|

市場調査レポート

商品コード

1693651

欧州の電気自動車:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Electric Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の電気自動車:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 290 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

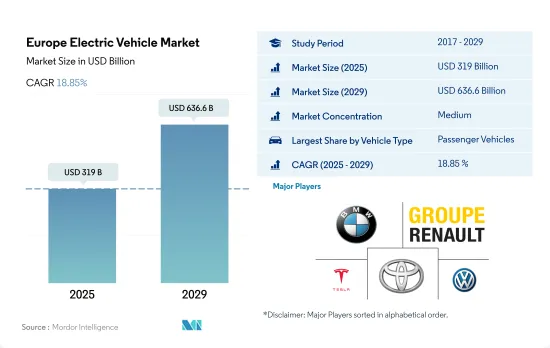

欧州の電気自動車市場規模は2025年に3,190億米ドルと推定され、2029年には6,366億米ドルに達すると予測され、予測期間中(2025-2029年)のCAGRは18.85%で成長する見込みです。

ロジスティクス、サプライチェーン、インフラ、建設分野の成長と公共輸送サービスの増加が欧州EV市場を強化

- 商用車の需要は、今後数年間で大幅に増加します。この成長の主な原動力は、物流、サプライチェーン、インフラ、建設部門などです。また、公共交通機関の増加もバス需要を押し上げています。しかし、商用車の販売は、パンデミックの影響などにより、2020年には低迷しました。市場は2021年に急速に回復し、欧州の気候計画が極めて重要な役割を果たしました。欧州では2030年までにディーゼルエンジン車を禁止することを目標としているため、業務用消費者の間で電気商用車への顕著なシフトが見られると予想されます。

- 欧州全域で、現代自動車とH2エナジーの提携のような新製品の導入や戦略的提携が、電気トラックの販売を促進する態勢を整えています。この提携により、スイスと欧州でグリーン水素エコシステムを育成するというビジョンを掲げて、2019年9月にヒュンダイ・ハイドロジェン・モビリティ(HHM)が誕生しました。HHMは2025年までに1,600台の燃料電池電気大型トラックを導入するという野心的な目標を掲げています。このような取り組みにより、2024年から2030年にかけて、欧州での大型電気トラックの販売に弾みがつくと期待されています。

- 2021年、ドイツの公共交通部門における電気バスの数はほぼ倍増し、新規登録台数は前年の689台から60%急増し、1,269台に達しました。そのうち586台がバッテリー式電気自動車で、燃料電池式やその他の技術を利用したものはほんの一握りでした。さらに、ドイツの地方交通会社と政府機関はともに、2025年までに3,000台以上のEバスを増やす計画を持っています。他の欧州諸国における同様の動向は、2024年から2030年にかけての欧州の商用車市場全体を牽引するものと思われます。

欧州の電気自動車市場は、インセンティブ、インフラ、消費者の嗜好の違いを反映した国レベルのばらつきが特徴です。

- 欧州は世界最大の電気自動車メーカーのひとつです。世界的にみても、電気モビリティの導入が最も早い国のひとつです。電気自動車に関しては、2023年に同地域全体で新規登録された乗用車のうち、完全電気自動車が8.3%を占め、最大のシェアを占めています。ガソリン車は、ほとんどの国で2030年と2035年までに禁止されると予想されており、電気自動車の販売に弾みをつけています。

- 新製品の発売と新ブランドの参入が、欧州の乗用車市場を牽引すると予想されます。2022年2月、中国の自動車メーカーXpengが電気自動車P7とP5セダンをデビューさせ、スウェーデンの電気乗用車に参入しました。2022年6月、米国の自動車メーカーであるフォードは、2030年までに欧州で電気自動車のみを生産・販売すると発表しました。同社はスペインのバレンシアにある製造工場で電気自動車を生産するために114億米ドルを投資する予定です。

- リベートや補助金といった政府の取り組みもあり、欧州各国では電気自動車の普及が進んでいます。例えば、2023年には、新車のバッテリー電気自動車には2,950ユーロ、中古のバッテリー電気自動車には約2,000ユーロの補助金が支給されるようになりました。ただし、車両価格は最低12,000ユーロ、最高45,000ユーロでなければならないです。このような利点は、顧客の関心を電気自動車に引きつけるため、2024年から2030年にかけて、欧州諸国ではさまざまなタイプの電気自動車の需要が高まると予想されます。

欧州の電気自動車市場の動向

環境問題、政府の支援、脱炭素化目標が欧州の電気自動車需要と販売に拍車をかける

- 欧州諸国における電気自動車の需要と販売は、ここ数年で大きく伸びています。ドイツは2022年に電気自動車の販売台数が2021年比で22%増加し、次いで英国が2022年に2021年比で18.40%増加しました。環境問題への関心の高まり、政府の厳しい規範、燃費の良さ、サービスコストの低さ、二酸化炭素排出量の少なさといった電気自動車の利点、政府による補助金などが、欧州諸国における電気自動車の成長に寄与している要因のひとつです。

