of the APIs market during the forecast period.

Also, ischemic heart disease, stroke, Alzheimer's and other dementias, and chronic obstructive pulmonary disease are the four most frequent causes of disability-adjusted life years among the population. For instance, according to an article published in BMC Public Health in June 2023, it was observed that about 40 million people living in China are expected to suffer from Alzheimer's disease and related dementias by 2050. Thus, the expected increase in the patient population raises the need to develop novel biological drugs, which is expected to increase the demand for APIs in China.

Moreover, the increasing adoption and approval of biologics and biosimilars are expected to drive the market during the forecast period. Healthcare systems worldwide actively seek ways to lower costs and raise revenues. Innovative formulary management provides a way to save prescription prices without sacrificing patient care. Specialty pharmaceuticals are one prominent area in which cost reductions would make a significant difference because of the high cost of biologics, which results in a disproportionate contribution to the total national drug spending. Thus, using less expensive biosimilars offers a chance to reduce drug costs and spending on biologics without compromising patient outcomes.

For instance, according to an article published in Health Policy in October 2023, it was observed that the cost of cancer biosimilars was 69% to 90% of the costs for the reference drugs, and their uptake reached 54% to 83% in China in 2022. Hence, biosimilars' lower cost and clinical benefits are expected to increase their adoption, ultimately driving the market during the forecast period. Similarly, in an article published in Bioengineered in June 2022, the Chinese researchers observed that biosimilar monoclonal antibodies are one of the hotspots of research and development in China, with continuous improvement of policies and increasing interest in research and development of biosimilars.

Thus, owing to the development of biopharmaceuticals markets, the demand for biosimilars in China is expected to grow gradually, with the improvement of the national guidelines, further increasing its adoption for the treatment of various chronic and infectious disorders, contributing to the market growth.

Therefore, the market is expected to grow during the forecast period due to the aforementioned factors, such as the increasing prevalence of chronic diseases and the increasing adoption and approval of biologics and biosimilars. However, the country's stringent regulations for drug approvals and drug price policies are expected to hinder market growth during the forecast period.

China Active Pharmaceutical Ingredients (API) Market Trends

The Oncology Segment is Expected to Register a High Annual Growth Rate

The growing burden of cancer cases is one of the primary healthcare concerns in China. The incidence of cancer rises dramatically with age, most likely due to a build-up of risks for specific cancers that increase with age. Hence, there should be proper management of cancer, which is possible with advanced medicines. Thus, the growing need for advanced medicines for the management of various types of cancers is projected to spur the demand for APIs to manufacture finished dosage forms of cancer medicine.

The significant burden of cancer cases in China is projected to foster demand for innovative medicines for cancer treatment, which is, in turn, projected to accelerate industry expansion during the forecast period. For instance, according to an article published in BMC Cancer in January 2023, there were 4,16,371 new cases of breast cancer in China over the last three years. Thus, the high prevalence of cancers is expected to drive the demand for new medicines for cancer treatment, which will likely support the country's market growth.

In addition, the increasing geriatric population in the country and a higher burden of cancer in the elderly population are projected to foster the country's market growth during the forecast period. For instance, according to an article published by the Science China Life Sciences Journal in December 2022, the burden of cancer among the geriatric population was higher in China. It is estimated that there were 2.79 million cases in older people, representing 55.8% of the overall population in 2022. Thus, the escalating burden of cancer among the Chinese population is anticipated to create a robust demand for novel drug therapies for cancer management, which, in turn, is projected to spur industry expansion.

Also, the rising company focus on developing various cancer-treating drugs raises the demand for APIs, propelling the market growth. For instance, in December 2023, AstraZeneca acquired Gracell, a Chinese cancer therapy firm, for USD 1.2 billion. The deal marks a further investment in cancer research and treatment in China, accounting for about one-third of AstraZeneca's business and its continued push to expand in China. Similarly, in January 2024, Glenmark Pharmaceuticals partnered with 3D Medicines and Jiangsu Alphamab Biopharmaceuticals to launch envafolimab to treat various types of cancers. Under this agreement, Jiangsu Alphamab is the manufacturer of envafolimab.

Thus, such agreements are projected to spur industry expansion during the forecast period. Hence, increasing strategic activities, such as acquisitions and collaborations by key players, are also expected to drive the segment revenue during the forecast period.

Therefore, owing to the above-mentioned factors, the rising prevalence of cancer cases in China and increasing strategic activities by key players are expected to drive the market during the forecast period.

The Branded Drugs Segment is Expected to Hold Significant Market Share

Branded drugs are usually innovative pharmaceuticals with legal patent protection for a specific period. When any investigational candidate fulfills all the research requirements, it is represented as a brand for a specific disease area. The segment growth is mainly driven by the increasing demand for branded medicines and robust API manufacturing facilities to manufacture the API required for the formulation of branded pharmaceuticals. In addition, the growing pharmaceutical market in the country and various strategic initiatives undertaken by market players are further projected to foster segment expansion during the forecast period.

China is one of the major pharmaceutical markets in the world. Hence, most market players launch and export their products in Chinese and international markets to strengthen their business avenues. Thus, various strategic initiatives undertaken by pharmaceutical companies, such as approvals, new launches, investments, and business expansions, are projected to foster demand for APIs to manufacture branded medicines in the country. This is projected to support segment expansion during the forecast period. For instance, in January 2024, Biogen and Eisai's Leqembi received approval from China's National Medical Products Administration. Leqembi is the antibody-based therapeutics used in the treatment of Alzheimer's disease. China has become the third country to approve Leqembi, following the United States and Japan. Thus, the approval of the new product is expected to propel the demand for Leqembi's API production in the country, which is expected to foster market growth during the forecast period. Similarly, the increased efforts of global pharmaceutical players to invest in the Chinese pharmaceutical market are expected to spur the development of novel therapies, which, in turn, are projected to fuel segment uptake over the study period. For instance, in January 2024, Bayer AG and RTW Investments, LP invested USD 35 million and 127 million in Ji Xing Pharmaceuticals Limited of China. This investment was made to accelerate the development of cardiovascular and ophthalmology medicines in China. In addition, this investment allowed Bayer AG to strengthen its presence in the Chinese market. Thus, such investments are expected to hold a strong promise for the development of branded medicines, which, in turn, is expected to foster the demand for APIs.

The segment is further expected to benefit from several efforts undertaken by market players to foster API production capabilities. For instance, in September 2022, Asymchem agreed to transfer land in Taixing, Jiangsu Province, China, to construct a proposed R&D and production facility for chemical raw materials, small-molecule APIs, and drug products. Thus, such instances are expected to strengthen API manufacturing capabilities in the country, which is expected to spur segment market growth during the forecast period.

Thus, the above-mentioned factors, increasing demand for branded products, growing pharmaceutical markets, and several strategic initiatives undertaken by companies are expected to accelerate segment expansion during the forecast period.

China Active Pharmaceutical Ingredients (API) Industry Overview

The Chinese active pharmaceutical ingredients market is relatively fragmented. The API market has several manufacturers focusing on expanding their footprints by adopting various business strategies, such as collaborations, facility expansion, and drug approvals. Some key market players include CSPC Pharmaceutical Group Limited (Shijiazhuang Pharmaceutical Group Co. Ltd), WuXi AppTec (WuXi STA), and Lonza.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope Of The Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Chronic Disorders

- 4.2.2 Increasing Adoption and Approval of Biologicals and Biosimilars

- 4.3 Market Restraints

- 4.3.1 Drug Price Control Policies

- 4.3.2 High Competition Between API Manufacturers and Stringent Regulations

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Business Mode

- 5.1.1 Captive API

- 5.1.2 Merchant API

- 5.2 By Synthesis Type

- 5.2.1 Synthetic

- 5.2.2 Biotech

- 5.3 By Drug Type

- 5.3.1 Generic

- 5.3.2 Branded

- 5.4 By Application

- 5.4.1 Cardiology

- 5.4.2 Oncology

- 5.4.3 Pulmonology

- 5.4.4 Neurology

- 5.4.5 Orthopedic

- 5.4.6 Ophthalmology

- 5.4.7 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Teva Pharmaceutical Industries Ltd

- 6.1.2 Shenzhen Shengda Pharma Limited

- 6.1.3 Jinzhou Pharmaceuticals

- 6.1.4 WuXi AppTec

- 6.1.5 Sandoz Group AG

- 6.1.6 Pfizer Inc.

- 6.1.7 Jinan Shengqi Pharmaceutical Co. Ltd

- 6.1.8 Reyoung Pharmaceuticals

- 6.1.9 Lonza

- 6.1.10 CSPC Pharmaceutical Group Limited (Shijiazhuang Pharmaceutical Group Co. Ltd)