- 電気商用車、特に小型トラックの需要は、欧州諸国で徐々に伸びています。さらに、各国の政府も電気自動車の導入を支援しています。2021年11月、英国政府は2040年までにすべての大型車をゼロ・エミッションにするという公約を発表しました。このような要因により、英国における2022年の電気商用車販売台数は2021年比で23.17%増加し、各国の同様の慣行が欧州全域で電気商用車の需要を高めています。

- 欧州諸国における車両の電動化は、今後数年間で飛躍的に成長すると予測されています。脱炭素化に向けた各国政府の取り組みが、欧州の電気商用車市場を牽引すると予想されます。例えば、2022年1月、ドイツの運輸大臣は、2030年までに1,500万台の電気自動車を走らせるという目標を発表しました。このような要因により、欧州諸国では2024年から2030年にかけて電気自動車の販売が増加すると予想されます。

欧州の電気自動車産業の概要

欧州の電気自動車市場は適度に統合されており、上位5社で43.69%を占めています。この市場の主要企業は以下の通り。 Bayerische Motoren Werke AG, Groupe Renault, Tesla Inc., Toyota Motor Corporation and Volkswagen AG(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 人口

- 一人当たりGDP

- 自動車購入のための消費者支出(cvp)

- インフレ率

- 自動車ローン金利

- シェアライド

- 電動化の影響

- EV充電ステーション

- バッテリーパック価格

- Xev新モデル発表

- 中古車販売

- 燃料価格

- OEM生産統計

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 車両タイプ

- 商用車

- 乗用車

- ハッチバック

- 多目的車

- セダン

- SUV

- 二輪車

- 燃料カテゴリー

- BEV

- FCEV

- HEV

- PHEV

- 国名

- オーストリア

- ベルギー

- チェコ共和国

- デンマーク

- エストニア

- フランス

- ドイツ

- アイルランド

- イタリア

- ラトビア

- リトアニア

- ノルウェー

- ポーランド

- ロシア

- スペイン

- スウェーデン

- 英国

- その他欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Audi AG

- Bayerische Motoren Werke AG

- Groupe Renault

- Hyundai Motor Company

- Kia Corporation

- Mercedes-Benz

- Tesla Inc.

- Toyota Motor Corporation

- Volkswagen AG

- Volvo Car AB

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 93039

The Europe Electric Vehicle Market size is estimated at 319 billion USD in 2025, and is expected to reach 636.6 billion USD by 2029, growing at a CAGR of 18.85% during the forecast period (2025-2029).

The growing logistics, supply chain, infrastructure, and construction sectors and the rise in public transportation services are bolstering the European EV market

- The demand for commercial vehicles is set to witness a significant uptick in the coming years. Key drivers of this growth include the logistics, supply chain, infrastructure, and construction sectors. Additionally, a rise in public transportation services is bolstering the demand for buses. However, the sales of commercial vehicles experienced a downturn in 2020, largely due to the impact of the pandemic. The market swiftly rebounded in 2021, with Europe's Climate Plan playing a pivotal role. As Europe aims to ban diesel-powered vehicles by 2030, a notable shift is expected to be witnessed among business consumers toward electric commercial vehicles.

- Across Europe, the introduction of new products and strategic collaborations, such as the partnership between Hyundai Motor Company and H2 Energy, are poised to drive sales of electric trucks. This collaboration produced Hyundai Hydrogen Mobility (HHM) in September 2019 with a vision to foster a green hydrogen ecosystem in Switzerland and Europe. HHM has set an ambitious target of introducing 1,600 fuel-cell electric heavy-duty trucks by 2025. Such initiatives are expected to fuel the sales of heavy electric trucks in Europe from 2024 to 2030.

- In 2021, the number of electric buses in Germany's public transport sector nearly doubled, with new registrations surging by 60% to reach 1,269, up from 689 in the previous year. Of these, 586 were battery electric vehicles, while only a handful was fuel cell-powered or utilized other technologies. Furthermore, both local transport companies and government bodies in Germany have plans to add over 3,000 e-buses by 2025. Similar trends in other European nations are poised to propel the overall commercial vehicle market in Europe from 2024 to 2030.

The European electric vehicles market is characterized by country-level variations, reflecting differing incentives, infrastructure, and consumer preferences

- Europe is one of the largest electric vehicle manufacturers globally. Globally, it has one of the fastest adoptions of electric mobility. In terms of electric vehicles, sales of electric passenger cars accounted for the largest share of 8.3% of all newly registered cars across the region in 2023, which were fully electric. Gasoline-powered vehicles are expected to be banned by 2030 and 2035 in most countries, providing a boost to the sales of electric vehicles.

- The launch of new products and the entry of new brands are expected to drive the market for passenger cars in Europe. In February 2022, the Chinese automaker Xpeng entered Sweden's electric passenger cars with its debut electric cars, P7 and P5 sedans. In June 2022, the American automaker Ford announced that it would produce and sell only electric cars in Europe by 2030. The company plans to invest USD 11.4 billion in producing an electric car at a manufacturing plant in Valencia, Spain.

- Several government efforts in terms of rebates and subsidies are increasing the adoption of electric vehicles in various European countries. For instance, in 2023, a subsidy of EUR 2,950 was made eligible for new battery electric cars and a subsidy of around EUR 2,000 for used battery electric cars. However, the price of the vehicles should be a minimum of EUR 12,000 and a maximum of EUR 45,000. Such advantages attract customer attention to these vehicles, which is expected to enhance the demand for various types of electric vehicles in European countries from 2024 to 2030.

Europe Electric Vehicle Market Trends

Environmental concerns, government support, and decarbonization goals fuel European electric vehicle demand and sales

- The demand and sales of electric vehicles in European countries have grown significantly over the past few years. Germany witnessed a growth in the sales of electric cars by 22% in 2022 over 2021, followed by the United Kingdom with an 18.40% increase in 2022 over 2021. Growing environmental concerns, stringent governmental norms, advantages of electric vehicles such as fuel efficiency, low service cost, no carbon emissions, and subsidies by the government are some of the factors contributing to the growth of electric vehicles in European countries.

- The demand for electric commercial vehicles, especially light trucks, is growing gradually in European countries. Moreover, the governments of various countries are also supporting the adoption of electric vehicles. In November 2021, the government of the United Kingdom announced a pledge that all heavy-duty vehicles would be zero-emission by the year 2040. Such factors have increased the sales of electric commercial vehicles in the United Kingdom by 23.17% in 2022 over 2021, and similar practices in various countries are enhancing the demand for electric commercial vehicles across Europe.

- It is projected that the electrification of vehicles in European countries is expected to grow tremendously in the next few years. The efforts of the governments in the regions for decarbonization are expected to drive the electric commercial vehicle market in Europe. For instance, in January 2022, the transport minister of Germany announced a goal to put 15 million electric vehicles on the road by 2030. Such factors are expected to increase the sales of electric vehicles during the 2024-2030 period in European countries.

Europe Electric Vehicle Industry Overview

The Europe Electric Vehicle Market is moderately consolidated, with the top five companies occupying 43.69%. The major players in this market are Bayerische Motoren Werke AG, Groupe Renault, Tesla Inc., Toyota Motor Corporation and Volkswagen AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Shared Rides

- 4.7 Impact Of Electrification

- 4.8 EV Charging Station

- 4.9 Battery Pack Price

- 4.10 New Xev Models Announced

- 4.11 Used Car Sales

- 4.12 Fuel Price

- 4.13 Oem-wise Production Statistics

- 4.14 Regulatory Framework

- 4.15 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Commercial Vehicles

- 5.1.2 Passenger Vehicles

- 5.1.2.1 Hatchback

- 5.1.2.2 Multi-purpose Vehicle

- 5.1.2.3 Sedan

- 5.1.2.4 Sports Utility Vehicle

- 5.1.3 Two-Wheelers

- 5.2 Fuel Category

- 5.2.1 BEV

- 5.2.2 FCEV

- 5.2.3 HEV

- 5.2.4 PHEV

- 5.3 Country

- 5.3.1 Austria

- 5.3.2 Belgium

- 5.3.3 Czech Republic

- 5.3.4 Denmark

- 5.3.5 Estonia

- 5.3.6 France

- 5.3.7 Germany

- 5.3.8 Ireland

- 5.3.9 Italy

- 5.3.10 Latvia

- 5.3.11 Lithuania

- 5.3.12 Norway

- 5.3.13 Poland

- 5.3.14 Russia

- 5.3.15 Spain

- 5.3.16 Sweden

- 5.3.17 UK

- 5.3.18 Rest-of-Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Audi AG

- 6.4.2 Bayerische Motoren Werke AG

- 6.4.3 Groupe Renault

- 6.4.4 Hyundai Motor Company

- 6.4.5 Kia Corporation

- 6.4.6 Mercedes-Benz

- 6.4.7 Tesla Inc.

- 6.4.8 Toyota Motor Corporation

- 6.4.9 Volkswagen AG

- 6.4.10 Volvo Car AB

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms